-

Curious Intrade Contract

Posted by Eddy Elfenbein on September 10th, 2008 at 9:51 amIntrade runs a series of contracts based on “presidential decisions.” This includes oil futures and long-term interest rates, which aren’t exactly presidential decisions, but I supposed there’s some kind of presidential impact.

Anyway, one of the contracts is for troop level in Iraq on June 30, 2010, which is a presidential decision. According to the contract rules, each point is the equivalent to 2,000 troops. If there are over 200,000 troops in theater by the middle of 2010, the contract will be 100.

The current price for a Democratic president — presumably Barack Obama — is 45. For a non-Democratic president — presumably Senator McCain — the contract is 34. So does this mean that the crowd’s wisdom is that John McCain would be more willing to withdraw American troops than Barack Obama? I find that hard to believe, but perhaps I’m missing some Nixon-to-China effect. Or maybe the market is simply very inefficient here. It’s happened before.

One other point to mention is that the respective contracts will expire at 0 if the candidates don’t win. Fair enough. However, the McCain-to-win and Obama-to-win contracts are roughly the same right now. I don’t get why there’s such a difference in the troop level contract.

Update: OK, I completely misread this one. A reader writes: “There is no special explanation, what you see is what you said you would expect, Obama is more likely to withdraw troops. Think of it as a stock, if someone were to tell you a stock would be $100 this time next year, one is $45 and one is $34 (completely random), which would be more likely? Of course the $45, like Obama is priced.” -

The Palin Fund

Posted by Eddy Elfenbein on September 9th, 2008 at 2:39 pmHere’s the governor’s financial disclosure form. The last two pages have the First Dude’s IRA and 401K.

-

Nouriel Roubini Blames Free Market Ideologues for Socialism, or Something Like That

Posted by Eddy Elfenbein on September 9th, 2008 at 1:54 pmComrades Bush, Paulson and Bernanke Welcome You to the USSRA (United Socialist State Republic of America)

The now inevitable nationalization of Fannie and Freddie is the most radical regime change in global economic and financial affairs in decades. For the last twenty years after the collapse of the USSR, the fall of the Iron Curtain and the economic reforms in China and other emerging market economies the world economy has moved away from state ownership of the economy and towards privatization of previously stated owned enterprises. This trends was aggressively supported the United States that preached right and left the benefits of free markets and free private enterprise.

Today instead the US has performed the greatest nationalization in the history of humanity. By nationalizing Fannie and Freddie the US has increased its public assets by almost $6 trillion and has increased its public debt/liabilities by another $6 trillion. The US has also turned itself into the largest government-owned hedge fund in the world: by injecting a likely $200 billion of capital into Fannie and Freddie and taking on almost $6 trillion of liabilities of such GSEs the US has also undertaken the biggest and most levered LBO (“leveraged buy-out”) in human history that has a debt to equity ratio of 30 ($6,000 billion of debt against $200 billion of equity).A little overheated, no? It actually gets worse.

-

Investing in Volatility

Posted by Eddy Elfenbein on September 9th, 2008 at 12:35 pmDid you know you can invest in volatility? Some hedge funds are finding it quite profitable this year.

Hedge funds that profit from turbulence in the financial markets are beating stock, bond and commodity investments for the first time in five years.

Volatility hedge funds returned 7.3 percent this year through August, according to the Newedge Volatility Trading Index, which started in 2003. Hedge funds overall lost 4.8 percent in the same period, according to Hedge Fund Research Inc. in Chicago.The size of daily fluctuations have increased this year.

The S&P 500 fluctuated by more than 1 percent on 71 trading days this year, the most since 2003 and exceeding the 61-day annual average since 1928, said Howard Silverblatt, an analyst at S&P in New York. The index may have its most volatile year since 2002, when there were 125 swings of more than 1 percent.

I wouldn’t say we’re in a highly volatile environment, but that volatility has returned to normal after a period of very low volatility.

-

American Voices

Posted by Eddy Elfenbein on September 9th, 2008 at 12:27 pmFrom The Onion:

The federal government announced this weekend that it would seize control of Freddie Mac and Fannie Mae, the country’s two biggest mortgage firms, in order to keep them afloat. What do you think?

Marc Rose,

Welder

“Crap! Almost my entire Fantasy Privatized Social Security portfolio was in Freddie Mac.”

