-

Morning News: December 16, 2019

Posted by Eddy Elfenbein on December 16th, 2019 at 6:51 amU.S. Top Trade Negotiator Praises Deal, China Remains Cautious

U.S. Economy Shakes Free of Recession Fears in Striking Turnaround Since August

There Are Economic Warning Signs for Trump in the Midwest

Market Primed for First Quarter ‘Melt-Up,’ Says Bank of America

A Third of America’s Economy Is Concentrated in Just 31 Counties

IFF Wins DuPont Nutrition Unit Over Kerry in $26.2 Billion Deal

Netflix Shuns Commercials, but It’s Cozying Up to Brands

Cineworld Tops North American Box Office With Cineplex Deal

From Zero to 4, Before the End of the Driveway

Europe’s Richest Man Earns $39 Billion in 2019

Joshua Brown: My Favorite Expense

Jeff Carter: Being Competitive and Grinding

Roger Nusbaum: Ultimately It Comes Down To Accountability & How Lifting Weights Can Improve Your Retirement Planning

Be sure to follow me on Twitter.

-

Cerner Increases Share Repurchase Program

Posted by Eddy Elfenbein on December 13th, 2019 at 2:16 pmCerner Corporation (CERN), a global health care technology company, today announced that its Board of Directors declared a cash dividend to stockholders of $0.18 per issued and outstanding share. The cash dividend will be payable on Jan. 9, 2020, to shareholders of record as of the close of business on Dec. 27, 2019.

Cerner intends to pay regular quarterly cash dividends, with future declarations subject to approval by its Board of Directors and their determination that the declaration of dividends remains in the best interests of Cerner and its shareholders. The decision of whether to pay future dividends and the amount of any such dividends will be based on the company’s financial position, results of operations, cash flows, capital requirements, the requirements of applicable law and any other factors the Board of Directors may deem relevant.

Cerner also announced that its Board has approved an amendment to its stock repurchase program, authorizing the repurchase of an additional $1.5 billion of its common stock. Cerner has repurchased $1.3 billion of its shares in 2019 and had $0.2 billion of available authorization remaining prior to the increase announced today. The total authorized amount available for repurchase is now $1.7 billion.

Cerner plans to repurchase shares in the open market, by block purchase, in privately negotiated transactions or possibly through other transactions managed by broker-dealers. No time limit was set for completion of the program, and the timing and amount of repurchases will depend on how much funding is used for other purposes, such as acquisitions. The Company intends to fund its capital allocation program, including share repurchases, dividend payments and other uses, with cash from operations and debt.

“The Board of Directors and our leadership team believe Cerner’s shares are an attractive investment, and our expanded repurchase program and quarterly dividend reflect our ongoing commitment to returning capital to shareholders and the company’s belief in Cerner’s long-term potential,” said Marc Naughton, executive vice president and chief financial officer. “We have a strong balance sheet and expect to continue generating strong cash flow that can support ongoing investments in growth and a balanced capital allocation strategy.”

-

CWS Market Review – December 13, 2019

Posted by Eddy Elfenbein on December 13th, 2019 at 7:08 am“The labor market remains strong and that economic activity has been rising at a moderate rate.” – This week’s FOMC policy statement

Wall Street is in a festive mood this holiday season. The S&P 500 just closed at another new all-time high. The index is now up 26.4% for the year. That’s the 27th time this year that the S&P 500 has broken records.

This week, the Federal Reserve decided against changing interest rates. In fact, the Fed’s outlook suggests they won’t touch rates during all of next year as well. Last week, we also had another strong jobs report. The unemployment rate is now down to a 50-year low. And it looks like we might finally get some sort of trade deal with China.

In this week’s CWS Market Review, we’ll take a closer look at what the Fed had to say. I also want to discuss how the U.S. economy is doing. Later on, I’ll preview next week’s earnings report from FactSet. (And don’t forget that on Christmas Day, I’ll be sending you the stocks for the 2020 Buy List.) But first, let’s look at last week’s jobs report.

The U.S. Economy Is Still Creating Jobs

Last Friday, the government released the November jobs report, and the numbers were quite good. The U.S. economy created 266,000 net new jobs last month. The forecast had been for 187,000. There were also positive revisions of 41,000 jobs (13,000 to September and 28,000 to October).

