-

Morning News: January 20, 2020

Posted by Eddy Elfenbein on January 20th, 2020 at 7:08 amFeel Good Factor Keeps World Stocks Near Record Highs, Oil Jumps

Capitalism Draws Fire Despite Strong Global Economy

Oil Advances to One-Week High as Unrest Hits Iraq and Libya

The Man Who Cut Libya’s Oil Supply Is Getting Harder to Handle

China’s Economic Strength Hidden In Its Weakest Growth Rate In 29 Years

Palladium Bulls Refuse to Blink

Trump’s China Deal Creates Collateral Damage for Tech Firms

France is Making Start-Up Friendly Reforms to Lure Tech Talent and Take on Silicon Valley

In Its 50th Year, Davos Is Searching for Its Soul

Climate Change Takes Center Stage in Davos

How An Exotic Investment Product Sold In Korea Could Create Havoc In The U.S. Options Market

Apple’s Cook Says Global Corporate Tax System Must Be Overhauled

Lawrence Hamtil: Breaking Down 50 Years of Industry Data

Jeff Miller: Weighing the Week Ahead: All Eyes on Earnings

Michael Batnick: Is This As Good As It Gets For the Stock Market?

Be sure to follow me on Twitter.

-

Housing Starts at 13-Year High

Posted by Eddy Elfenbein on January 17th, 2020 at 12:31 pmThe stock market will be closed on Monday in honor of Dr. Martin Luther King’s birthday. It will be interesting to see how many traders will want to be net long going into a three-day weekend.

This morning’s housing starts report showed an increase of 16.9% last month. Housing starts are now at a 13-year high. That’s good news for a stock like Trex (TREX) which is at another new high today.

The Federal Reserve said that industrial production fell 0.3% in December. Part of the reason why is that utilities dropped by 5.6% due to unseasonably warm weather.

China said its economy grew by 6.1% last year. That would be great for the U.S. but for China, it’s actually the slowest rate in 29 years.

-

CWS Market Review – January 17, 2020

Posted by Eddy Elfenbein on January 17th, 2020 at 7:08 am“The dangers of life are infinite, and among them is safety.” — Goethe

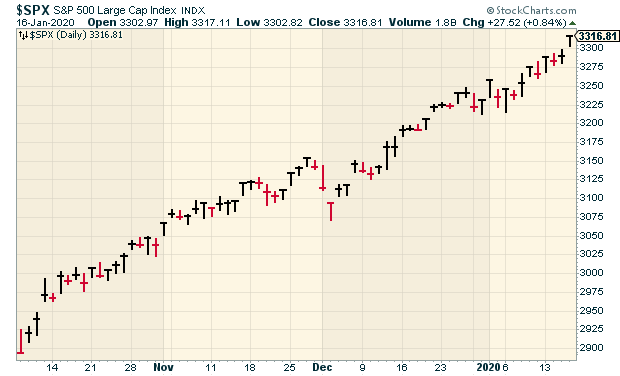

On Thursday, the S&P 500 closed above 3,300 for the first time ever. If you’re into numerology, the index first broke 330 in 1987, meaning 33 years ago, and it first broke 33 in 1954 which was 33 years before that. I don’t know what it means, but that’s a lot of threes.

In any event, not only is the market moving higher, but it’s been a fairly broad rally. That’s always a good sign. I tend to be suspicious when a market rally leans heavily on just a few stocks. This time, the minnows are joining in. Right now, the number of stocks in the S&P 500 that are above their 200-day moving average is at a five-year high.

The S&P 500 is divided into eleven sectors. Eight are currently at or near new 52-week highs. Two more aren’t that far away. Only Energy is lagging behind, and even that sector has perked up this year.

Here’s another cool stat: The stock market hasn’t had a down election year when an incumbent was running in 80 years.

This week, we got our first earnings report of this season. Eagle Bancorp missed by a penny per share. (Or more accurately, analysts missed reality.) Despite the miss, the bank’s doing just fine. I’ll have more in a bit. I also have a complete Buy List earnings calendar for you. But first, let’s look at some recent economic news.

