-

Morning News: August 6, 2019

Posted by Eddy Elfenbein on August 6th, 2019 at 7:05 am‘Ready to Rumble’: U.S.-China Fight Puts World Economy on the Brink

China Acts to Limit Yuan Plunge, Bringing Some Relief to Markets

Good Will Is a Thing of the Past in the Trade War

India Raises Cost of Refinery Project with Aramco by 36%

Why Bitcoin Is Rising As Stocks and the Yuan Fall

Former Fed Chiefs Unite in Call on Trump to End Powell Threats

Dear Walmart C.E.O.: You Have the Power to Curb Gun Violence. Do It.

Barneys Files for Bankruptcy As Rents Rise and Visitors Fall

Gannett, the Owner of USA Today, Is About to Get a Whole Lot Bigger

Apple, Goldman Sachs Start Issuing Apple Cards to Consumers

For J.C. Penney CEO, Debt Haunts Turnaround Bid

Cullen Roche: How I Think of the Stock Market During its Ups and Downs

Ben Carlson: The Big Lie in Personal Finance & Re-Kindled: Superforecasting

Be sure to follow me on Twitter.

-

The Yuan Falls and Takes Us With It

Posted by Eddy Elfenbein on August 5th, 2019 at 10:46 amThe Chinese government allowed the yuan to fall below seven to the dollar. This is a pretty big deal because it had previously supported that level.

This is a strike back from the PRC government to President Trump’s latest round of tariffs. The Chinese government also said it would forego buying U.S. agricultural products.

The Dow has been down as much as 600 points this morning. The problem is we don’t know how far this can escalate. If you recall, the U.S. market was knocked four years ago when the yuan was last devalued.

-

Morning News: August 5, 2019

Posted by Eddy Elfenbein on August 5th, 2019 at 7:14 amChina Hits Back at Trump by Weakening Yuan, Halting Crop Imports

Stocks Tumble, Treasuries Surge as the Yuan Hits 7

Traders Brace for Full-Blown Currency War as China’s Yuan Sinks

Russians Pull Out Credit Cards, and Consumer Debt Spirals

Drug Industry Urges Canada to Act Early on U.S. Import Plan

Bad Times in Tech? Not if You’re a Start-Up Serving Other Start-Ups

Promotions and Patriotism: ‘Battle Mode’ Huawei Sees China Smartphone Sales Surge

Murdoch’s Fox Corp to Buy Fintech Credible Labs in $397 Million Deal

New Japanese Flying Car Gets Off the Ground, for About a Minute

China’s Didi Chuxing Launches Autonomous Driving Unit as Independent Company

HSBC’s Chief Steps Down, in a Surprise

In the Wake of Latest Massacres, Walmart is Pressured to Stop Selling Guns

Cullen Roche: Three Things I Think I Think – Rate Cut Edition

Jeff Miller: Weighing the Week Ahead: Have the Facts Changed Your Mind?

Joshua Brown: Beyond Meat “Rage Dad” Sweeps Financial Twitter – What Do You Think?

Be sure to follow me on Twitter.

-

July NFP = +164K

Posted by Eddy Elfenbein on August 2nd, 2019 at 11:19 amThe jobs machine continues. The U.S. economy created 164,000 net new jobs last month. The unemployment rate stayed at 3.7%.

Overall, the job market is healthy, and the data were broadly in line with expectations. Economists surveyed by The Wall Street Journal had forecast a gain of 165,000 new jobs in July, a 3.6% unemployment rate and 3.1% annual wage growth.

Through the first seven months of the year, employers have added 165,000 jobs a month, on average, below 2018’s average monthly pace of 223,000.

The decadelong U.S. expansion became the longest on record in July. While there is no rule that says the expansion must end, Friday’s jobs report adds to the evidence it is still solid but losing some steam.

Gross domestic product, a broad measure of goods and services across the economy, increased at a 2.1% annual rate in the second quarter, down sharply from a 3.1% pace in the first quarter. Business spending has faltered in recent months. Manufacturing output has declined since the end of 2018, though more recently it has ticked up slightly.

-

CWS Market Review – August 2, 2019

Posted by Eddy Elfenbein on August 2nd, 2019 at 7:08 am“There seems to be some perverse human characteristic that likes to make easy things difficult.” – Warren Buffett

There was a lot of news this week. Let me give you the highlights up front:

1. On Wednesday, the Federal Reserve cut interest rates by 0.25%. This was the first cut since 2008. However, the Fed signaled that this was a “mid-cycle” cut, not the start of a rate-cutting cycle.

