-

Fed May Alter Statement

Posted by Eddy Elfenbein on December 12th, 2005 at 2:24 pmFed watchers beware. Greenspan & Co. may alter the language in tomorrow’s post-meeting statement:

Lehman Brothers Inc. and Banc of America Securities LLC are among 12 of the 22 primary dealers of U.S. government securities that say the central bank will stop saying interest rates provide “accommodation,” meaning they are low enough to spur economic growth. All 22 expect the Fed to lift its key rate to 4.25 percent from 4 percent.

Removing that one word from the Fed statement explaining policy decisions may fuel the debate between economists and investors over whether the central bank is almost finished raising rates, setting the stage for a rally.

“The message they want to convey is that they are still concerned about inflation and that they will continue to raise rates until inflation pressures subside,” said Joseph Abate, a senior economist at Lehman in New York. “It’s not difficult to reconcile the Fed keeping the ‘measured’ language in there but altering the accommodative language.”

Fifteen dealers predict policy makers will repeat rates are likely to rise at a “measured” pace, citing the potential for faster inflation.Here’s more on what the Fed needs to consider.

-

Welcome to the Global Economy

Posted by Eddy Elfenbein on December 12th, 2005 at 1:23 pmOne of Brazil’s fastest-growing companies is a home-grown Arabic fast-food chain.

-

Stock Options: Old Game, New Tricks

Posted by Eddy Elfenbein on December 12th, 2005 at 11:29 amBusiness Week looks at the game of stock options accounting. One of the variables of the Black-Scholes pricing formula is volatility. Now that companies have to account for employee stock options, their volatility assumptions are magically falling:

Time Warner’s lowering of its expected volatility in 2004 cut its options expense by $72 million, a 28% drop, according to New Constructs. Wireless service provider Nextel Partners slashed estimated options expenses from $41 million to $33 million. A Time Warner spokeswoman says the new calculation accurately reflects the more stable range in which the company’s stock now trades. Nextel Partners declined to comment.

Another tactic hundreds of companies have used is accelerated vesting. Options traditionally become effective over a period of years after they’re granted and are canceled if the recipient leaves the company. By making options vest in 2005 rather than in future years, companies can bury the cost in the footnotes of their 2005 paperwork. That boosts earnings in 2006 and beyond.

The number of companies employing the practice has almost doubled since midyear, from 234 in July to 439 by late November, according to Bear Stearns. The activity has slashed $4 billion from expenses for 2006 and later years. Senyek of Bear Stearns projects that 600 companies could speed up vesting by the end of 2005, boosting future profits by over $5 billion. -

Still More Mergers

Posted by Eddy Elfenbein on December 12th, 2005 at 10:37 amThe merger deals continue to roll along. Today we learn the Viacom (VIA-B) beat out GE (GE) for DreamWorks. According to the New York Times, the deal was high drama up to the last minute.

Also, ConocoPhillips (COP) is going after Burlington Resources (BR) for $30 billion. Plus, Electronic Arts (ERTS) is going to buy Jamdat Mobile (JMDT).

But despite those headline deals, the most fascinating one is the verbal/bidding war for the London Stock Exchange. In the U.S., the exchanges have seen their stocks soar. Now there’s a bidder for the venerable LSE. The London Stock Exchange has roots that date back over 400 years. The problem is that the bidder ain’t British but a slovenly colonist, the Australian investment bank Macquarie. This has the Brits rather upset.

Last week, Macquarie bid 580 pence for the exchange. The LSE call the offer “derisory.” Yes, even the British insults sound classy. Just once, wouldn’t you love to hear an American company say that about an offer?

The Aussies have hit back and said that they’re really not that interested in a “boring utility.” Yep, it’s getting ugly. Now Macquarie is being totally silent, which in Australian is very suspicious. Meanwhile, London is abuzz and a formal offer is expected soon. Personally, I hope they don’t find it too opprobrious. -

Case: Break Up Time Warner

Posted by Eddy Elfenbein on December 11th, 2005 at 9:32 pmIn today’s Washington Post, Steve Case argues for breaking up Time Warner (TWX):

This past July, having concluded that integration would never happen, I proposed to the company’s board that it was time to “liberate” and split the conglomerate into four freestanding companies — Time Warner Cable, Time Warner Entertainment, Time Inc. and AOL — each with its own strategy, stock, balance sheet, management team and board.

