-

Count De Monet

Posted by Eddy Elfenbein on June 25th, 2008 at 4:21 pm

At Christie’s, they were looking to sell Monet’s “Le Bassin aux Nymphéas” (above) for $36 million to $47 million. The winning bid was for $80.4 million. -

No Change

Posted by Eddy Elfenbein on June 25th, 2008 at 2:15 pmHere’s the Fed’s latest statement:

The Federal Open Market Committee decided today to keep its target for the federal funds rate at 2 percent.

Recent information indicates that overall economic activity continues to expand, partly reflecting some firming in household spending. However, labor markets have softened further and financial markets remain under considerable stress. Tight credit conditions, the ongoing housing contraction, and the rise in energy prices are likely to weigh on economic growth over the next few quarters.

The Committee expects inflation to moderate later this year and next year. However, in light of the continued increases in the prices of energy and some other commodities and the elevated state of some indicators of inflation expectations, uncertainty about the inflation outlook remains high.

The substantial easing of monetary policy to date, combined with ongoing measures to foster market liquidity, should help to promote moderate growth over time. Although downside risks to growth remain, they appear to have diminished somewhat, and the upside risks to inflation and inflation expectations have increased. The Committee will continue to monitor economic and financial developments and will act as needed to promote sustainable economic growth and price stability.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Timothy F. Geithner, Vice Chairman; Donald L. Kohn; Randall S. Kroszner; Frederic S. Mishkin; Sandra Pianalto; Charles I. Plosser; Gary H. Stern; and Kevin M. Warsh. Voting against was Richard W. Fisher, who preferred an increase in the target for the federal funds rate at this meeting.Ron Isana summed it up well by saying that this statement has nothing for everyone.

-

Quote of the Day

Posted by Eddy Elfenbein on June 25th, 2008 at 10:16 amThe Oracle of Omaha speaks:

Warren Buffett is in Toronto, fielding questions from a crowd of 300 executives. One asks what makes people want to sell their companies to him.

The Berkshire Hathaway Inc. chief executive officer replies that he tells a prospective seller to think of the company as a work of art.

“You can sell it to Berkshire, and we’ll put it in the Metropolitan Museum; it’ll have a wing all by itself; it’ll be there forever,” he says at the February meeting. “Or you can sell it to some porn shop operator, and he’ll take the painting and he’ll make the boobs a little bigger and he’ll stick it up in the window, and some other guy will come along in a raincoat, and he’ll buy it.” -

Why Soccer Will Never Be Really Big Here

Posted by Eddy Elfenbein on June 24th, 2008 at 2:39 pmI just looked at the numbers of the Euro 2008 tournament. So far, there have been 28 games. The team that scores first has gone 20-3-3! Two other games have been 0-0 ties. Remarkably, the Turks have won two of the tournament’s three come-from-behind victories.

That’s one of the problems I have with soccer, come-from-behind wins are so rare. The U.S. is a country built on the idea of coming from behind to upset the champs.

I admire the athleticism of the players, and I think it’s fascinating that most of them look like guys you could see walking down street (unlike a pro football or basketball player). But I’m sorry, there has to be more scoreboard action. If you score the first goal, you basically have the game wrapped up. Do they just run out the clock? In baseball, scoring the first is good, but it’s just a start.

I’m curious what the equivalent start you need in baseball or football to have something close to a 20-3-3 record. My guess is that you need a 6-0 lead in baseball, and a 17-0 lead in football. -

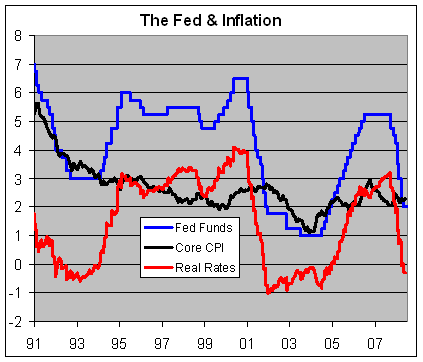

From Another Credit Crunch

Posted by Eddy Elfenbein on June 24th, 2008 at 11:54 amThe New York Times from November 1991:

Is the credit crunch real? Are banks denying creditworthy businesses the loans they need to invest the economy out of the recession?

The idea certainly appeals to the White House, which is in hot pursuit of a villain or three to explain why the stalled recovery is not the President’s fault. But many economists remain skeptical. The fall in the volume of bank loans, they point out, could be explained equally well by a recession-induced decline in the demand for credit.

Or at least it could until now. Minds are bound to be changed by the release of the first serious analysis of the crunch hypothesis, by Ben Bernanke of Princeton University and Cara Lown of the New York Federal Reserve Bank. The study, to be published in the January issue of the Brookings Papers on Economic Activity, confirms that a scarcity of bank capital has indeed affected the supply of loans. But the two economists believe that the full weight has been felt only in the Northeast. And they say the impact on jobs and incomes may be smaller than anecdotes of businesses’ drying up for want of liquidity would suggest. -

Have Lunch With Warren Buffett

Posted by Eddy Elfenbein on June 24th, 2008 at 11:42 amFor charity, you can have lunch with Warren Buffett. The current bid on eBay is $77,100.