2. On Monday, Fiserv officially merged with First Data. This was a $22 billion deal.

3. Church & Dwight reported Q2 earnings of 57 cents per share, five cents more than expectations. CHD also ditched the low end of its full-year guidance.

4. Cognizant Technology Solutions made 94 cents per share, two cents more than expectations. The stock rallied 3.8% on Thursday.

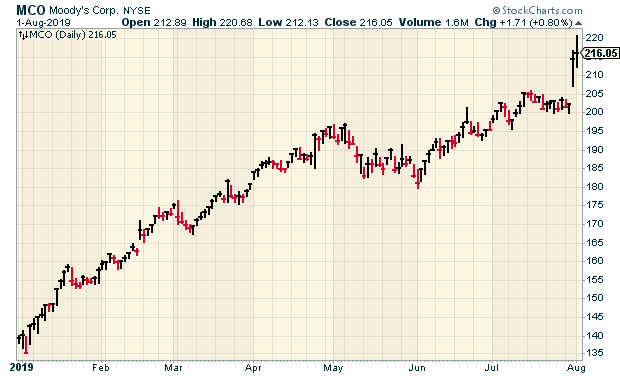

5. Moody’s earned $2.07 per share. Wall Street had been expecting $2.00 per share. The stock gained 6% on Wednesday. MCO also raised full-year guidance.

6. Broadridge Financial earned $1.72 per share, one penny more than expectations. The company raised its dividend by 11%. BR sees growth of 8% to 12% next year.

7. Intercontinental Exchange said it made 94 cents per share. That was two cents more than expectations.

8. Continental Building Products earned 43 cents per share for Q2. That was four cents below estimates.

The Federal Reserve Cut Interest Rates by 0.25%

On Wednesday, the Federal Reserve cut interest rates for the first time since George W. Bush was president. The new range for the Fed funds rate is 2.00% to 2.25%. The Fed last raised rates just over seven months ago.

It may sound odd that the Fed is cutting rates. The economy is mostly fine. The unemployment rate is low, and the stock market has done quite well. I wasn’t a big fan of the Fed’s last increases in December, but I didn’t think they’d cut rates so soon. I was wrong on that.

The bond market clearly led the Fed to make its move now. The two-year yield has been falling for the last several months. As a very general rule of the thumb, the Fed doesn’t get very far from where the two-year yield is. There were even some folks who thought the Fed would jump in and cut by 0.50%.

Fed Chairman Jerome Powell listed three reasons for this recent move: “to insure against downside risks from weak global growth and trade policy uncertainty; to help offset the effects these factors are currently having on the economy; and to promote a faster return of inflation to our symmetric two percent objective.”

Powell also said that “we’re thinking of it as essentially in the nature of a mid-cycle adjustment to policy.” In other words, the Fed doesn’t see this move as the first in a long series of rate cuts going into a recession. Instead, they see a few cuts to help the economy during an expansion. That statement disappointed investors and caused the market to drift lower on Wednesday.

Powell also said, “After simmering early in the year, trade-policy tensions nearly boiled over in May and June, but now appear to have returned to a simmer.” Well, that simmer didn’t last long. On Thursday, President Trump tweeted that the U.S. will impose a whole slew of new tariffs on Chinese goods starting in September.

The market didn’t like that, and I’m sure Powell was probably less than pleased as well. On Thursday, the S&P 500 dropped immediately after the tweet (see below) and closed the day at its lowest level in one month. The damage was mostly done among “high beta” and cyclical stocks. Our Buy List is skewed away from those areas, so we didn’t fall nearly as much.

What happens from here? I think there’s a good chance that the Fed will cut rates again at its meeting next month. After that, it gets a little murky. It really depends on how well the economy does.

For now, the rate cut is good for investors, but the trade war stuff is not. The good news is that this has been a good earnings season for us (besides Eagle, of course). Over the last six trading days, the S&P 500 has lost 2.19% while our Buy List is down just 0.17%. Investors should continue to focus on high-quality stocks. You also want to make sure you have some nice dividend yields in your portfolio. That’s the best defense against an easing Fed.

Let’s look at our Buy List earnings reports from this week:

Six Buy List Earnings Reports this Week

It was another busy week for us. We had three reports on Wednesday and another three on Thursday.

Let’s start with Church & Dwight (CHD). On Wednesday morning, the company reported Q2 earnings of 57 cents per share. That was five cents better than Wall Street’s forecast. That was also up 16.3% over last year. Gross margins rose to 44.6%, and organic sales rose by 4.9% (9.1% internationally).

The CEO said it was CHD’s fifth quarter in a row of organic sales growth in excess of 4%. The company now sees full-year earnings of $2.47 per share and 60 cents per share for Q3. The previous EPS guidance was for $2.43 to $2.47.