The Lowest Jobless Rate in Half a Century

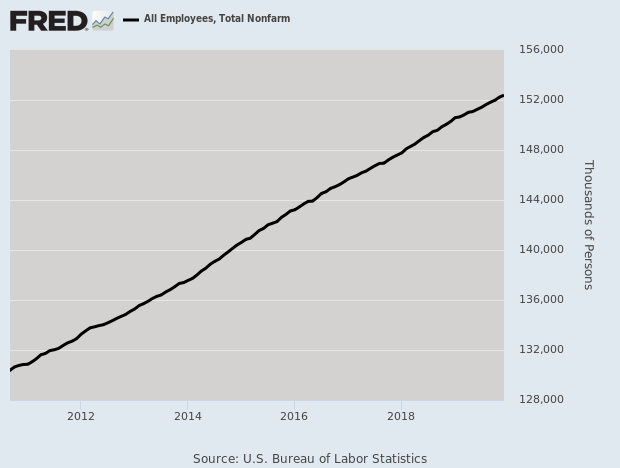

Last Friday, the government released the jobs report for December. The U.S. economy created 145,000 net new jobs which was below expectations of 160,000. The unemployment rate fell to its lowest level since June 1969.

The labor market is doing well. The government also tracks a broader measure of employment called the U-6 rate. For December, that rate fell to 6.7% which is the lowest rate since the data series was first tracked in 1994.

The weak spot, however, is wages. To be fair, we’re seeing some improvement here, but we need to see more. Over the past year, average hourly earnings are up by 2.9%. That’s more than inflation, but not by much. Bear in mind that higher wages will eventually translate into higher sales and profits for our companies.

We may be seeing evidence that workers are in demand. There was a recent story that Taco Bell is willing to pay general managers $100,000 per year. The company will also start paying employees 24 hours of sick time each year.

Here’s a look at nonfarm payrolls over the last decade. People who aren’t in finance would be astounded if they knew how much time and energy goes into forecasting this line.

Here’s a remarkable look at how the U.S. economy has changed. If we were to have the same jobs-to-population ratio that we had 20 years ago, we’d need 8.8 million more jobs. We could also achieve it if we had 13 million fewer people. What’s changed is that there are many more retirees.

Despite the lackluster wage gains, consumers were still out at the malls spending money. On Thursday, the Commerce Department said that December retail sales rose by 0.3%. Also, retail-sales growth for November was revised higher to +0.3%. This suggests that the U.S. economy ended 2019 at a moderate pace. In the last year, retail sales grew by 6.1%. That’s close to the fastest pace since 2012.

Remember that consumer spending accounts for two-thirds of the economy. Economists like to watch “core” retail sales, which excludes cars, gas, building materials and food. For December, the core rate was up +0.5%. That’s quite good, and it’s an improvement over the 0.1% increase we had for November.

In fact, the strong jobs market may continue. The recent jobless-claims report fell to 204,000. That’s very good.

Fortunately, there’s been no evidence yet of an uptick in inflation. On Tuesday, the government said that the Consumer Price Index rose by 0.2% last month. That comes after a 0.3% increase in November. For all of 2019, the CPI increased by 2.3%. That’s the highest annual rate in eight years, but it’s still not that high. Importantly, inflation is still close to the Federal Reserve’s target of 2%.

Digging into the numbers a bit, we see that the “core” rate of inflation increased by 0.1% last month. This is the regular inflation rate, except for food and energy prices, which can be very volatile. The core rate was up by 0.2% in November. For the year, the core rate increased by 2.3%.

Overall, these are good numbers, and it looks like the Federal Reserve won’t need to make a move, in either direction, in the immediate future. It’s especially impressive that inflation is so low considering that the unemployment rate is low as well.

The Fed meets again in two weeks. Don’t expect much. In my opinion, the best market proxy for what the Fed will do is the two-year Treasury yield. On Thursday, the two-year yield closed at 1.58%, and that’s right in line with the Fed’s current target of 1.50% to 1.75%.