That’s less than two-thirds of one Berkshire share. -

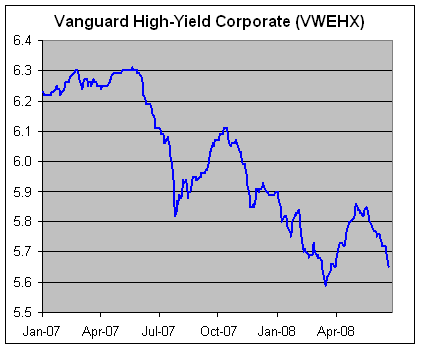

Junk Default Recoveries Maybe Lower Than Usual

Posted by Eddy Elfenbein on June 24th, 2008 at 10:31 amI’ve been surprised by the wide yield spread between low-risk bonds and high-risk bonds. Just look at the downward drift of Vanguard’s High-Yield Corporate Bond Fund (VWEHX).

I called Vanguard and the fund pays a dividend yield of 8.61%. Wow, that creams just about anything else you can find today.

Of course, they’re called junk for a reason. High-yield bonds have a greater risk of defaulting than investment grade debt. In today’s Wall Street Journal, Liz Rappaport says that if defaults do happen, the amount recovered could be less than it has been in the past.A report to be published Tuesday by Moody’s Investors Service argues that the explosion of loans issued by junk-rated companies in the past few years means that if they default, the recoveries on these loans might be less than in the past.

The highest-priority loans, called first-lien senior secured bank loans, will likely recover on average 68 cents on the dollar upon default in this downturn, compared with a historical average of 87 cents, Moody’s said.Here’s the money quote:

Now, Moody’s expects loan investors to fare almost as badly as investors in riskier junk bonds have done in previous busts. “It doesn’t matter what you call something,” says Kenneth Emery, author of the report. “What matters is where you sit in the liability structure.”

Historically, it’s fairly rare for a bond, even a junk bond, to default. The long-term rate for junk is about 2.6%, but for investment grade bonds, the default rate is just 0.1%. However, defaults can often spike dramatically higher. There have been times when the junk default rate has hit 15%, while it’s never gone above 1.6% for the highest-grade bonds.

Reuters reports today:The U.S. default rate on junk bonds, high-yield debt that is below investment grade, rose to 1.89 percent in May, a 26-month high, from 1.64 percent in April. The rate is expected to rise to 4.7 percent within a year and there is a 20 percent chance it could go as high as 8.5 percent, S&P said.

-

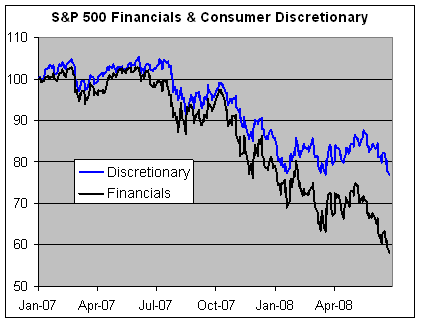

Goldman Admits It Goofed

Posted by Eddy Elfenbein on June 24th, 2008 at 9:34 amYou don’t find the word “goofed” in many financial headlines, especially ones dealing with Goldman Sachs, but Reuters has the goods:

Goldman cuts financials, admits goofed on upgrade

Goldman Sachs & Co strategists urged stock investors on Monday to “underweight” U.S. financial and consumer shares, admitting it was wrong when it upgraded both sectors just seven weeks ago.

The downgrades sparked selling in the two sectors as investors feared that weakening consumer demand and deterioration in the credit markets will weigh on profitability.

“We boosted our consumer discretionary and financials weights in May on the belief the sectors would benefit from bank recapitalizations and fiscal stimulus,” Goldman strategists led by David Kostin wrote. “Our thesis was clearly wrong in hindsight.”Good for them for reversing their call. One of the biggest mistakes investors make is refusing to admit defeat on an investment. People will hang on to the worst sorts of stocks just so because they don’t “want to take a loss.” Stocks don’t have egos. Sometimes it’s best just to let it go.

Here’s a look at how the S&P 500 Financials and Consumer Discretionary Indexes have done since the beginning of last year.

This chart reminds me of another big mistake investors make: “It’s already down so much, it can’t possibly go any lower?” -

UNH Under $27

Posted by Eddy Elfenbein on June 23rd, 2008 at 3:07 pmUnitedhealth Group (UNH) got down to $26.35 today. That’s the lowest price in over four years. The company said that it expects earnings this year of $3.55 to $3.60 per share.

I’m going go out on a limb here and say, I don’t think the market believes that. -

Aussie Power Crisis Leads to Flat Beer

Posted by Eddy Elfenbein on June 23rd, 2008 at 2:40 pmTalk about globalization. Thanks to demand from China, a town in Australia is booming. That is, until an explosion cut off natural gas supplies.

Hotels are turning off heaters, dirty laundry is piling up and restaurants and bars expect shortages of beef and draught beer. The crisis may shave a quarter point off Australia’s gross domestic product as mines and processing plants cut production, slowing the state’s commodities-driven boom, estimates Brian Redican, a senior economist at Macquarie Group Ltd. in Sydney.

It’s a nightmare deciding what stays on and what stays off. My favorite quote:

”When it gets to the stage where you can’t pour a beer in a pub, you know this crisis has the potential to affect every aspect of business,” says Bradley Woods, CEO of the Australian Hotels Association’s West Australian branch.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His