-

Support.com: The Latest Meme Stock

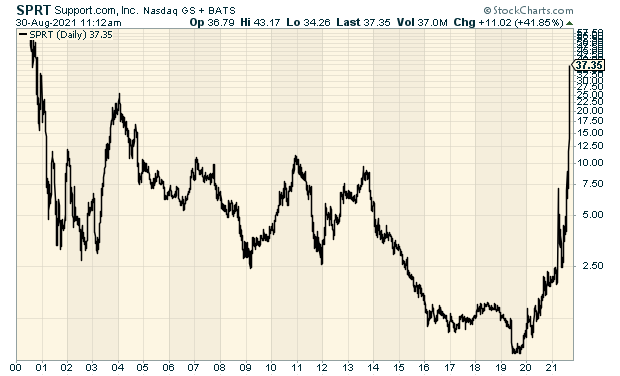

Posted by Eddy Elfenbein on August 30th, 2021 at 11:07 amThe latest meme stock is Support.com (SPRT). No, I don’t know anything about it either except it goes up a lot. SPRT is up 40% today, and that comes on top of being up 33% on Friday.

Going back to last Monday’s low, Support.com is up 315%. It’s actually down a lot from Friday’s intra-day high.

So what do they do? Beats me. This is from their recent earnings report:

Support.com, Inc. (NASDAQ:SPRT) is a leading provider of customer and technical support solutions and security software delivered by home-based employees. For more than twenty years, the company has achieved stellar results for enterprise clients, leading businesses, and consumers. Support.com efficiently meets rapidly-changing market needs with a highly-scalable homesourcing model, IoT expertise, omnichannel solutions, and proprietary software. With no bricks and mortar facilities, no commuting, and a secure cloud-based infrastructure, Support.com is a global leader in sustainability.

Hmmm. I’m still not clear on what they do. Here’s the long-term chart:

-

“Being Bullish Brings a Competitive Advantage”

Posted by Eddy Elfenbein on August 30th, 2021 at 9:53 amThe blogger at Dividend Growth Investor linked to this interview with Nick Train. In it, Train shares a lot of investing wisdom. Here’s a sample.

John Templeton once said, “History shows that time, not timing, is the key to investment success. Therefore, the best time to buy stocks is when you have money” – a philosophy you share. What would you do in a 1999 or2007- like scenario? Continue to invest? Yet another view says, “Wait till there is ‘blood in the streets’.” How do you reconcile these two?

I have never suffered from any delusion that I am an unusually smart or far-sighted investor. A keen sense of my many investing Imitations means I have had to keep my approach simple. I am mostly concerned with avoiding obviously bad or ‘losing’ investment behavior such as over-trading or backing low-quality companies and I’m willing to stick with basic investment principles that seem to me likely to work over time, even accepting there will be periods when they don’t.

Your first question is a good example. For a while, as an inexperienced investment professional, I tried to judge whether equity markets were cheap or expensive. I even allowed myself to express pessimistic views about market prospects in public and, worse, to act on them.

Now looking back over the thirty or more years of my career, it seems to me every one of those negative calls I made on markets was just plain wrong. They’ve gone up a lot over time and in hindsight there was always something to be enthused about. And likely there always will be.

Eventually I acknowledged, for me, the futility of such guesswork about market levels and concluded that it makes good commercial, investment and – perhaps most importantly – emotional sense to be permanently bullish.

This, I believe, is good, ‘winning’ investment behavior. Being bullish brings a competitive advantage over the many market participants who are either negative because that is their habitual outlook on life (an outlook that tends to overstate temporary problems and to underestimate human problem-solving ingenuity) or who back themselves to trade in and out of equity markets on the basis of their hunches about market levels; or both.

Of all the losing investment approaches out there, that of being a pessimistic trader must be the most certain to lead disappointing returns. So I practice the exact opposite – I’m an optimistic buy-and-holder. In this way I put history on my side, given the long-term propensity of stock markets to rise over time, Anglo-Saxon ones at least. In addition, I feel a lot better about myself — optimism keeps you young!

You can see the whole thing here.

