-

Troubled Toshiba Sells Stake in Joint Venture with Carrier

Posted by Eddy Elfenbein on February 7th, 2022 at 9:16 amA good way to find bargains is when another company is holding a fire sale. That’s sort of what’s happening with Toshiba. The company is a bit of a mess right now and they’re taking bold action to change course.

The original plan was to split up into three different companies. The problem was that shareholders hated the idea. Now the plan is to split into two companies and sell off “non core assets.”

One business will be their devices business (semiconductors). The other will be its infrastructure business which will carry the Toshiba name. The rest will be called Toshiba Tec Corp. which is their electronic equipment business.

For us, the important news is that Toshiba will sell its stake in a joint venture with Carrier Global back to Carrier for around 100 billion yen ($870 million). Toshiba now owns a 60% stake in the venture, and they’re going to sell 55% of it to Carrier.

The planned acquisition will strengthen Carrier’s position in one of the fastest-growing HVAC segments, as well as scale its global VRF product platform with leading and differentiated technology and the addition of a renowned brand to its portfolio.

Established in 1999, TCC designs and manufactures flexible, energy-efficient and high-performance VRF and light commercial HVAC systems utilizing its own proprietary inverter technology, as well as commercial products, compressors and heat pumps. VRF delivers high-performance heating and cooling through systems that are typically all-electric and highly efficient, consistent with Carrier’s sustainability goals to reduce its customers’ carbon footprint by more than one gigaton by 2030.

Carrier’s acquisition will include all of TCC’s advanced research & development centers and global manufacturing operations, strong product pipeline, and the long-term use of Toshiba’s deeply respected and iconic brand.

“Carrier sees significant growth potential in the global VRF, light commercial and heat pump segments and is excited by the opportunity to expand our business through this strategic acquisition. TCC’s proven R&D expertise, strong global brand and talented employees will be tremendous additions to Carrier’s multi-brand channel strategy,” said Dave Gitlin, Chairman & CEO, Carrier. “We look forward to offering complementary, high-performance and sustainable solutions to our customers that will help them achieve their environmental goals.”

The global market for VRF and light commercial equipment is the fastest growing HVAC equipment segment. Upon close, the acquisition will position Carrier as a VRF leader, more than doubling its sales in the market segment.

“We are pleased that TCC employees will continue the growth and innovation journey of Toshiba’s HVAC business as part of Carrier, benefiting from its unparalleled global reach, strong dealer network and shared history of innovation,” said Satoshi Tsunakawa, President & CEO, Toshiba. “This is a value-enhancing opportunity for investors, customers and employees.”

Today’s announcement builds on Carrier’s recent acquisition of Guangdong Giwee Group, a China-based manufacturer of HVAC products, offering a portfolio of high-quality products including VRF and light commercial air conditioners.

Combined with Carrier’s existing partnerships, the acquisition strengthens Carrier’s portfolio of innovative, environmentally responsible solutions with a broader range of highly efficient, all-electric products, positioning Carrier to lead the world’s heating and cooling sustainability transformation.The acquisitions also demonstrate the company’s commitment to investing in growth, while delivering on Carrier’s commitment to increase product extensions and broaden geographic coverage. In addition, the acquisition is also another step in Carrier’s continuing efforts to simplify its HVAC joint venture structure.

The acquisition is expected to close by the end of Q3, subject to customary closing conditions, including regulatory approvals. Upon closing, Toshiba will retain a 5% ownership stake in TCC, and Carrier will consolidate over $2 billion in unconsolidated revenue.

