-

Morning News: August 11, 2025

Posted by Eddy Elfenbein on August 11th, 2025 at 7:08 amThe Dollar Still Rules, But US Policy Is Making It Less Special

Forgotten US Global Bond Funds Face ‘Show-Me-the-Money’ Moment

Hedge Fund Schonfeld’s Millennial Boss Drags It Back From the Brink

The Death of Diversification: Why Buffett Was Right All Along

Is Dow Inc. Doxing the Shareholders Who Ask the Wrong Questions?

Inflation Up or Down? What About Jobs? The Agency That Should Know Is on the Rocks

What Happens When Politicians Meddle With Economic Data: Argentina’s Example

The U.S. Marches Toward State Capitalism With American Characteristics

On Economic Policy, the White House Is Its Own Worst Enemy

Supercharging ICE Threatens to Be a Costly Mistake

The Economy Is Starting to Pay for Trump’s Chaos

US Consumers to Bear Brunt of Tariff Hit, Goldman Economists Say

Small Businesses Brace for the Punishing Side Effects of Trump’s Tariffs

Small US Firms Paying Trump Tariffs Face $202 Billion Annual Hit

How to Offset Trump’s Aluminum Tariffs: Recycle Your Beer Can

Orsted Shares Tumble After Halting of U.S. Wind Project Sale; $9.4 Billion Rights Issue Proposal

Lab-Grown Diamonds Are Testing the Power of Markets

Lithium Market Soars as CATL Shuts One of World’s Biggest Mines

Rare-Earth Magnet Maker Raises $65 Million in Push to Counter China

China’s Automakers Are Taking a Shortcut to European Markets

Builder China South City Ordered to Liquidate by Hong Kong Court

U.S. Government to Take Cut of Nvidia and AMD A.I. Chip Sales to China

An AI Replay of the Browser Wars, Bankrolled by Google

Rumble Mulls $1.17 Billion All-Stock Deal For Northern Data

Goodbye, $165,000 Tech Jobs. Student Coders Seek Work at Chipotle.

AOL Will End Its Dial-Up Internet Service (Yes, It’s Still Operating)

Activist Investor to Push Avantor to Make Changes or Sell Itself

Inside Target, Frustrated Employees and the Search for a New CEO

Can AriZona’s 99-Cent Iced Tea Survive Trump’s Tariffs?

Be sure to follow me on Twitter.

-

Morning News: August 8, 2025

Posted by Eddy Elfenbein on August 8th, 2025 at 7:01 amIsrael to Seize Gaza City, Stopping Short of Full Takeover

Can Russia’s Economy Withstand Trump’s Pressure?

China Defends Buying Russian Oil After Trump’s Tariff Threat

Congo Peace May Herald $700 Million Power Deal With US Company

A Mile Underground, America’s Largest Untapped Copper Mine Inches Toward Reality

Taiwan Strained by 20% Tariffs, No Trade Deal and Political Uncertainty

Japan Says Trump to Correct ‘Extremely Regrettable’ Error in Tariff Order

Gold Hit By Surprise US Tariffs, Unleashing New Turmoil

Why a Product’s Country of Origin Matters in Trump’s Trade War

US Trade Shifts From Bretton Woods to the ‘Turnberry System’

It’s Only a Matter of Time Until Americans Pay for Trump’s Tariffs

You Don’t Enhance Free Speech By Giving Politicians Control of It

Trump’s Surprise Fed Pick Buys Him Time on Chair Selection

JPMorgan Says Treasury Curve Can Steepen on Miran Fed Pick

Sahm: The BLS Can’t Be Replaced by the Private Sector

SpongeBob on the Syllabus of Class Examining the Shackles of Work

Follow the Money: The Inevitable Rise of Crypto and Blockchain

Playing by the Rules Costs Wall Street an Extra 51 Million Hours a Year

Wall Street and AI Startups Are Fighting Over Entry-Level Quants

Don’t Turn Chip Controls Into Bargaining Chips

Trump Reminds CEOs Who the Ultimate Boss Is

Intel CEO Dogged by Decades of China Chip Bets, Board Work

Intel’s Chief Holds Firm After Trump Demands His Resignation

SoftBank Buys Foxconn’s Ohio Plant to Jumpstart Stargate AI Push

Silver Lake Invests $400 Million to Tackle Data-Center Power Bottleneck

The AI Building Boom Is Bound to Bust

E.P.A. to Stop Updating Popular Database After Lead Scientist Criticized Trump

Truck Companies Sour on California’s Strict Clean Air Rules

What If Everything We Think About Obesity Is Wrong?