-

Morning News: August 30, 2021

Posted by Eddy Elfenbein on August 30th, 2021 at 7:08 amOil and Gas Futures Gyrate After Ida Disrupts Production

Mississippi River is Flowing in Reverse as Ida Pushes Inland

China Sees Skilled Labor Shortages Worsening Amid Tech Push

China Slashes Kids’ Gaming Time to Just Three Hours a Week

Billionaire Paulson Who Shorted Subprime Calls Crypto ‘Worthless’ Bubble

Biden’s Alliance with Big Tech Shows a Power Shift

The Social-Media Stars Who Move Markets

The World Is Still Short of Everything. Get Used to It.

Housing Affordability to Worsen Near-Term, Even as Prices Cool Off

Singapore’s Shopee Changes the Game in Brazil’s e-Commerce Sector

McDonald’s, Others Consider Closing Indoor Seating Amid Delta Surge in U.S.

Demand Surges for Deworming Drug for Covid, Despite No Evidence It Works

Australia’s Fortescue Sets Sights on Becoming World’s First Supplier of Green Iron Ore

The ‘Best Places to Live’ May Not Be the Best Places to Live

How the Left Wrist Became the Right Wrist for Watches

FTC Interviewed Zuckerberg in 2012 Making Facebook Suit Hard

Schemer or Naïf? The Trial of Elizabeth Holmes

Be sure to follow me on Twitter.

-

The S&P 500 Breaks 4,500

Posted by Eddy Elfenbein on August 27th, 2021 at 3:20 pmThis morning, the government released the personal income and spending numbers for July. This report always comes out the day after the GDP report. Personal income gained 1.1% while spending rose 0.3%. The slowdown in spending is probably due to the delta variant.

Over the last year, the core personal consumption price index is up by 3.6%. That’s the fastest growth rate in 30 years. This is the Fed’s preferred measure of inflation.

Atlanta Fed President Raphael Bostic told CNBC on Friday that business contacts in his region have told him they see inflation persisting beyond the near-term time frame.

“We don’t want and we really can’t afford to have inflation that is too high, because people at the lower end of the spectrum are going to be hurt pretty significantly,” he told CNBC’s Steve Liesman during a “Squawk Box” interview.

Much of the current inflation pressure is coming from energy and food, which rose 23.6% and 2.4%, respectively, from a year ago.

The stock market doesn’t seem too bothered. The S&P 500 is up to another new high. The S&P 500 broke 4,500 today. It first topped 45 on September 16, 1955. It then broke 450 on March 8, 1993. Going way back, the index last broke 4.5 on July 11, 1932.

-

Morning News: August 27, 2021

Posted by Eddy Elfenbein on August 27th, 2021 at 7:02 amPushing the Limits Paid Off for Didi, Until China Cracked Down

China Blasts ‘996’ Excessive Work Culture

Bitcoin Helped Tank El Salvador Bonds. Now They’re Rising Back.

Exit Game: Central Banks’ Shift From Crisis Policies Gathers Momentum

Gold Is Out, Bonds Are In for Investors’ Jackson Hole Playbook

Fed’s Bostic Says ‘Reasonable’ to Begin Bond-Buying Taper in October

Billionaire-Backed Stock Picker Says Bubble Talk Is for Boomers

Supreme Court Scraps Biden’s Eviction Protection for Tenants

Apple Settlement Gives App Developers a Way to Avoid Its Commission

Tim Cook Receives Over 5 Million Shares of Apple Stock Worth $750 Million

Barclays Buys $3.8 Billion Gap Credit Card Portfolio in the U.S.

Peloton Stock Is Falling Because the Stay-at-Home Trade Is Definitely Over

German Publisher Axel Springer to Acquire U.S. News Website Politico for Over $1 Billion

FedEx Ground Delivery Becomes a Road to Riches for Contractors

Why Kanye West’s Name Change Could Make Him Richer

Be sure to follow me on Twitter.

-

51 Record Closes This Year

Posted by Eddy Elfenbein on August 26th, 2021 at 10:38 amThe stock market closed at another all-time high yesterday. It’s the 51st new high of this year. The market is down a little this morning. Once again, the high beta stocks are beating up on the low vol stocks. This has been the trend lately.

The August jobs report will come out next Friday. This morning, we got another jobless-claims report and for the first time in five weeks, jobless claims increased but only slightly. Jobless claims were 353,000 which is very close to another pandemic low.

