-

Smucker’s Earnings Miss

Posted by Eddy Elfenbein on August 27th, 2019 at 9:04 amSmuckers (SJM) is out with its earnings report this morning. The company earned $1.58 per share which came in below expectations of $1.74 per share.

The CEO said:

“Our first quarter performance fell short of our expectations primarily due to the timing of shipments and deflationary pricing in the coffee and peanut butter categories, as well as competitive activity in the premium dog food category,” said Mark Smucker, Chief Executive Officer.

“We have continued momentum in many key product categories, and we are already taking decisive actions and prioritizing initiatives that strengthen our business. We remain confident in our strategy, which includes a continued focus on our growth imperatives to lead in the best categories, build brands consumers love, and be everywhere, combined with a relentless focus on operating with financial discipline, all of which will enhance shareholder value for the long term.”

Now for their outlook.

Net sales are expected to range from down 1 percent to flat compared to the prior year, which includes the loss of $105.9 million of sales in the first 4 months of fiscal 2019 related to the divested U.S. baking business and $25.4 million of incremental noncomparable sales for Ainsworth. On a comparable basis, net sales are expected to range from flat to up 1 percent.

Adjusted earnings per share is expected to range from $8.35 to $8.55, based on 114.0 million shares outstanding. Earnings guidance reflects the reduced contribution from sales, gross profit margin of approximately 38.5 percent, and SD&A expenses declining slightly compared to the prior year.

The previous forecast was $8.45 and $8.65 per share.

SJM is down about 8% this morning.

-

Morning News: August 27, 2019

Posted by Eddy Elfenbein on August 27th, 2019 at 7:13 amNorway Wealth Fund Should Move More Investments to North America, Central Bank Says

After 24 Hours, China Still Unaware of Calls Mentioned by Trump

Trump Can Battle China or Expand the Economy. He Can’t Do Both.

The Fed Shouldn’t Enable Donald Trump

Here’s How Wildly Stocks Swing When Trump Mentions the Trade War

Three U.S. Bond Kings Wield Same Strategy, Get Same Result: Lag Their Peers

China Eases Rules on Cheap Drug Imports to Fight Chronic Diseases

Johnson & Johnson Ordered to Pay $572 Million in Landmark Opioid Trial

Cadillac’s Last Stand? Storied Brand Aims (Again) for Revival

GlobalFoundries Sues TSMC, Wants U.S. Import Ban on Some Products

KFC To Test Plant-Based ‘Meatless Chicken’ In Atlanta

Nick Maggiulli: Skewed Expectations

Ben Carlson: Re-Kindled: Amusing Ourselves To Death & Does the Stock Market Have a Say in the Presidential Election?

Joshua Brown: ‘The Mandalorian’ Trailer Hits!

Be sure to follow me on Twitter.

-

Decent New Home Sales Report

Posted by Eddy Elfenbein on August 26th, 2019 at 11:43 amI wanted to touch on Friday’s report on new home sales. The numbers weren’t great, but they were good enough. This is probably better news for the economy than anything the yield curve says.

These figures are very noisy and they bump around a lot. It’s important to look at the overall trend.

The Commerce Department said Friday that new homes sold at a seasonally adjusted annual rate of 635,000 units. That’s down from a sharply revised upward rate of 728,000 in June. So far this year, sales have risen 4.1%, a sign that buyers are beginning to respond to lower mortgage rates.

The volatility in home sales reflects broader uncertainty in the housing market. Buyers have been eager to take advantage of wage growth and historically-low mortgage rates. The average rate on a 30-year loan declined to 3.55% this week, according to mortgage buyer Freddie Mac. The revisions to the June figure, coupled with a rebound in existing home sales in July according to data released by the National Association of Realtors, show sales reacting largely well to lower borrowing costs.

The mortgage market is helping. This year will probably be the best year for new home sales since 2007.

Don’t let negative news about the economy overwhelm you. There’s still a lot left in the current economic cycle.

-

Morning News: August 26, 2019

Posted by Eddy Elfenbein on August 26th, 2019 at 7:07 amJapan Denies it Gave Trump Too Much in Trade Talks

Gold Steadies as Trump Ratchets Down China Trade Tension

Oil Rises on Hopes of Easing U.S.-China Trade Tension

Corporate America Sounds Alarm on Trump’s Threats Over China

Trump Faces a Stubborn Opponent in Fed’s Economic Experts

Fund Manager Who Beat 98% of Peers Says Stay Calm and Buy Stocks

Nissan Got Rid of Carlos Ghosn. The Way It Did So May Prove Costly.

