-

CWS Market Review – March 6, 2020

Posted by Eddy Elfenbein on March 6th, 2020 at 7:06 am“The stock market is going to fluctuate. Sometimes it will fluc down; other times it will fluc up.” – Louis Rukeyser

In last week’s issue, I wrote, “I think there’s a good chance the Fed will cut rates before the next meeting.”

Sure enough, that’s exactly what happened. On Tuesday, the Federal Reserve cut interest rates by 0.5% two weeks before its scheduled meeting. And the market responded…by falling flat on its face. The S&P 500 fell by 2.8%, which came after one of the market’s best days in decades.

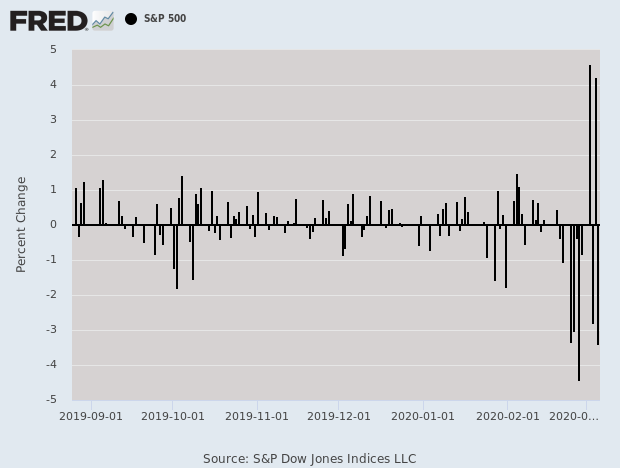

So how come a rate cut didn’t work? Well, as much as we hope, low rates won’t cure any virus. Simply put, the market is on edge right now. It’s hard to state just how volatile the market has become. It hasn’t been like this in years. Check out the daily changes for the S&P 500.

Consider some stats. The S&P 500 has now closed up or down by more than 2.5% for four straight days. It hasn’t done that in more than eight years. At one point, the S&P 500 closed up or down by more than 4% three times in five days. In the eight years prior to that, it happened just twice. (For that last stat, Brian Sullivan gave me a shout-out on CNBC.).

Trading Nation and @EddyElfenbein got a shout-out from @SullyCNBC on tonight's @CNBCFastMoney. Aw, shucks. pic.twitter.com/QWEW9fDxdX

— Trading Nation (@TradingNation) March 4, 2020

In this week’s issue, I’ll break down what’s happening, and more importantly, I’ll tell you how to position yourself. But I’ll warn you, it’s very likely we’re not done just yet. I’ll also update you on this week’s earnings report from Ross Stores. The deep-discounter beat earnings and hiked its dividend, but guidance wasn’t so hot. I’ll have more on that in a bit. But first, let’s look at the Fed’s surprise rate cut.

The Fed Cuts Rates and the Market Drops

I’d like to credit my Fed prediction to my wisdom and sagacity. In reality, I simply saw that the Fed had few other choices. They had to cut, and cut fast. The stock market was plunging, bonds were soaring and commodity prices were in free fall.

I like to follow the “break evens.” That’s basically the market’s estimate for what inflation will be. The 10-year break-even had dropped sharply in just a few days. That was a clear sign from the market that a rate cut was needed. The entire TIPS (Treasury Inflation Protected Securities) yield curve is negative. I wasn’t surprised to see that the Fed’s vote this week was unanimous.

In its statement, the Fed said, “The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity.” We may see negative rates soon.

Of course, lower rates won’t do much to stop the spread of coronavirus, but they may help soften the economic dislocations caused by the virus. Cruise stocks, for example, have been creamed. Many airline stocks are near multi-year lows. Natural gas is at a four-year low.

I think it’s likely that economic growth will take a hit this year, but it’s too early to say how long and by how much. But the slide in the yield of long-term bonds suggests that Wall Street isn’t expecting much in terms of growth this year. At a first guess, I’d say we can expect a flat economy with 0% growth. Look at how steeply the 10-year yield fell.

The fallout from the world of the coronavirus isn’t always so obvious. For example, shares of Clorox (CLX) have done well. Makes sense once you think about it. Campbell Soup (CBP) is also up. (People staying at home?)

Quick quiz: Guess what country’s stock market just hit a fresh two-year high?

