-

Oil Surges After Attack on Saudi Arabia’s Oil Production

Posted by Eddy Elfenbein on September 16th, 2019 at 10:11 amOver the weekend, Iran attacked Saudi Arabia’s oil production infrastructure. The result is that 6% of the world’s production has been knocked offline. Oil prices are surging today although the gains aren’t as dramatic as the initial pop we saw in other markets. Right now, I see that crude futures are up about 10%.

Most of the market is down today although energy stocks are up sharply. This is something you don’t see every day.

XLE +3.37%

XLB -1.08%

XLY -0.70%

XLP -0.48%I doubt any production shortfall will last long. There’s certainly a lot of incentive to fill the void. The big question is, what comes next?

There are a lot of reserves held globally so no one is going to run out of oil. Right now, some experts are saying that it will take months for Saudi Arabia to get back to normal production. I’d take the under on that bet.

-

Morning News: September 16, 2019

Posted by Eddy Elfenbein on September 16th, 2019 at 7:22 amOil Prices Jump Most on Record After Saudi Arabia Strike

U.S. Shale Seen Unlikely to Quickly Replace Barrels Lost in Attack on Saudi Facilities

China’s Economy Aches All Over as Beijing Seeks Trade Fix With the U.S.

Fed Trades ‘Remarkably Positive’ For ‘No Precedents’ After Volatile Year

The Fed Faces a Tough End to 2019 as Worries Cloud the Horizon

Auto Union Digs In for GM Strike Over Pay and Benefits

OxyContin Maker Purdue Pharma Files for Bankruptcy to Wipe Out 2,000 Lawsuits

Senators Urge F.C.C. to Review Licenses of 2 Chinese Telecom Companies

Dream Global REIT to Be Bought by Blackstone Funds in $4.7 Billion Deal

NPR Shopping Cart Economics: How Prices Changed At A Walmart In 1 Year

Maybe We’re Not All Going to Be Gig Economy Workers After All

Better Bees May Be Able to Remake a $435 Million Crop Business

Lawrence Hamtil: The Low Vol – Momentum Barbell Using Sectors

Ben Carlson: The Powder Keg of Comparison & A Market of Stocks

Cullen Roche: Is This The Hardest Investing Environment Ever?

Be sure to follow me on Twitter.

-

Bloomberg’s “The Close”

Posted by Eddy Elfenbein on September 13th, 2019 at 10:46 pmHere’s my appearance on Bloomberg’s market-wrap show “The Close” from this afternoon.

The link has the entire show but I’m on between 1:28:22 and 1:36:40.

-

CWS Market Review – September 13, 2019

Posted by Eddy Elfenbein on September 13th, 2019 at 7:08 am“The Federal Reserve should get our interest rates down to ZERO, or less, and we should then start to refinance our debt.” – President Trump

So tweeted the President of the United States. He might get his wish. Circle your calendars for next Wednesday, September 18. That’s when the Federal Reserve meets again, and it seems very likely that the central bank will once again cut interest rates. Of course, it’s not guaranteed, but the futures market thinks there’s an 89% chance that the Fed will cut. Personally, I think it will happen.

The rate cutting may not end there. The futures market thinks there’s a decent chance of another rate cut in October or December. Investors actually appear somewhat undecided as to the future of the market and the economy. That’s for a good reason. We’ve had a few economic reports pointing in different directions. This week, we also saw the market deliver one of its most abrupt sector rotations in decades. It’s confusing, but have no fear. In this week’s issue, I’ll explain what it all means.

The S&P 500 Nears Another New All-Time High

The stock market peaked on July 25. After that, it had a fairly minor downturn, but it spooked a lot of investors. I believe this was the 25th drop of 5% or more since the bull market began more than 10 years ago. The 24 others were all false drops. The market turned back every single one.

It looks like the S&P 500 is about to do it again. On Thursday, the index closed at 3,009.57. During the day, the index got over 3,020 and came within striking distance of its all-time high close of 3.025.86.