Irish Whiskey Makers Crumble Under Trump’s Trade Tariffs

Nicotine Is Hot, Beer Is Not. What Vice Stocks Say About America’s Guilty Pleasures.

Be sure to follow me on Twitter.

-

Morning News: August 7, 2025

Posted by Eddy Elfenbein on August 7th, 2025 at 7:04 amA Defiant Israel Eyes a Full Gaza Takeover Despite Global Isolation

Bank of England Cuts Rates to Two-Year Low After Rare Re-Vote

China’s Exports Surged Again in July, but Not to America

German Exports to U.S. Fall for Third-Straight Month as Industry Slumps

Trump’s Tariffs Take Effect in Fresh Test for Global Economy

Trump Doubles Tariff on India to 50%, Sparking Outrage in Delhi

Southeast Asia Looks for Clarity From U.S. on ‘Rules of Origin’

‘Next Era of Dollarization’ Is Visible From Bolivia to Indonesia

US Would Be Wise Not to Count Its Winnings on Trade Just Yet

Dollar Falls to 10-Day Low as Tariffs Take Effect

This Isn’t How You Deal With Free Riders

Stablecoins, Digitized Bank Deposits, and Future Banking Risk?

Trump to Sign Order Easing Path for Private Assets in 401(k)s

Youth Is Losing to Experience in This Job Market

The BLS Isn’t Alone in Facing Data Challenges; U.K. Has Them Too

Taxation Is Easily the Least Harmful Aspect of Government Spending

US Offers to ‘Simplify’ Harvard Case Over Foreign Student Ban

Japan’s Auto Giants Are Expecting Pain Despite Trump Trade Deal

Auto Industry Takes $12 Billion Hit From Trade War

Trump’s Latest Attacks Stun Wind and Solar Industries

Space Company Firefly Poised for Wall Street Debut

The Real Nuclear Moonshot Is Here on Earth

Siemens Beats Market Views With Order Momentum in Mobility

Artificial Intelligence, and the Future of the Magnificent 7

Elon Musk Takes on Sam Altman, This Time Over the Chessboard

Foodpanda Aims to Double Pakistan Business in Three Years

Lilly Obesity Pill Cut Weight by Just 11% in Study; Shares Drop

How Ozempic’s Maker Lost Its Shine After Creating a Wonder Drug

It Was a Promising Addiction Treatment. Many Patients Never Got It.

Disney’s Thriving Parks Are Buying It Time to Figure Out Streaming

Be sure to follow me on Twitter.

-

Morning News: August 6, 2025

Posted by Eddy Elfenbein on August 6th, 2025 at 7:06 amAmerica’s Ultimatum to Russia Is About to Pass. Now What?

Ukraine Appoints Head of Economy Watchdog After Anti-Graft Protests

German Factory Orders Dip as Sluggish International Demand Weighs

Germany Gets No Bidders in Zero-Subsidy Offshore Wind Auction

Shale Oil Drillers Tap the Brakes on Production Until Prices Gain Speed

In Hawaii, New Tourism Tax Aims to Offset Costs of Climate Change

US Is Still Critically Reliant on China, ECB Finds

China Is a Nation of Savers. Many Are Drowning in Debt.

India’s Central Bank Stands Pat as Tariff Pressures Linger

The Tariff Effect: Billions in Revenue but No Economic Earthquake

Trump Ramps Up Tariff Blitz With India, Pharma, Chips in Sights

Does Japan Want American Cars? Trump’s Push to Open Foreign Markets Faces Test

Detroit Rediscovers Its Love for Giant Gas Guzzlers

Why the B.L.S. Regularly Revises Jobs Data

Trump Airs Personal Financial Grievances Ahead of ‘Debanking’ Crackdown

Goldman Trader Says Buoyant Stocks Are Ignoring Recession Risks

The New Economics of People in a World of Closing Doors

When Top Lawyers Earn $30 Million, Who Pays?