Iceland’s Purple Planes Are Grounded, and With Them, Its Economy

Amgen to Buy Celgene’s Psoriasis Drug Otezla for $13.4 Billion in Cash

Tesla to Raise Prices in China on August 30, May Increase Again in December

Dorm to Table: College Start-Ups Take Aim at Food Industry

Michael Batnick: Calibrating Your Risk Tolerance

Cullen Roche: Black Hole Monetary Economics

Jeff Miller: Weighing the Week Ahead: Can Feedback Alter Trump’s Course?

Be sure to follow me on Twitter.

-

CWS Market Review – August 23, 2019

Posted by Eddy Elfenbein on August 23rd, 2019 at 7:08 am“Losing an illusion makes you wiser than finding a truth.” – Ludwig Borne

After the stock market reached an all-time high on July 26, the S&P 500 fell for six days in a row. Fears about the trade war and China and the yuan combined to knock 6% off the stock market in those six days.

This is the 25th correction of more than 5% in this bull market dating back to March 2009. All 24 of the previous drops failed to turn into bear markets. I strongly suspect this will eventually become #25, but at some point, the streak will end. The good news is that the market has calmed down over the last few days.

On our Buy List, we had impressive earnings reports from Hormel Foods and Ross Stores. I’ll cover that in a bit. The outlook from Ross was a bit light due to the tariffs with China. Later on, I’ll preview next Tuesday’s earnings report from Smucker. That will be our last earnings report for some time. But first, let’s take a closer look at the divided economy.

The Consumer Is Healthy but Factories Are Not

In last week’s CWS Market Review, I mentioned how there’s a growing divergence in the U.S. economy. The consumer sector is doing just fine. Consumer spending is rolling along. Retail sales are doing well. This week, in fact, shares of Target jumped 20% after the company’s earnings report.

The industrial sector, however, has hit the skids. The numbers on manufacturing have been pretty sluggish. We can also see this divide in the stock market. I’m often asked when the stock market will finally break. In one respect, it’s already broken down. If we measure from late January 2018, then the stock market hasn’t done that well, especially compared with alternatives such as bonds or gold.

Since January 26, 2018, the S&P 500 is up just 1.74%. That’s nothing. It’s as if we had a silent bear market and no one noticed. The market didn’t plunge 20%, but we’ve barely moved over a period when the stock market averages about 20%, give or take. It’s not exactly the same, but there are some similarities.

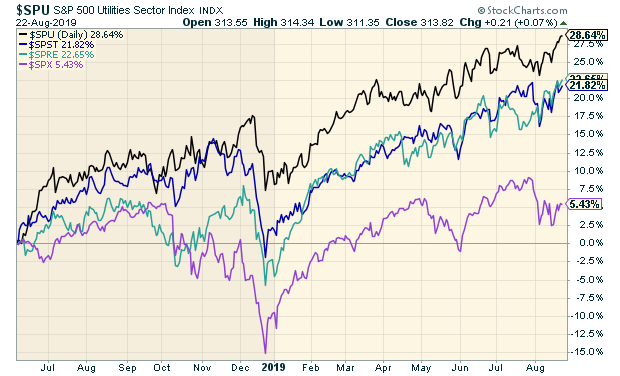

Not only that, but we can see the effect within the stock market. There’s the defensive side of the market. That includes Consumer Staples, Utilities and Real-Estate Investment Trusts (REITs). These stocks have done fairly well. All those sectors are near new 52-week highs. These stocks are sometimes called Low Volatility stocks because they’re far more stable than other shares. On our Buy List, this includes stocks like Church & Dwight (CHD) and Hershey (HSY). Chocolate and condoms aren’t going to be terribly impacted by a recession.

This chart shows how the three defensive sectors have outpaced the S&P 500 (in purple) for several months.

At the other end of the market, you have cyclical stocks. This includes sectors like Energy, Materials, Industrials and Financials. These stocks have not done well at all. In particular, the plunge in the Energy sector is remarkable. The S&P 500 Energy sector is still more than 40% below its high from five years ago. The scars from the recession are still visible. The S&P Bank Index is lower than where it was over 20 years ago.

Part of our success this year compared with the market is that the Buy List is skewed toward these defensive areas. That wasn’t a macro call on my part. Most any portfolio will lean in one direction or another even without trying. This year we’ve been fortunate enough to catch the tailwind helping defensive sectors.

