-

Morning News: May 15, 2019

Posted by Eddy Elfenbein on May 15th, 2019 at 7:11 amThe Global Economy Was Improving. Then the Fighting Resumed.

China’s Economy Lost Momentum Even Ahead of Trump’s New Tariffs

Trump’s Tariffs, Once Seen as Leverage, May Be Here to Stay

In China, Some Fear the End of ‘Chimerica’

Rising U.S. Oil Output Helps Fill Gap Left by Iran, Venezuela: IEA

Rise of Smaller Rivals Throws Up Fresh Challenge to Bitcoin

U.S. 2018 Births Fall to Lowest Level in 32 Years

Tencent Beats Estimates, Signaling the Worst Is Behind It

Startups Target Banks’ Small Business Customers in FX Payments Drive

You Can No Longer Buy a $35,000 Tesla Model 3 — the Price Just Went Up

Caesars, ESPN Forge Sports-Betting Partnership

Netflix Is Losing Some of Its Most Popular Shows, Thanks to AT&T

Nick Maggiulli: Losing More Than a Bet

Lawrence Hamtil: How Inflation Makes the ‘Value’ Factor a Sector Bet

Roger Nusbaum: Simple Vs Easy & Is Bitcoin Talebian?

Be sure to follow me on Twitter.

-

Morning News: May 14, 2019

Posted by Eddy Elfenbein on May 14th, 2019 at 7:14 amOil Rises as Saudi Arabia Reports Drone Attacks on Pump Stations

Modi Cut India’s Red Tape. Now He Hopes to Win Votes for His Work.

U.S. Readies New Tariffs as Trump Says He’ll Meet China’s Xi

Fed’s Williams Says Policymakers Need to Better Prepare for Lower Interest Rate World

Supreme Court Allows Antitrust Lawsuit Against Apple to Proceed

Israeli Firm Tied to Tool That Uses WhatsApp Flaw to Spy on Activists

Bayer Stock Continues Rout After $2 billion Award in Roundup Trial

Uber Blame Game Focuses on Morgan Stanley After Shares Drop

Members Only: U.S. Retailers Revamp Loyalty Schemes for Amazon Era

The $1.9 Trillion Fund Giant With a Crazy Idea About Investing

As Swine Fever Roils Asia, Hogs Are Culled and Dinner Plans Change

Nissan Flags Weakest Profit in 11 Years, Ghosn Woes, Bleak Sales Weigh

Ben Carlson: What Inning Are We In?

Michael Batnick: What Do You Know Now?

Joshua Brown: The Book That Changed My Life & Buyable VIX Spike

Be sure to follow me on Twitter.

-

Morning News: May 13, 2019

Posted by Eddy Elfenbein on May 13th, 2019 at 7:20 amPakistan to Accept $6 Billion Bailout From I.M.F.

Saudi Arabia Says Oil Tankers Attacked as Iran Tensions Rise

U.S.-China Trade Standoff May Be Initial Skirmish in Broader Economic War

Trump Trade Talks With China Head for Stalemate

Making America Carbon Neutral Could Cost $1 Trillion a Year

Morgan Stanley Says Rest of 2019 Might Turn Against U.S. Markets

As TV Industry’s $20 Billion Week Starts, Signs That Streaming Isn’t King Yet

Why Rewards for Loyal Spenders Are ‘a Honey Pot for Hackers’

Amazon Rolls Out Machines That Pack Orders and Replace Jobs

Impossible Foods Raises $300 Million with Investors Eager for Bite of Meatless Burgers

Bar Rises for Shale Takeovers as Chevron Bows Out of Anadarko Fight

Howard Lindzon: Momentum Monday – Those Darn Tariffs

Jeff Miller: Weighing the Week Ahead: Stalemate?

Jeff Carter: Stablecoins vs Derivatives

Be sure to follow me on Twitter.

-

CWS Market Review – May 12, 2019

Posted by Eddy Elfenbein on May 12th, 2019 at 7:08 am“The greatest ability in business is to get along with others and to influence their actions.” – John Hancock

Fourteen years ago, Twitter didn’t exist. Today it can help destroy trillions of dollars in global market cap. Bloomberg ran the numbers and found that President Trump’s 102-word tweet storm regarding Chinese tariffs sparked a selloff that totaled $1.36 trillion. The volatility index jumped 50% in just two days—and it all began with two tweets.