Each of the four units would benefit from the separation. Time Warner Cable would be better positioned to compete effectively against aggressive communications companies like Verizon and the new AT&T — and it would lose little in being divorced from the Time Warner movie and television companies, as few benefits have ever materialized from having Time Warner Cable and Turner Broadcasting under the same roof. Time Warner Entertainment (Warner Bros., New Line, HBO and Turner Broadcasting) could build on its strength as one of the world’s leading entertainment companies, and more vigorously embrace new technologies and new distribution channels. Time Inc. would be able to grow from being a traditional magazine company into a multifaceted media and information company, focused on expanding its brands well beyond magazines.

AOL would be the fourth company, and perhaps the one with the greatest potential. At a time when some of the fastest-growing enterprises in our economy are Internet leaders — such as Google — shareholders would benefit from seeing AOL return to its roots in the Internet sector. A split into separate companies has one other advantage for shareholders: Investors who don’t believe in the promise of one of these endeavors could sell their shares in that business and double up in their holdings in other parts of the former Time Warner empire.

The success that Warner Music has had since being spun off from the parent company is an example of how this strategy can deliver value for all stakeholders. When Warner Music was part of Time Warner, it was — much like AOL — seen as a business in decline, a troubled division with a glorious past but a questionable future. But since being separated, Warner Music has increased in value by cutting bureaucracy, signing new artists and investing more aggressively in digital music. The private equity firm buyers have already recouped their initial investment, and are still major owners of a stock that is up 20 percent since its initial public offering six months ago.

My sense is that other parts of Time Warner would achieve similar results if set free from the conglomerate. Time Warner has proven to be too big, too complex, too conflicted and too slow-moving — in other words, too much like a classic conglomerate — to seize new opportunities. -

Greenspan Warns

Posted by Eddy Elfenbein on December 11th, 2005 at 6:55 pm

AP:Times Online:

Reuters:

AP:

UPI:

Internet:

-

Sarboxed In

Posted by Eddy Elfenbein on December 11th, 2005 at 2:14 pmIn the current New Yorker, James Surowiecki defends Sarbanes-Oxley. I enjoy Surowiecki’s writing, especially his recent book, “The Wisdom of Crowds.” My problem, however, is that his article doesn’t defend the law itself, in fact Surowiecki calls it “decidedly flawed,” but he defends the law due to its good intentions.

Surowiecki writes that fraud was “becoming endemic” on Wall Street, and that there were “nearly a thousand earnings re-statements” between 1997 and 2002. But an earnings restatement isn’t an admission of fraud. Under current accounting rules, a company can legally—and I might add, ethically—report wildly different earnings for a given quarter. The reason accounting rules are so complex is because it’s a complex thing to do.

Surowiecki says that “fraud cost investors and lenders an enormous amount of money, vaporizing hundreds of billions of dollars in shareholder value.” Fraud is already illegal, and there’s no economic incentive to lie. If a guy in a bar tells a girl that he’s a billionaire, that fact that she may believe him has no effect on his bank account.

The tech bubble, much like the tango, needs two parties—companies and an investing public. Business Week had a fascinating article about how Cisco (CSCO) managed its earnings. On the last day of the quarter, the company frantically loaded boxes on to trucks so it could record them as “sold” for accounting purposes (and yes, that’ the rule).

Do you want to point the finger at Cisco and say what a horrible company they are? Fine, go right ahead. Oh by the way, here’s another fact. When midnight came, Cisco failed. The company had to report that it missed earnings by a wee penny a share. The stock promptly dropped 13%. Now, is it still Cisco’s fault?

While Sarbanes-Oxley has good intentions, the law is not increasing transparency. The law has fueled a private equity boom that’s decreasing transparency. Sarbanes-Oxley has also a huge boon for the accounting industry. Just look at the stock chart of a company like Resources Connection (RECN).

So far, the public hasn’t realized how dramatically Sarbanes-Oxley has hurt corporate efficiency. Autodesk (ADSK) said that 130 of its 135 internal auditors are solely focused on Sarbanes-Oxley. In the spirit of Sarbanes-Oxley we need an honest accounting of this misguided law’s true impact.

For more on Sarbanes-Oxley, you can read this, this and this. -

Extreme Makeover: The QQQQ Edition

Posted by Eddy Elfenbein on December 10th, 2005 at 4:26 pmIt’s mid-December and that means it’s time for two things—effeminate claymation elves and the Nasdaq 100 (^NDX) rebalancing. For now, let’s focus on the latter.

This year, the gatekeepers of the Nasdaq 100 have decided to add 12 new stocks, while 12 current members have been voted off the island. The tribe has spoken. And in Wall Streetistan, this tribe speaks very loudly.

If you’re not familiar with the Nasdaq 100, it’s hard to overemphasize how important it is. To quote Reuters:There are 22 U.S. mutual funds and nine international funds linked to the index, which also serves as a benchmark for some 400 related options, futures and other products.