I’m not fully convinced that the economy is in trouble, the inverted yield curve aside. Historically, an inverted yield curve can presage a recession by as much as two years. Also, with rates already so low, perhaps the indicator isn’t as reliable as it once was.

The important variable to watch is the housing market, and that’s moving along. This week’s report on existing-home sales was above expectations. Lower mortgage rates are playing a big role here. As long as the housing market remains healthy, it’s very hard for the economy to fall into a recession.

In fact, Edward Leamer, a well-known economist and econometrician, wrote a piece called “Housing IS the Business Cycle” arguing that housing is central to the overall economy. This isn’t due to its size but due to its cyclical nature.

Any Fed rate cuts for the rest of this year probably won’t have the stimulating impact that the recent decline in mortgage rates has had and will have later this year.

For now, investors should make sure their portfolios have plenty of defensive stocks and stocks with generous dividends. On the Buy List, Check Point Software (CHKP) looks quite good now. I also like Becton, Dickinson (BDX). If you’re more speculative, then Eagle Bancorp (EGBN) is worth a look. Now let’s check out this week’s earnings reports.

Earnings from Hormel Foods and Ross Stores

We had two Buy List earnings reports this week. On Thursday morning, Hormel Foods (HRL) reported fiscal Q3 earnings of 37 cents per share. That was one penny better than expectations.

In many ways, this earnings report was a big sigh of relief. Hormel’s numbers weren’t outstanding, but they were good enough. I think some investors had pretty low expectations, so Hormel proved that things are mostly okay.

In May, the Spam folks lowered their full-year guidance due to African swine fever and other issues. I think that rattled investors. Fortunately, there was no lower guidance this time. Instead, Hormel stood by its full-year forecast for earnings of $1.71 to $1.85 per share.

Since Hormel has already earned $1.33 through the first three quarters, the guidance implies a range for fiscal Q4 of 38 to 52 cents per share. Wall Street had been expecting 45 cents per share. Hormel also sees full-year sales of $9.5 billion to $10 billion.

For Q3, Hormel’s operating margin was 11.2% which is up from 10.9% a year ago. That’s a good sign. Shares of HRL rallied 4.8% on Thursday, and we now have a slight gain on the year. I’m cautiously raising my Buy Below on Hormel Foods to $46 per share.

After the bell on Thursday, Ross Stores (ROST) reported fiscal Q2 earnings of $1.14 per share. That was above their guidance range of $1.05 to $1.11 per share. Quarterly sales were up 6% to $4.0 billion. The all-important comparable-store-sales figure was up 3%. Ross had projected growth of 1% to 2%.

Barbara Rentler, ROST’s CEO, said, “We delivered respectable gains in both sales and earnings for the second quarter. While our Ladies business continued to trail the chain, trends in this important area showed some improvement during the period. Operating margin of 13.7% was better than expected, mainly due to favorable timing of expenses that are expected to reverse in the second half.”

Now for guidance. Ross sees comparable-store sales growth of 1% to 2% for Q3 and Q4. However, because of the trade war with China, Ross is adjusting its second-half guidance. Ross now expects Q3 earnings of 92 to 96 cents per share. Wall Street had been expecting $1 per share. For Q4, which is their biggest, Ross sees earnings of $1.20 to $1.25 per share. Wall Street had been expecting $1.24 per share.

That adds up to full-year guidance of $4.41 to $4.50 per share which is narrower than the previous guidance of $4.38 to $4.52 per share. Despite the tariff issues, Ross continues to do very well. Remember that they like to low-ball their guidance. I’m raising my Buy Below on Ross Stores to $113 per share.

Earnings Preview for Smuckers

We’ll get the last of our August earnings reports next Tuesday when Smuckers (SJM) reports. The jelly stock started off very strongly for us this year but hasn’t done much this summer.

That’s a shame because in June, the company released a strong earnings report. For Q4, Smucker earned $2.08 per share. That was 13 cents better than Wall Street had been expecting.

Smucker also provided guidance for the current fiscal year. The company expects sales growth of 1% to 2% and earnings ranging between $8.45 and $8.65 per share. That’s a bold forecast. Wall Street had been expecting $8.33 per share.

The company has worked to integrate the recent purchase of Ainsworth. The core brands are performing well. The pet-food business is also holding up. For Tuesday, Wall Street expects $1.74 per share.

Buy List Updates

There are a few Buy List updates I have for you. Shares of AFLAC (AFL) got dinged on Wednesday after the Japan Times said that Japan Post “improperly sold around 104,000 insurance policies issued by U.S. partner Aflac Inc.”