Does this mark the beginning of the end? Eh…I doubt it. Let’s remember that the bulls have had a good run this year, so it’s natural for the bears to strike back. First, some recent history. On April 26, the S&P 500 finished the session at an all-time high close. In other words, we made back everything we lost from the ugly market we had late last year. Then on Tuesday, April 30, the index closed out the month at 2,945.83, yet another all-time high close.

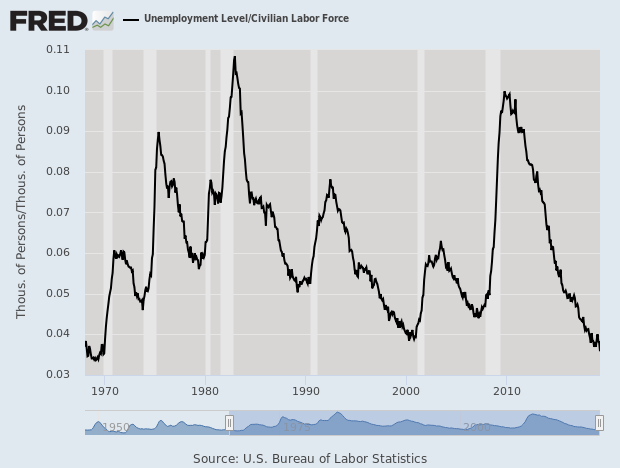

On Friday, May 3, the government reported that the unemployment rate fell to its lowest point in 50 years. That day, the S&P 500 closed at 2,945.64, a hair below its all-time high close from three days before. That can often be a bad omen, when the index fails to make a new high, even by a tiny bit.

After that, we got the president’s tweets, and then bad things started to happen. The S&P 500 fell four days in a row for a total loss of 2.54%. Of course, in the large scheme of things, that’s not a very big loss. Plus, the market gained another 0.37% on Friday.

So what’s going on? In this week’s issue, we’ll take a closer look at the president’s tweets and their impact on the market. We’ll also focus on our three Buy List earnings reports from this week. I’m also happy to say that our Buy List has been performing quite well versus the market in recent days. As usual, when investors get scared, they find solace in high-quality stocks, and that’s us. But first, let’s look at the amazing April jobs report.

The Lowest Jobless Rate in 50 Years

On Friday, May 3, the government reported that the unemployment rate fell to 3.6%. That’s the lowest level since December 1969. If we look at the peacetime rate, then it’s the lowest in 70 years. For women, we now have the lowest jobless rate since 1953. The brief slowdown we saw earlier this year has clearly passed.

The jobs report said the U.S. economy created 263,000 net new jobs last month. If you recall, we had a pretty lousy jobs report just two months ago. The government said the economy created just 20,000 net new jobs in February. That report shocked a lot of people, and some even thought it might be the beginning of a recession. As it turns out, the February slowdown was a minor blip in the economy. The jobs gain for February has now been revised upward to a gain of 56,000 jobs.

There is a weak spot amid the good news, and that’s wage growth, which is still sluggish. Over the past year, average hourly earnings are up 3.2%. That’s better, but I’d like to see it higher. Higher wages means more revenue for businesses. Plus, there’s no evidence that inflation is heating up. On Friday, the government said that consumer prices rose 0.3% last month. That’s not much, and the “core” rate increased by 0.1%. That’s the third month in a row that core inflation is up by 0.1%. Over the last year, inflation is up 2%, while core inflation is up 2.1%. This is good news for investors. Importantly, it suggests that the Fed won’t do much for the rest of this year.

Now let’s look at the Twitter front of the trade war. The stock market got spooked this week by a pair of tweets President Trump posted last Sunday evening. In them, he threatened to escalate the brewing trade war with China. I need to stress that markets aren’t particularly worried about the tariffs the U.S. imposes. Rather, they’re concerned about retaliatory tariffs from China, or other countries, on U.S-made goods. Worst of all, this kerfuffle could spark an all-out trade war in which tariffs are constantly hiked by two sides that refuse to back down.