-

Morning News: February 7, 2022

Posted by Eddy Elfenbein on February 7th, 2022 at 6:14 amSamsung, Blue Ocean Launch U.S. Stock Trading During South Korean Business Hours

How China’s Communist Officials Became Venture Capitalists

Adults Back in Charge of Stock Market as Fed Awakens Big Money

Earnings Are Driving the Market but It’s Not Clear Where

An American Labor Market Mystery

Counting on ‘Endemic’: The Travel Industry Readies for a Potentially New Phase

Peloton Deal May Pose Regulatory ‘Headache’ for a Tech Giant

Spotify’s CEO Is ‘Deeply Sorry’ But Won’t Drop Joe Rogan

Credit Suisse, a Coke-Smuggling Wrestler and Stashes of Cash

A Side-Effect of China’s Strict Virus Policy: Abandoned Fruit

Toshiba Now Plans To Split Into Two, Hikes Shareholder Return Targets

Worker Absences From Covid-19 Hold Back Companies’ Growth

Kohl’s Adopts ‘Poison Pill’ To Ward Off Hostile Takeover Bids

Be sure to follow me on Twitter.

-

January NFP = +467,000

Posted by Eddy Elfenbein on February 4th, 2022 at 9:12 amThe January jobs report is out and the U.S. economy added 467,000 net new jobs last month. The numbers for November and December were also revised much higher. The unemployment rate rose 0.1% to 4.0%.

December, which initially was reported as a gain of 199,000, went up to 510,000. November surged to 647,000 from the previous reported 249,000. For the two months alone, the initial counts were revised up by 709,000. The revisions came as part of the annual adjustments from the BLS that saw sizeable changes for many of the months in 2021.

“The benchmark revisions helped the numbers a bit just because it moved out some of the seasonal factors that have been at work. But overall the job market is strong, particularly in the face of omicron,” said Kathy Jones, chief fixed income strategist at Charles Schwab. “It’s hard to find a weak spot in this report.”

For January, the biggest employment gains came in leisure and hospitality, which saw 151,000 hires, 108,000 of which came from bars and restaurants. Professional and business services contributed 86,000, while retail was up 61,000.

There was more good jobs news: The labor force participation rate rose to 62.2%, a 0.3 percentage point gain. That took the rate, which is closely watched by Fed officials, to its highest level since March 2020 and within 1.2 percentage points of where it was pre-pandemic.

A more encompassing level of unemployment that counts discouraged workers and those holding part-time jobs for economic reasons dropped to 7.1%, 0.2 percentage point decline and to just above its pre-pandemic level.

The job gains brought employment back to about 1.7 million below where it was in February 2020, a month before the pandemic declaration.

The broader U-6 unemployment rate is nearly back to where it was pre-Covid. It’s now at 7.1%. The last pre-Covid low was 6.8% in December 2019.

The Labor Force Participation Rate is down but it’s not quite as dire as some people think. The LFPR for prime working age (25 to 54) is back to 82.0% which is higher than where it was in 2017 and much of 2018.

-

Morning News: February 4, 2022

Posted by Eddy Elfenbein on February 4th, 2022 at 7:04 amCentral Bank Balance of Power Shift Raises Policy Error Risk

Flatter U.S. Yield Curve Dominates Emerging-Market Trader Minds

Why the World’s Biggest Ocean Shipping Lines Are Buying Cargo Planes

Automakers, Chip Firms Differ on When Semiconductor Shortage Will Abate

America Is Facing a Great Talent Recession

Amazon Set to Add More Than $150 Billion in Wild Value Swing

Meta Erases $251 Billion in Value, Biggest Wipeout in History

A Change by Apple Is Tormenting Internet Companies, Especially Meta

Snap Stock Is Soaring on a Surprise Profit. It Doesn’t Have All of Facebook’s Problems.

Microsoft’s Videogame Boss and the Long Battle to Reinvent the Company

World’s Most Influential Money Manager Enters the TikTok Sphere

NBC Opens Olympics With ‘Worst Hand Imaginable’

Why the Beijing Olympics Are Awkward for Corporate Do-Gooders

More Thoughts on America’s Feel-Bad Boom

Be sure to follow me on Twitter.

-

Earnings from Hershey and ICE

Posted by Eddy Elfenbein on February 3rd, 2022 at 9:04 amIt’s a busy morning today. First, we had the jobless claims report. Weekly jobless claims were 238,000. That was a little below expectations of 245,000. This data series has crept higher over the past two months. The government will release its jobs report for January tomorrow.