Investing consists of trends and reversals. I know that sounds obvious, but it really does lie at the heart of investing. Once the market is decided on a trend, it can last a long time. That’s perfectly well and good for investors. That is, until the reversal.

For the last several months, and years really, growth stocks have been crushing value stocks. It’s been one of the longest growth cycles on record. Then came the reaction. Since September 3, the S&P 500 Value Index is up 5.19% while the S&P 500 Growth Index is up 2.16%. That’s a huge divergence for such a short period of time.

What does it mean? Investors are rushing back to areas of the market like Financials and Cyclicals.

Areas with bond substitutes like Utilities and REITs have lagged. Not surprisingly, bonds have turned back as well. Nearly the entire yield curve beyond two years has added 0.25% in yield in the past few days. Again, that may not sound that dramatic, but it’s a major outlier from what the market has done for the last several months. At some point, the trend becomes the counter-trend.

The one ETF I like to watch here is is the Momentum ETF (MTUM). The thing about momentum investing is that it can be any industry. It’s simply what’s been working lately.

Last Friday, shortly after I sent you last week’s issue, the government reported that the U.S. economy created 130,000 net new jobs last month and that the unemployment rate remained at 3.7%. I wouldn’t call that an outstanding report, but it’s largely in line with the current trend.

Some good news is that average hourly earnings rose 11 cents to $28.11 per hour. That’s an increase of 0.4%, and it’s up 3.2% in the last year. Remember that wage hikes mean more revenues for our businesses. That will filter its way to our stocks.

There were some revisions to the nonfarm payroll data. June was revised lower by 15,000, and July was down 5,000. Within the job gains, the Census Bureau added 25,000 jobs, while manufacturing added 3,000 jobs. The Labor Force Participation Rate rose to 63.2% from 63%.

By the way, the Labor Force Participation Rate is a very misunderstood statistic, and it gets pulled out by partisans on both sides. While there is some truth that the LFPR has fallen in recent years, if you look at it from the perspective of prime working-age folks, it’s not that much of a change. For the most part, the LFPR is driven by broader demographic trends, not short-term policy proposals.

I think the big shocker this week was the inflation report. The CPI showed a modest increase in core prices. We like to look at the core rate, which excludes food and energy prices, because those can be impacted by supply issues. The core rate tends to be a lot more stable, and it gives us a good idea of the true trend of consumer prices.

Buy List Updates

I want to cautiously raise the buy below prices for two of our stocks. The first is Eagle Bancorp (EGBN). The stock got murdered a few weeks ago, but I think it’s worth holding onto. I’ll caution you that Eagle is a speculative position, but it’s always good to have a small number of these. The legal issues are serious, and I don’t want to dismiss them. Still, the shares are going for a bargain price. This week, I’m raising my Buy Below on Eagle to $47 per share.

I’m also going to raise my Buy Below on Continental Building Products (CBPX). Their last earnings report wasn’t so hot, but that probably reflected issues in the housing market. Mortgage rates have come down a lot, and that should help CBPX. I’m raising my Buy Below on CBPX to $30 per share.

The next two earnings reports we have coming up are FactSet (FDS) on September 26 and RPM International (RPM) on October 2.

That’s all for now. The big event next week will be the Federal Reserve meeting on Tuesday and Wednesday. The policy statement will come out at 2 p.m. ET on Wednesday. This will be followed by a press conference by Jerome Powell. The Fed members will also update their economic projections. Also next week, the industrial production report comes out on Tuesday. The last few haven’t been that good. On Thursday we’ll get a look at the latest report on sales of existing homes. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Later today, I’ll be on Bloomberg TV’s market wrap segment at 4 p.m. Tune in!