In the short term, tariffs on Chinese goods would give a quick boost to their U.S.-based competitors. Of course, those companies would quickly raise prices on consumers since the playing field has been emptied. But it gets tricky because trade is a nonlinear relationship. For example, tariffs would also hurt American companies that rely on suppliers based in China. The recent CPI report showed that inflation isn’t a problem, so consumers aren’t yet feeling the pinch of these policies.

I think the safe assumption is that the trade threats can only go so far. Both sides have too much to lose. President Trump has often mentioned that in negotiations, he likes to talk tough as an initial bid only to soften his stance as the discussions progress. That leaves the White House in a precarious situation where it wants to convince China that it’s serious while assuring financial markets that it’s open to bargaining.

There could be something to this. On Friday, the Dow staged a 450-point comeback after President Trump tweeted positive comments on trade negotiations. He even left the door open to tariffs being removed in the future. Surely, much of this (on both sides) is due to domestic political concerns rather than a coherent overview of trade policy.

As usual, I’ll skip the political angle and focus on what it means for us. Make no mistake, a trade war is bad for business. The recent tariffs aren’t good for stock investors. However, it’s in everyone’s interest to work together on these issues. That’s why the trade rhetoric will be much more heated than actual policy. The tariffs are a thorn in the side, not a dagger in the heart. The overall climate continues to be very good for investors.

On that note—though I’ll probably jinx it by even mentioning it—the market’s recent slide has been quite good for our Buy List. I should add that I mean that in a relative sense. We’re down, but not as much as everyone else. I sometimes hear investors criticize me for the “we suck less” argument, but in my view, these are the periods that really separate good investors from the pack.

Over the last week, our Buy List is down 0.65% compared to the S&P 500’s loss of 2.18%. That’s a lot for one week. Since April 22, the Buy List is up 1.61%, while the S&P 500 is down 0.91%. I should caution investors not to be overly frightened by short-term losses nor overly pleased by short-term gains. As always, we’re focused on the long term.

Through Friday, our Buy List is up 16.59% this year (that doesn’t include dividends). The S&P 500 is up 14.94%. Sixteen of our 25 stocks are beating the market. FactSet (FDS) is our biggest winner with a 40% YTD gain. Eight of our stocks are up more than 22% on the year.

At the beginning of 2018, we added Church & Dwight (CHD) as a new stock. Early on, it was a flop, but I’m glad we stuck with it. In a little over a year, CHD is up over 61%. In fact, most of our defensive stocks have been doing well lately, names like Smucker (SJM) and AFLAC (AFL). Hershey (HSY) has also been strong. This makes sense. A trade war won’t have much of an impact on the chocolate-bar biz. Now let’s look at some recent earnings news.

Three Buy List Earnings Reports this Week

We had our final three Buy List earnings reports of this earnings season. On Tuesday, Broadridge Financial Solutions (BR) reported fiscal Q3 earnings of $1.59 per share. That was nine cents better than expectations.

However, Broadridge had mixed news on their guidance. The company lowered its full-year revenue growth forecast from 3% to 5% down to about 1%. BR reiterated its full-year EPS growth of 9% to 13%. Last year, the company made $4.19 per share, so the current outlook works out to $4.57 to $4.73 per share. Through the first three quarters, Broadridge had earned $2.94 per share.

The shares pulled back a bit on Tuesday but stabilized and then rallied on Friday. The CEO said, “After a solid third quarter, Broadridge is very well-positioned to deliver strong full-year results.” I have to agree. In the last seven weeks, the stock is up 19%. This week, I’m lifting my Buy Below on Broadridge to $125 per share.

After the bell on Wednesday, Disney (DIS) reported Q1 earnings of $1.61 per share, three cents better than estimates. There’s been so much news about Disney recently that the earnings report almost seems anti-climatic.

Disney said it expects Disney+, the new streaming service, to be profitable by 2024. The Avengers movie is still crushing it at the box office, and the theme parks had a very good Q1. Net income for the parks totaled $1.5 billion for the first quarter.

Disney’s overall profits are down this year, but that’s because of the big movie hits it had in 2017. That’s the nature of the entertainment business. I really like the direction that Disney is taking. I’m raising my Buy Below on Disney to $140 per share.