AFLAC had partnered with Japan Post to sell AFLAC’s policies, but Japan Post double-charged some customers or left others uninsured. Japan Post said it will stop selling third-party insurance products but it will make an exception for AFLAC’s cancer products.

AFLAC issued a press release to address the issue. I don’t expect this will be a major issue. Shares of AFLAC lost more than 5.5% on Wednesday. Don’t let this concern you. AFLAC is a very strong company.

Shares of Disney (DIS) dropped about $3 per share just before the closing bell on Monday. A whistleblower had told the SEC that Disney has been inflating its revenue for years. A long-time analyst with the company said they had overstated the amount of revenue the parks were taking in.

I can’t judge the merits of the accusation. Disney said they had reviewed the matter and found no wrongdoing. Following Monday’s quick drop, shares of Disney seem to have moved on. Disney remains a solid buy.

Before I go, I want to adjust a few of our Buy Below prices. Fiserv (FISV) continues to look very strong since its last earnings report. The company beat expectations, reiterated guidance and completed the big deal with First Data. This week, I’m lifting our Buy Below on Fiserv by $10 to $113 per share. Hershey (HSY) has also performed well since its earnings report. I’m lifting my Buy Below on HSY to $162 per share.

That’s all for now. There will be no newsletter next week. I’m on the road ahead of Labor Day. Next week is the final trading week of August. On Monday, we’ll get the latest report on durable goods. The data here have been pretty weak lately. Then on Tuesday, the report on consumer confidence will be released. On Thursday, the government will update its report on Q2 GDP growth. The initial report said that the U.S. economy grew in real terms by 2.1% last quarter. That’s right in line with the average for the last 10 years. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 23, 2019

Posted by Eddy Elfenbein on August 23rd, 2019 at 7:05 amG-7 Is Well Timed to Fight Recession But Leaders Unlikely to Act

The Trade War Is Creating a Windfall for Rivals of U.S. Soy in China

Protest Fears Stalk Hong Kong Businesses as China Threat Looms

Powell, Carney to Speak at Jackson Hole But Draghi, Kuroda Skip

YouTube Disables 210 Channels That Spread Disinformation About Hong Kong Protests

Huawei Says U.S. Curbs to Cut Smartphone Unit’s Revenue by Over $10 Billion

Recession or Not, a Payroll Tax Cut Would Be a Bad Move. It Could Hurt Social Security.

Apple and Goldman Sachs Launch Their Credit Card

Phone Companies Ink Deal With All 50 States And D.C. To Combat Robocalls

The Cursed Legacy of the Most Expensive Plot of Land in Los Angeles

Many Are Abandoning Facebook. These People Have the Opposite Problem.

Patrick Byrne, Overstock C.E.O., Resigns After Disclosing Romance With Russian Agent

Ben Carlson: When the Short-Term Impacts the Long-Term: Are We There Yet?

Howard Lindzon: Greedy, Sloppy, Silly …The IPO Market of 2019 Continues

Jeff Carter: Crypto and Bear Markets

Be sure to follow me on Twitter.

-

Hormel Foods Earns 37 Cents per Share

Posted by Eddy Elfenbein on August 22nd, 2019 at 12:43 pmThis morning Hormel Foods (HRL) reported fiscal Q3 earnings of 37 cents per share. The company also reiterated their full-year guidance of $1.71 to $1.85 per share.

Hormel has already made $1.33 per share for the first three quarters. That means they expect 38 to 52 cents per share for Q4. Wall Street had been expecting 45 cents per share.

EXECUTIVE SUMMARY

Volume of 1.1 billion lbs., down 4%; organic volume1 down 1%

Net sales of $2.3 billion, down 3%; organic net sales1 flat

Pretax earnings of $261 million, up 1%

Operating margin of 11.2% compared to 10.9% last year

Effective tax rate of 23.6% compared to 18.4% last year

Diluted earnings per share of $0.37, down 5% due to a higher effective tax rate

Year-to-date cash flow from operations of $573 million, down 23% due to higher working capital

Fiscal 2019 earnings guidance reaffirmed at $1.71 to $1.85 per shareCOMMENTARY

“We delivered earnings in line with our expectations this quarter as our experienced management team reacted quickly and appropriately to rapidly changing market conditions,” said Jim Snee, chairman of the board, president and chief executive officer. “Disciplined pricing, strategic promotional activity, effective advertising and insight-led innovation all played a positive role in our performance. The fundamentals of our company are strong, and we remain focused on delivering our key results as we navigate near-term commodity market uncertainty.”