Julie Meyer,

Farmer

“Nothing rectifies out-of-control market failures like a healthy dose of government intervention and mountains of bureaucracy.”

Max Ramzi,

Roofer

“I think the government should let them go broke and give some of America’s mom-and-pop mortgage lenders a chance.”I actually agree with Max.

-

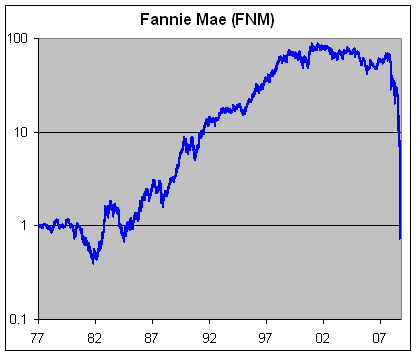

30 Years of Fannie Mae

Posted by Eddy Elfenbein on September 9th, 2008 at 11:33 am

A year ago, the shares were close to $70. -

NYT: Why the Bear Is Alive and Well

Posted by Eddy Elfenbein on September 9th, 2008 at 11:00 amOver the weekend, Paul J. Lim wrote in the New York Times:

If there’s a silver lining to bear markets, it is that they make stocks cheap for the next wave of investors. But so far in this downturn, it isn’t working out that way.

Based on the price-to-earnings ratio, stocks have actually become more expensive even as share prices have come tumbling down. In fact, the P/E ratio for the Standard & Poor’s 500-stock index, based on earnings over the previous four quarters, has risen to just over 24 from around 19, according to S.& P.Superficially, that’s correct. The problem is that the earnings decline is heavily weighted toward certain sectors — most particularly financials.

We don’t have the final numbers in yet, but the earnings of the financial stocks in the S&P 500 will probably be about -0.01. The S&P 500 Financials Index is currently around 300. So that’s a P/E ratio of…negative a lot. Consider that financials make up about 16% of the index, and I think we’ve found the squeaky wheel. Compare that with Health Care which is currently going for 15.6 times earnings or Staples (18.0), Tech (18.1) and Industrials (13.8).

Bear markets generall come in one of two forms. Either stock prices shoot past reality as they did in 1987 and 2000. Or fundamentals crumble beneath prices, which is what happen in 1990 and is happening again. -

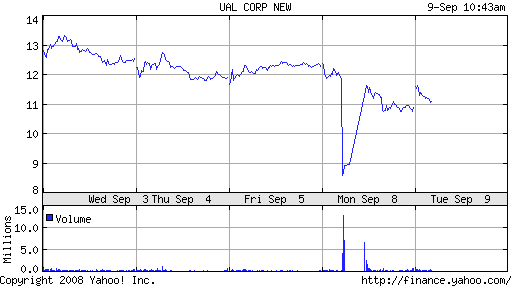

United Shares Plummet on Six-Year Old Story

Posted by Eddy Elfenbein on September 9th, 2008 at 10:55 amYesterday, a financial newsletter circulated a story that United Airlines was seeking bankruptcy protection, which lead to a sell-off in its shares. The story was correct but there was one important detail — it was from 2002.

Investors clearly took the article as news that the Chicago-based airline had once again sought protection from creditors, a scenario that had grown less remote in the past year as jet fuel prices skyrocketed.

United had refuted a report by late morning in New York, but not before the stock lost more than 75 per cent of its value. The shares appeared to trade at 1 cent, the default price assigned following its halt.

-

RIP: Georges Yared

Posted by Eddy Elfenbein on September 8th, 2008 at 4:54 pmI wanted to express my condolences to the family and friends of Georges Yared. I always enjoyed Georges’ market commentary and found him to be a sane voice in often insane times. He will be missed.

-

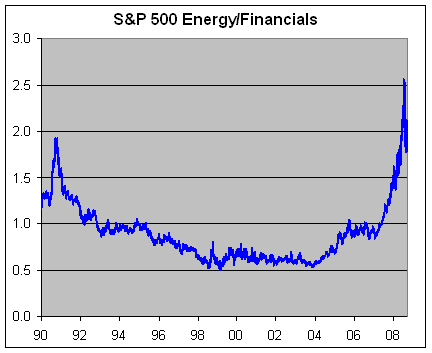

Chart of the Day

Posted by Eddy Elfenbein on September 8th, 2008 at 11:32 amHere’s the S&P 500 Energy Index divided by the S&P 500 Financial Index.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His