-

Morning News: September 13, 2019

Posted by Eddy Elfenbein on September 13th, 2019 at 7:05 amE.C.B. Acts to Head Off Recession Threat in Europe, With a Caveat

Charles Li Linked Hong Kong and China but LSE Deal Could Be a Bridge Too Far

China Backs U.S. Farm Purchases as Trade Talks Atmosphere Warms

Trump Trade-War Aid Sows Frustration in Farm Country

Gig Economy in Crosshairs After Decade of Freewheeling Growth

Vaping Was Called Safer Than Smoking. What Happened?

Top SoftBank Investments Slammed From Wall Street to California

WeWork to List Shares on Nasdaq, Make Governance Changes

Ford, GM Rev Up Electric Pickup Trucks to Head Off Tesla

Forever 21, Losing Young Shoppers, Is Said to Be Near Bankruptcy Filing

Grand Jury Indicts GE’s Baker Hughes for Exposing Workers to Toxic Chemicals

Ben Carlson: Passive Bubble Feedback

Roger Nusbaum: The Low Volatility Dilemma

Michael Batnick: A Behavioral Prescription

Be sure to follow me on Twitter.

-

Morning News: September 12, 2019

Posted by Eddy Elfenbein on September 12th, 2019 at 7:42 amDraghi Gears Up for ECB Showdown on Stimulus: Decision Day Guide

Political Risks of Hong Kong Exchange’s $39 Billion LSE Approach Takes Toll on Shares

China, U.S. Are Showing a Little Goodwill as Trade Talks Near

As Trade Talks Loom, Chinese Firms Look Into Buying U.S. Farm Goods

U.S. Recession Indicators Flash Mixed Signals as Talk Heats Up

Trump Wants Negative Rates. Here’s How That Would Work.

Low-Cost Fracking Offers Boon to Oil Producers, Headaches for Suppliers

California Approves Statewide Rent Control to Ease Housing Crisis

Apple’s New iPhones Shift Smartphone Camera Battleground to AI

Purdue Pharma Tentatively Settles Thousands of Opioid Cases

Walmart is Expanding Its ‘Unlimited’ Grocery Delivery Service Nationwide

GameStop Shares Fall as Company Turns to Store Closures

Nick Maggiulli: The Financial Turing Test

Michael Batnick: Animal Spirits: Economically Unattractive

Be sure to follow me on Twitter.

-

Morning News: September 11, 2019

Posted by Eddy Elfenbein on September 11th, 2019 at 7:38 amTrump Says Fed ‘Boneheads’ Should Cut Interest Rates to Zero ‘Or Less,’ US Should Refinance Debt

Bolton Exit Shifts Outlook in Oil Market Roiled by Sanctions

China Exempts Certain Products From Tariffs

Hong Kong Stock Exchange Makes $36.6 Billion Bid for London Stock Exchange

California Passes Landmark Bill to Remake Gig Economy

Apple Reveals Triple-Camera iPhone; $5 Monthly Streaming TV Undercuts Disney

Apple’s New, Lower Priced iPhone Draws Tepid Response in Asia

WeWork Mulls Governance Changes To Save IPO

GE Rips Off the Band-Aid at Baker Hughes

Activist Wants AT&T to Be More Like Verizon

A $100 Billion Tech Company You’ve Never Heard of Just Listed in Europe

The Frankfurt Auto Show’s Heaviest-Hitting Debuts

Ben Carlson: What to Make of a Stock Market That Has Gone Nowhere for a Year-and-a-Half

Jeff Carter: Dual Momentum Investing

Jeff Miller: Stock Exchange: Still Letting Your Winners Run? (Zoetis Edition)

Be sure to follow me on Twitter.