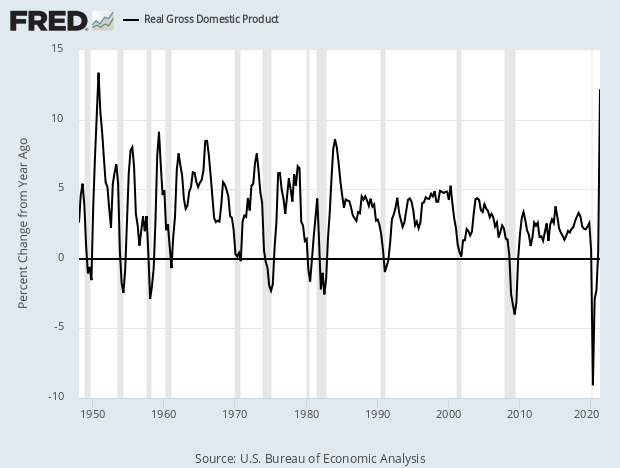

We also got our first revision to the Q2 GDP report. The initial report said the economy grew by 6.5% in Q2. Today that was revised up to 6.6%. Wall Street had been expecting an increase to 6.7%. We may see the fastest full-year GDP growth since the 1980s.

The economy has grown by over 12% in real terms over the last four quarters. That’s the fastest rate in 70 years. Of course, that’s largely due to last year’s plunge.

-

Morning News: August 26, 2021

Posted by Eddy Elfenbein on August 26th, 2021 at 7:09 amSouth Korea’s Rate Hike Suggests It’s Not Too Worried About Delta

Spies for Hire: China’s New Breed of Hackers Blends Espionage and Entrepreneurship

Google and Microsoft Promise Billions to Help Bolster US Cybersecurity

India Urges Its Automakers to Cut Reliance on Imports From China

The World Economy’s Supply Chain Problem Keeps Getting Worse

Maersk’s Green Ships Have First-Mover Disadvantage

Vaccinated Democratic Counties Are Leading the Economic Recovery

Virtual Jackson Hole Underscores Uncertainty in Fed’s Next Steps

Inflation Could Stay High Next Year, and That’s OK

How Should the Fed Deal With Climate Change?

The Hybrid Work Revolution Is Already Transforming Economies

Delta’s Extra $200 Insurance Fee Shows Vaccine Dilemma for Employers

Rent-a-Robot: Silicon Valley’s New Answer to the Labor Shortage in Smaller U.S. Factories

Dollar General Forecasts Bleak Profit View As Transport, Raw Material Costs Bite

Dollar Tree Cuts Full-Year Earnings Forecast

Why the Baby on Nirvana’s ‘Nevermind’ Album Is Suing Now

Be sure to follow me on Twitter.

-

Broadridge: “A True Monopoly”

Posted by Eddy Elfenbein on August 25th, 2021 at 12:15 pmThe Financial Times profiles Broadridge Financial Solutions (BR). The FT calls them “an obscure but lucrative Wall Street utility.” That sounds about right. They note that Broadridge holds a market share of 80%, and that’s not sitting well with some mutual funds.

The New York Stock Exchange regulates fees for investor communications, setting a cap of 25 cents a report. Broadridge charges the full 25 cents for an email, according to analysts. It costs more than for paper mailings because of a 10 cent fee that Broadridge charges to review whether shareholders prefer email over paper, according to the company.

The fees vastly exceed the cost, according to the Investment Company Institute, a trade group for the fund industry in Washington. For investor accounts not held through a broker, a typical fund paid 5 cents to send a shareholder report by either email or paper mail exclusive of postage, ICI said.

(…)

The payrolls company Automated Data Processing spun off Broadridge in 2007. In the fiscal year ended June 30, Broadridge reported a record $5bn in revenue and $902m in adjusted operating income, equal to an operating profit margin of 18 per cent.

Most of the company’s revenues and profits derive from the Broadridge “investor communication solutions” business, which includes organising virtual shareholder meetings and votes, an area that was increasing in popularity even before the pandemic and has since boomed.

In 2019 it handled more than 90 per cent of proxy voting services for public companies and mutual funds in the US, according to the company, whose annual report states, “We operate in a highly competitive industry.”

Broadridge recently said it made $2.19 for its fiscal Q4. That matched Wall Street’s consensus. That was a 13% increase over the same quarter last year. Full-year EPS was $5.66. That’s up nicely from $5.03 per share last year.