Manufacturing saw an increase of 54,000 jobs. Motor vehicles and parts rose by 41,000 thanks to the end of the GM strike. Healthcare, as well as leisure and hospitality, rose by 45,000.

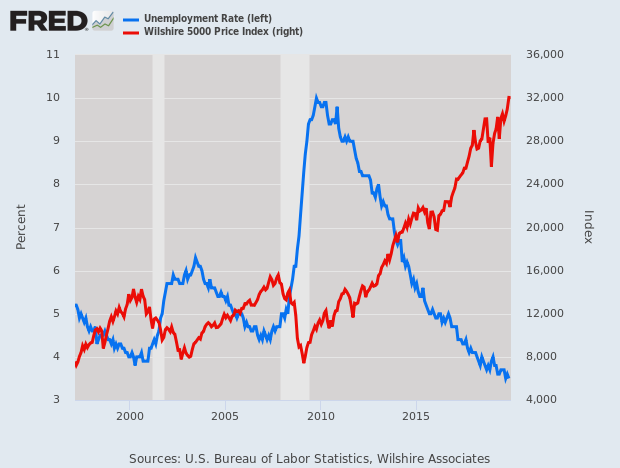

The unemployment rate ticked down to 3.5%, which is a 50-year low. The U-6 Rate, which is a broader measure of joblessness, ticked down 0.1% to 6.9%. The labor-force participation rate is 63.2%. That also fell by 0.1%.

The jobs market is the best it’s been in a generation. The investment writer Gary Alexander notes some interesting stats. The number of Americans able to work but not actively seeking jobs fell by 432,000 (-27%) over the last year. Only one-fifth of the 3.5% jobless have been out of work for 27 weeks versus 45% of the jobless who were out of work that long in 2011. In Ames, Iowa, the unemployment rate is just 1.3%.

The weak point is still wages. For November, average hourly earnings rose seven cents to $28.29. In the last year, wages are up 3.1%. That’s actually an improvement, but we still need to see more. Wages eventually become revenue.

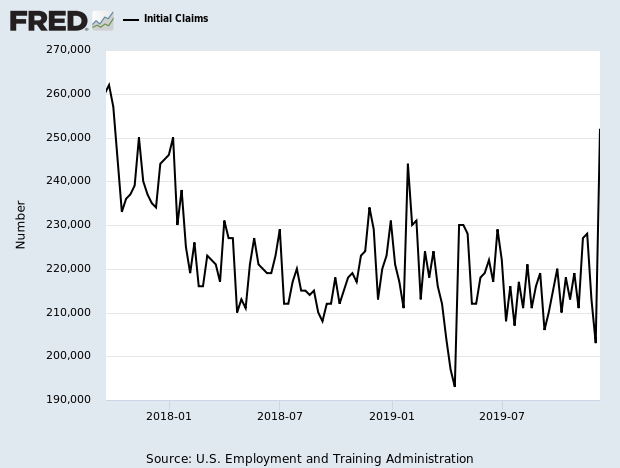

On Thursday, we got an unusually high jobless-claims report. It was the highest in more than two years. The number tends to be “noisy,” so I’m not concerned just yet, but it’s something to take note of.

Fortunately, inflation still isn’t a problem. On Wednesday, the government said that inflation rose 0.3% in November. That topped expectations by 0.1%. Part of the rise was due to gasoline prices. In the last 12 months, consumer prices are up 2.1%.

The core rate, which excludes food and energy, rose by 0.2% in November. In the last year, core prices rose by 2.3%. The important point is that the Fed is still below the inflation rate. This means that real rates are negative. They had been positive a few months ago. So where do rates go from here?

In this week’s Fed policy statement, the central bank had good things to say about the economy. The Fed said the labor market is strong and the economy is growing at a moderate rate. Household spending is rising at a strong pace, and inflation is tame. The Fed noted that two weak areas are business fixed investment and exports.

The Fed decided against raising rates, and the decision was unanimous. The Fed hasn’t had a one-sided vote in several months. Fed Chairman Jay Powell said that the recent rate cuts were merely mid-cycle adjustments. There were a lot of doubters, but it appears that Powell has prevailed.