Give up? The answer may surprise you. It’s China. “The blue-chip CSI 300 Index jumped 2.2% on the day to 4,206.72, its highest point since February 2018.” In China, seven of 31 provincial-level governments have pledged to spend $505 billion on infrastructure projects. That’s a staggering number and it will get even bigger as other cities join in. I’m curious to see if the U.S. will do something similar.

I also want to point out that our Buy List continues to do well in a relative sense. Outperforming in a down market is a key aspect of long-term success. I don’t yet have Friday’s final numbers, but it looks like our Buy List is set to outperform the S&P 500 for the fifth week in a row. Since our portfolio is focused on high-quality stocks, it tends to fare better in downdrafts. We also beat the market last year in a strong up year. Since February 20, the S&P 500 has shed 10.52%, but our Buy List is down by 8.97%.

What to Do Now

There are three things to do now.

1. Do not panic and sell.

2. Expect more volatility. We’ll probably retest the low.

3. Pick up bargains with any free cash.I’ll restate the Peter Lynch quote from last week: “The real key to making money in stocks is not to get scared out of them.”

I can’t predict that we’ve already seen the low. Going by historical patterns, we probably haven’t. The market likes to test and retest prior low points. Last Friday, the S&P 500 got down to 2,855.84. I think we’ll test that soon. If it breaks, then the bears will be back. On Thursday, the S&P 500 closed below its 200-day moving average, which is not an encouraging sign.

Now to point #3. What bargains? Thanks to the downturn, some of our Buy List stocks look pretty good. Here are three:

Shares of AFLAC (AFL) are quite attractive here. The stock has gotten seriously beaten. Remember that most of their business comes from Japan. In fact, the company had a coronavirus case in one of its call centers. The shares are now down more than 25% from their 52-week high.

Don’t forget how well run this company is. Going by yesterday’s close, AFL currently yields 2.7%. That’s a solid dividend, too. Last month, AFLAC raised its dividend for the 37th year in a row. For 2020, the duck stock expects earnings of $4.32 to $4.52 per share. I think there’s a chance that AFL many lower guidance at some point.

I’m dropping my Buy Below down to $46 per share, but if you can pick up AFL below $42, then you’ve made a good deal.

Globe Life (GL) also looks very good in this range. For 2020, Globe life expects earnings of $7.03 to $7.23 per share. That gives the stock a P/E Ratio of less than 13. I’m lowering my Buy Below to $100 per share, but if you can get GL below $90, that’s a very good entry price.

I also like Check Point Software (CHKP). The stock recently hit a 52-week low. The last earnings report was pretty good. I’m dropping my Buy Below price on Check Point to $110 per share.

The selloff has thrown several of our Buy Below prices off. I don’t think it’s worthwhile to do a mass adjustment in one issue, but I’ll gradually readjust several Buy Belows over the next few weeks.

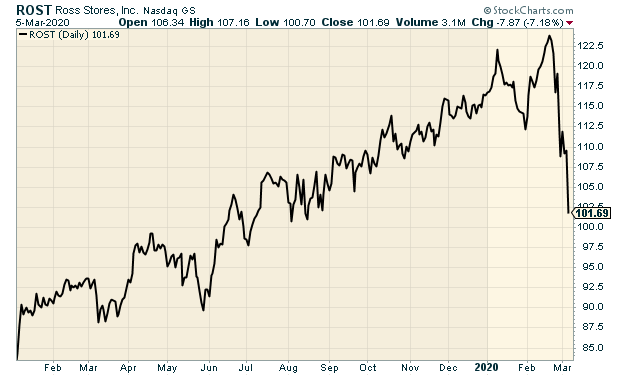

Ross Stores Beats Earnings and Raises Dividend

On Tuesday, Ross Stores (ROST) reported fiscal Q4 earnings of $1.28 per share. This was for the months of November, December and January. That’s the key holiday-shopping season for Ross. Previously, Ross had given us a range of $1.20 to $1.25 per share.

They key stat to watch for any retailer is same-store sales. For Ross, that rose by 4% last quarter. Ross has been expecting same-store sales growth of 1% to 2%. For the year, Ross made $4.60 per share. That’s up from $4.26 in 2018. Annual sales rose 7% to $16.0 billion.

Barbara Rentler, Chief Executive Officer, commented, “We delivered strong sales and earnings growth for both the fourth quarter and fiscal year. Our ongoing ability to offer compelling bargains to our customers enabled us to achieve these results despite our own challenging multi-year comparisons and a fiercely competitive holiday season.”