While I like the news from the previous two companies, I wasn’t thrilled by the news from Becton, Dickinson (BDX). For Q2, the company reported earnings of $2.59 per share, which beat estimates by one penny per share.

Becton, Dickinson lowered its full-year revenue guidance of growth of 8.5% to 9.5% down to 8.0% to 9.0%. The company blamed the negative impact of currency exchange. BDX hasn’t changed its currency-neutral forecast of revenue growth of 4% to 6%. Becton sees full-year earnings ranging from $11.65 to $11.75. The company blames currency exchanges plus “recent regulatory and market pressures related to paclitaxel-coated devices.” The previous range was $12.05 to $12.15 per share.

The shares dropped over 3% at Thursday’s open. Fortunately, the stock didn’t fall as much as I had feared. Nevertheless, I’m lowering my Buy Below on Becton from $260 to $234 per share.

That concludes the first-quarter earnings season for our Buy List stocks. Coming up, we have three Buy List stocks with reporting quarters that ended in April. The three stocks are Hormel Foods (HRL), JM Smucker (SJM) and Ross Stores (ROST). Ross and Hormel are due to report on May 23, while Smucker is due to report on June 6.

That’s all for now. I expect to see more volatility in the market next week. We’re going to get a few key economic reports. On Wednesday, the retail-sales report for April is released. This will be one of our first data points to see how well Q2 is looking. Also on Wednesday, we’ll also see the report on industrial production. On Thursday, we’ll get the housing-starts report, plus another jobless-claims report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: May 10, 2019

Posted by Eddy Elfenbein on May 10th, 2019 at 7:03 amThe ECB Weighs a Profound Shift in Policy

Argentina Was Supposed to Be Over Populism. Economic Misery Could Bring It Back

U.S. Hikes Tariffs on $200B of Chinese Goods. China Says It Will Retaliate

A Short Seller Bets It All on a Spectacular Market Crash

The VC Who Engineered the 2017 Uber CEO Coup Just Got Very Rich

Banks Waking Up to Fintech Threat Throw Billions Into Digital

A $90 Billion Fee Pool Beckons as BofA Considers First Data Split

Occidental Petroleum Emerges With the Prize in a Takeover Fight

Facebook Rejects Co-Founder Call for Breakup, Senator Urges U.S. Antitrust Probe

AB InBev Files for Hong Kong IPO of Asia Business to Raise $5 Billion

Sam Adams Brewer to Buy Rival Dogfish Head in $300 Million Deal

Trash, the Library and a Worn, Brown Table: The 2019 College Essays on Money

Ben Carlson: Financial Superpowers

Roger Nusbaum: take Your Bitcoin and Head to Ecuador

Joshua Brown: Coming Up! & Whoever is Winning At the Moment Will Always Seem to Be Invincible.

Be sure to follow me on Twitter.

-

Q1 2019 Earnings Calendar

Posted by Eddy Elfenbein on May 9th, 2019 at 4:39 pmTwenty of our 25 Buy List stocks have reported their Q1 earnings this cycle. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

Company Ticker Date Estimate Result Eagle Bancorp EGBN 17-Apr $1.12 $1.11 Signature Bank SBNY 17-Apr $2.77 $2.65 Torchmark TMK 17-Apr $1.59 $1.64 Check Point Software CHKP 18-Apr $1.31 $1.32 Danaher DHR 18-Apr $1.01 $1.07 Sherwin-Williams SHW 23-Apr $3.69 $3.60 Stryker SYK 23-Apr $1.84 $1.88 Moody’s MCO 24-Apr $1.93 $2.07 AFLAC AFL 25-Apr $1.06 $1.13 Cerner CERN 25-Apr $0.61 $0.61 Hershey HSY 25-Apr $1.46 $1.59 Raytheon RTN 25-Apr $2.47 $2.77 Fiserv FISV 30-Apr $0.82 $0.84 Church & Dwight CHD 2-May $0.66 $0.70 Cognizant Technology Solutions CTSH 2-May $1.04 $0.91 Continental Building Products CBPX 2-May $0.34 $0.42 Intercontinental Exchange ICE 2-May $0.90 $0.92 Broadridge Financial BR 7-May $1.50 $1.59 Disney DIS 8-May $1.58 $1.61 Becton, Dickinson BDX 9-May $2.58 $2.59 Morning News: May 9, 2019