The Texas Gerrymandering Fight Could Ignite a National Fire

OpenAI in Talks for Share Sale at $500 Billion Valuation

How Palantir Won Over Washington—and Pushed Its Stock Up 600%

Disney, McDonald’s and the State of the U.S. Economy

Disney Tops Profit Estimates, Led by Parks Division, Streaming

Disney Paying $1.6 Billion for WWE Rights

The NFL Is Taking a 10% Stake in Disney’s ESPN

McDonald’s Returns to Sales Growth With Toys, Budget Meals

Uber Boosts Buybacks by $20 Billion After Upbeat Forecast

How One Company Maintained a Monopoly on U.S. Fire Retardant

Shopify Rallies on Revenue Beat, Strong Third-Quarter Outlook

Aldi’s Passionate, Cultlike Following Fuels Its Rapid Expansion Plans

Be sure to follow me on Twitter.

-

CWS Market Review – August 5, 2025

Posted by Eddy Elfenbein on August 5th, 2025 at 10:01 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Weak July Jobs Report

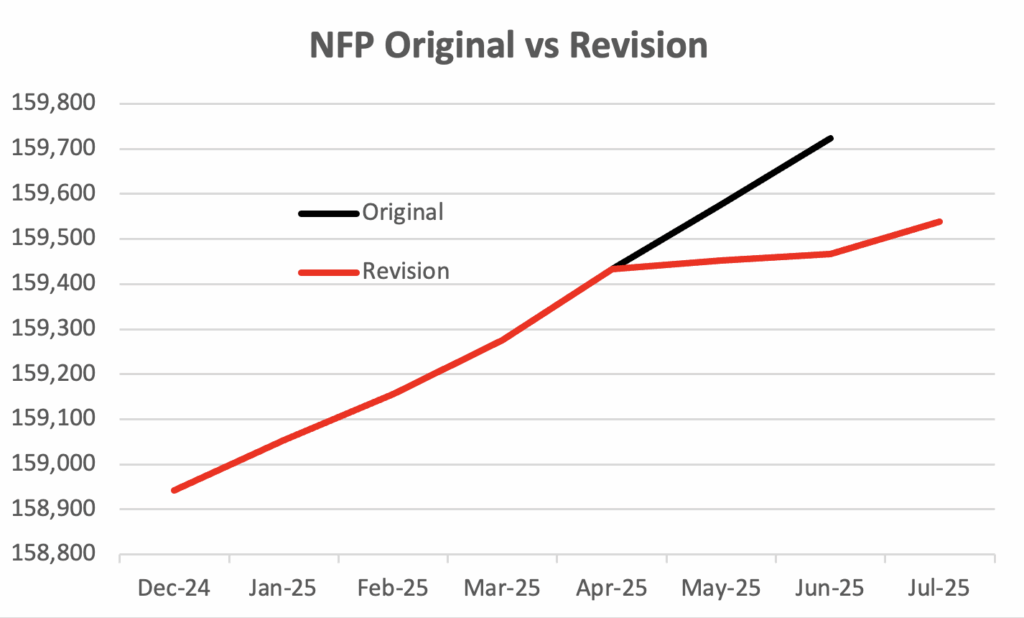

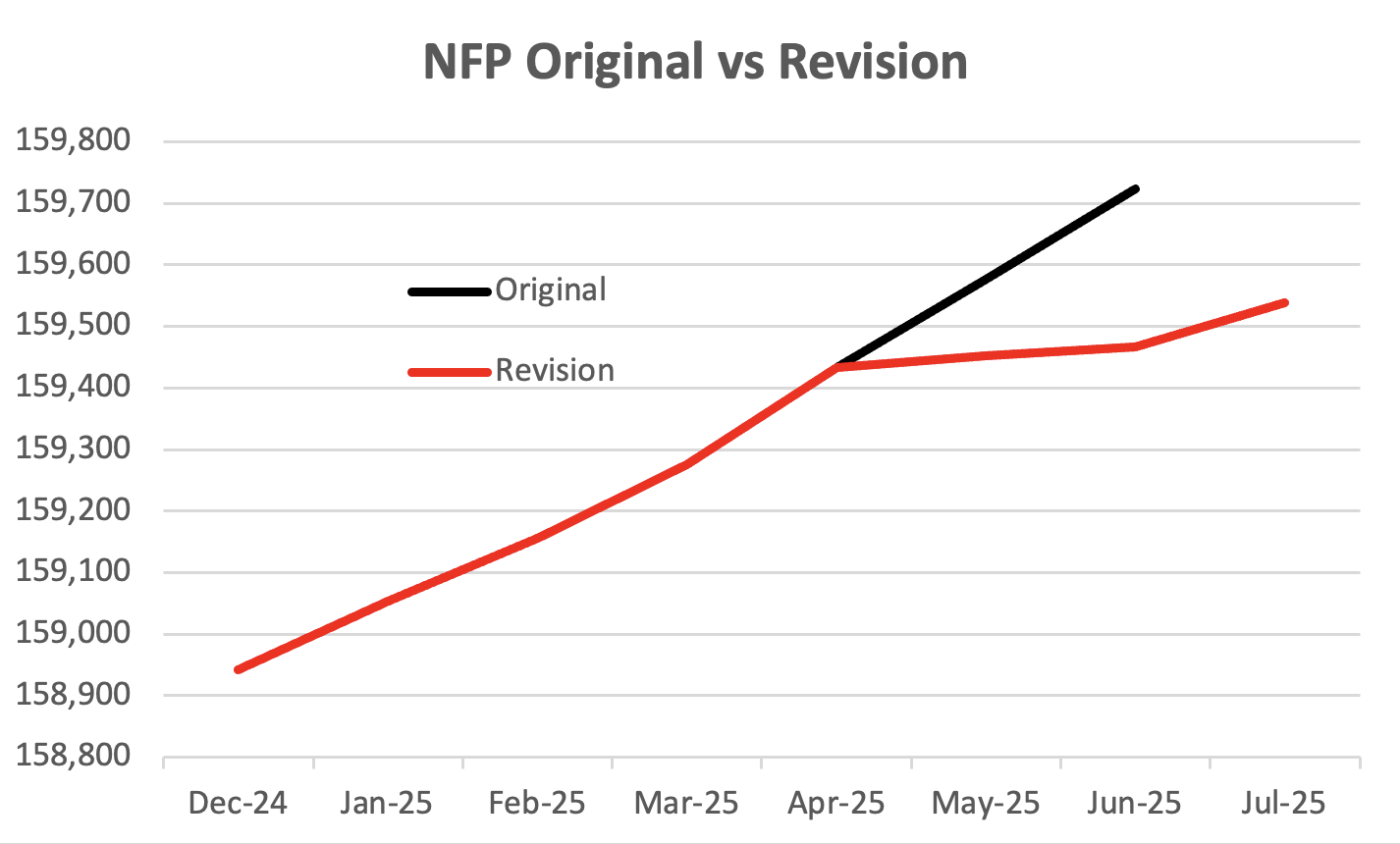

The stock market got a big shock on Friday when the Labor Department said that only 73,000 new jobs were created last month. That was below expectations for a gain of 100,000 jobs, and as expectations go, that’s quite modest.

But what really hit Wall Street were the revisions to the old data. The numbers for May and June were revised lower by a combined 258,000. That means that the economy created only 19,000 jobs in May and 14,000 in June.

Here’s a look at the original jobs report compared with the revisions.

The unemployment rate increased by 0.1% to 4.2% for July. I like to look at the decimals, and the unemployment rate came very close to rounding up to 4.3%. We now have the highest unemployment rate since October 2021.

This was a very unusual jobs report. For example, health care and social assistance combined for 94% of the job growth.

The jobs report is the cause for a major change in outlook because these new numbers indicate that the jobs market isn’t nearly as strong as we thought. It was only last Wednesday that the Federal Reserve said in its policy statement that the “unemployment rate remains low, and labor market conditions remain solid.”

Maybe not.