-

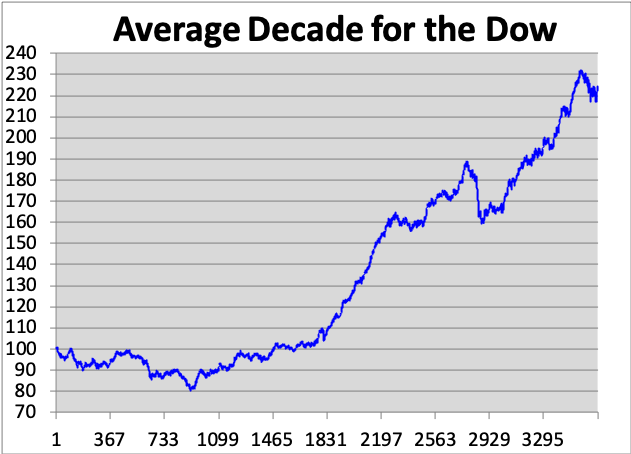

The Peak of the Decade Cycle

Posted by Eddy Elfenbein on September 10th, 2019 at 1:58 pmToday is the peak day in the decade cycle for stocks.

Let me be clear that I don’t put much faith in these things. I would never make an investment decision based on this. I just think it’s interesting for historic reasons.

Having said that, historically, the Dow has peaked on September 10 of the last year of a decade (years that end in 9).

After that, the Dow has fallen 22.3% to a low on June 27 of the third year of decade (ending in 2).

Stocks have continued to be negative until October 27 of the fifth year of the decade (years that end in 4). That’s slightly more than half the time. The stock market’s entire capital gain comes in the other half.

From June 27 of the third year until September 10 of the last year, the Dow has gained 188.9%. That’s a little over seven years.

The big weakness of this analysis is that it’s a small sample size. Sure, the Dow dates back to 1896, but that’s not that many decades to work with.

The average decade gain for the Dow is 124.4% (through the end of last year).

This is what the average decade has looked like for the Dow (set to 100 on January 1 of the first year).

-

Morning News: September 10, 2019

Posted by Eddy Elfenbein on September 10th, 2019 at 7:30 amChina Scraps Foreign Investment Limit in Stock, Bond Markets

China’s Pork Prices Soar, Adding to Beijing’s Troubles

Singapore Economy Shows Some Signs of Hope as Trade War Drags On

U.S. States Launch Antitrust Probe of Google, Advertising in Focus

Juul Illegally Marketed E-Cigarettes, F.D.A. Says

Subduing the Housing Godzillas

WeWork Reportedly Pressured by SoftBank to Shelve IPO

Elliott Appears to Revert to Old Form in Taking On AT&T

Jack Ma Ends 20-Year Reign Over Alibaba Wealth Creation Empire

Alibaba’s New Chairman Says He Has to Reinvent Retail Before Someone Else Does

‘Target Circle’ Loyalty Program Going Nationwide in October

PG&E Plan Offers Nearly $18 Billion to Wildfire Victims and Public Entities

The Best and Worst Case Scenarios for Bonds from Here

Joshua Brown: The Ancient Relationship Between Financial Advice and FinTech & CX

Roger Nusbaum: 25% In One Alternative? No & Don’t Underestimate The Sleep Factor

Be sure to follow me on Twitter.

-

Morning News: September 9, 2019

Posted by Eddy Elfenbein on September 9th, 2019 at 7:48 amRussia’s Massive Gold Stash Is Now Worth More Than $100 Billion

China Has Added Nearly 100 Tons of Gold to Its Reserves

Apple, Foxconn Broke a Chinese Labor Law to Build Latest iPhones

U.S. States Kick Off Antitrust Probe Expected to Focus on Google

How Each Big Tech Company May Be Targeted by Regulators

A Manufacturing Recession Could Cost Trump a Second Term

The World Wastes Tons of Food. A Grocery ‘Happy Hour’ Is One Answer.

Amazon’s Effort to Recruit 30,000 Workers Collides With Saturated Job Market

Volkswagen Hopes Fresh Logo Signals an Emission-Free Future

There Will Be Blood: How a Manhattan Scion Built a Rural Empire

Nearly All British Airways Flights Canceled as Pilots Go on Strike

JPMorgan Creates ‘Volfefe’ Index to Track Trump Tweet Impact

Jeff Miller: Is it Time to Worry about Crowded Trades?

Howard Lindzon: Momentum Monday – Sneaky Good

Jeff Carter: Tech in The Classroom

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His