Ms. Rentler continued, “Fourth quarter operating margin of 13.3% was slightly better than expected, driven by higher merchandise margin.”

During Q4, Ross bought back 2.7 million shares for $309 million. For the year, they bought back 12.3 million shares for $1.275 billion. There’s still $1.275 billion left in the current authorization.

Ross also raised its quarterly dividend by 12%. The quarterly payout will rise from 25.5 cents to 28.5 cents per share. The new dividend is payable on March 31 to stockholders of record as of March 17. Ross has raised its dividend every year since 1994.

Now for guidance:

For the 52 weeks ending January 30, 2021, the Company is planning same-store sales to grow 1% to 2% and earnings per share of $4.67 to $4.88. We also plan to open about 100 stores this year, consisting of approximately 75 Ross Dress for Less and 25 dd’s DISCOUNTS locations.

For the first quarter ending May 2, 2020, comparable-store sales are forecast to be up 1% to 2% with earnings per share projected to be $1.16 to $1.21 versus $1.15 for the first quarter ended May 4, 2019.

That’s not so hot, but I think Ross is playing it safe. Wall Street had been expecting $1.25 per share for Q1 and $5.01 per share for the year. The stock just fell to a six-month low. I still like Ross, but I’m lowering my Buy Below price to $110 per share.

That’s all for now. The jobs report is due out later today. Next week, there’s not much in the way of economic reports. The CPI comes out on Wednesday. I expect it will show more low inflation. Also on Wednesday, we’ll get an update on the Federal budget. The deficit is looking quite large this year. Then on Thursday, we’ll get the weekly jobless-claims report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: March 6, 2020

Posted by Eddy Elfenbein on March 6th, 2020 at 7:01 amCoronavirus Wreaks Financial Havoc as Infections Near 100,000

Bonds Extend Rally as Investors Retreat From Stocks

Sovereign Bond Yield Collapse Shows the World Is in Crisis Mode

It’s Time to Really Fret, Says Manager Who Beat 98% of Peers

Why the Coronavirus Could Threaten the U.S. Economy Even More Than China’s

The Fed is Already Behind the Curve as Goldman Says Firepower Could Be Half as Much as Usual

Mortgage Rates Dip To Lowest Point On Record

Tencent-Backed WeDoctor Invites Banks to Lead $1 Billion Hong Kong IPO

Costco Crushed February Same-Store Sales. It Was the Coronavirus.

Jamie Dimon’s Emergency Heart Surgery Puts Spotlight on JPMorgan’s Bench

Tito’s Vodka: Please Don’t Use Our Booze as Coronavirus Hand Sanitizer

U.A.W. Corruption Case Widens as Former Chief Is Charged

Cullen Roche: Three Things I Think I Think – Corona Edition

Michael Batnick: Don’t Catch a Falling Knife

Ben Carlson: Advice Doesn’t Have to Be Complicated to Be Effective

Be sure to follow me on Twitter.

-

Morning News: March 5, 2020

Posted by Eddy Elfenbein on March 5th, 2020 at 7:27 amGlobal Economy Is Gripped by Rare Twin Supply-Demand Shock

A Global Outbreak Is Fueling the Backlash to Globalization

Larry Kudlow Says ‘We’re Not Going to Panic’ Over the Economy

Dow Futures Tumble as U.S. Coronavirus Cases Increase, California Declares State of Emergency

Fed ‘Beige Book’ Shows Business Worried About Coronavirus and the Election

DealBook: Lloyd Blankfein Says He Knows Why the Market Is Moving

OPEC Backs Extra 1.5 Million BPD Output Cut if Russia Joins In

Airlines May Lose Up to $113B in Revenue – IATA

British Airline Flybe Collapses as Coronavirus Deals Final Blow

HP Rejects Xerox’s Hostile Takeover Offer, Calling Bid Too Low

Nick Maggiulli: How Stocks Perform After the Fed Cuts Rates

Ben Carlson: How Do We Get People to Save More For Retirement?

Michael Batnick: Animal Spirits: The Emergency Rate Cut & Today Was Weird

Joshua Brown: What You Should Buy In A Recession

Jeff Carter: Rearranging Distribution

Be sure to follow me on Twitter.

-

Morning News: March 4, 2020

Posted by Eddy Elfenbein on March 4th, 2020 at 7:05 amGlobal Health Crisis 1, Economic Policymakers 0

The Fed Has No Tools for an Outbreak. Here’s Why It Acted Anyway.

