-

Something’s Brewing in China

Posted by Eddy Elfenbein on February 15th, 2010 at 11:09 amGoldman’s chief economist, Jim O’Neill, thinks China is about to revalue its currency by as much as 5%. This would be a huge deal.

For the second time, China has ordered its banks to increase their reserves. The country is desperately trying to contain bank lending which is skyrocketing. Consider that in January alone, banks used up nearly one-fifth of this year’s lending target.

For the last 18 months, China has firmly kept the yuan in place, but the cracks are starting to show. Their export market is booming and assets continue to inflate. Most importantly, the rest of the world isn’t happy with Beijing.

If China did revalue the yuan, it would help cool off their economy, and it would help our economy which is something we desperately need.

Why have the Chinese been so stringent? Let’s say you’re a communist official in Beijing. Which choice would you rather face? A) Millions of unemployed young men in your central cities. B) Anything that’s not A.

Now you get the idea. The migration of people from rural China to their major cities isn’t merely big, it’s the largest migration in human history. Think of Tom Joad, now multiply that by 100. -

Looking at the Fed’s Exit Strategy

Posted by Eddy Elfenbein on February 15th, 2010 at 9:49 amSince the financial crisis began, the Federal Reserve has exploded its balance sheet from less than $1 trillion to over $2.2 trillion. Last week, Ben Bernanke discussed the Fed’s exit strategy. James Hamilton has an interesting take on what the Fed plans. Essentially, all of the strategies boil down to one thing—borrowing from the public.

As Arnold Kling has noted, the Fed is doing something very different here. It’s moving away from its basic function of being a central bank:The Fed should be engaging in ordinary open market operations, which means buying Treasuries. The only reason to buy anything other than Treasuries would be if it ran out of Treasuries to buy and still could not meet its overall target–whether that target is for the money supply, nominal GDP, or some weighted average of inflation and unemployment.

When the Fed instead is selling Treasuries or paying interest on reserves in order to sterilize the effect of buying other stuff, it is not being a central bank. It is being a piggy bank. -

Odd Lots

Posted by Eddy Elfenbein on February 12th, 2010 at 3:06 pmPoll: 79% of Democrats support “gays” in the military, but only 44% of Democrats support “homosexuals” in the military.

Senator Kudlow?

Ignore anyone who tells you that debt levels don’t matter.

36 songs that use the same 4 chords

Superbowl team: online finance’s best I’m honored to have been named a Defensive Coach along with many outstanding blogs.

Adam Corolla – Businessman

Marijuana Farm Found Inside UK Bank -

Quote of the Day

Posted by Eddy Elfenbein on February 12th, 2010 at 10:43 amFrom Arnold Kling: “The Fed has changed from a central bank to a piggy bank.”

-

Wright Express Beats By Two Cents

Posted by Eddy Elfenbein on February 12th, 2010 at 10:39 amOn Wednesday, Wright Express (WXS), one of the new stocks on this year’s Buy List, reported Q4 earnings, after costs, of 56 cents a share which was two cents higher than estimates. For 2009, net income pre share rose to $2.18 from $1.88 last year.

On the earnings call, this is what they had to say about future projections:For the first quarter of 2010 we expect to report revenues in the range of 82 to $87 million. This is based on an average retail sales price of $2.78 per gallon. For the full year 2010, we expect revenues ranging from 360 to $370 million based on an average retail sales price of $2.80 per gallon.

In terms of earnings for Q1 of 2009 we expected to report adjusted net income in the range of $21 to $23 million or $0.53 to $0.58 per diluted share. We expected adjusted net income for the full year 2010 in the range of 89 to $97 million or $2.26 to $2.46 per diluted share and approximately 39 million shares outstanding.If we take $2.36 as the midpoint, that means the stock is going for about 12 times this year’s earnings. The stock dropped initially on the news but rallied back yesterday. So far, it’s our biggest loser of the year.