This was a good quarter for the company. Church & Dwight remains a buy up to $82 per share.

Also on Wednesday morning, Moody’s (MCO) reported Q2 earnings of $2.07 per share. That beat the Street by seven cents per share.

I like to see how Moody’s Analytics performs. That’s the gem of the company. For Q2, revenues were up 12% to $475.2 million. Moody’s Analytics makes up about 40% of revenues for the entire company.

The best news is that Moody’s raised its full-year guidance. The company had been expecting earnings to range between $7.85 and $8.10 per share. Now Moody’s 2019 earnings range is between $7.95 and $8.15 per share.

The stock jumped 6% on Wednesday and rallied some more on Thursday. Moody’s is now a 54% winner for us this year. It’s our #1 performer. This week, I’m lifting our Buy Below on Moody’s to $225 per share.

After the close on Wednesday, Cognizant Technology Solutions (CTSH) reported Q2 earnings of 94 cents per share. That was two cents above estimates. If you recall, I was concerned about CTSH because the last earnings report was a dud. I’m relieved by these latest numbers.

Quarterly revenue rose 3.4% to $4.14 billion. In constant currency, that’s up 4.7%. Cognizant said they expect full-year earnings between $3.92 and $3.98 per share. That’s an increase from the previous range which was $3.87 to $3.95 per share. However, that was a big cut from the initial guidance of at least $4.40 per share.

These are encouraging signs, but CTSH has more work to do. Simply put, they need to cut costs. The market was relieved. CTSH gained 2% in Thursday’s trading. After the May earnings report, CTSH lost 18% in two days. The shares are up 12.5% since then. I’m cautiously raising my Buy Below on Cognizant to $70 per share.

On Thursday morning, Broadridge Financial Solutions (BR) reported earnings of $1.72 per share which was one penny more than expectations. The company is also raising its full-year dividend from $1.94 to $2.16 per share. This is the eighth-straight year that BR has raised its dividend by double-digit percentages.

This was BR’s fiscal fourth quarter. The company made $4.66 per share for the year. For 2020, the company sees earnings growth of 8% to 12%. That implies a range of $5.03 to $5.22 per share. Wall Street had been expecting $5.14 per share. BR sees recurring-fee growth of 8% to 10% and operating margins around 18%.

I like these numbers. The shares started dropping a few days ago. I think some folks were expecting a miss. The report halted that. I’m raising my Buy Below on Broadridge to $137 per share.

Intercontinental Exchange (ICE) also reported on Thursday morning. For Q2, ICE made 94 cents per share which was two cents better than estimates (exact same as CTSH).

Revenues rose 4% to $1.3 billion. Adjusted operating margin came in at 58%. ICE said that through June 30, it has returned over $1 billion to shareholders.

ICE didn’t offer EPS guidance but it did for a few other metrics. What stood out to me was the ranges for data revenue. ICE said Q3 data revenues are expected to be in a range of $550 million to $555 million. For all of 2019, they see data revenues in a range of $2.19 billion to $2.24 billion. I’m lifting my Buy Below on ICE to $95 per share.

Finally, there’s Continental Buildings Products (CBPX). After the close on Thursday, the company reported sluggish numbers for Q3. CBPX earned 43 cents per share which was four cents below Wall Street’s forecast.

The problem isn’t with Continental; it’s the housing market. For the quarter, net sales fell 10.8% to $124.2 million. Wallboard sales fell 6.1% to 678 million square feet. Mortgage rates have come down a lot, and that should help CBPX.

Wall Street is very down on this stock, but I like what I see. On Thursday, shares closed at their lowest point in six weeks. If you’re patient, this could be a worthwhile investment. CBPX remains a buy up to $28 per share.

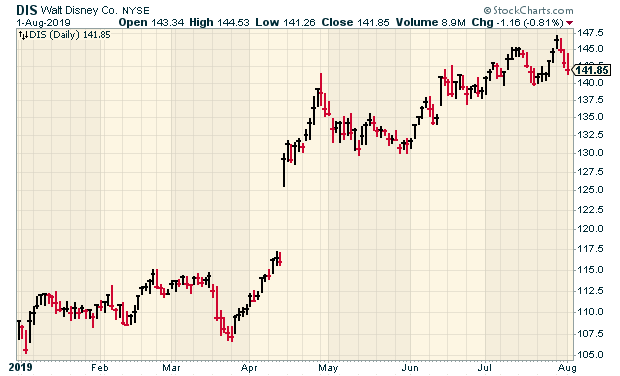

Earnings Next Week from Disney and Becton, Dickinson

Earnings season is just about over. We have two more Buy List reports next week. On Tuesday, August 6, Disney (DIS) and Becton, Dickinson (BDX) are due to report earnings.

