-

Not Regina!

Posted by Eddy Elfenbein on May 14th, 2009 at 2:24 pmZero Hedge has this ultra-cool map of Chrysler dealership closures.

States that are big losers are:

* Pennsylvania: 53

* Ohio: 47

* Texas: 45

* Illinois: 43

* Michigan: 40

* California: 31

* New Jersey: 30

* Florida: 29

* New York: 26 -

8 Bedroom/7 Bathroom House for $675,000

Posted by Eddy Elfenbein on May 14th, 2009 at 1:00 pmHere’s a great deal on an 8 bedroom/7bathroom Tudor home. It has a three-car garage and a koi pond.

About the location…. -

Merrll Lynch Goes After Zero Hedge

Posted by Eddy Elfenbein on May 14th, 2009 at 10:18 amNow that Merrill Lynch has upgraded every single REIT and has a price target of +/- infinity, (conveniently pocketing over $100 million in the process), the company can focus on more pressing issues at hand (and no, not redecorating Thain’s legacy office in the neo-uber-criminal style). Instead, the bank has sent not one, not two, but a whopping six cease and desist orders to Zero Hedge. As the recently acquired bank can finally afford to pay lawyers again compliments of its REIT analysts, it has decided to pursue the source of all evil: all those David Rosenberg posts Zero Hedge has published, that seek to educate and provide some color to otherwise confused and CNBC abused readers and investors.

If it is any consolation, now that David is literally out of the building, ML can sleep soundly that ZH will only focus on the bank’s daily REIT upgrades (no, we have not forgotten about those) as it is alas the only source amusement coming out of doomed mother Merrill.

So, dear readers, please be aware that the following six posts will be removed at some point tonight as Zero Hedge is unable to underwrite and collect on average $10 million per REIT dilution events and thus afford any lawyers (except potentially for White & Case’s Tom Lauria).

http://zerohedge.blogspot.com/2009/05/parting-thoughts-from-rosenberg-ver-10.html

http://zerohedge.blogspot.com/2009/05/shooting-shoots.html

http://zerohedge.blogspot.com/2009/05/look-back-at-week.html

http://zerohedge.blogspot.com/2009/04/are-fed-and-markets-on-same-page.html

http://zerohedge.blogspot.com/2009/04/spin-on-6-gdp.html

http://zerohedge.blogspot.com/2009/04/busy-day-for-reit-analysts.html

As for the 500 or so websites that fervently and automatically repost and redistribute ZH content, well, those we have no control over. -

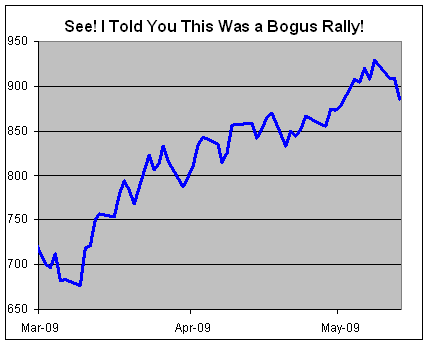

See! I Told You This Was a Bigus Rally!

Posted by Eddy Elfenbein on May 13th, 2009 at 4:02 pm

-

The Yield Curve Knows Best

Posted by Eddy Elfenbein on May 13th, 2009 at 11:53 amCaroline Baum is one of my favorite columnists. She has an article on one of the best economic forecasters out there. His name is Dr. Yield Curve.

The yield curve, or spread, has several things going for it:

First, it’s a leading economic indicator, officially added to the index designed to predict the economy’s ebbs and flows in 1996. It was a leader well before that, even though it was unofficial.

Second, what you see is what you get. The spread is never revised, always available and in no way proprietary.

Third, and most curious, the majority of economists don’t get it. They see rising bond yields in isolation — without paying attention to what that price-setter, the Fed, is doing at the front end of the curve.

It’s the juxtaposition of short and long rates, not their level, that conveys information about monetary policy.

In a July 2008 working paper, San Francisco Fed economists Glenn Rudebusch and John Williams examined the tendency for professional forecasters to ignore the spread. They compared the forecasts provided by the Survey of Professional Forecasters (SPF) to that generated by a simple, real-time model based on the yield spread.

Guess who won? And it wasn’t even close.Two years ago, I looked at the impact of the yield curve on the stock market and I was stunned to find:

Probably the most fascinating stat is that all of the stock market’s net capital gains have come when the 10-year yield is 65 or more basis points above the 90-day yield (that happens about 70% of the time). The yield curve hasn’t been that positive in 15 months.

Anything less than 65 basis points, including a negative yield curve, works out to a net equity return of a Blutarsky. Zero Point Zero.Today the spread is out to nearly 300 basis points.

-

FactSet Raises Dividend

Posted by Eddy Elfenbein on May 13th, 2009 at 11:45 amI have to add one quick post on the news that FactSet Research Systems (FDS) raised its dividend from 18 cents to 20 cents a share. It’s not a gigantic increase—last year FDS raised the dividend by 50% and the year before, they doubled it—but it’s very nice to see.