We also had two Buy List earnings reports. Intercontinental Exchange (ICE) said it made $1.34 per share. That was two cents more than expectations. ICE also raised its quarterly dividend by 15%, from 33 to 38 cents per share. The first quarter cash dividend is payable on March 31 to stockholders of record as of March 17.

Hershey (HSY) reported earnings of $1.69 which topped the consensus estimate of $1.61 per share. Hershey said it expects 2022 earnings of $7.84 to $7.98 per share. The consensus on Wall Street had been for $7.57 per share.

-

Morning News: February 3, 2022

Posted by Eddy Elfenbein on February 3rd, 2022 at 7:03 amEurozone Inflation Rises to Fresh Record, Against Expectations

Turkey’s Inflation Hits Nearly 50%, Highest in Two Decades

BOE Hikes Rates as Four Officials Vote for a Bigger Increase

Biden’s Pick for Bank Cop Faces a Contentious Senate Hearing

What Does a Federal Reserve Governor Do?

Meta’s ‘Unmitigated Disaster’ of a Quarter

Facebook Owner Meta Set for $195 Billion Wipeout, Biggest in Market History

Never Mind the Metaverse. Facebook Must Solve Its TikTok Problem

Apple Makes Progress in India as iPhone Sales Rise 34% to Record

Hershey’s Quarterly Profit Rose, Helped by Price Increases

The Rise of the $2.5 Billion Ugly-Shoe Empire

Jeff Zucker Leaves CNN In Limbo With Streaming Launch Weeks Away

Carlyle’s Q4 Earnings Jump Nearly Fourfold on Record Asset Sales

Spotify, Facing Pushback Against Joe Rogan, Reports Jump in Users

Cremation Borrows a Page From the Direct-to-Consumer Playbook

Be sure to follow me on Twitter.

-

AFLAC Earned $1.28 per Share for Q4

Posted by Eddy Elfenbein on February 2nd, 2022 at 4:21 pmAfter the bell, AFLAC (AFL) reported Q4 earnings of $1.28 per share. That’s an increase of 19.6%. The weaker exchange rate pinged earnings by five cents per share.

Q4 revenues were $5.4 billion. That’s down from $5.9 billion in the fourth quarter of 2020.

During Q4, Aflac spent $625 million to repurchase 11.1 million of its common shares. For the full year, Aflac deployed $2.3 billion in capital to repurchase 43.3 million of its common shares. At the end of December 2021, the company had 55.8 million remaining shares authorized for repurchase.

Shareholders’ equity was $33.3 billion, or $50.99 per share, at December 31, 2021, compared with $33.6 billion, or $48.46 per share, at December 31, 2020. The annualized return on average shareholders’ equity in the fourth quarter was 12.4% and 12.9% for the full year.

For the full year of 2021, total revenues were down 0.2% to $22.1 billion, compared with $22.1 billion for the full year of 2020. Adjusted earnings for the full year of 2021 were $4.0 billion, or $5.94 per diluted share, compared with $3.6 billion, or $4.96 per diluted share, in 2020. Excluding the negative impact of $0.06 per share from the weaker yen/dollar exchange rate, adjusted earnings per diluted share increased 21.0% to $6.00 for the full year of 2021.

DIVIDEND

The board of directors declared the first quarter dividend of $0.40 per share, payable on March 1, 2022 to shareholders of record at the close of business on February 16, 2022.

OUTLOOK

Commenting on the company’s results, Chairman and Chief Executive Officer Daniel P. Amos stated: “The company generated strong earnings for the year, largely supported by the continuation of low benefit ratios associated with pandemic conditions and better-than-expected returns from alternative investments. While we saw improvements in the quarter for both the United States and Japan, we continue to remain cautiously optimistic in the face of ongoing pandemic conditions.

“Looking at our operations in Japan, I am encouraged by the 7.7% sales increase for the year, which included the first quarter introduction of our medical product EVER Prime and the September launch of our new nursing care product. However, we continued to navigate evolving pandemic conditions in Japan, including various states of emergency that may impact our ability to meet face-to-face with customers, which continues to be key to a recovery in sales.