With the Fed now in reserve, let’s look at our upcoming earnings reports.

Fourth-Quarter Earnings Calendar

Here’s a table of the 21 Buy List stocks that are reporting this earnings season (the other four don’t follow the March/June/September/December cycle). I’ve included each stock’s earnings date, Wall Street’s consensus and the actual results. Please note that not all the dates are out, and the earnings consensus may change.

Company Symbol Date Estimate Result Eagle Bancorp EGBN 15-Jan $1.07 $1.06 Silgan Holdings SLGN 28-Jan $0.38 Stryker SYK 28-Jan $2.46 Danaher DHR 30-Jan $1.24 Hershey HSY 30-Jan $1.24 Sherwin-Williams SHW 30-Jan $4.39 Church & Dwight CHD 31-Jan $0.55 Check Point Software CHKP 3-Feb $1.99 AFLAC AFL 4-Feb $1.02 Disney DIS 4-Feb $1.48 Fiserv FISV 4-Feb $1.14 Cerner CERN 4-Feb $0.74 Globe Life GL 5-Feb $1.72 Intercontinental Exchange ICE 6-Feb $0.96 Becton, Dickinson BDX 6-Feb $2.64 Moody’s MCO 12-Feb $1.94 ANSYS ANSS tba $1.98 Broadridge Fin Solutions BR tba $0.72 Middleby MIDD tba $1.72 Stepan SCL tba $0.88 Trex TREX tba $0.51 Eagle Bancorp Earned $1.06 per Share

Now let’s look at our first earnings report. After the close on Wednesday, Eagle Bancorp (EGBN) reported Q4 earnings of $1.06 per share. That’s one penny below estimates, and it’s down from $1.17 per share from one year ago.

For all of 2019, Eagle made $4.18 per share. That’s down from $4.44 per year in 2018. The big issue I’ve been watching is Eagle’s legal fees. For Q4, the bank’s legal, accounting and professional fees and expenses rose 68% to $4.1 million. That’s about 12 cents per share.

Here’s what Eagle had to say:

The Company expects to continue to incur elevated levels of legal and professional fees and expenses in 2020 as it continues to cooperate with these investigations. Other than these increased costs, we do not believe at this time that the resolution of these investigations will be materially adverse to the Company. As a result of these ongoing investigations, there have been no regulatory restrictions placed on the Company’s ability to fully engage in its banking business as presently conducted. We are, however, unable to predict the duration, scope or outcome of these investigations.

Looking past these expenses, the bank is doing fine. For Q4, Eagle had a return-on-equity of 11.78%. The bank’s efficiency ratio was 39.7% for the quarter and 40% for the entire year. The legal expenses aren’t pleasant, but it’s a manageable problem. The market clearly over-reacted. Over the summer, the shares plunged $14 per share on the news.

Eagle opened Thursday’s trading down more than 3%, but it quickly righted itself and closed lower by just 0.3%. This is a good bank that’s sailing through some rough seas. Eagle remains a buy up to $53 per share.

Buy List Updates

Danaher (DHR) won’t report earnings until January 30. However, the CEO made some relevant comments at a healthcare conference this week. CEO Thomas P. Joyce, Jr. said that for Q4, Danaher’s sales will come in above the company’s previously-announced expectations. He also said that earnings will be “at or above” the high end of their range.

Allow me to translate. When a CEO says, “at or above,” they mean “above.”

Speaking of Danaher, it, along with a few other of our stocks like Moody’s (MCO) and Fiserv (FISV), has crept above our Buy Below prices. So has Trex (TREX), one of our newbies. It’s already up 11% in 11 trading days. I’m going to hold off adjusting our Buy Below prices until I get a chance to see their earnings reports. As always, there’s never a need to chase after good stocks. You always want to be a disciplined investor.