The dividend increase is 11% and FactSet is probably on its way toward growing its earnings by 15% this year. That’s very good considering the rotten environment. You really don’t buy FactSet for the dividend yield (currently 1.5%), but it’s a nice reminder from the company that they’re continuing to prosper. -

Outrageous Executive Perks

Posted by Eddy Elfenbein on May 13th, 2009 at 9:58 amMarketWatch lists 10 of the most egregious executive perks. I liked #3 in particular, a “stay” bonus even if you die:

Some companies are so keen to hold on to executives that they promise big pay and benefits even if the talent dies — in contracts known as golden coffins.

Life insurance policies worth millions of dollars are the least controversial part of these packages — even though buying such coverage without company help shouldn’t be too difficult for executives pulling in six or seven figures a year.

A peek under the lid of several golden coffins also reveals big severance payments, pensions and continued salaries if executives pass away.

Abercrombie & Fitch agreed to pay Chief Executive Michael Jefferies a $6 million “stay bonus” to keep him running the successful fashion clothing retailer, according to its 2007 proxy statement.

If Jefferies dies, the bonus stays and is paid out, along with $10 million from a company-purchased life insurance policy, to his estate. The retailer would also pay some of his incentive compensation, bringing the golden coffin’s value to more than $17 million, assuming he died on Feb. 2, 2008, according to the proxy. -

The Wonderful Dullness of Small Banks

Posted by Eddy Elfenbein on May 12th, 2009 at 1:31 pmDavid Segal writes about a topic that’s near and dear to our hearts—the boring stability of small banks. There are tons of little banks across the country that have barely noticed that credit crisis. Their businesses are boring and predictable, plus many of them are publicly traded.

Segal quotes a small-town banker:“I was on vacation in California and this guy I had just met said, ‘So, traveling on that bailout money, huh?’ ” said Blake Heid, of First Option Bank in Paola, Kan., which didn’t take any bailout money. “I didn’t find that very amusing.”

Though they greatly outnumber the national and regional banks, community banks have barely registered in any of the fallout from the credit crisis, in part because they hold less than 10 percent of the $13.8 trillion in bank assets nationwide.A few years ago, I wrote about three high-quality small-town banks. Not a single analyst followed them. Not long after I highlighted them, all three were bought out.

-

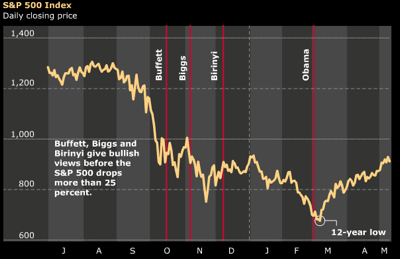

Obama Beats Buffett In Market Timing

Posted by Eddy Elfenbein on May 12th, 2009 at 1:00 pmPresident Barack Obama is proving to be a better judge of the stock market than Warren Buffett, the world’s second-richest person.

The CHART OF THE DAY shows the Standard & Poor’s 500 Index began its biggest rally since the 1930s after Obama said on March 3 that equities offered bargains for investors with a “long-term perspective.” While the measure fell 3.5 percent over the next week, reaching a 12-year low on March 9, it went on to surge as much as 37 percent.

Buffett, the chairman of Berkshire Hathaway Inc., wrote a column titled “Buy American. I Am.” for the New York Times in October, saying he may put all of his personal investments into U.S. stocks. The S&P 500 then plunged 29 percent through March 9 and is still down 3.9 percent. Berkshire, based in Omaha, Nebraska, posted its largest loss in at least two decades on May 8, in part because of Buffett’s “major mistake” of buying ConocoPhillips shares before oil retreated from a record.

Congratulations Mr. President! We’ve gained back everything we lost during you administration. -

The Diamond Market Is a Scam

Posted by Eddy Elfenbein on May 12th, 2009 at 11:11 amThe New York Times has an article today on the diamond market and how Russia is loading up on supply and waiting for the economy to recover.

I find the world diamond market fascinating because it’s almost completely rigged. If the free market had its way, diamonds would be insanely cheap.

The diamond market used to be controlled by De Beers. They’re the ones who run those “diamonds are forever” ads. (Sure they’re forever, all carbon is.) I believe that diamond rings are a wedding staple only in the United States. Lately, De Beers has fallen on hard times and Russia is taking over the market.The recession also coincided with a settlement with European Union antitrust authorities that ended a longtime De Beers policy of stockpiling diamonds, in cooperation with Alrosa, to keep prices up.

Though it is a major commodity producer, Russia has traditionally not embraced policies that artificially keep prices up. In oil, for example, Russia benefits from the oil cartel’s cuts in production, but does not participate in them.

Diamonds are an exception. “If you don’t support the price,” Andrei V. Polyakov, a spokesman for Alrosa, said, “a diamond becomes a mere piece of carbon.”You know the song, “carbon is a girl’s best friend.”

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}