Posted by Eddy Elfenbein on May 9th, 2019 at 6:57 amWhy China Decided to Play Hardball in Trade Talks

Weakest U.S. Bond Auction in Decade Validates Dimon’s Warning

U.S. Recession Would Spur ‘Massive’ Corporate Bond Losses, Eisman Says

Walmart Raises Minimum Age to Buy Tobacco Products to 21

Intel Shares Drop, Three-Year Outlook Seen Lagging Rivals

EQT and Digital Colony Agree to Buy Zayo for Over $8 Billion

New York Times Posts Higher Profit, Adds 223,000 Digital Subscribers

Novartis to Buy Takeda Eye Drug Assets in $5.3 Billion Deal

Roku’s Platform Revenue Soars, Sending the Stock Higher

Uber Is Going Public: How Today’s Tech I.P.O.s Differ From the Dot-Com Boom

The Answer to Uber’s Profit Challenge? It May Lie In Its Trove of Data

China to Bid on D.C. Metro Rail Deal as National Security Hawks Circle

Jeff Miller: Stock Exchange: Do You Trade News Cycles Or Market Cycles?

Cullen Roche: Capitalism Vs. Socialism

Michael Batnick: The Big Short, The Rorschach Test & Imagining a Different World

Be sure to follow me on Twitter.

Becton, Dickinson’s Fiscal Q2 Results

Posted by Eddy Elfenbein on May 9th, 2019 at 6:18 amAs reported, revenues of $4.195 billion decreased 0.6 percent.

– On a comparable, currency-neutral basis, revenues increased 3.4 percent.

– As reported, diluted earnings per share of $(0.07) increased 63.2 percent.

– As adjusted, diluted earnings per share of $2.59 decreased 2.3 percent, and increased 7.2 percent on a currency-neutral basis.

– The company reaffirmed its full fiscal year 2019 comparable, currency-neutral revenue guidance, and updated its adjusted diluted earnings per share guidance.BD (Becton, Dickinson and Company) (NYSE: BDX), a leading global medical technology company, today reported quarterly revenues of $4.195 billion for the second fiscal quarter ended March 31, 2019. This represents a decrease of 0.6 percent from the prior-year period. On a comparable, currency-neutral basis, revenues increased 3.4 percent over the prior-year period.

“Through the second quarter we have delivered solid revenue growth and operating performance,” said Vincent A. Forlenza, chairman and CEO. “Our revised fiscal year 2019 outlook reflects recent, near-term regulatory and market pressures related to paclitaxel-coated devices and foreign currency, which will affect our EPS guidance range. We remain confident that our business is strong, fundamentals are in-tact, and we will continue to deliver value to our shareholders and customers around the world.”

Second Quarter and Six-Month Fiscal 2019 Operating Results

As reported, diluted earnings per share for the second quarter were $(0.07), compared with $(0.19) in the prior-year period. This represents an increase of 63.2 percent. Adjusted diluted earnings per share were $2.59, compared with $2.65 in the prior-year period. This represents a decrease in adjusted diluted earnings per share of 2.3 percent, or an increase of 7.2 percent on a currency-neutral basis.

For the six-month period ended March 31, 2019, as reported, diluted earnings per share were $1.98, compared with $(0.90) in the prior-year period. This represents an increase of 320.0 percent. Adjusted diluted earnings per share were $5.29, compared with $5.15 in the prior-year period. This represents an increase in adjusted diluted earnings per share of 2.7 percent, or 10.5 percent on a currency-neutral basis.

Current period adjusted results exclude, among other items, charges to record product liability reserves of $331 million and the estimated cost of a product recall of $65 million.

Segment Results

In the BD Medical segment, as reported, worldwide revenues for the quarter of $2.180 billion increased 0.4 percent over the prior-year period, or 3.8 percent on a comparable, currency-neutral basis. The segment’s results were driven by performance in the Medication Management Solutions, Diabetes Care and Pharmaceutical Systems units. Performance in the Medication Delivery Solutions unit reflects a tough comparison to the prior year, as well as distributor inventory adjustments during the quarter in the United States.