Fed Makes Emergency Rate Cut, but Markets Continue Tumbling

Bonds Hold Gains After Fed’s Surprise Rate Cut

Treasury 10-Year Yield Sets Record Below 1% on Virus Fears

Trump Balks at Stimulus, Saying Economy Is Immune to Coronavirus

A Hedge Fund Pioneer Bets on Higher Rates, Recovery In Stocks

A U.S. Steel Mill Found a Savior in China. Rivals See a Trojan Horse

What Happens in Vegas if No One Stays in Vegas?

How An Ill-Timed Bet On A U.S. Oil Refinery Cost ICBCS Millions

SoftBank-Backed CloudMinds Blocked From Exporting U.S. Tech to China

U.S. Surges Ahead as World’s Top Hotspot for the Fabulously Rich

Ben Carlson: Questions Every Investor Needs To Ask Themselves Right Now

Nick Maggiulli: 3 Reasons Why You Should Invest in Bonds

Joshua Brown: They Did It: The First Emergency Interest Rate Cut Since 2008, Why the Rate Cut “Didn’t Work” & We Might Need a Retest

Be sure to follow me on Twitter.

-

Ross Stores Beats Earnings and Hikes Dividend

Posted by Eddy Elfenbein on March 3rd, 2020 at 5:41 pmRoss Stores (ROST) reported fiscal Q4 earnings of $1.28 per share. This is for the months of November, December and January. Previously, Ross had given us a range of $1.20 to $1.25 per share.

Same-store sales rose by 4%. Ross has been expecting growth of 1% to 2%. For the year, Ross made $4.60 per share. That’s up from $4.26 in 2018. Annual sales rose 7% to $16.0 billion

Barbara Rentler, Chief Executive Officer, commented, “We delivered strong sales and earnings growth for both the fourth quarter and fiscal year. Our ongoing ability to offer compelling bargains to our customers enabled us to achieve these results despite our own challenging multi-year comparisons and a fiercely competitive holiday season.”

Ms. Rentler continued, “Fourth quarter operating margin of 13.3% was slightly better than expected, driven by higher merchandise margin.”

During Q4, Ross bought back 2.7 million shares for $309 million. For the year, they bought back 12.3 million shares for $1.275 billion. There’s $1.275 billion left in the current authorization

Ross is also raising its quarterly dividend 12%, from 25.5 cents to 28.5 cents per share. The new dividend is payable on March 31 to stockholders of record as of March 17. Ross has raised its dividend every year since 1994.

Now for guidance:

For the 52 weeks ending January 30, 2021, the Company is planning same store sales to grow 1% to 2% and earnings per share of $4.67 to $4.88. We also plan to open about 100 stores this year, consisting of approximately 75 Ross Dress for Less and 25 dd’s DISCOUNTS locations.

For the first quarter ending May 2, 2020, comparable store sales are forecast to be up 1% to 2% with earnings per share projected to be $1.16 to $1.21 versus $1.15 for the first quarter ended May 4, 2019.

Wall Street had been expecting $1.25 per share for Q1 and $5.01 per share for the year. The shares are down about 3% after hours.

-

The Fed Cuts by 0.50%

Posted by Eddy Elfenbein on March 3rd, 2020 at 11:06 amMe a few days ago.

I think there's a good chance of a non-meeting rate cut from the Fed.

Soon.

— Eddy Elfenbein (@EddyElfenbein) February 27, 2020

And today.

Federal Reserve issues FOMC statement

The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity. In light of these risks and in support of achieving its maximum employment and price stability goals, the Federal Open Market Committee decided today to lower the target range for the federal funds rate by 1/2 percentage point, to 1 to 1‑1/4 percent. The Committee is closely monitoring developments and their implications for the economic outlook and will use its tools and act as appropriate to support the economy.

The market rallied. For a bit.

-

Morning News: March 3, 2020

Posted by Eddy Elfenbein on March 3rd, 2020 at 7:01 amG-7 to Hold Emergency Call on How to Lift Economy From Virus Threat

Saudis Renew Push for Output Cuts as Coronavirus Weakens Oil Business

Hottest Bond Market in History Is Starting to Make Some Nervous

Could the Coronavirus Cause a Recession (and How)?

Is Fiscal Stimulus the Answer to Preventing a Coronavirus Recession?

