-

Thanks Ben!

Posted by Eddy Elfenbein on August 12th, 2009 at 3:15 pmHere’s the latest statement from the FOMC:

Information received since the Federal Open Market Committee met in June suggests that economic activity is leveling out. Conditions in financial markets have improved further in recent weeks. Household spending has continued to show signs of stabilizing but remains constrained by ongoing job losses, sluggish income growth, lower housing wealth, and tight credit. Businesses are still cutting back on fixed investment and staffing but are making progress in bringing inventory stocks into better alignment with sales. Although economic activity is likely to remain weak for a time, the Committee continues to anticipate that policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability.

The prices of energy and other commodities have risen of late. However, substantial resource slack is likely to dampen cost pressures, and the Committee expects that inflation will remain subdued for some time.

In these circumstances, the Federal Reserve will employ all available tools to promote economic recovery and to preserve price stability. The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period. As previously announced, to provide support to mortgage lending and housing markets and to improve overall conditions in private credit markets, the Federal Reserve will purchase a total of up to $1.25 trillion of agency mortgage-backed securities and up to $200 billion of agency debt by the end of the year. In addition, the Federal Reserve is in the process of buying $300 billion of Treasury securities. To promote a smooth transition in markets as these purchases of Treasury securities are completed, the Committee has decided to gradually slow the pace of these transactions and anticipates that the full amount will be purchased by the end of October. The Committee will continue to evaluate the timing and overall amounts of its purchases of securities in light of the evolving economic outlook and conditions in financial markets. The Federal Reserve is monitoring the size and composition of its balance sheet and will make adjustments to its credit and liquidity programs as warranted.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; Elizabeth A. Duke; Charles L. Evans; Donald L. Kohn; Jeffrey M. Lacker; Dennis P. Lockhart; Daniel K. Tarullo; Kevin M. Warsh; and Janet L. Yellen. -

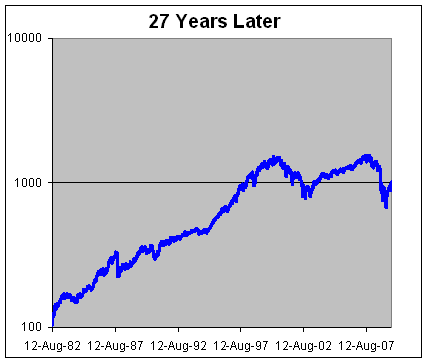

August 12, 1982

Posted by Eddy Elfenbein on August 12th, 2009 at 1:54 pmThe great bull market began 27 years ago today, and ended a little over nine years ago.

Here’s a look at the S&P 500 since then:

-

If Anyone Can Occupy that Space to Larry Kudlow’s Right

Posted by Eddy Elfenbein on August 12th, 2009 at 1:31 pmIt’s John Carney.

-

Goldman Discussion on KCRW

Posted by Eddy Elfenbein on August 12th, 2009 at 10:37 amI missed this when it first came out. Here’s a discussion about Goldman Sachs on KCRW from about a month ago. It’s long but if you have the time, it’s worth listening to.

Richard Bove is especially worth hearing while Matt Taibbi is completely and totally out of his depth. It’s actually pretty embarrassing. -

Short Selling of S&P 500 Drops to Lowest Level Since February

Posted by Eddy Elfenbein on August 12th, 2009 at 9:26 amWagers against the Standard & Poor’s 500 Index fell to the lowest level since February as investors shorted fewer shares of financial stocks.

Short interest on the S&P 500 declined to 8.77 billion shares as of July 31, a 12 percent decrease from two weeks earlier, according to data compiled by U.S. exchanges and Bloomberg yesterday. That’s the steepest drop since Sept. 30. Investors reduced bearish bets on financial stocks the most, slashing them by 31 percent to 2.05 billion shares. -

What to Expect from the Fed

Posted by Eddy Elfenbein on August 12th, 2009 at 9:22 amI remember when Fed meetings used to be interesting:

The Federal Reserve is expected to give a nod to signs the U.S. recession is waning but will likely warn that the recovery will be slow and dampen any expectations it will soon start to raise interest rates.

The Fed’s policy-setting committee, which meets on Tuesday and Wednesday, is expected to hold its benchmark overnight rate in a range of zero to 0.25 percent. A statement on the decision is due about 2:15 p.m. EDT on Wednesday.