The Fed also released its economic projections for the next few years. According to the median vote, the Fed doesn’t see itself changing rates all next year. Even in 2021, the Fed forecasts one rate change, and again, no changes in 2022.

Permit me one econo-nerdy point. In the Fed’s projections, they forecast a “long run” rate for different data series. They peg the long-run interest rate at 2.5% and the long-run inflation rate at 2.0%. Frankly, those are pretty meaningless, but with one exception. This implies that the Fed sees the neutral real rate at 0.5%.

For years, the neutral rate was assumed to be about 2%, give or take. If someone told you 10 or 15 years ago that the Fed would eventually see the neutral rate at 0.5%, they would have been stunned. The lower neutral rate has changed so many basic assumptions about the financial markets, and getting used to it has caused a lot of the doomsday crowd to miss a great stock market. Now let’s look at our Buy List earnings report for next week.

Earnings Preview for FactSet

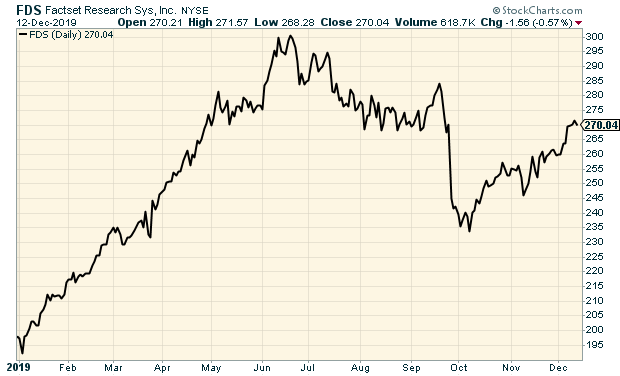

FactSet (FDS) is due to report its fiscal Q1 earnings on Thursday, December 19. Three months ago, the company had a very good earnings report. The problem was that guidance was below expectations.

For its fiscal Q4, FactSet said that revenues rose 5.3% to $364.3 million. Annual Subscription Value, or ASV, rose to $1.48 billion. Quarterly earnings rose 18.6% to $2.61 per share. Wall Street had been expecting $2.47 per share.

This was FactSet’s 39th year in a row of revenue growth and 23rd year in a row of EPS growth. I was particularly glad to see FactSet’s operating margin come in at 33.9%. For the quarter, client count rose by 119 to 5,574. User count rose by 3,871 to 126,833. FactSet’s annual retention rate is running at 89%. The company now has 9,681 employees.

Now let’s look at guidance, and let’s bear in mind that FDS is being quite conservative. The company sees earnings for the current fiscal year (ending in August 2020) ranging between $9.85 and $10.15 per share. That’s basically no growth at all. The range is -1.5% to +1.5%. Wall Street had expected $10.52 per share.

FactSet sees revenues ranging between $1.49 billion and $1.50 billion. That’s up from $1.44 billion for the year that just ended.

Regarding guidance, I want to remind you that FactSet’s initial guidance for last year was $9.50 to $9.65 per share, and they ended up making $10.00 per share. That should tell you how they look to keep expectations low.

The shares took a big hit in September, but FDS has made back most of the lost ground.

Buy List Updates

Disney (DIS) has another big hit with Frozen 2. Elsa and her friends will soon top $1 billion at the box office. That will be Disney’s sixth billion-dollar release this year. Of course, that doesn’t include Star Wars, which is due out in a few days. All told, Disney has made $10 billion at the box office this year. The new streaming service, Disney+, has been downloaded 22 million times. Disney remains a buy up to $152 per share.

RPM International (RPM) said it will release its fiscal Q2 earnings before the bell on January 8. The consensus on Wall Street is for earnings of 73 cents per share.

Danaher (DHR) is giving its shareholders an option to buy shares of Envista (NVST) that DHR owns. Envista used to be Danaher’s dental business. Now it’s a stand-alone company with its own stock.

The deal works like this: You can get 5.5784 shares of NVST for each share of DHR you tender.