I feel like I’m running out of adjectives for Disney. Their business has been astounding this year. The Lion King is another monster hit for them. Disney owns five of the ten highest grossing movies this year.

Disney said it expects Disney+, its new streaming service, to be profitable by 2024. The theme parks had a very good Q1. Net income for the parks totaled $1.5 billion for Q1. Wall Street expects earnings of $1.75 per share.

In May, Becton, Dickinson had decent earnings, but the company lowered guidance. Becton now sees full-year earnings ranging from $11.65 to $11.75. The company blamed currency exchanges plus “recent regulatory and market pressures related to paclitaxel-coated devices.” The previous range was $12.05 to $12.15 per share.

BDX also lowered its full-year revenue guidance of growth of 8.5% – 9.5% down to 8.0% – 9.0%. The company blamed the negative impact of currency exchange. BDX didn’t change its currency-neutral forecast of revenue growth of 4% to 6%.

The stock has been impressively resilient. Wall Street expects Q3 earnings of $3.05 per share.

That’s all for now. The big jobs report comes out later this morning. For June, the unemployment rate was 3.7%. The economic news will be a little slower next week. On Monday, we’ll get the ISM Non-Manufacturing Index. Yesterday we learned that the ISM Manufacturing Index was the lowest in three years. On Wednesday, we’ll get the report on consumer credit. Then on Friday, we’ll see the report on wholesale inflation. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 2, 2019

Posted by Eddy Elfenbein on August 2nd, 2019 at 7:04 amTrump Threats and Trade Worries Rattle Global Investors

China Pledges to Counter Trump’s Threat of More U.S. Tariffs

Japan Imposes Broad New Trade Restrictions on South Korea

Chance of No-Deal Brexit Hampers Bank of England’s Powers of Prediction

The CEO of Nasdaq Wants You to Know the Company Isn’t Just About Stocks

Apple Suspends Listening to Siri Queries Amid Privacy Outcry

In the Fed’s Rate Cut, a Focus on Everyday Workers

Campbell Confirms Sale of Australian Snacks Unit Arnott’s to KKR for $2.2 Billion

Foxconn Eyes Sale of $8.8 Billion China Plant amid Trade War Woes

Stronger Yen Prompts Toyota to Trim Profit Forecast, Saps Honda

The $20 Million Nazi Porsche That May Not Be a Porsche at All

Howard Lindzon: Fire Tim Cook?

Michael Batnick: A Few Charts and a Few Thoughts

Roger Nusbaum: Why Your Retirement Needs Plans B & C

Ben Carlson: Different Ways to be Rich in 2019

Be sure to follow me on Twitter.

-

Earnings from Broadridge and ICE

Posted by Eddy Elfenbein on August 1st, 2019 at 10:03 amWe had two more earnings reports this morning. Broadridge Financial (BR) and Intercontinental Exchange (ICE) both reported earnings.

Broadridge earned $1.72 per share which was one penny more than expectations. The company is also raising its full-year dividend from $1.94 to $2.16 per share. This is the eighth-straight year that BR has raised its dividend by double-digit percentages.

“Fiscal year 2019 was a strong year as we generated double-digit EPS growth and executed against our strategic goals,” said Tim Gokey, Broadridge’s President and Chief Executive Officer. “Broadridge achieved 6% Recurring fee revenue growth and 11% Adjusted EPS growth. We also closed out the year on a very positive note as a strong fourth quarter powered another year of record Closed sales, and we made three tuck-in acquisitions that will further strengthen our business.

This was BR’s fiscal fourth quarter. The company made $4.66 per share for the year. For 2020, the company sees earnings growth of 8% to 12%. That implies a range of $5.03 to $5.22 per share. Wall Street had been expecting $5.14 per share. BR sees recurring fee growth of 8% to 10% and operating margins around 18%.

The stock is currently up about 1.6% today.

Intercontinental Exchange reported Q2 earnings of 94 cents per share. That beat estimates by two cents per share. Revenues rose 4% to $1.3 billion. Adjusted operating margin came in at 58%. ICE said that through June 30, it has returned over $1 billion to shareholders.

We are pleased to report our second quarter results, which extends our track record of revenue and earnings-per-share growth. These results reflect the strength of our global energy business as well as the value of compounding growth in our subscription-based Data & Listings business,” said ICE Chairman and Chief Executive Officer, Jeffrey C. Sprecher. “We remain focused on innovating for our customers, investing in future growth and creating value for our stakeholders.”