DealBook: Capitalists Make Their Case Against Sanders

Thermo to Buy Qiagen for $10 Billion in 2020’s Top Health Deal

SoftBank CEO Tells U.S. Investors He’ll Be More Careful

Amazon Adds Warehouse Network Closer to Cities to Speed Up Same-Day Delivery

Xerox, HP Blame Each Other As Takeover Battle Heats Up

Waymo Brings In $2.25 Billion from Outside Investors, Alphabet

Michael Batnick: Volatility Will Continue

Jeff Carter: The Future of Work Is Automated

Roger Nusbaum: This Past Week As A Micro Example Of Sequence Of Return Risk

Ben Carlson: Talk Your Book: Investing in Commodities, What Happens to Stocks After a Big Down Month?

Be sure to follow me on Twitter.

-

Morning News: March 2, 2020

Posted by Eddy Elfenbein on March 2nd, 2020 at 7:12 amChina Inc Thinks Outside the Box as Coronavirus Keeps Consumers at Home

Virus Pushes Global Economy Toward First Contraction Since 2009

Coronavirus Expected to Hurt U.S. Earnings Harder and Longer

Wall Street Has Lost Its Nerve. What Will It Take to Get It Back?

How to Fight That Sinking Feeling

JPMorgan Sees a $1.2 Trillion Reason to Nix a U.S. Yield Rebound

Think-Tank Report on Uighur Labor in China Lists Global Brands

Where Is Jack Dorsey? Not in the Room as His Twitter Future Debated

Intel’s Culture Needed Fixing. Its C.E.O. Is Shaking Things Up.

Nokia Replaces CEO with Fortum Boss Lundmark to Revive 5G Business

Beyond Meat Shares Plummet Despite Revenue Tripling Year Over Year

Boeing’s Other Headache Is Its Joint Venture With Embraer

Joshua Brown: Reasons to Sell, Updated

Howard Lindzon: Pizza Over Panic

Jeff Miller: Should Investors Heed the Message of the Markets?

Be sure to follow me on Twitter.

-

Buffett’s Shareholder Letter

Posted by Eddy Elfenbein on February 29th, 2020 at 4:42 pmHere’s Warren Buffett’s latest letter to his shareholders. Here’s a sample:

In 1924, Edgar Lawrence Smith, an obscure economist and financial advisor, wrote Common Stocks as Long Term Investments, a slim book that changed the investment world. Indeed, writing the book changed Smith himself, forcing him to reassess his own investment beliefs.

Going in, he planned to argue that stocks would perform better than bonds during inflationary periods and that bonds would deliver superior returns during deflationary times. That seemed sensible enough. But Smith was in for a shock.

His book began, therefore, with a confession: “These studies are the record of a failure – the failure of facts to sustain a preconceived theory.” Luckily for investors, that failure led Smith to think more deeply about how stocks should be evaluated.

For the crux of Smith’s insight, I will quote an early reviewer of his book, none other than John Maynard Keynes: “I have kept until last what is perhaps Mr. Smith’s most important, and is certainly his most novel, point. Well-managed industrial companies do not, as a rule, distribute to the shareholders the whole of their earned profits. In good years, if not in all years, they retain a part of their profits and put them back into the business. Thus there is an element of compound interest (Keynes’ italics) operating in favour of a sound industrial investment. Over a period of years, the real value of the property of a sound industrial is increasing at compound interest, quite apart from the dividends paid out to the shareholders.”

And with that sprinkling of holy water, Smith was no longer obscure.

It’s difficult to understand why retained earnings were unappreciated by investors before Smith’s book was published. After all, it was no secret that mind-boggling wealth had earlier been amassed by such titans as Carnegie, Rockefeller and Ford, all of whom had retained a huge portion of their business earnings to fund growth and produce ever-greater profits. Throughout America, also, there had long been small-time capitalists who became rich following the same playbook.

Nevertheless, when business ownership was sliced into small pieces – “stocks” – buyers in the pre-Smith years usually thought of their shares as a short-term gamble on market movements. Even at their best, stocks were considered speculations. Gentlemen preferred bonds.

Though investors were slow to wise up, the math of retaining and reinvesting earnings is now well understood. Today, school children learn what Keynes termed “novel”: combining savings with compound interest works wonders.

-

CWS Market Review – February 28, 2020

Posted by Eddy Elfenbein on February 28th, 2020 at 7:08 am“Markets trend only about 15 percent of the time; the rest of the time they move sideways.” – Paul Tudor Jones

In last week’s issue, I wrote about the market’s rally, “I want to urge caution. We’ve had some nice gains, but don’t get too complacent. The bear loves to knock you over the moment you get too comfortable.”

