We got a strong jobs report this morning. The U.S. economy created 224,000 net new jobs last month. That was a lot more than expectations. The unemployment rate ticked up to 3.7%.

In the past year, average hourly earnings are up 3.1%. The broader U6 unemployment rate is 7.2%.

“The laws of probability, so true in general, so fallacious in particular.”

– Edward Gibbon

The trading week was shortened by the July 4th holiday. As a result, there wasn’t much news. Sensing this, many Wall Street big shots took off for the Hamptons, causing the usual financial frenzy to be cut short.

I want to take advantage of this lull in market news to summarize our Buy List at the midpoint of the year. I’m happy to report that our Buy List is doing quite well this year.

We also had a somewhat poor ISM report on Monday. This could be further evidence that the Fed will cut rates at its meeting later this month. I’ll review the latest numbers. But first, let’s look at how well our Buy List is doing in 2019.

Our Buy List Is Up 23.21% This Year

I’ll be honest: at the start of the year, I would not have guessed that stocks would do so well in 2019. Fortunately, we always stay in the market and so don’t miss out on any unexpected surges.

The stock market closed early on Wednesday and was closed all day on Thursday. At the closing bell on Wednesday, the S&P 500 reached 2,995.82. That’s another all-time high.

For some context, the index first broke 300 in 1987. The old version of the index broke 30 in 1929. We may break 3,000 any day.

Now let’s look at some numbers. Through Wednesday, our Buy List is up 22.48% on the year compared with 19.51% for the S&P 500. Including dividends (and I always include dividends in our final calculation), we’re up 23.21% while the S&P 500 is up 20.75%.

Our “beta” is running at 0.800 which is bit low compared with previous years (in reality, I don’t pay much attention to it). There’s been a 90.1% correlation between the daily changes of our Buy List and those of the S&P 500.

Our Buy List generally yields about 1%, which is about half the yield of the S&P 500. I don’t plan it this way, but that’s usually how it works out. We’re running a little higher this year.

Twenty of our 25 stocks are up this year. The biggest winner by price percentage is FactSet (FDS). FDS is currently up 47.93% for us this year. Moody’s (MCO) isn’t far behind at 44.68%.

We have four positions up more than 40%, and seven are up more than 30%. Fourteen of our stocks are up, beating the market this year. Sherwin-Williams (SHW) is just a tiny bit behind. Our worst stock this year is Hormel Foods (HRL). The Spam stock is down just over 2%. On Thursday, eight of our Buy List stocks touched new 52-week highs.

Our sells from last year aren’t doing that well. Alliance Data Systems is down 2% this year. Ingredion is off by 8%. Snap-on is up 12%. Wabtec is up by 5%. Carriage Services is the big winner with a 22% gain.

Our most dramatic stock this year has been Cognizant Technology (CTSH) which dropped 18% over the course of two trading sessions. It’s still up a bit for us this year. Due to broad diversification, the drop didn’t shake our portfolio much.

I nearly forgot the most important part—we didn’t make a single trade all year. Yet we still beat the market, and we did it with lower volatility.

Here’s a look at how each stock has done, along with its dividend-adjusted gain.