The company increased its quarterly dividend from 57.5 cents per share to 64 cents per share. That’s an increase of 11.3%. This is Broadridge’s 15th annual dividend increase in a row. In eight of the last nine years, the dividend has increased by double digits.

For the coming year, Broadridge expects earnings growth of 11% to 15%, recurring-revenue growth of 12% to 15% and operating margins around 19%. That translates to earnings for this year of $6.28 to $6.51 per share.

-

Morning News: August 25, 2021

Posted by Eddy Elfenbein on August 25th, 2021 at 7:08 amThe Pandemic Is Testing the Federal Reserve’s New Policy Plan

Inflation vs Jobs Hole: A Tradeoff the Fed Still Hopes to Skirt

SEC Chief Warns ‘Clock Is Ticking’ on Delisting Chinese Stocks

Banks Are Bingeing on Bonds, but Not Because They Want To

Biden’s Cybersecurity Summit Will Gather Very Important People to Solve America’s Hacking Problem

Desperate U.S. Cities Pitch Wall Street-Style Sign-On Bonuses

U.S. Holds Largest Sale of Strategic Oil Reserves in 7 Years

Higher U.S. Food Benefits Give Legs to Dollar Stores’ Fresh Food Push

GameStop, AMC Stock Surge in a Rally for Meme Stocks

‘Made in Afghanistan’ Once Symbolized Hope. Now It’s Fear.

Few Women Ascend Japan’s Corporate Ladder. Is Change Finally Coming?

Corporate America’s $50 Billion Promise

Takata’s Ticking Time Bomb Is Still On The Road

Be sure to follow me on Twitter.

-

CWS Market Review – August 24, 2021

Posted by Eddy Elfenbein on August 24th, 2021 at 8:21 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year.)

The S&P 500 closed at another all-time high today. The index is up nearly 20% this year, and we’re not even at Labor Day.

This comes at an interesting anniversary. One hundred years ago today, the Dow Jones Industrial Average closed at 63.90. That was the low point of a nasty bear market that began on November 3, 1919 when the Dow closed at 119.62.

This was a difficult and ugly time for the country. There had been several labor and race riots during the Red Summer of 1919, and in 1921 there was the infamous Tulsa Massacre. The country suffered a long recession that started in early 1920 and didn’t peter out until the summer of 1921.

As is often the case, bad times meant it was a great time to invest. The U.S. was about to embark on the Roaring Twenties. Americans became enthralled by new technologies like radio and movies (and even talking movies!).

The stock market started to boom. Less than one year after the low, the Dow broke 100. By 1925, it hit 150 and by 1927, the Dow topped 200. It nearly doubled again by the summer of 1929. (After that, things got a wee bit problematic.)

Still, the Roaring Twenties was a great time for investors. There were some cracks showing in the façade. Florida, for example, experienced a massive real estate bubble. This was lampooned in the Marx Brothers’ first movie, The Cocoanuts.

Groucho: You can have any kind of a home you want. You can even get stucco. Oh, how you can get stuck-oh!

The Dow had a fantastic run lasting eight years and ten days. The Dow rose nearly sixfold in that time. The index eventually peaked at 381.17 on September 3, 1929. While that was the high, the market didn’t break for another seven weeks. Interestingly, market crashes usually don’t happen at the peak. Instead, they happen on downward slides from the peak.

In this issue, I want to address a topic that I’m often asked about: how I go about selecting stocks to invest in. I like to find companies that have a competitive advantage. Warren Buffett refers to this as a company that has a strong “moat” protecting it. This concept is sometimes misunderstood, and I wanted to take some time to explain what it properly means.

Finding a Competitive Advantage

With investing I like to find companies with a distinct competitive advantage. Here’s a good way to think about this (I’m heavily borrowing from our friends at Investopedia for this example).

Let’s say you have a lemonade stand and business is going well. You suddenly have an idea. Normally, your stand buys lemons each morning. Instead of doing that, you decide to buy a bunch of lemons at the beginning of the week. Your supplier gives you a bulk discount.

Let’s say this cuts your cost of goods sold by 20%. In terms of economics, this is a huge deal. In fact, an innovation like this is what all business is about. This means you can cut your prices by 20%, thereby gaining market share, and it will have zero impact on your gross profit margins. This is great news for you and your business.

As much as we love this, there’s one small problem. While it’s a great idea, it’s just an idea—and one that can be easily copied by your competitors. Once they discover the secret, your advantage is gone.