Scott A. Hill, ICE Chief Financial Officer, added: “Through the first half of the year, we have grown revenues, earnings-per-share and cash flows, enabling us to return over $1 billion to stockholders. As we look to the second half of 2019, we remain focused on disciplined investment in support of our strategic growth initiatives.”

ICE didn’t offer EPS guidance but it did for a few other metrics:

ICE’s third quarter 2019 GAAP operating expenses are expected to be in a range of $632 million to $642 million and adjusted operating expenses(1) are expected to be in a range of $552 million to $562 million.

ICE’s full year 2019 GAAP operating expenses are expected to be in a range of $2.50 billion to $2.52 billion and adjusted operating expenses(1) are expected to be in a range of $2.19 billion to $2.21 billion.

ICE’s third quarter 2019 data revenues are expected to be in a range of $550 million to $555 million.

ICE’s full year 2019 data revenues are expected to remain in a range of $2.19 billion to $2.24 billion.

ICE’s interest expense is expected to be $73 million in the third quarter.

ICE’s diluted share count for the third quarter is expected to be in the range of 560 million to 566 million weighted average shares outstanding.Shares of ICE are up a little bit today.

-

Morning News: August 1, 2019

Posted by Eddy Elfenbein on August 1st, 2019 at 7:26 amPowell Suggests Fed Embarking on 1990s-Style Mini Easing Cycle

BOE Says Brexit Uncertainty Skews Forecasts, Keeps Rate on Hold

Factory Pain Spreads Through Asia, Europe; Stimulus Expected

Lower Rates Already Hit Housing. They’re Not Helping Much.

Skip Cash for Equifax Breach and Get Credit Monitoring, F.T.C. Tells Victims

A Paradox at the Heart of the Newspaper Crisis

Britain’s LSE Lands ‘Defining’ $27 Billion Refinitiv Deal in Data Drive

Thomson Reuters Raises Outlook, Grows Fastest Since Financial Crisis

A $1 Trillion Valuation Stays Out of Reach for Apple

General Electric CEO Larry Culp Speaks Out on the Turnaround, China, and Boeing

Investments in Cleaner Vehicles Hit BMW Profits

NYT: Are You Rich? This Income Rank Quiz Might Change How You See Yourself

Ben Carlson: A Short History of Fed Rate Cuts & Rush to the Exits

Jeff Carter: How Should Economics Shape Public Policy?

Roger Nusbaum: Stress & Negativity Leading To Bad Decisions

Be sure to follow me on Twitter.

-

Cognizant Earned 94 Cents per Share

Posted by Eddy Elfenbein on July 31st, 2019 at 4:21 pmQuarterly revenue rose to $4.14 billion, up 3.4% (4.7% in constant currency1) from the year-ago quarter.

Quarterly Adjusted Diluted EPS was $0.94, compared to $1.05 in the year-ago quarter.

“We are taking the necessary steps to position Cognizant for improved commercial and financial performance,” said Brian Humphries, Chief Executive Officer. “While there is lots of work ahead, I am encouraged by what I have seen to date and am optimistic on our future.”

The Company is providing the following guidance:

Third quarter 2019 year-over-year revenue growth in the range of 3.8-4.8% in constant currency.

Full year 2019 year-over-year revenue growth in the range of 3.9-4.9% in constant currency.

Full year 2019 Adjusted Operating Margin expected to be approximately 17.0%.

Full year 2019 Adjusted Diluted EPS expected to be in the range of $3.92-$3.98.

“Second quarter results were in-line with our guidance and position us to achieve our full-year outlook,” said Karen McLoughlin, Chief Financial Officer. “We are implementing actions in the second half of the year that we expect will lower our existing cost structure and allow for greater investment in growth, talent, and digital solutions. Using our strong balance sheet we returned over $1.1 billion to shareholders in the second quarter.”

The shares are up about 4% after hours.

-

The Fed Cuts 25

Posted by Eddy Elfenbein on July 31st, 2019 at 2:00 pmThe Fed cut by 25 basis points. The new range for Fed funds is 2.00% to 2.25%. The vote was 8 to 2.

Information received since the Federal Open Market Committee met in June indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although growth of household spending has picked up from earlier in the year, growth of business fixed investment has been soft. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 2 to 2-1/4 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. As the Committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

The Committee will conclude the reduction of its aggregate securities holdings in the System Open Market Account in August, two months earlier than previously indicated.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; James Bullard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against the action were Esther L. George and Eric S. Rosengren, who preferred at this meeting to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His