| Symbol |

31-Dec |

3-Jul |

Gain |

Adj Gain |

| AFL |

$45.56 |

$56.85 |

24.78% |

26.11% |

| BDX |

$225.32 |

$255.24 |

13.28% |

14.00% |

| BR |

$96.25 |

$131.85 |

36.99% |

38.14% |

| CPBX |

$25.45 |

$26.08 |

2.48% |

2.48% |

| CERN |

$52.44 |

$74.53 |

42.12% |

42.48% |

| CHD |

$65.76 |

$75.04 |

14.11% |

14.86% |

| CHKP |

$102.65 |

$119.47 |

16.39% |

16.39% |

| CTSH |

$63.48 |

$64.18 |

1.10% |

1.71% |

| DHR |

$103.12 |

$145.31 |

40.91% |

41.27% |

| DIS |

$109.65 |

$142.98 |

30.40% |

30.40% |

| EGBN |

$48.71 |

$54.23 |

11.33% |

11.77% |

| FDS |

$200.13 |

$296.06 |

47.93% |

48.73% |

| FISV |

$73.49 |

$94.23 |

28.22% |

28.22% |

| HRL |

$42.68 |

$41.77 |

-2.13% |

-1.16% |

| HSY |

$107.18 |

$138.00 |

28.76% |

30.31% |

| ICE |

$75.33 |

$88.59 |

17.60% |

18.42% |

| MCO |

$140.04 |

$202.61 |

44.68% |

45.49% |

| ROST |

$83.20 |

$100.00 |

20.19% |

20.85% |

| RPM |

$58.78 |

$62.30 |

5.99% |

7.30% |

| RTN |

$153.35 |

$173.45 |

13.11% |

13.70% |

| SBNY |

$102.81 |

$123.97 |

20.58% |

21.62% |

| SHW |

$393.46 |

$470.16 |

19.49% |

20.12% |

| SJM |

$93.49 |

$119.73 |

28.07% |

29.99% |

| SYK |

$156.75 |

$208.15 |

32.79% |

33.49% |

| TMK |

$74.53 |

$91.63 |

22.94% |

23.69% |

| Buy List |

|

|

22.48% |

23.21% |

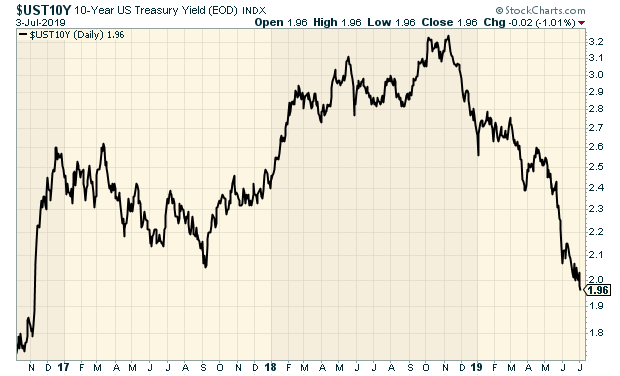

The 10-Year Yield Drops Below 2%

On Monday, the ISM report for June came in at 51.7. That’s the lowest since October 2016. Then on Wednesday, the ADP payroll report came in light. That helped send the 10-year Treasury down to 1.96%. That’s the lowest yield since late 2016.

We’ll learn more about the state of the economy in the jobs report, which is coming out later today. Wall Street seems convinced that the Fed will cut rates at the end of this month. I can’t say I share their certitude.

I need to make a correction to last week’s issue. Danaher (DHR) shareholders will not get shares of Envista, the dental spinoff. Instead, it will IPO and Danaher will retain a position. In effect, we’ll still own it, but only via DHR.

That’s all for now. The June jobs report is due out later today. Next Tuesday, Jerome Powell will be speaking at a Fed conference on stress testing. We might get clues as to what the Fed is thinking on the economy. Folks pay careful attention to every remark he makes. Then on Thursday, the CPI report for June is released. We’ll also get an update on the budget for this year. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Europe Tamed a Populist and Now He’s Paying the Price

China Reiterates Demand That U.S. Must Lift All Tariffs

What Economists Are Saying Ahead of the June U.S. Jobs Report

Consumers Are Spending. Businesses Aren’t. Who’s Right About the Future?

‘Safe Like China’: In Argentina, ZTE Finds Eager Buyer for Surveillance Tech

Telemundo, Presidential Debate Under Its Belt, Moves Into 2020 Spotlight

Univision Owners Seek Exit After Tumultuous Run

Beverage Companies Embrace Recycling, Until It Costs Them

UK Competition Regulator Puts Brake on Amazon’s Deliveroo Investment

Interest Rates Just Keep Falling. Economic Orthodoxy Is Falling With Them.

Deutsche Bank’s Fleeting U.S. Dreams to Be Unraveled in Revamp

Ferraris Seized by Danish Police in Crackdown on Tax Evasion

Roger Nusbaum: What Have You Learned?

Jeff Miller: Payroll Employment Data: You Can’t Believe Your Eyes

Joshua Brown: The Broker Who Saved America

Be sure to follow me on Twitter.

South Korea Says May Retaliate Against Japan High-Tech Export Curbs

Draghi Should Replace Lagarde at the IMF

Trump’s Decision to Tap Shelton Creates Political Risk for the Fed

Gold Bull Mobius Says Every Portfolio Needs at Least 10%

Coca-Cola Gets Good News, Monster Beverage Gets Bad News

Tesla Delivers a Win for Bulls, but Investors Should Hold Off on Shifting to Ludicrous Mode

Samsung in Hot Water Over Splashy Australian Phone Ads

Boeing Pledges $100 Million to Those Affected by 737 Max Crashes

The Horrible Place Between the Apps

BMW and Daimler Team Up On Automated Driving

Cullen Roche: When “Bonds” Aren’t Bonds

Howard Lindzon: Is It Safe?

Jeff Carter: When You Get to The Top Of The Mountain, It’s Easy to Give Advice

Be sure to follow me on Twitter.

The stock market closes at 1 p.m. today and it’s pretty quiet out there. The market is up this morning and the Buy List just made a new high. We’re now up 22% on the year.

The market is closed tomorrow but it will be open on Friday. That’s also when we’ll get the official jobs report. This morning, ADP said that by there numbers, 102,000 jobs were created last month. The market seems to think there’s a good chance the Friday report will be bad and the Fed will have to step in and cut rates.