Now let’s say you come up with a second idea. You invent a revolutionary new lemon squeezer that’s so good, you get 20% more juice out of each lemon. Once again, this is a huge deal in terms of business economics. You’re effectively cutting your costs of goods sold by 20%, and again, you can pass those savings on to your customers with no impact on your gross margins.

But there’s a crucial difference between the first example and the second. In the second case, you can patent your lemon squeezer. That means you can line up state power to enforce your invention monopoly. The idea in the first example isn’t protected the same way. (In reality, you’d probably license your technology and draw a revenue stream.)

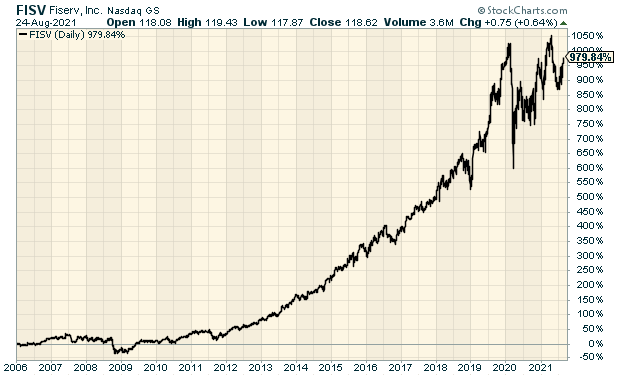

The second example shows the kind of company I look for. I look for firms that do things that no one else can do. Several stocks on our Buy List have strong competitive advantages. In particular, I think of companies like Moody’s (MCO) or Fiserv (FISV).

Check out our tenfold gain in Fiserv.

Keep the Competition Out

Harvard professor Michael Porter has said that a business is first and foremost concerned with differentiating itself and keeping competitors out. Ideally, you want to have a business with high barriers to entry and low barriers to exit, and you want to differentiate yourself with whatever it is you do. You can do that by exclusivity or by price. That’s your competitive advantage. Once you get that, then you get better managers, better advertising and a stronger brand name. But it starts with a competitive advantage.

I think people often have difficulty with the concept of competitive advantage because they want to see sinister forces at work. And make no mistake: I do believe the tempering forces of free enterprise can sometimes break down and give a particular firm a lasting advantage that has nothing to do with its own inherent merit. It could be that they were in the right place at the right time. Or they can use their excess profits to lobby the government to protect their advantage.

For example, many years ago, the Japanese government gave AFLAC (AFL) a monopoly on selling cancer insurance, and this translated into a huge market share today. Naturally, this is unsettling to those of us raised on the idea that the world wants a better mousetrap. But the truth is, it doesn’t. It wants the one it’s heard of. Just like in politics, the incumbent holds a lot of power.

Here’s an example. One of my friends who works with the U.S. Navy explained to me that there are only a handful of shipyards left that are capable of building modern, large-scale ships for the Navy. These shipyards have become, in effect, government sponsored quasi-monopolies. I doubt anyone wanted that to happen, but things turned out that way.

This is an important point that Warren Buffett has often discussed. Nowadays, Buffett is the “aw shucks” face of nice-guy American capitalism, but it wasn’t always this way. In the 1970s, he and Munger bought the Buffalo Evening News.. The Buffalo Courier-Express, a rival newspaper, did everything it could to make them seem like evil out-of-town capitalists. Buffett was beaten up hard in the press, and I think that episode has stayed with him ever since.

In the court case that followed, the opposing lawyer used Buffett’s words against him:

Warren Buffett once said that owning a monopoly newspaper was like owning an unregulated toll bridge. His words were, “…in an inflationary world, a toll bridge would be a great thing to own if it was unregulated.” When he was asked for his rationale, he said, “Because you have laid out the capital cost. You build the bridge in old dollars and you don’t have to keep replacing it.” He was then questioned whether he used the term “unregulated” to mean the ability to raise prices. Buffett said, “That is true.”

It sounds rough, but that’s about the best description of a competitive advantage I can think of. With that said, how do you know if a company has a strong competitive advantage? There are a few characteristics that typically show up.

What Does a Competitive Advantage Look Like?

Oftentimes, the company we’re looking at has a consistent operating history. Sales and earnings edge higher nearly every year. There may be bad years, but the positive trend is clear.