“The markets have begun pricing in a near-term increase in interest rates. That is extremely unlikely. The Fed is going to want to discourage that,” said former Fed Governor Lyle Gramley.

The Fed is likely to decide to let its $300 billion Treasury purchase program expire, as scheduled, in September. Fourteen out of 16 primary dealers polled by Reuters last week said they expect the Fed not to extend the controversial program. -

The Case Against Talented Coin Flippers

Posted by Eddy Elfenbein on August 11th, 2009 at 4:10 pmProponents of Efficient Market Theory often dismiss the track records of superior money managers as something that ought to be expected given normal probability. They claim that it’s like calling a person who just nails ten heads in a row a superior coin flipper.

Sorry Mr. Buffett, old sport, you just got really, really lucky.

The problem I have with this is that the folks who are often listed as the top money managers seem to share some key traits—specifically they’re often value investors who have no time for EMT. If it truly were an odds game, I doubt we would see these traits appear so often.

Megan McArdle links to a post of managers who have excellent long-term track records. At the top is the late Bill Ruane who was a good friend of Warren Buffett. They met at Ben Graham’s value investing course at Columbia. In other worlds, they took the same class, learned the same lessons and both generated superior returns. There are plenty of other Graham-and-Dodd guys like Peter Lynch, or the guys at Leucadia National (LUK), and the guys at Danaher (DHR), who went on to trash the market year after year.

So it’s not just good coin tossing—it’s good coin tossing following the same coin-tossing lessons, the same coin-tossing methods taught by the same coin-tossing teachers. At what point do we agree that it ain’t just luck?

The Forbes list of billionaires contains lots of shrewd investors. I’m not aware of any that are pure technical guys. There are people who follow every conceivable strategy from astrology to Elliot Wave. Yet, time after time, it’s the value guys who rank near the top. -

Stocks Hate the President — Any President

Posted by Eddy Elfenbein on August 11th, 2009 at 10:49 amI had never heard this one:

According to research from the folks at Ned Davis dating all the way back to 1959, stocks do better when the public thinks the man in the White House is doing worse.

In fact, in weeks when the presidential approval rating sagged below 50 percent, stocks rose at an annual rate of 9 percent — versus only 2 ½ percent when the president in office sported a wildly popular 65 percent approval rating in the polls.

Americans witnessed this phenomenon firsthand on Inauguration Day; despite the national excitement about an Obama presidency and an approval rating near 70 percent, the Dow plunged 332 points. -

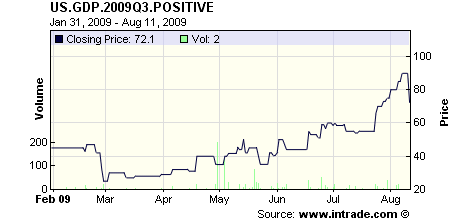

Outlook for Q3 Improves

Posted by Eddy Elfenbein on August 11th, 2009 at 10:29 amHere’s an interesting chart. This shows the Intrade contract betting that third-quarter GDP will be positive.

When the market was at its low in March, it was widely assumed that Q3 would be another bad quarter. Since then, the outlook has steadily improved and now it’s assumed that GDP will be positive. (Don’t read too much into that last downward data point, it seems to be a trade going off at the bid.)

One positive quarter doesn’t mean the recession is over. Also, it’s possible to see the numbers jump thanks to inventory rebuilding which may not mean that the underlying economy is improving. Still, the Intrade contract seems to match the resurgence of stock prices. We won’t get our first report on Q3 until late October. -

Productivity Surges

Posted by Eddy Elfenbein on August 11th, 2009 at 8:51 amPeople were complaining that Q2 earnings reports were good simply due to cost-cutting. That’s true, but they said it as if it doesn’t count. Improving productivity is crucial for an expanding economy:

The productivity of U.S. workers grew in the second quarter at the fastest pace in almost six years as employers squeezed more out of remaining staff to bolster profits.

Productivity, a measure of how much an employee produces for each hour worked, rose at an annual 6.4 percent pace, more than forecast, after a 0.3 percent gain the prior three months, Labor Department data showed today in Washington. Labor costs fell by the most in eight years.

Lower expenses mean companies may need to fire fewer workers as sales stabilize, the first step toward ending the worst employment slump in the post World War II era. Efficiency gains also help curb inflation, giving Federal Reserve policy makers, meeting today and tomorrow, extra time to remove stimulus.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His