That’s all for now. The stock market will be closed on Monday in honor of Dr. Martin Luther King, Jr.’s birthday. Dr. King would have been 91. Next week will be dominated by earnings news. There’s not much in the way of economic reports next week. On Wednesday, the new-homes sales report is out. Then on Thursday, the jobless-claims report comes out. The last report was for 204,000, which is a very low number. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Morning News: January 17, 2020

Posted by Eddy Elfenbein on January 17th, 2020 at 7:04 amChina’s Economic Growth Hits 30-Year Low

China’s Improving Economic Data Masks Deeper Problems

China’s Birthrate Hits Historic Low, in Looming Crisis for Beijing

U.S. Passes Global Growth Baton to Rest of World, For Now

The Debate Over Whether to Call It QE Is Over, and the Fed Lost

Trump Fans or Not, Business Owners Are Wary of Warren and Sanders

Banks That Shun Risky Borrowers Offer Rosy View of U.S. Consumer

Google Reaches $1 Trillion in Value, Even as It Faces New Tests

Temasek, Trustbridge Target Majority Stake in WeWork China at $1 Billion Valuation

Sinopec to Review Potential $16 Billion U.S. Gas Deal With Cheniere

Tesla Overruns German Forest in Attack on Auto Establishment

Facebook Foes Sue to Force Zuckerberg to Sell Majority Stake

Ben Carlson: Updating My Favorite Performance Chart For 2019

Roger Nusbaum: I Got Ratio’d On Twitter Big Time & Learned A Ton

Joshua Brown: The “Trade Deal” is Hilarious, Bond Market Doesn’t Bite & Dow 29,000 and the Markets Are Grinding Away

Be sure to follow me on Twitter.

The Gold Bubble 40 Years On

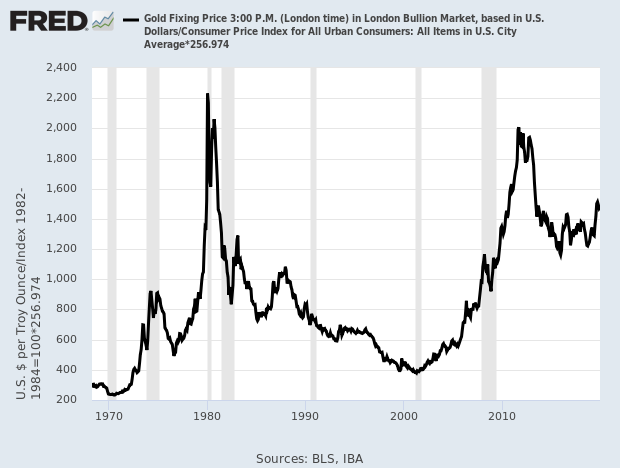

Posted by Eddy Elfenbein on January 16th, 2020 at 8:57 amNext week will mark the 40th anniversary of gold’s peak, on January 21 to be exact.

Since then, gold is down one-third in real terms (gold has nearly doubled while inflation has tripled).

Here’s the price of gold adjusted to today’s dollars:

What’s interesting is that gold seems to move in decade-long patterns that are either really good or really bad. Not much in between.

December Retail Sales Rose by 0.3%

Posted by Eddy Elfenbein on January 16th, 2020 at 8:45 amThis morning, the Commerce Department said that December retail sales rose by 0.3%. This report is important to watch because it’s often a good indicator of consumer spending. Also, retail sales growth for November was revised higher to +0.3%.

This suggests that the U.S. economy ended 2019 at a moderate pace.

Excluding automobiles, gasoline, building materials and food services, retail sales jumped 0.5% last month after falling by a downwardly revised 0.1% in November.

The so-called core retail sales correspond most closely with the consumer spending component of gross domestic product. They were previously reported to have edged up 0.1% in November.

Consumer spending accounts for two-thirds of the economy.

Growth estimates for the fourth quarter are as high as a 2.5% rate, in part because of a drop in imports, which compressed the trade deficit.