“In the U.S., I am pleased with the 16.9% sales increase for the year. At the same time, I am encouraged by reports of new small business formation and the resiliency of larger businesses. Our sales in the fourth quarter reflect increased face-to-face sales opportunities. We continue to work toward reinforcing our position and generating stronger sales in 2022, realizing we may face headwinds from pandemic conditions.

“As always, we are committed to prudent liquidity and capital management. This includes maintaining strong capital ratios on behalf of our policyholders in both the U.S. and Japan. It goes without saying that we treasure our record of dividend growth. Coming off our 39th consecutive year of dividend increases, I am pleased with the board’s decision to increase the quarterly dividend by 21.2% in the first quarter, as we announced in November. Our dividend track record is supported by the strength of our capital and cash flows. At the same time, we remain in the market repurchasing shares with a tactical approach and focused on integrating the growth investments we have made in our platform. By doing so, we look to emerge from this period in a continued position of strength and leadership.”

-

Thermo Fisher Beats Earnings

Posted by Eddy Elfenbein on February 2nd, 2022 at 9:00 amThis morning, Thermo Fisher Scientific (TMO) reported Q4 earnings of $6.54 per share which was much more than Wall Street’s forecast of $5.27 per share. I said I was expecting a big earnings beat and I was right.

For the entire year, Thermo made $25.13 per share. That was an increase of 28% over 2020. Thermo’s revenue grew 22% to $39.21 billion. The company’s most recent guidance had been for $23.37 per share.

TMO’s quarterly revenue rose by 1% to $10.70 billion. The company had Covid revenue of $2.45 billion.

For 2022, Thermo sees revenue of $42 billion. Wall Street had been expecting $40.7 billion. The company sees 2022 earnings of $22.43 per share. Wall Street had been expecting $21.87 per share.

One other news item. The big jobs report is due out on Friday, but this morning we got a possible preview. ADP said that private payrolls fell by 301,000 last month. This was the first jobs loss since December 2020.

According to ADP, Omicron wreaked havoc on the jobs market. The leisure and hospitality sector lost 154,000 jobs. The jobs gain number for December was revised downward to 776,000.

Trade, transportation and utilities cut 62,000 while the other services category declined by 23,000.

Manufacturing also lost 21,000 positions, while education and health services reported a drawdown of 15,000 and construction fell by 10,000.

Service-providing industries were responsible for 274,000 of the job losses, with goods producers falling by 27,000.“The labor market recovery took a step back at the start of 2022 due to the effect of the omicron variant and its significant, though likely temporary, impact to job growth,” ADP chief economist Nela Richardson said.

For Friday’s official government report, Wall Street expects to see a gain of 150,000 net new jobs.

-

Morning News: February 2, 2022

Posted by Eddy Elfenbein on February 2nd, 2022 at 7:09 amEuro-Zone Inflation Unexpectedly Hits Record, Pressuring ECB

Japanese Banks Sound Caution for Earnings As Omicron Highlights Bad Loan Risks

Why Are Oil Prices So High and Will They Stay That Way?

A Normal Supply Chain? It’s ‘Unlikely’ in 2022.

Warehouse Space Is the Latest Thing Being Hoarded

Consumers Are Pivoting Spending to Services Like Dining and Travel

Wall Street Bankers Heading for Biggest Bonus Payday in Decade

U.S. Job Openings, Quits Remained Elevated at End of Last Year

First Black Woman Picked for Fed Draws GOP Fire Over Research

Zuckerberg’s Plan to Overcome Washington’s Aversion to Metaverse

Alphabet Stock Split Aimed at Bringing Google Shares to Masses

Google Vanquished a Rival in Prague. Payback Could Hurt.