-

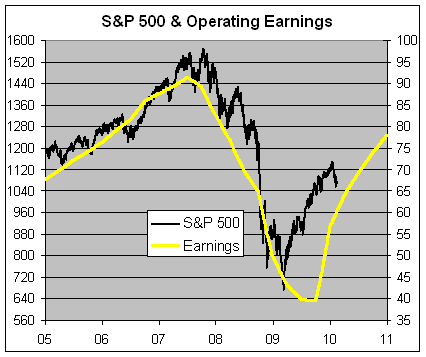

The S&P’s P/E Ratio Falls to 18

Posted by Eddy Elfenbein on February 12th, 2010 at 9:13 amWith the recent dip in the stock market, the P/E Ratio of the S&P 500 is now down to 18. That number, however, is a bit misleading since earnings are still in the process of recovering from a nasty downturn.

Here’s a look at the S&P 500 (left scale) along with its earnings line (right scale). The two scales are plotted at a ratio of 16-to-1 so when the lines cross, the P/E Ratio is exactly 16. The future earnings line is S&P’s estimate.

The total earnings for 2009 will be about $57. Bear in mind that at one point, Goldman Sachs thought that it would be $40. I still think stocks are a good buy, but this is an instance where looking at the P/E ratio doesn’t tell us much. The recent earnings trend is such an outlier. Naturally, if the earnings forecast holds up, then I would expect stocks to be much higher one year from now.

Remember that stocks are best measured by their alternatives. In this case, I think the more telling metric isn’t the Price/Earnings, but the yield curve. The spread between the 30-year T-bond the 90-day T-bill is over 450 basis points, which is gigantic. Even at 5-years out, a Treasury only offers a yield of about 2.3%. With the kind of competition, stocks are the best investment. -

Unraveling the Profit Puzzle at Goldman Sachs

Posted by Eddy Elfenbein on February 12th, 2010 at 9:10 am -

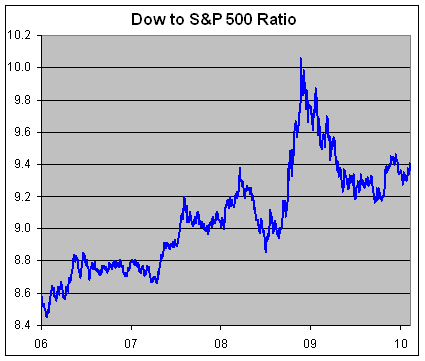

Despite 10,000, the Dow Has Been Beating the S&P 500

Posted by Eddy Elfenbein on February 9th, 2010 at 11:48 amYesterday, the Dow closed below 10,000 for the first time in three month. As far as indexes go, I’m not a big fan of the price-weighted Dow. The cap-weighted S&P 500 is far superior.

Still, I will give the Dow credit for beating the S&P 500 over the past four years. Here’s a look at the Dow/S&P 500 Ratio:

For two days in November 2008, the ratio closed above 10. Before that, the ratio had last been above 10 in 1966. -

Goldman Goes A-Blogging

Posted by Eddy Elfenbein on February 9th, 2010 at 11:00 amGoldman Sachs’ spokesman, Lucas van Praag, responds to the NYT’s article at the Huffington Post. Here’s a sample:

NYT assertion: “Goldman’s demands for billions of dollars from the insurer helped put it in a precarious financial position by bleeding much-needed cash.”

The facts: Relative to the size of AIG’s overall business, Goldman Sachs was a small counterparty. We don’t believe our marks were “aggressive,” they reflected market prices at the time. We requested the collateral we were entitled to under the terms of our agreements. The idea that AIG collapsed because of our marks is not credible. In any event, the story later asserts that, by the spring of 2008, AIG’s dispute with Goldman Sachs was just one of its many woes.

NYT assertion: “In addition, according to two people with knowledge of the positions a portion of the $11 billion in taxpayer money that went to Societe Generale, a French bank that traded with A.I.G, was subsequently transferred to Goldman under a deal the two banks had struck.”

The facts: The assertion is false and misleading. Goldman Sachs provided financing to many counterparties, but in that role we would not have known whether a counterparty had obtained credit default protection, let alone from whom or in what amount.(HT: Felix)

-

The Geography of a Recession

Posted by Eddy Elfenbein on February 8th, 2010 at 2:02 pm

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His