In December, auto sales fell 1.3%, the biggest drop since last January, after increasing 1.5% in November. Higher gasoline prices lifted receipts at service stations, which jumped 2.8%. Online and mail-order retail sales rose 0.2% after being unchanged in November.

Sales at electronics and appliance stores rebounded 0.6% in December. Receipts at building material stores surged 1.4% and sales at clothing stores accelerated 1.6%. Spending at furniture stores edged up 0.1%.

Americans also spent more at restaurants and bars, with sales rising 0.2% last month. Spending at hobby, musical instrument and book stores rebounded 0.9%.

Also, weekly jobless claims fell to 204,000. That’s a very good number.

Morning News: January 16, 2020

Posted by Eddy Elfenbein on January 16th, 2020 at 7:14 amWhat’s In (and Not In) the U.S.-China Trade Deal

The $95 Billion Centerpiece of the Trade Deal Is Already In Doubt

Trump Hopes Trade Deals Will Boost Growth. Experts Don’t Agree.

Trump Tax Break That Benefited the Rich Is Being Investigated

In Huawei Battle, China Threatens Germany ‘Where It Hurts’: Automakers

Will Beyond Meat Get Nibbled to Death?

Comcast, Late to the Streaming Party, to Give Details of NBC’s Peacock Service

Nissan Is in Trouble. Carlos Ghosn May Deserve the Blame.

Hyundai, Kia Invest $110 Million in UK Electric Van Startup Arrival Ltd

BlackRock’s Assets Blow Past $7 Trillion in Milestone for Investment Giant

Nobody Makes Money Like Apollo’s Ruthless Founder Leon Black

Flash Crash Culprit Seen as Childlike Gamer Not Fit for Prison

Ben Carlson: The Relationship Between War & The Stock Market

Howard Lindzon: Fintech On Fire…No Surprise To Us Here

Jeff Carter: Markets And Preferences And Longevity

Be sure to follow me on Twitter.

Eagle Bancorp Earned $1.06 per Share

Posted by Eddy Elfenbein on January 15th, 2020 at 4:32 pmAfter the close, Eagle Bancorp (EGBN) reported Q4 earnings of $1.06 per share. That’s one penny below estimates. It’s also down from $1.17 per share from one year ago.

For all of 2019, Eagle made $4.18 per share. That’s down from $4.44 per year in 2018.

“Notwithstanding the negative impact that declining interest rates in the second half of 2019 and a flat yield curve are having on our revenues and net interest margin, we are pleased to report a continued trend of both average loan and deposit growth, together with continuing solid asset quality and favorable operating leverage. Additionally, our capital base remains very strong, with ratios well in excess of the requirements for well capitalized status,” noted Susan G. Riel, President and Chief Executive Officer of Eagle Bancorp, Inc. Ms. Riel added that “While period end loan balances in the fourth quarter 2019 were flat as compared to September 30, 2019, average loans increased 0.5% over the third quarter of 2019 and were 9% higher in the fourth quarter of 2019 as compared to the fourth quarter of 2018. In the fourth quarter of 2019 the funding of construction loans tapered off as expected and we experienced higher loan payoffs. These payoffs (which accounted for about 40% of the full year of 2019 payoffs) were expected and reflected in part the successful completion of projects. Funding of C&I loans improved during the quarter and the loan pipeline remained strong. For the full year of 2019, loan balances increased 8% while average loans increased 10% over 2018, close to planned levels.”

Ms. Riel added, “Deposit activity in the fourth quarter 2019 was very fluid as period end balances declined by about 2% as compared to September 30, 2019, however, average deposit balances increased a strong 5% in the fourth quarter 2019 over the third quarter in 2019. We have many large depositor clients whose balances fluctuate regularly and can impact overall deposit levels at a point in time. We focus more on growing average balances, which more directly relate to revenue. For the fourth quarter of 2019, average deposits were 11% higher as compared to the fourth quarter in 2018. For the full year 2019, deposit balances increased by 4%, while average deposit balances increased a strong 12%.”

The shares are down a little over 1% after hours.