“Innovative branded product lines such as Hormel® Bacon 1™ cooked bacon, Hormel® Fire Braised™ products, SKIPPY® P.B. & Jelly Minis, and Herdez® salsas all delivered strong sales growth,” Snee said. “Our team also grew sales across many core brands such as SPAM®, Dinty Moore®, Mary Kitchen® and Old Smokehouse®.”

“Double-digit earnings growth in Refrigerated Foods offset weaker results in Grocery Products,” Snee said. “Refrigerated Foods effectively managed sales growth and profitability in the midst of volatile input costs caused by African swine fever. Many of our established brands in Grocery Products continue to outpace center store growth. However, the disappointing bottom-line performance for Grocery Products was driven by higher avocado costs in our MegaMex joint venture and lower results for our SKIPPY® peanut butter spreads business.”

“The Jennie-O Turkey Store team is working diligently to regain lean ground turkey distribution following the two voluntary product recalls,” Snee said. “Our International team made progress growing the SPAM® and SKIPPY® brands in China while U.S. exports continue to be impacted by global trade uncertainty.”

OUTLOOK

“We are reaffirming our fiscal 2019 earnings guidance range,” Snee said. “While we have yet to see sustained higher pork prices due to African swine fever, we have seen input cost volatility and are expecting further volatility. The Refrigerated Foods team has proven its ability to operate in various market conditions with a continued focus on value-added growth, disciplined pricing and innovation. Earnings pressure from higher avocado prices and peanut butter category dynamics will continue to impact results in Grocery Products in the fourth quarter.”

“Our experienced management team will continue to leverage our company’s long-term strategy of building brands, innovating, making strategic acquisitions and increasing balance in our business to deliver long-term growth,” Snee said.

-

Morning News: August 22, 2019

Posted by Eddy Elfenbein on August 22nd, 2019 at 7:11 amGerman Companies Signal Looming Recession After Demand Plunges

Inside India’s Messy Electric Vehicle Revolution

Jackson Hole’s Greatest Hits Justify Obsessing Over Fed Meeting

Fed Was Divided About Interest Rate Cut

Job Gains Were Weaker Than Reported, by Half a Million

Hedge Funds Have Already Bled $55.9 Billion This Year

This Nobel Prize-Winning Idea Is Instead Piling Debt on Millions

Apple Readies Camera-Focused Pro iPhones, New iPads, Larger MacBook Pro

Target Shares Surge on Same-Day Delivery Boost

Wal-Mart Suit Against Tesla May Prove Buying SolarCity Was a Mistake

A Popeyes Chicken Sandwich and a Tactic to Set Off a Twitter Roar

What Are the Obstacles to Bayer Settling Roundup Lawsuits?

Ben Carlson: Is The United States Turning Japanese? & Animal Spirits: Paycheck to Paycheck

Roger Nusbaum: Is The 60/40 Portfolio Really Dead?

Jeff Miller: Stock Exchange: Are You Paying Attention To Market Conditions?

Be sure to follow me on Twitter.

-

From the Fed Minutes

Posted by Eddy Elfenbein on August 21st, 2019 at 2:03 pmThe Federal Reserve just released the minutes from their last meeting. This is when they decided to cut interest rates:

Participants’ Views on Current Conditions and the Economic Outlook

Participants agreed that the labor market had remained strong over the intermeeting period and that economic activity had risen at a moderate rate. Job gains had been solid, on average, in recent months, and the unemployment rate had remained low. Although growth of household spending had picked up from earlier in the year, growth of business fixed investment had been soft. On a 12-month basis, overall inflation and inflation for items other than food and energy were running below 2 percent. Market-based measures of inflation compensation remained low; survey-based measures of longer-term inflation expectations were little changed.

Participants continued to view a sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes. This outlook was predicated on financial conditions that were more accommodative than earlier this year. More accommodative financial conditions, in turn, partly reflected market reaction to the downward adjustment through the course of the year in the Committee’s assessment of the appropriate path for the target range of the federal funds rate in light of weak global economic growth, trade policy uncertainty, and muted inflation pressures.

Participants generally noted that incoming data over the intermeeting period had been largely positive and that the economy had been resilient in the face of ongoing global developments. The economy continued to expand at a moderate pace, and participants generally expected GDP growth to slow a bit to around its estimated potential rate in the second half of the year. However, participants also observed that global economic growth had been disappointing, especially in China and the euro area, and that trade policy uncertainty, although waning some over the intermeeting period, remained elevated and looked likely to persist. Furthermore, inflation pressures continued to be muted, notwithstanding the firming in the overall and core PCE price indexes in the three months ending in June relative to earlier in the year.