GM Earnings Rose Sharply in 2021

Where Olympic Sponsor Coca-Cola Stands With China

Cathie Wood’s True Believers Are Sticking With Her

A Year On, GameStop Champion Roaring Kitty Is Quiet — Yet Much Richer

Why Is Matt Damon Shilling for Crypto?

Be sure to follow me on Twitter.

-

CWS Market Review – February 1, 2022

Posted by Eddy Elfenbein on February 1st, 2022 at 6:12 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Stock Market Stumbled Into January

The stock market certainly didn’t get off to a good start this year. For the month of January, the S&P 500 lost 5.26%. That was the market’s worst month since March 2020 and it was the worst January since 2009.

Actually, it could have been worse. The S&P 500 posted big gains on the final two trading days of the month. In fact, we came very close to being in an official correction. From the market’s closing high on January 3 to the closing low from last Thursday, the S&P 500 lost 9.80%. The Nasdaq Composite did even worse and it’s still in correction territory.

We’ve got a decent bump on Friday and Monday plus a nice gain today, but it’s too early to say the selling wave is over. How do we know when the coast is clear? That’s hard to say, but one encouraging sign is that the S&P 500 has poked its head back above its 200-day moving average (the green line in the chart below). We still have about 1.8% to go until the index breaks above its 50-day moving average.

Don’t be surprised to see another downswing. The market likes to test and retest its recent low. Wall Street bears are easily startled, but they’ll soon be back, and in greater numbers.

Wall Street has finally acclimated itself to the idea that the Fed is really truly going to raise interest rates. The futures market has literally priced the odds of a March hike at 100%. That sounds pretty certain. There’s even been some recent talk of the Fed hiking rates by 0.50%. Call me a doubter.

The big question for the Fed is how inflation will behave. Consider some facts: Crude oil is up 65% in the last year, and it recently touched a seven-year high. Cotton is at a 10-year high. Orange juice futures got to their highest level since 2018.

This morning, the Institute for Supply Management said that its ISM Manufacturing index fell to 57.6 last month. That’s the lowest number in 15 months. This signals that the factory sector of the economy may be slowing. Goldman Sachs cut its Q1 GDP growth forecast to 0.5% from 2%.

Church & Dwight Rallies on Strong Earnings

One of the ideas I try to stress to investors is understanding what kind of stocks they own. Specifically, investors should know if a stock they own is a defensive stock or a cyclical stock.

It’s not that one kind of stock is better than the other. It’s that both groups move in big waves. That means that no matter how good or bad a given stock is, it can easily get wrapped up in the broader trend.

By defensive stock, I mean a company whose business fortunes aren’t closely tied to the status of the economy. A perfect example from our Buy List is Church & Dwight (CHD). The company owns a broad range of consumer brands. They have everything from Arm and Hammer to Trojan, OxiClean and Nair.

If the economy hits the skids, Church & Dwight’s business won’t be terribly impacted. It makes the kind of things people need all the time. Contrast that with a company like a chemical company or a homebuilder. Those sectors tend to be “feast or famine.” In fact, much of the business for these kinds of companies involves managing themselves between the busts.

Over the summer, CHD warned us that Q3 was going to be weak. It saw earnings coming in at 70 cents per share. The official word was that they were “temporarily constrained by supply.”

Apparently, they weren’t as constrained as advertised. CHD had a great Q3, earning 80 cents per share.

Over the last few months, shares of Church & Dwight have performed quite well. Much of that is due to the market’s recent concerns that the economy may be slowing down. Lots of defensive stocks have done well. Another good example from our Buy List is Hershey (HSY).

A few months ago, Church & Dwight told us to expect Q4 earnings of 61 cents per share. On Friday we got the report and again, CHD underestimated themselves. The company made 64 cents per share for its Q4. That’s up 20.8% from a year ago. Wall Street had been expecting earnings of 60 cents per share.

For the year, the company made $3.02 per share. That’s up 6.7% from a year ago. Full year net sales grew 6% to $5.19 billion.