This tells me a few things about the business. First and most obviously, it’s a growing enterprise with a steady demand for its products. It also tells me that management is probably on the ball. That’s because in a dynamic marketplace, you need to make a lot of small corrections to keep the ship moving.

A company with a consistent operating history also probably has a loyal customer base. Never overthink a business. You can make a lot of money selling the same thing to the same people. Ask Starbucks (SBUX

The coffee shop went public in 1992 at $17 per share. Since then, it’s split 2-for-1 six times. That comes to 64-for-1 which means the adjusted IPO price is about 27 cents per share. SBUX closed today $115.08.

Lastly, investing in companies with a consistent track record is an easy way of reducing risk. I’m not a fan of “oil well” stocks. These are companies that appear flat broke but are pinning all their hopes on some deal that may never come. There are too many of these stocks around. When in doubt, I always prefer a stock that grows its business each year.

Tying back to what Buffett said before, a company with a strong moat should also be able to raise prices. This is a subtle rule, so let me explain what I mean.

You’ll notice that I didn’t say I look for companies that do raise their prices. Rather, the key is finding ones that, if the need arises, can raise their prices.

Think about the items in your home or office. Now imagine which ones you would still buy even if they raised their price by 10% or 15%. Some items you’d simply stop buying. But not all.

Why? Maybe you’re attached to a certain item. Or maybe it’s an integral part of your day. I have friends who would make their daily Starbucks run no matter what.

A company that can raise its prices most likely has a firm handle on its costs. There’s a risk component as well. No company wants to raise prices, but it’s nice to be in a position where they can do so if need be.

Ability to raise prices is often a sign that a company has a dominant position in its market. I often think of Harley-Davidson (HOG), the legendary hog stock and former Buy List member.

Is Harley-Davidson a monopoly? Well, in the legal sense, of course not. There are lots of motorcycle companies. Yet Harley is a brand so differentiated that it can be thought of as a pseudo-monopoly. Harley buyers would never view their hogs as just another bike. Harley is quite aware of this (a good portion of their revenue is apparel).

I also like to see a company that is the dominant player in a niche market. A company doesn’t have to own the world to be successful. Owning the best autobody shop in town, or the best Thai restaurant in town, can be a great business.

Why? Because the firm is doing something no else can do. In business, there’s a term called “switching costs.” This refers to the cost for a consumer to change his or her preference. With toothpaste, folks aren’t so picky. With eating habits, people can be very picky. Ross Stores (ROST) is a good example of a company with fairly tight margins (net income margin is around 10%), but high switching costs. Ross’s customers like it exactly where it is.

For a business, you want to be the dominant player, even if it’s in a very narrowly-defined market. Think of the ratings agencies. If you want to float a bond, you pretty much have to deal with Moody’s or S&P.

On our Buy List, we have Broadridge Financial Solutions (BR). This is the dominant player in share-voting proxies. This is the kind of business not one person in 20 ever thinks about, but it fills a concrete need. You can spot a dominant player because it often has modest debt levels, wide operating margins and strong cash flow.

I want to touch on First-Mover Advantage. This was a huge idea in the 1990s, and I think it served as unrecognized fuel for the Tech Bubble. The idea also goes by the name Winner-Take-All.

The idea is that an early entrant could establish an industry standard which remains in place simply because it’s already there. It’s not better—it’s just there. I can’t tell you how many times I was told that some Internet stock was just like the QWERTY keyboard.

In the 1990s, Microsoft was an obvious example of a first mover that became enormously successful, but investors wanted to see where the next standard would be. There was even a magazine called the Industry Standard. Wikipedia tells us that “in 2000, it sold more ad pages than any magazine in America.” Unfortunately, the magazine went belly-up in August 2001.

While being a first mover can certainly give one a competitive advantage, it doesn’t mean it will last. It’s also a bit more complicated than being first. For example, it’s nice to have lots of upgrade cycles.

I hope this issue has helped you better understand what competitive advantage is, and how it can help your investing. If you want to see a list of companies with competitive advantages, you can see my Watch List (subscriber only). Another good resource is the holdings of the VanEck Vectors Morningstar Wide Moat ETF (MOAT). I don’t always agree with them, but at least we’re looking for the same things.

I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you haven’t had a chance, you can subscribe to our premium newsletter. It’s only $20 a month or $200 a year. Please join us!

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His