In their discussion of the business sector, participants generally saw uncertainty surrounding trade policy and concerns about global growth as continuing to weigh on business confidence and firms’ capital expenditure plans. Participants generally judged that the risks associated with trade uncertainty would remain a persistent headwind for the outlook, with a number of participants reporting that their business contacts were making decisions based on their view that uncertainties around trade were not likely to dissipate anytime soon. Some participants observed that trade uncertainties had receded somewhat, especially with the easing of trade tensions with Mexico and China. Several participants noted that, over the intermeeting period, business sentiment seemed to improve a bit and commented that the data for new capital goods orders had improved. Some participants expressed the view that the effects of trade uncertainty had so far been modest and referenced reports from business contacts in their Districts that investment plans were continuing, though with a more cautious posture.

Participants also discussed developments across the manufacturing, agriculture, and energy sectors of the U.S. economy. Manufacturing production had declined so far this year, dragged down in part by weak real exports, the ongoing global slowdown, and trade uncertainties. Several participants noted ongoing challenges in the agricultural sector, including those associated with increased trade uncertainty, weak export demand, and the effects of wet weather and severe flooding. A couple of participants commented on the decline in energy prices since last fall and the associated reduction in economic activity in the energy sector.

Participants commented on the robust pace of consumer spending. Noting the important role that household spending was currently playing in supporting the expansion, participants judged that household spending would likely continue to be supported by strong labor market conditions, rising incomes, and upbeat consumer sentiment. A few participants noted that the continued softness in residential investment was a concern, and that the expected boost to housing activity from the decline in mortgage rates since last fall had not yet materialized. In contrast, a couple of participants reported that some recent indicators of housing activity in their Districts had been somewhat more positive of late.

In their discussion of the labor market, participants judged that conditions remained strong, with the unemployment rate near historical lows and continued solid job gains, on average, in recent months. Job gains in June were stronger than expected, following a weak reading in May. Looking ahead, participants expected the labor market to remain strong, with the pace of job gains slower than last year but above what is estimated to be necessary to hold labor utilization steady. Reports from business contacts pointed to continued strong labor demand, with many firms reporting difficulty finding workers to meet current demand. Several participants reported seeing notable wage pressures for lower-wage workers. However, participants viewed overall wage growth as broadly consistent with the modest average rates of labor productivity growth in recent years and, consequently, as not exerting much upward pressure on inflation. Several participants remarked that there seemed to be little sign of overheating in labor markets, citing the combination of muted inflation pressures and moderate wage growth.

Regarding inflation developments, some participants stressed that, even with the firming of readings for consumer prices in recent months, both overall and core PCE price inflation rates continued to run below the Committee’s symmetric 2 percent objective; the latest reading on the 12-month change in the core PCE price index was 1.6 percent. Furthermore, continued weakness in global economic growth and ongoing trade tensions had the potential to slow U.S. economic activity and thus further delay a sustained return of inflation to the 2 percent objective. Many other participants, however, saw the recent inflation data as consistent with the view that the lower readings earlier this year were largely transitory, and noted that the trimmed mean measure of PCE price inflation constructed by the Federal Reserve Bank of Dallas was running around 2 percent. A few participants noted differences in the behavior of measures of cyclical and acyclical components of inflation. By some estimates, the cyclical component of inflation continued to firm; the acyclical component, which appeared to be influenced by sectoral and technological changes, was largely responsible for the low level of inflation and not likely to respond much to monetary policy actions.

In their discussion of the outlook for inflation, participants generally anticipated that with appropriate policy, inflation would move up to the Committee’s 2 percent objective over the medium term. However, market-based measures of inflation compensation and some survey measures of consumers’ inflation expectations remained low, although they had moved up some of late. A few participants remarked that inflation expectations appeared to be reasonably well anchored at levels consistent with the Committee’s 2 percent inflation objective. However, some participants stressed that the prolonged shortfall in inflation from the long-run goal could cause inflation expectations to drift down—a development that might make it more difficult to achieve the Committee’s mandated goals on a sustained basis, especially in the current environment of global disinflationary pressures. A couple of participants observed that, although some indicators of longer-term inflation expectations, like TIPS-based inflation compensation and the Michigan survey measure, had not changed substantially this year, on net, they were notably lower than their levels several years ago.