CEO Matthew Farrell said:

Our brands once again experienced strong consumption in Q4 2021. In the U.S. we grew consumption in 11 of the 16 categories in which we compete. Five of our brands experienced double digit consumption growth including ARM & HAMMER® Scent Boosters, ARM & HAMMER® Clumping Litter, OXICLEAN® stain fighters, BATISTE® dry shampoo and ZICAM® zinc supplements. Consumption continues to outpace shipments as supply chain disruptions continue. This strong consumption would likely have been higher if not for the ongoing supply chain challenges. This demonstrates the strength of our brands as we gained share on 6 of the 13 power brands in a difficult supply environment. Global online sales grew 12.7% in 2021, and as a percentage of total sales has expanded to 15% for the full year.

Church & Dwight said rising material costs have pinged their gross margins. The company also said it’s facing higher transportation costs and labor shortages. While they expect supply issues to gradually abate, the company is raising prices. By the end of this month, Church & Dwight expects to have taken pricing action on 80% of their portfolio brands. Fortunately, most CHD brands have a strong position in their respective markets so they can command higher prices. Companywide gross margins were 42.5% in Q4.

The company also raised its quarterly dividend from 24.25 cents per share to 26.25 cents per share. That comes to $1.05 for the year. That’s a yield of a little over 1%. This is CHD’s 26th consecutive annual dividend increase.

The market apparently liked the report as shares of CHD rallied 4.40% to close at $103. I continue to rate CHD a strong buy up to $110 per share.

Rollins Is Worth a Look

One of the best ways to find good investment opportunities is to follow excellent companies and wait for their share prices to fall apart.

A good example is Rollins (ROL). The company is in the pest control business. In plainer terms, they kill bugs for money. Rollins is the parent company of Orkin.

I realize it sounds icky, and it is, but that doesn’t mean it’s a bad investment. Quite the opposite. In his book One Up on Wall Street, Peter Lynch wrote, “Better than boring alone is a stock that’s boring and disgusting at the same time. Something that makes people shrug, retch, or turn away in disgust is ideal.” Yep, that’s Rollins.

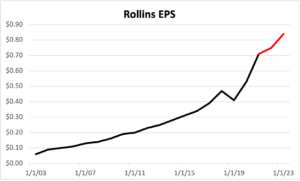

Check out the growth in its EPS:

The red part of the line is the estimate.

It’s amazing how few people know about this stock. Only five analysts on Wall Street bother following Rollins even though it has a market value of $15 billion. Years ago, Rollins was a diversified company with lots of holdings. They eventually spun off their oil and gas units into another company. What was left was the pest control business which is a very nice business to own.

The company is able to maintain gross margins in excess of 50%. As it turns out, killing bugs is very profitable. Since 2000, shares of Rollins are up more than 55-fold.

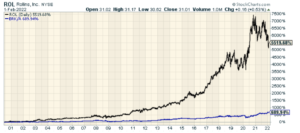

Check out this chart of ROL’s performance since May 2000. For context, see that blue line down there? That’s Berkshire Hathaway:

Rollins now has two million customers at 700 locations around the world. The company currently pays a quarterly dividend of 10 cents per share, but it’s been known to hand out special dividends at the end of the year. I like companies that do that.

Despite the company’s long-term success, the stock hasn’t done that well lately. Shares of ROL peaked at $43 in October 2020. Last week, the stock got as low as $28.51 per share.

The earnings report came out last Wednesday and Rollins said it had Q4 earnings of 14 cents per share. That was one penny below estimates. This was the second quarter in a row that Rollins has missed estimates.

Rollins has faced some serious issues over the past year. The SEC said it was investigating the company’s accounting. Rollins doesn’t appear to be consistent in how they’ve reported revenue. The company is working with the SEC to resolve these issues. The takeaway for us is that the stock is down a lot. I wouldn’t say the shares are cheap, but they’re much cheaper than they used to be.

If Rollins can again command the earnings multiple that it used to have (around 45X), and if it can manage the earnings growth it used to have (12% to 14%), then this is a very inexpensive stock. Of course, that’s a lot of ifs. I’m going to keep a close eye on Rollins.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His