For Buy List purposes, we’re not taking the deal because it would violate our set-and-forget philosophy, but it’s not a bad one for shareholders. The ratio works out to a 4.5% discount for NVST based on Thursday’s close.

I’ll caution you that you might not get all the shares you want. That’s just how these deals work. Remember that as a DHR shareholder, you’ll still own some NVST indirectly. The deal expires at midnight tonight. I’m raising my Buy Below on Danaher to $155 per share.

I also want to raise my Buy Below prices on two more our Buy List stocks. This week, I’m lifting my Buy Below on Moody’s (MCO) to $245 per share, and I’m lifting Signature Bank (SBNY) to $141 per share.

That’s all for now. Next week will be rather light for economic news. On Tuesday, we’ll get the report on industrial production. On Thursday, the existing-home-sales report is due out. Then on Friday, we’ll get the second revision to the Q3 GDP report. The last revision showed growth of 2.1%. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: December 13, 2019

Posted by Eddy Elfenbein on December 13th, 2019 at 7:05 amJohnson Wins Crushing Majority in Election That Upends Britain

British Election, Advancing Brexit, Heralds End of a Global Trade Era

Brexit Once Meant a Weaker British Pound, but Not Anymore

Lagarde Wants an `Economic Ballet.’ It Could Be a Mosh Pit.

Trump’s China Deal Flirts With the Curse of a Phase One and Done

U.S. Sets China Trade Deal Terms, Sources Say, But Beijing Mum

How Ethanol Plant Shutdowns Deepen Pain for U.S. Corn Farmers

Saudi Aramco IPO is Latest Example of Why It’s Best to Wait to Invest in Newly Public Companies

Why the Fed May Need to Slash Rates to Zero Before the End of 2020

Bank Regulators Disagree on Changes to Rules for Poor Communities

Broker Group Warns of Investor Risks Posed by U.S. Direct Share-Listing Proposal

Oracle Won’t Return to Dual-CEO Structure

Ben Carlson: Raising the Best Kids You Can & Animal Spirits: Murder of the American Dream

Michael Batnick: The Rise and the Fall & Emotional Alchemy

Howard Lindzon: Domino’s The True Netflix and Chill Winner

Be sure to follow me on Twitter.

-

Jobless Claims Rise to Two-Year High

Posted by Eddy Elfenbein on December 12th, 2019 at 3:34 pmI wouldn’t worry about this just yet, but it does catch my attention:

The number of Americans filing applications for unemployment benefits jumped to more than a two-year high last week, but that probably does not signal a pickup in layoffs as the claims data tends to be volatile in the period following the Thanksgiving Day holiday.

Initial claims for state unemployment benefits surged 49,000 to a seasonally adjusted 252,000 for the week ended Dec. 7, the highest reading since September 2017, the Labor Department said on Thursday. The increase was the largest since August 2017.

Claims dropped to 203,000 in the prior week, which was a seven-month low. The decline likely reflected a late Thanksgiving Day this year compared to 2018, which could have thrown off the model used by the government to strip out seasonal fluctuations from the data.

-

New All-Time High

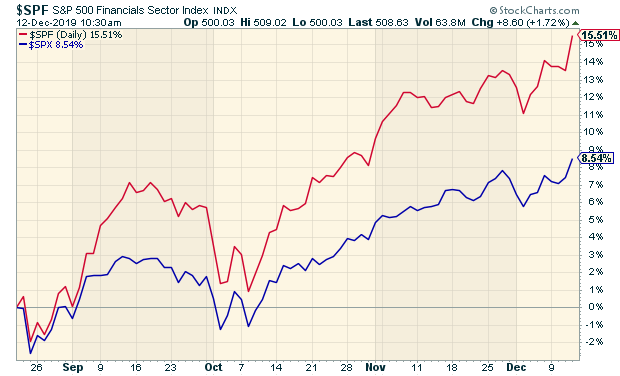

Posted by Eddy Elfenbein on December 12th, 2019 at 10:31 amThe stock market is up to another new all-time high today. Lately, the financial sector has been particularly strong. The financials have been leading for over three months.