For the six-month period ended March 31, 2019, BD Medical revenues were $4.316 billion as reported, which represents an increase of 7.2 percent over the prior-year period. On a comparable, currency-neutral basis, BD Medical revenues increased 4.5 percent.

In the BD Life Sciences segment, as reported, worldwide revenues for the quarter of $1.052 billion decreased 4.2 percent from the prior-year period. On a comparable, currency-neutral basis, revenues increased 2.7 percent. Revenue growth was driven by performance in the Biosciences and Preanalytical Systems units. Growth in the Diagnostic Systems unit reflects a tough comparison to the strong flu season in the prior-year period.

For the six-month period ended March 31, 2019, BD Life Sciences revenues were $2.108 billion as reported, which represents a decrease of 1.6 percent from the prior-year period. On a comparable, currency-neutral basis, BD Life Sciences revenues of $2.099 billion increased 3.7 percent.

In the BD Interventional segment, as reported, worldwide revenues for the quarter of $0.963 billion increased 1.1 percent over the prior-year period, or 3.5 percent on a comparable, currency-neutral basis. The segment’s results were driven by performance in the Urology and Critical Care and Peripheral Intervention units. Growth in the Surgery unit reflects a tough comparison to the prior-year period.

For the six-month period ended March 31, 2019, BD Interventional revenues were $1.932 billion as reported, which represents an increase of 70.2 percent over the prior-year period. On a comparable, currency-neutral basis, BD Interventional revenues increased 4.6 percent.

Geographic Results

As reported, second quarter revenues in the U.S. of $2.341 billion increased 0.7 percent from the prior-year period. On a comparable basis, U.S. revenues increased 2.2 percent over the prior-year period. Growth in the U.S. was driven by performance in the BD Medical and BD Interventional segments. BD Life Sciences’ growth in the U.S. reflects the aforementioned comparison to a strong flu season in the prior year in the Diagnostic Systems unit.

As reported, revenues outside of the U.S. of $1.854 billion decreased 2.3 percent from the prior-year period. On a comparable, currency-neutral basis, revenues outside of the U.S. increased 4.9 percent over the prior-year period. International revenue growth was driven by strong performance in China and EMA.

For the six-month period ended March 31, 2019, U.S. revenues were $4.728 billion as reported, which represents an increase of 18.7 percent over the prior-year period. On a comparable basis, U.S. revenues of $4.724 billion grew 4.1 percent over the prior-year period. As reported, revenues outside of the U.S. of $3.628 billion grew 9.2 percent over the prior-year period. On a comparable, currency-neutral basis, revenues outside the U.S. of $3.623 billion grew 4.5 percent over the prior-year period.

Fiscal 2019 Outlook for Full Year

As reported, the company expects full fiscal year 2019 revenues to increase 8.0 to 9.0 percent, compared to 8.5 to 9.5 percent previously communicated, due to the estimated additional negative impact from foreign currency. The company continues to estimate full fiscal year 2019 revenues will increase 5.0 to 6.0 percent on a comparable, currency-neutral basis.

The company expects adjusted diluted earnings per share to be between $11.65 and $11.75, resulting in growth of approximately 12.0 percent on a currency-neutral basis. This is a decrease from previously issued guidance of approximately 13.0 to 14.0 percent growth, and is due to recent regulatory and market pressures related to paclitaxel-coated devices. Including the estimated additional unfavorable impact of foreign currency, adjusted diluted earnings per share are expected to grow approximately 6.0 to 7.0 percent over fiscal 2018 adjusted diluted earnings per share of $11.01.

Estimated adjusted diluted earnings per share for fiscal 2019 excludes potential charges or gains that may be recorded during the fiscal year, such as, among other things, the non-cash amortization of intangible assets, acquisition-related charges, and certain tax matters. BD does not attempt to provide reconciliations of forward-looking non-GAAP earnings guidance to the comparable GAAP measure because the impact and timing of these potential charges or gains is inherently uncertain and difficult to predict and is unavailable without unreasonable efforts. In addition, the company believes such reconciliations would imply a degree of precision and certainty that could be confusing to investors. Such items could have a substantial impact on GAAP measures of BD’s financial performance.