The Nasdaq 100 index is vital to traders. It’s represented by the Mac Daddy of all ETFs, the QQQQ. The Nasdaq 100 is the 100 largest non-financial stocks on the Nasdaq. For many years, this effectively made the index a proxy for large-cap tech stocks. These were all the must-own stocks of the 1990s.

But many investors don’t realize that the index has changed a lot over the past few years. As the tech bubble burst, each December more techs stock have been yanked and replaced with non-tech names. For example, Bed, Bath & Beyond (BBBY) and Expeditors (EXPD) are now members.

It’s still a tech heavy index, but it’s nowhere near as techirific as it used to be. The daily changes of the Nasdaq 100 used to have a 97%-98% correlation with the daily changes of the S&P 500 Tech Index. That’s now down to 85% and by glancing at this year’s replacements, it’s going to go even lower.

Some of the new stocks are in the classic QQQQ mold—Google (GOOG) and Nvidia (NVDA). But there are also stocks like Urban Outfitters (URBN) and Patterson-UTI Energy (PTEN). These new guys are having a major impact. In fact, I think a better way to trade tech stocks now is not with the QQQQ but with the XLK—the S&P Tech Spyders. I should add that right now, neither of those indexes has the action of the S&P 500 Energy Spyders, the XLE.

Now if you’ll excuse me, they’re about to show the part with the Abominable Snowman. -

The Market Today

Posted by Eddy Elfenbein on December 9th, 2005 at 7:00 pm

Today was a good lesson on the benefits of diversification. Even though Frontier Airlines (FRNT) got slammed due to a downgrade from Goldman Sachs, our Buy List not only closed higher, but edged out the S&P 500.

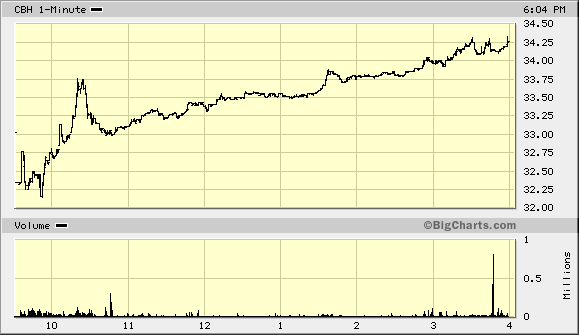

For the record, Frontier fell 7.3% to $7.91 a share. The S&P 500 gained 0.28% and our Buy List rose 0.39%. Not a bad day. We were helped by strong gains from Zimmer Holdings (ZMH), Progressive (PGR) and Commerce Bancorp (CBH).

Commerce rose despite issuing an earnings warning. What caused the stock to climb?

Perhaps the stock rose due to Jim Cramer’s article “Let the Bears Raid Commerce Bancorp.” I don’t have access to Cramer’s article, but here’s the free blurb:Seems the big money can’t wait for the Fed to finish and is taking up Commerce on its lower guidance. The compression to its net interest margin could have sent it below $30, if people hadn’t realized that was in the cards. I still expect a bear raid on Commerce, but now am confident enough to take the other side of it.

And here’s today’s movement in CBH:

I think there’s a good chance that Cramer’s article moved the stock. I don’t have any proof, and I don’t have any complaints either. He’s liked Commerce for a long time. But here’s my problem. This is how Matthew Goldstein at Cramer’s company, TheStreet.com, summarized today’s Commerce news.In September, the bank warned that analysts had to reduce their earnings estimates for both the third and fourth quarters. When Commerce issued the warning, analysts had been looking for fourth quarter earnings of 49 cents a share.

For next year, the bank says it expects to earn between 40 cents and 42 cents a share in the first quarter. The consensus estimate before the update had the bank earning 44 cents a share.

Investors, however, ignored the bad news. In midday trading Friday, Commerce shares rose 31 cents, or 1%, to $33.34.Couldn’t he find any room to mention the possible influence of his own company’s article?

In other news, Business Week discovers Expeditors (EXPD). Lastly, two stocks on our Buy List that look especially cheap right now are Fiserv (FISV) and Lincare Holdings (LNCR). Also, I’m just about positive that I’m going to add Bed, Bath and Beyond (BBBY) to the 2006 Buy List. The stock dropped from $44 on Tuesday to $41.99 today.

I hope everyone has a great weekend! -

Cool Links

Posted by Eddy Elfenbein on December 9th, 2005 at 4:29 pmHere are some very good stock bloggers that I’ve been reading lately:

The Mess That Greenspan Made

The Stalwart

Abnormal Returns

Under the Counter

Naked Shorts

Check ’em out. I’ll be here when you get back.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His