Participants generally judged that downside risks to the outlook for economic activity had diminished somewhat since their June meeting. The strong June employment report suggested that the weak May payroll figures were not a precursor to a more material slowdown in job growth. The agreement between the United States and China to resume negotiations appeared to ease trade tensions somewhat. In addition, many participants noted that the recent agreement on the federal debt ceiling and budget appropriations substantially reduced near-term fiscal policy uncertainty. Moreover, the possibility of favorable outcomes of trade negotiations could be a factor that would provide a boost to economic activity in the future. Still, important downside risks persisted. In particular, participants were mindful that trade tensions were far from settled and that trade uncertainties could intensify again. Continued weakness in global economic growth remained a significant downside risk, and some participants noted that the likelihood of a no-deal Brexit had increased.

In their discussion of financial market developments, participants observed that financial conditions remained supportive of economic growth, with borrowing rates low and stock prices near all-time highs. Participants observed that current financial conditions appeared to be premised importantly on expectations that the Federal Reserve would ease policy to help offset the drag on economic growth stemming from the weaker global outlook and uncertainties associated with international trade as well as to provide some insurance to address various downside risks. Participants also discussed the decline in yields on longer-term nominal Treasury securities in recent months. A few participants expressed the concern that the inversion of the Treasury yield curve, as evidenced by the 10-year yield falling below the 3-month yield, had persisted for about two months, which could indicate that market participants anticipated weaker economic conditions in the future and that the Federal Reserve would soon need to lower the federal funds rate substantially in response. The longer-horizon real forward rate implied by TIPS had also declined, suggesting that the longer-run normal level of the real federal funds rate implicit in market prices was lower.

Among those participants who commented on financial stability, most highlighted recent credit market developments, the elevated valuations in some asset markets, and the high level of nonfinancial corporate indebtedness. Several participants noted that high levels of corporate debt and leveraged lending posed some risks to the outlook. A few participants discussed the fast growth of private credit markets—a sector not subject to the same degree of regulatory scrutiny and requirements that applies in the banking sector—and commented that it was important to monitor this market. Several participants observed that valuations in equity and corporate bond markets were near all-time highs and that CRE valuations were also elevated. A couple of participants noted that the low level of Treasury yields—a factor seen as supporting asset prices across a range of markets—was a potential source of risk if yields moved sharply higher. However, these participants judged that in the near term, such risks were small in light of the monetary policy outlooks in the United States and abroad and generally subdued inflation. A few participants expressed the concern that capital ratios at the largest banks had continued to fall at a time when they should ideally be rising and that capital ratios were expected to decline further. Another view was that financial stability risks at present are moderate and that the largest banks would continue to maintain very substantial capital cushions in light of a range of regulatory requirements, including rigorous stress tests.

In their discussion of monetary policy decisions at this meeting, those participants who favored a reduction in the target range for the federal funds rate pointed to three broad categories of reasons for supporting that action.

First, while the overall outlook remained favorable, there had been signs of deceleration in economic activity in recent quarters, particularly in business fixed investment and manufacturing. A pronounced slowing in economic growth in overseas economies—perhaps related in part to developments in, and uncertainties surrounding, international trade—appeared to be an important factor in this deceleration. More generally, such developments were among those that had led most participants over recent quarters to revise down their estimates of the policy rate path that would be appropriate to promote maximum employment and stable prices.

Second, a policy easing at this meeting would be a prudent step from a risk-management perspective. Despite some encouraging signs over the intermeeting period, many of the risks and uncertainties surrounding the economic outlook that had been a source of concern in June had remained elevated, particularly those associated with the global economic outlook and international trade. On this point, a number of participants observed that policy authorities in many foreign countries had only limited policy space to support aggregate demand should the downside risks to global economic growth be realized.

Third, there were concerns about the outlook for inflation. A number of participants observed that overall inflation had continued to run below the Committee’s 2 percent objective, as had inflation for items other than food and energy. Several of these participants commented that the fact that wage pressures had remained only moderate despite the low unemployment rate could be a sign that the longer-run normal level of the unemployment rate is appreciably lower than often assumed. Participants discussed indicators for longer-term inflation expectations and inflation compensation. A number of them concluded that the modest increase in market-based measures of inflation compensation over the intermeeting period likely reflected market participants’ expectation of more accommodative monetary policy in the near future; others observed that, while survey measures of inflation expectations were little changed from June, the level of expectations by at least some measures was low. Most participants judged that long-term inflation expectations either were already below the Committee’s 2 percent goal or could decline below the level consistent with that goal should there be a continuation of the pattern of inflation coming in persistently below 2 percent.