-

Morning News: December 12, 2019

Posted by Eddy Elfenbein on December 12th, 2019 at 7:19 amLagarde Leaves Draghi’s Shadow for ECB Debut: Decision Day Guide

Aramco Reaches Prince’s $2 Trillion Goal in Second-Day Surge

China’s Companies Binged on Debt. Now They Can’t Pay the Bill.

Natural Gas Boom Fizzles as a U.S. Glut Sinks Profits

Apple to Dodge $150-Per-IPhone Levy If Trump Delays Tariffs

Want a Bigger Say on Corporate Behavior? Move Your Money

‘Black Swan’ Index Flashes Yellow: Wall Street Is Not Scared

Delta Predicts 2020 Profit Growth; CEO Says More People Turning to Air Travel

Citi, Credit Suisse Drop China’s Ucommune U.S. IPO Over Valuation

Magic Mushrooms Pass First Hurdle as Depression Treatment

GameStop Just Taught Investors a Painful Lesson

Home Depot Ties Opioid Crisis to Recent Surge in Store Theft

Howard Lindzon: Digging For Broken IPOs

Lawrence Hamtil: 2019’s Top Posts

Be sure to follow me on Twitter.

-

No Change from the Fed

Posted by Eddy Elfenbein on December 11th, 2019 at 2:01 pmInformation received since the Federal Open Market Committee met in October indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports remain weak. On a 12‑month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee decided to maintain the target range for the federal funds rate at 1‑1/2 to 1-3/4 percent. The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective. The Committee will continue to monitor the implications of incoming information for the economic outlook, including global developments and muted inflation pressures, as it assesses the appropriate path of the target range for the federal funds rate.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; James Bullard; Richard H. Clarida; Charles L. Evans; Esther L. George; Randal K. Quarles; and Eric S. Rosengren.

Here are the latest projections.

-

The Santa Claus Rally

Posted by Eddy Elfenbein on December 11th, 2019 at 12:19 pmWe’re right at the historically best time of the year for stocks. Actually, that’s an understatement. Historically, this is the best time of the year by far. Over the last 123 years, one-third of the Dow’s annual gain has come in the next half a month.

Let me be clear: I don’t think there’s any useful trading information in these historical seasonal patterns. I would never make an investment decision based on the calendar. Plus, if you run enough data, some oddball pattern will emerge. That doesn’t mean it’s real.

But I do think these patterns are interesting for their own sake. My guess is that the ending of each year brings forth some optimism for the new year.

Now let’s dig into the numbers. Crunching 123 years’ worth of data we find that from December 21 to January 8, the Dow has gained an average of 2.83%. That’s 18 days and trading is always closed on Christmas and New Year’s Day. That’s 36.5% of the Dow’s total annual price gain (dividends aren’t included) coming in just 4.9% of the year. What’s also interesting is how meager the gains have been for the rest of the time.

-

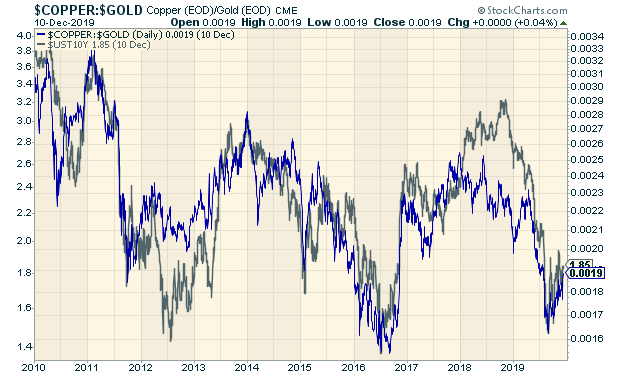

The Gundlach Ratio

Posted by Eddy Elfenbein on December 11th, 2019 at 11:37 amSteve Goldstein introduces us to the “Gundlach Ratio,” named after Jeffrey Gundlach.

The ratio is copper divided by gold. It makes sense.

Gundlach tracks the ratio of copper prices to gold. Gundlach believes in the predictive value of the ratio since copper is sensitive to swings in the economy, while gold climbs when investors get frightened.

As the chart shows, copper is starting to climb relative to gold, which should imply that bond yields will rise, meaning bonds will fall in value.

Works for me.

The ratio has tracked the 10-year Treasury pretty closely for the last few years.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His