More details:

Ms. Riel further commented, “For the fourth quarter of 2019, as noted, we experienced very strong growth of average deposits as compared to minimal loan growth, resulting in significantly higher average liquidity. This higher average liquidity ($739 million for the fourth quarter of 2019 vs. $306 million normalized average for the first three quarters of 2019) contributed to a decline in the net interest margin to 3.49% for the fourth quarter from 3.72% in the third quarter of 2019. The higher liquidity position in the fourth quarter resulted in an average loan to deposit ratio of 98% as compared to 102% for the third quarter of 2019. Also contributing to the decreased net interest margin for the fourth quarter was a 21 basis point decline in the yield on the loan portfolio to 5.18% versus 5.39% for the third quarter 2019, largely due to the sharp decline in the one month average LIBOR interest rate in the fourth quarter (down 39 basis points to 1.79%). Approximately 40% of the Bank’s loan balances are on notes indexed to this LIBOR rate.” Ms. Riel added, “While we were able to realize declines in our cost of funds as market rates declined in the fourth quarter of 2019 (13 basis points from 1.28% to 1.15%), the variable rate nature of our loan portfolio has resulted in a sharper decline in asset yields than in the cost of funds. Importantly, our credit quality remained very strong in the fourth quarter as the level of nonperforming assets was 0.56% of total assets at December 31, 2019 and the annualized level of net charge offs to average loans was 0.13%.” Ms. Riel added, “The Company’s operating efficiency, another key driver of our financial performance, remained favorable.” For the fourth quarter in 2019, the efficiency ratio was 39.7%, as compared to 36.1% in the fourth quarter of 2018, and was 40.0% for the full year 2019, which is inclusive of elevated legal costs as discussed below.

Combining all operating factors for the fourth quarter 2019, the company achieved a return on average assets of 1.49%, a return on average common equity of 11.78%, and a return on average tangible common equity ratio of 12.91%, while sustaining strong capital levels.

For the full year 2019 over 2018, average deposit growth was 12%, average loan growth was 10%, revenue growth was 3% and noninterest expense growth was 10%. The net interest margin for 2019 was 3.77% as compared to 4.10% for the year 2018. While lower, we believe our net interest margin for 2019 remains above peer banking companies. Period end to period end, loan growth in 2019 was 8% and deposit growth was 4%.

“The real key to making money in stocks is not to get scared out of them.”

Posted by Eddy Elfenbein on January 15th, 2020 at 1:05 pmPeter Lynch once said, “The real key to making money in stocks is not to get scared out of them.” There’s a lot of truth in that.

I’ll give you an example.

Here’s a look at Clorox (CLX) over the last 30 years. The stock has been a huge winner. CLX is up more than 30-fold over 30 years.

Here’s the same stock, but I’ve zoomed in a bit on one five-year stretch.

The point is that even with big winners, there are periods of lackluster performance. Just don’t get scared out of them.

Morning News: January 15, 2020

Posted by Eddy Elfenbein on January 15th, 2020 at 7:09 amRace to Refine: The Bid to Clean Up Africa’s Gold Rush

Trump to Sign Trade Deal With China While Leaving Tariffs in Place

Why the U.S.-China Trade Deal Targets Corporate Secrets

U.S. Data-Release Plan Has Wall Street Readying for Algo Wars

JPMorgan First Major Brokerage to Rate Saudi Aramco ‘Overweight’

Target Says Holiday Sales Missed Its Forecasts

Bank of America Beat Analysts’ Profit Estimate on Rebound in Bond-Trading Revenue

BlackRock Profit Beats as Exchange-Traded Funds Boom

Amazon in India: Jeff Bezos Announces $1 Billion Indian Investment

Twitter’s Top Lawyer Is Final Word on Blocking Tweets—Even Donald Trump’s

Climate Change Is Killing Alpine Skiing as We Know It

Nick Maggiulli: The Investor’s Fallacy

Michael Batnick: Animal Spirits: The 10 Best Jobs in America

Jeff Carter: The Free Market Always Is Better

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His