A couple of participants indicated that they would have preferred a 50 basis point cut in the federal funds rate at this meeting rather than a 25 basis point reduction. They favored a stronger action to better address the stubbornly low inflation rates of the past several years, recognizing that the apparent low sensitivity of inflation to levels of resource utilization meant that a notably stronger real economy might be required to speed the return of inflation to the Committee’s inflation objective.

Several participants favored maintaining the same target range at this meeting, judging that the real economy continued to be in a good place, bolstered by confident consumers, a strong job market, and a low rate of unemployment. These participants acknowledged that there were lingering risks and uncertainties about the global economy in general, and about international trade in particular, but they viewed those risks as having diminished over the intermeeting period. In addition, they viewed the news on inflation over the intermeeting period as consistent with their forecasts that inflation would move up to the Committee’s 2 percent objective at an acceptable pace without an adjustment in policy at this meeting. Finally, a few participants expressed concerns that further monetary accommodation presented a risk to financial stability in certain sectors of the economy or that a reduction in the target range for the federal funds rate at this meeting could be misinterpreted as a negative signal about the state of the economy.

Participants also discussed the timing of ending the reduction in the Committee’s aggregate securities holdings in the SOMA. Ending the reduction of securities holdings in August had the advantage of avoiding the appearance of inconsistency in continuing to allow the balance sheet to run off while simultaneously lowering the target range for the federal funds rate. But ending balance sheet reduction earlier than under its previous plan posed some risk of fostering the erroneous impression that the Committee viewed the balance sheet as an active tool of policy. Because the proposed change would end the reduction of its aggregate securities holdings only two months earlier than previously indicated, policymakers concluded that there were only small differences between the two options in their implications for the balance sheet and thus also in their economic effects.

In their discussion of the outlook for monetary policy beyond this meeting, participants generally favored an approach in which policy would be guided by incoming information and its implications for the economic outlook and that avoided any appearance of following a preset course. Most participants viewed a proposed quarter-point policy easing at this meeting as part of a recalibration of the stance of policy, or mid-cycle adjustment, in response to the evolution of the economic outlook over recent months. A number of participants suggested that the nature of many of the risks they judged to be weighing on the economy, and the absence of clarity regarding when those risks might be resolved, highlighted the need for policymakers to remain flexible and focused on the implications of incoming data for the outlook.

-

AFLAC: Allegation and Response

Posted by Eddy Elfenbein on August 21st, 2019 at 11:56 amToday it’s AFLAC’s turn.

The Japan Times revealed that Japan Post “improperly sold around 104,000 insurance policies issued by U.S. partner Aflac Inc.”

The actions of Japan Post, which sells Aflac policies at post offices nationwide, resulted in customers becoming temporarily uninsured and or being double charged for a one-year period that ended in May this year, the sources said.

Japan Post halted sales of its own and third-party life insurance products after admitting in July to conducting inappropriate sales of around 183,000 policies and leaving customers at a disadvantage over the past five years.

It continues to sell Aflac’s cancer insurance products, however, treating them as an exception.

Aflac has long been a leader in cancer insurance in Japan. It signed a business partnership with Japan Post Holdings in 2013 and agreed last December to receive direct investment from Japan Post to expand their cooperation.

Under an arrangement with Aflac, a new customer cannot be insured for three months after he or she purchases the insurance to prevent a person who has already developed cancer from receiving a payout.

The rule caused people switching to a new Aflac insurance policy from an old one to pay for both contracts or be left without coverage for three months.

Since 2014, Aflac eliminated the duplication of premium payments in a contract renewal, but Japan Post did not make the necessary upgrade to its computer system to reflect that change, the sources said.

Shares of AFL are down over 4% today. The company responded:

Contrary to a certain media report, during the formal meeting of the Strategic Alliance Committee on July 17, 2019, Japan Post Holdings Co., Ltd. confirmed to Aflac Life Insurance Japan, Ltd. (Aflac Japan) that the Japan Post Group does not plan to halt the sales of Aflac Japan’s cancer insurance through the Japan Post Group system. Furthermore, consistent with comments on Aflac Incorporated’s July 26th earnings call, on July 26th Japan Post Holdings Co. Ltd. reconfirmed to Aflac Japan that there is no plan to halt the sales of Aflac Japan’s cancer insurance policies.

I’m not sure of the long-term impact of this but my first guess is that this will soon blow over.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His