Clairvoyance? Nope. I was just being prudent, but my timing was spot on. What a raucous week on Wall Street! The fears of the coronavirus have finally landed on Wall Street and the S&P 500 has fallen for six days in a row. If you’re keeping score, this is the 26th pullback of more than 5% since the bull market began 11 years ago.

Let’s review the damage. On Monday, the S&P 500 lost -3.35% for its worst loss in more than two years. Then on Tuesday, it fell by -3.03%. On Thursday, the S&P 500 plunged for a loss of -4.42%. That was its biggest fall in 8½ years.

From its closing high on the Wednesday before last, the S&P 500 has lost just over 12%. That’s in six trading sessions. This is the fastest correction (over 10% loss) in history. There’s an old saying on Wall Street, “a bull walks up the steps and a bear jumps out the window.” Boy is that true.

Here’s an example of how irrational markets have been. Shares of ZOOM Technologies (ZOOM) jumped more than 50% on the belief that its video-conferencing technology would benefit from the coronavirus.

One small problem. That’s the wrong company!

The company that makes Zoom is Zoom Video Communications. Their ticker is ZM.

ZOOM Technologies is not longer in business. In fact, it hasn’t been in business for years!

Traders didn’t care. At its high, ZOOM was up more than 56% on Thursday. Let me reiterate, this is a company that’s no longer in business.

In this week’s CWS Market Review, I’ll try to bring some sanity back to Wall Street. Fortunately, our Buy List has been outperforming lately (meaning down less). Since February 20, the S&P 500 has lost 11.69% while our Buy List has fallen 9.75%. I realize talking about falling less may sound odd, but it’s an important aspect of long-term investing success.

I’ll go over our three Buy List earnings reports from this week. They were all quite good. At one point, Middleby jumped for a 20% gain. I’ll have the details in a bit. I’ll also preview next week’s earnings report from our favorite deep-discounter, Ross Stores. But first, let’s try to make sense of this week’s mayhem.

The Fastest Correction in History

I certainly won’t say that I have any expertise in public health, so I can’t say much about what will eventually happen with coronavirus. But I do know something about financial markets, and they’ve been very anxious this week. The yield on the 10-year Treasury fell below 1.25%. That’s an all-time low.

This week has seen some of the most severe few days since the Financial Crisis. Still, we’ve seen many weeks worse than this. We should also bear in mind how well the market had done before now. The S&P 500 is still up over 18% since the start of 2019. As far as one-day losses go, in percentage terms, Thursday doesn’t crack the top 100.

What’s struck me is the big divide among the kinds of stocks feeling the most pain. Stocks that tend to bounce around a lot have been down the most whereas stocks that are more stable have suffered the least. Some of this is to be expected simply due to the nature of these stocks. But the gap between these groups has been especially wide this week even in regard to the overall market.

Here’s a chart of the S&P 500 High Beta Index (red) along with the S&P 500 Low Vol index (blue):

In plainer terms, investors have been dumping risky stocks at a mad pace. In return, they’re running toward anything that looks safe. One beneficiary has been bonds. The yield on U.S. Treasuries has plunged. I think there’s a good chance the Fed will cut rates before the next meeting. In fact, it could be a 0.5% cut. Of course, that’s not exactly a vaccine for coronavirus, but it would calm Wall Street’s nerves.

What to do now? First, whatever you do, do not panic and sell. That would be a huge mistake. As Peter Lynch said, “The real key to making money in stocks is not to get scared out of them.” Make sure you have a well-diversified portfolio of high-quality stocks. The downturn has given us some bargains. AFLAC (AFL), for example, is going for 10 times earnings. Disney (DIS) is another stock going for a discount.

Now let’s take a look at our Buy List earnings from this week.

Trex Is a Buy up to $107 per Share

This week, we had our final three Buy List earnings reports for this earnings season. After the close on Monday, Trex (TREX) reported Q4 earnings of 61 cents per share. That was 10 cents more than estimates. Sales rose 18% to $165 million. The company had been expecting sales of $160 million. For the year, Trex earned $2.47 per share on sales of $745 million.

CEO James E. Cline said, “Fourth-quarter results were in line with our expectations for strong double-digit sales growth and sequential gross margin expansion.” This was a very good quarter for Trex.

