-

The State of Macro

Posted by Eddy Elfenbein on September 4th, 2009 at 10:31 amPaul Krugman has a very good article in the New York Times on the state of macroeconomics and how the profession got blindsided by the credit crisis. As an economics writer, there simply isn’t anyone better at bringing complex issues to the average reader. As a partisan political writer, well, that’s a different matter.

I only have two minor quibbles. The first is that I think Krugman overstates the importance that economic ideas have on theory. Just because a lot of professors who write in journals and show up at conferences believe in efficient markets doesn’t mean that impacts policy at all. That’s a tough line to draw from theory to results.

The second point is that I think he overstates the faith in efficient markets. I could be wrong here, but I’ve rarely met a trader of professional investors who believes in, or even cares about, efficient markets. Krugman makes it sounds as if this were a widely held doctrine that was suddenly exposed by the housing bubble. For many economists, that could be correct. I would think the tech bubble, which Krugman doesn’t mention, was a better refutation of efficient markets.

Anyway, those are minor points. It’s a good read. -

Most Folks Trade Too Much

Posted by Eddy Elfenbein on September 4th, 2009 at 10:13 amWise words from David Merkel:

Most people and investment managers trade too often. They sell their winners too rapidly, and panic too soon on their losers. Now, I’m not advocating “buy and forget,” or Buffett’s statement, “Our favorite holding period is forever.” Buffett has had a huge opportunity loss on many of his “permanent” holdings. Granted, when you are managing that much money, it is tough, so I give him a pass, not that he needs it from me. (Rather, I am the needy one. If you ever read me, Mr. Buffett, sir, would you send me an e-mail? I have one favor to ask.)

Measure twice, cut once. Risk control is best done on the front end, analyzing what you will buy, rather than having strict sell rules that limit losses. Many who have strict sell rules die the death of a thousand cuts. Careful selection matters more, in my opinion. What should you aim for at present?

* A strong balance sheet

* Cheap price versus earnings and book

* An industry that is needed even in bad times.

* Earnings quality — low earnings from accrual entries.You can also check out David’s list of buy candidates.

-

The Market and Future Earnings

Posted by Eddy Elfenbein on September 2nd, 2009 at 11:17 amI was playing with some numbers I got off Robert Shiller’s website. I was curious to see historically how long it’s taken the market to earn back its value. The P/E ratio is concerned with past earnings, but I wanted to see how good the market is at valuing future earnings.

It turns out, the market is generally worth about its earnings for the next 40 quarters, or 10 years. This makes sense since the historic P/E ratio is around 14-16, so going by normal growth, it ought to take roughly ten years to earn your money back. Let me add that the market has been known to be wrong about such things.

Here’s a look at the S&P 500 compared with its earnings ten years hence. Because of that restriction, the chart has to stop in the late 1990s.

From the 1929 peak, it took the market 24 years to earn its money back. In 1942 and 1982, it took less than seven years. -

Morning News

Posted by Eddy Elfenbein on September 2nd, 2009 at 10:47 amI’m relieved to see that Donaldson (DCI) has come off its rotten open from this morning. This is typical after bad news—a sharply lower open followed by a rally. Let’s hope it holds.

Danaher (DHR) is in the news today. The company said it’s cutting 3,300 jobs and it will close 30 facilities which more than previously planned. The company also said it’s paying $1.1 billion for MDS’s instruments business. The shares are up today.

Joe Bank (JOSB) is also doing nicely today. The company just reported earnings of 68 cents a share, 14 cents better than estimates. Sales were up close to 10%. A year ago, the company earned 48 cents a share so that’s very nice growth. This stock is insanely erratic, but it’s been good to us this year. JOSB is up over 70% since January 1. -

Donaldson’s Earnings Report

Posted by Eddy Elfenbein on September 1st, 2009 at 11:26 pmOur filtration company, Donaldson (DCI), released pretty bad earnings after the close. For their fiscal fourth quarter, Donaldson made 35 cents a share which was five cents better than estimates but still down from 60 cents a year ago. Sales dropped over 30%.

More bad news is that the company sees fiscal 2010 EPS ranging between $1.44 and $1.64 which is less than Wall Street was expecting. I’m afraid that the stock is too high right now. -

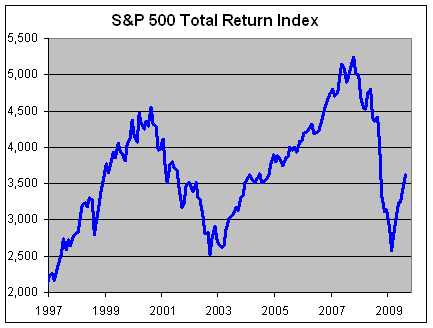

S&P 500 Total Return Index

Posted by Eddy Elfenbein on September 1st, 2009 at 11:05 pmForget talk of a V-shaped or W-shaped economy, we’ve had an M-shaped market for the last several years. Here’s the S&P 500 total return index since 1997:

Through Monday, the S&P 500 is up 14.97% this year including dividends. -

Altria Yields 7.5%

Posted by Eddy Elfenbein on September 1st, 2009 at 12:35 pmI really like shares of Altria (MO) and it’s probably a good candidate for next year’s Buy List. The stock is going for about 10 times this year’s earnings. The company just raised its quarterly dividend by two cents a share to 34 cents. That works out to an increase of 6.25%, and a yearly dividend payment of $1.36 comes to a yield of 7.5%.

I’ve also been impressed by the recent earnings trend. For Q2, Altria earned 50 cents a share, three cents better than expectations. The company also raised its 2009 EPS outlook for continuing ops to a range of $1.51 to $1.56 from the earlier range of $1.47 to $1.52. The net EPS range increased to $1.72 to $1.77 from $1.70 to $1.75, hence the roughly 10 times earnings I mentioned before. -

Bernie’s Beach House Up for Sale

Posted by Eddy Elfenbein on September 1st, 2009 at 10:25 am

If you’re in the market for some beach front property, Bernie Madoff’s crib in Montauk is up for sale. The Feds are asking for $8.75 million. I should warn you that the AP said it’s “not that palatial.” -

A Real Cash Cow

Posted by Eddy Elfenbein on September 1st, 2009 at 10:06 am

Looking to find a higher yield? French savers are turning to cows. I’m serious.Pierre Marguerit, director of Gestel, a company in southeastern France that manages some 30,000 animals on behalf of 1,000 investors, said sales have doubled in the past year.

“You buy one or more cows, which are rented out to professional farmers. Your herd then increases as the years go by. A herd of 20 cows will bring you one extra cow every year, that’s roughly 4-5 percent,” said Marguerit.

Although the birth rate within the herd is higher, a portion of the offspring will make up for deaths, while others are sold off to cover the costs of rearing the animals.

However, in a particularly fertile year, the net increase can run as high as 7 percent.

Investors can choose to sell the new cows and take the cash, or allow their herd to build up over the years by keeping the offspring, then draw a regular income at retirement. -

U.S. Libor Drops to Record Low

Posted by Eddy Elfenbein on September 1st, 2009 at 9:59 amHow things have changed. Last October 10, the three-month Libor hit 4.8%. Now it’s down to 0.33%. The TED spread has plunged as well.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His