The Industries Propelling the S&P to Records Aren’t the Ones Driving the Economic Expansion

Say Hello to the E.C.B.’s New Chief, Christine Lagarde

The Politicians Are Taking Charge at the ECB

Trump Picks Two Fed Nominees Likely to Support Easier Policy

U.S. Jobs Report Holds Make-or-Break Sway Over Fed Rate Strategy

U.S. Government Staff Told to Treat Huawei as Blacklisted

Samsung Electronics’ Second-Quarter Profit Likely Halved as Huawei Woes Worsen Chip Glut

Coal-Fired Power Plants Just Had Their Worst Month in Decades

Citing ‘Massive Risks,’ House Democrats Ask Facebook to Halt its Cryptocurrency Plans

Tesla Delivers Record Number of Electric Cars in Quarter, Shares Up 7%

U.S. Judge to Slash $80 Million Roundup Jury Verdict

Lee Iacocca, Visionary Automaker Who Led Both Ford and Chrysler, Is Dead at 94

Nick Maggiulli: Should You Take the Annuity or the Lump Sum?

Ben Carlson: On The Benefits of Being Average & The Upside of a Recession

Michael Batnick: Animal Spirits, Talk Your Book: Factor Investing With Invesco & Animal Spirits: A Single Pushup

Be sure to follow me on Twitter.

USTR Proposes $4 Billion in Potential Additional Tariffs Over EU Aircraft Subsidies

Li Keqiang, Chinese Premier, Makes a Modest Peace Offering on Trade

Trump Talk of Easing Huawei Ban Lifts Suppliers’ Shares Despite Doubts

OPEC Extends Oil Cut to Prop Up Prices as Economy Weakens

To Evade Sanctions on Iran, Ships Vanish in Plain Sight

Saudi Aramco to Restart Preparations for Mega IPO

Roubini Lives Up to ‘Dr. Doom’ Alias With Global Recession Call

Rich Get Richer, Everyone Else Not So Much in Record U.S. Expansion

Japan Resumes Commercial Whaling. But Is There an Appetite for It?

Chobani Turns to Fair-Trade Program to Help Struggling Dairy Industry

Nike Pulls ‘Betsy Ross Flag’ Shoes at Kaepernick’s Urging

Empty Desks and Early Beers: Life at Deutsche Bank in New York

Cullen Roche: The Longest Recovery Ever – Does it Matter?

Joshua Brown: Fama vs. Shiller: Are Markets Efficient or Not?

Jeff Carter: Tipping Points

Be sure to follow me on Twitter.

The Dow had its best June in 81 years, and the S&P 500 had its best June in decades. The market had its best first half in over 20 years.

Everything seems to be going right for stocks. The market was up again today. Our Buy List is now up over 20% for the year.

This morning, the ISM report came in a bit weak. It was just 51.7. This was the lowest ISM since October 2016. I should add that the economy has had a period of doing just fine with low ISMs.

With the July 4 holiday, trading will be shortened this week. The exchanges close early on Wednesday and they’re closed all day on Thursday. After that, we’ll get the big June jobs report on Friday.

The market opened much higher this morning, but we slowly lost ground all day. It was still a good day but most of the hard work happened before the bell. We had news highs today from AFLAC, Cerner, Danaher, Fiserv and Stryker. Torchmark came within a penny of a new high.

E.U. Signs Trade Deal With Vietnam

Swiss Stocks Trade Smoothly on Day One Without EU Recognition

Russians Do Without as Government Squirrels Away $100 Billion

Trump Restarts China Trade Talks, but the Two Sides Remain Far Apart.

What Trump’s Huawei Reversal Means for the Future of 5G

What Just Happened Also Occurred Before The Last 7 U.S. Recessions. Reason To Worry?

As U.S. Expansion Notches Record, Recovery May Have Only Just Begun

Factories Faltered in June, Trade Truce Fails to Brighten Outlook

Traders Seen Sticking to Fed Rate-Cut Bets as Tariffs Remain

Iran Warns ‘Unilateralism’ Between Saudi Arabia and Russia Could Lead to the Death of OPEC

U.S. Oil Companies Find Energy Independence Isn’t So Profitable

Deutsche Bank Plans to Cut as Many as 20,000 Jobs in Revamp

Jeff Miller: Chinese Fireworks?

Howard Lindzon: Catching Up On Bitcoin

Roger Nusbaum: That’s What I’m Talking About

Be sure to follow me on Twitter.

-

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His Buy List has beaten the S&P 500 over the last 20 years. (more)

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His Buy List has beaten the S&P 500 over the last 20 years. (more)

-

Archives