For 2020, Trex expects “strong double-digit sales growth.” For Q1, they expect sales of $200 million which is an 11% increase over last year. During 2019, Trex bought back 500,000 shares of stock at an average price of $77 per share.

The stock rose on Tuesday while most everything else was down. On Wednesday, Trex pulled back 5% as a number of analysts trimmed their Q1 EPS forecasts. The shares rallied again on Thursday. This week, I’m raising my Buy Below on Trex to $107 per share.

One other note. James E. Cline will be retiring as CEO later this year. The board has chosen Bryan Fairbanks to be the new CEO.

Our final two reports came on Wednesday. On Wednesday morning Middleby (MIDD) released a fantastic earnings report. At one point on Wednesday morning, the shares were up over 20%.

For Q4, the company made $2.00 per share. That crushed estimates of $1.71 per share. Quarterly sales rose 4.1% to $787.6 million. For the year, Middleby made $7.02 per share. Business is going very well.

CEO Timothy FitzGerald said, “Over the past year we made significant investments in new product innovations addressing these categories and are pleased to see growing interest as we enter 2020. We are well-positioned with a much-improved backlog as we closed out 2019 and are confident it will translate into sales and profitability growth for the upcoming year.”

The shares gained 8% on Wednesday. I’m keeping my Buy Below on Middleby at $120 per share.

After the closing bell, Ansys (ANSS) reported Q4 earnings of $2.24 per share. That was a great number. Wall Street had been expecting $1.98 per share. For the year, Ansys made $6.58 per share.

Ajei Gopal, Ansys President & CEO, said, “Q4 was an outstanding quarter concluding a stellar 2019. We grew double digits across revenue and ACV for the quarter and the year, and I am confident we are tracking towards our 2022 objective of $2 billion in ACV.”

Now for the bad news. Ansys gave poor guidance for Q1 and the whole year. Bear in mind, they could be playing it safe. For Q1, Ansys sees revenues ranging between $300 million and $320 million and earnings between 75 and 88 cents per share. Wall Street had been expecting $360 million and earnings of $1.36 per share.

For the year, Ansys sees revenues between $1.64 billion and $1.70 billion and EPS between $6.19 and $6.71. Wall Street had been expecting $1.68 billion and earnings of $6.76 per share. This implies that much of the Q1 weakness will be made up later in the year,

In early trading on Thursday, Ansys was down as much as 12.8%. It later rallied some to close down by 9.6%. I’m keeping my Buy Below at $270 per share. Stick with Ansys-it’s a great company.

Ross Stores Earnings Preview

Ross Stores (ROST) will report its Q4 earnings on Monday, March 3. This is for their fiscal year which ends at the end of January. I’m a big fan of this deep discounter.

Three months ago, Ross earned $1.03 per share. That was well above their own forecast of 92 to 96 cents per share. Quarterly sales were up 8%, but the really impressive stat was comparable-store sales. For Q3, that was up 5%. The company had been expecting a gain of 1% to 2%.

Q4 is the biggie for Ross. That covers the holiday shopping season: November, December and January. Ross expects Q4 earnings of $1.20 to $1.25 per share which includes a tax benefit of two cents per share. Again, Ross expects same-store sales of 1% to 2%. (They always say that.) The Q4 range implies a full-year 2019 range of $4.52 to $4.57 per share. Ross Stores is a very good stock.

Buy List Updates

I wanted to add a quick note on Disney (DIS). This week, Robert Iger said he’ll be retiring. He’s been a remarkable leader for the entertainment powerhouse. Shares of Disney took a hit on the news. I should add that he’s not disappearing. Instead, Iger will serve as executive chairman. The stock has also lagged due travel concerns. DIS is lower now than where it was in mid-2015. Disney is a very good buy here. I’m lowering my Buy Below on Disney to $130 per share.

On Thursday, Silgan (SLGN) raised its quarterly dividend by 9% to 12 cents per share. This is their 16th consecutive annual dividend increase. The dividend is payable on March 31 to shareholders of record on March 17. Based on Thursday’s close, that works out to a yield of 1.63%. That’s more than a 20-year Treasury.

That’s all for now. Next week, we’ll get all the key turn-of-the-month econ reports. The ISM Manufacturing report comes out on Monday. The ADP jobs report is on Wednesday. Weekly jobless claims are due out on Thursday. That leads up to Friday when the February jobs report is due out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His