“Cerner Controls a Quarter of Electronic Medical Records Market”

Posted by Eddy Elfenbein on May 9th, 2019 at 5:53 amFrom the Kansas City Business Journal:

Cerner Corp., along with its competitor Epic Systems Corp., ruled the electronic health record (EHR) market in 2018, with a combined 85 percent market share in the large, 500-plus-bed hospital space, according to KLAS Research reports cited in Healthcare Dive. Epic holds a 58 percent share, while Cerner holds 27 percent.

The split is closer when it comes to all acute care hospitals in the U.S. In this larger market, Epic has a 28 percent market share and North Kansas City-based Cerner (Nasdaq: CERN) claims 26 percent of the market.

Although fewer large hospitals and health systems are buying EHRs — 80 percent of all doctors will be working at a facility that uses an EHR system by the end of this year according to Business Insider — Cerner signed the most new hospitals last year. This is due, in part, to a 10-year, $10 billion contract with the U.S. Department of Veterans Affairs. The contract, won in May 2018, includes 147 acute care and 20 specialty contracts.

In February, the VA terminated a $624 million 2015 contract with Epic and Leidos Holdings Inc. (NYSE: LDOS) so that it could adopt Cerner’s patient scheduling system, Millennium. It’s unclear how much Cerner’s new contract is worth.

In contrast, Cerner lost 65 Millennium EHR customers in the private hospital sector, including 52 from a single health system.

EHR purchases in 2018 were higher than previous years, with the continued consolidation of the health care market helping to drive those 445 deals. Since 2014, a fifth of all EHR switches at acute care hospitals have stemmed from mergers and acquisitions, according to KLAS.

Disney Beats Earnings

Posted by Eddy Elfenbein on May 8th, 2019 at 6:32 pmAfter the bell, Disney (DIS) earned $1.61 per share. That was three cents better than estimates. The stock is up a bit after hours.

Walt Disney Co’s theme parks lifted quarterly earnings past Wall Street targets on Wednesday, helping offset big investments to support the media and entertainment company’s bid to draw audiences to streaming media.

Shares of Disney rose 1.5 percent to $137 in after-hours trading.

“Avengers: Endgame”, the end of a decade-long superhero series with $2.2 billion in box office sales worldwide, will stream exclusively on Disney+ starting Dec. 11, the company announced.

Growth at Disney parks in the United States boosted results above analyst expectations. From January to March, Disney reported adjusted earnings per share of $1.61, ahead of analyst estimates of $1.58, according to IBES data from Refinitiv. Heavy investment accounted for a 13 percent drop from a year ago by that measure.

Revenue rose 3 percent to $14.92 billion. Analysts had been expecting a small decline.

Disney is trying to transform from a cable TV leader to a streaming media powerhouse that, like Netflix Inc, sells subscriptions directly to consumers. Costs to build digital services will weigh on profits for several years, the company has said.

Its biggest streaming bet, the family-oriented Disney+, is set to launch in November. The company told analysts in April that it expects Disney+ to achieve profitability in fiscal 2024.

The just-ended quarter reflected the purchase of film and TV assets from 21st Century Fox, which brought Disney more content for its streaming future.

For the quarter, the direct-to-consumer and international unit recorded a loss of $393 million from streaming costs.

Disney also recorded a $353 impairment charge from its ownership stake in media startup Vice.

In the theme park unit, net income hit $1.5 billion as more visitors showed up at Walt Disney World in Florida and at Hong Kong Disneyland, and occupied hotel nights increased.

“Increased ticket prices haven’t put visitors off, and hotels continue to be a major driver of additional spending,” said Nicholas Hyett, equity analyst at Hargreaves Lansdown. “It’s easy to get caught up in the hype surrounding new films … but it’s the less glamorous Media Networks and Parks that pay the lion’s share of the bills.”

Overall net income jumped 85 percent, to $5.4 billion, thanks to Disney’s acquisition of a controlling stake in Hulu through the Fox acquisition.

Media networks, a division that includes ESPN and ABC, reported $2.2 billion in operating income for the quarter.

The movie studio reported profit of $534 million, lifted by “Captain Marvel,” which was a global hit but did not reach the level of “Black Panther” and “Star Wars: The Last Jedi” a year earlier.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His