The futures market responded immediately, and it looks like a September rate hike is back on the table. The odds of a Fed rate cut in September soared to 89%. Before the jobs report, the odds were around 40%. There’s even talk now of the Fed cutting by 1% before the end of the year.

The S&P 500 lost 1.60% on Friday. That was the biggest lost for the index since late May. During the month of July, Friday’s loss was more than double the next worst daily loss.

The quiet upwards market that we’ve been enjoying this summer may no longer be with us:

There were few signs of strength in the July jobs count, with gains coming primarily from health care, a sector that has continued to show strength in the post-Covid recovery. The group added 55,000 jobs, easily leading the way. Social assistance also contributed 18,000 jobs. The two sectors combined for some 94% of the job growth.

Retail added nearly 16,000 jobs and the financial sector was up 15,000.

However, federal government employment continued to decline, down 12,000 for the month and 84,000 since its January peak, before Elon Musk’s Department of Government Efficiency began paring down the jobs rolls. Professional and business services lost 14,000.

Is the economy slowing, or it coming to a crashing halt? We don’t have the data yet to say.

There were some good bits in the jobs report. For example, average hourly earnings rose by 0.3% last month which matched estimates. Over the past year, average hourly earnings are up 3.9%. That’s not bad, but I want to see it go higher. Over the last year, average hourly earnings increased by 3.9%.

The labor force participation rate edged down to 62.2% That’s the lowest since November 2022. The broader U-6 rate, which counts “discouraged workers,” rose to 7.9%.

President Trump was not happy with the jobs report, especially the revisions. He fired Erika McEntarfer, the head of the Bureau of Labor Statistics.

The president has demanded lower interest rates from the Fed, and he may soon get his wish. On top of that, Adriana Kugler just announced her retirement from the Federal Reserve Board. That gives the president an opportunity to appoint a new member.

Folks on Wall Street are now talking about the Fed lowering rates by 1% before the end of the year. If that’s correct, that would be a big boost for value and defensive stocks. I’ll give you an example. On Friday, as the market was falling, shares of American Water Works (AWK), one of our Buy List stocks, gained nearly 4%.

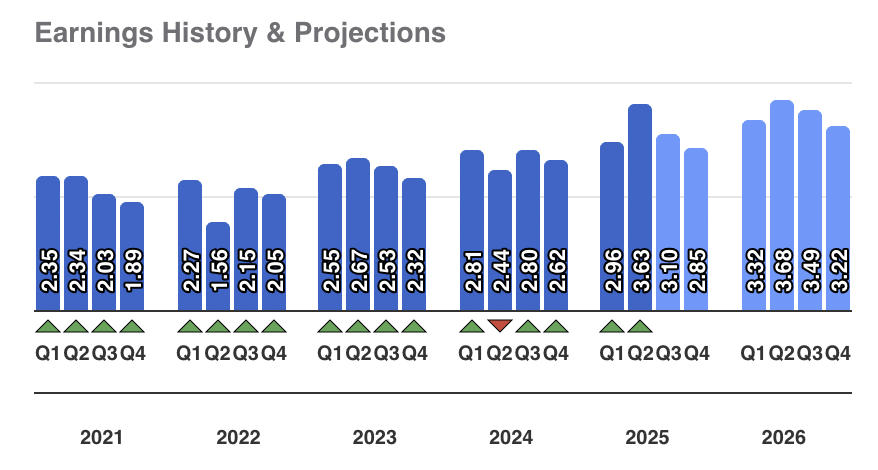

IDEXX Labs (IDXX) Soars 27% on Earnings Beat

In last week’s issue, I listed some stocks that I’m considering for next year’s Buy List. One of them, IDEXX Laboratories (IDXX), gave us a nice surprise on Monday. The company beat earnings, raised guidance and soared by more than 27% in Monday’s trading.

I wish I could take credit for predicting this, but I was as surprised by the big move as the market was. I merely said I was looking at the stock.

IDEXX is an interesting company, and it had a few industry segments. For example, IDEXX provides diagnostic solutions for pets. It also develops diagnostic tests to detect diseases in livestock and poultry. The company also does water testing so it can spot E. coli. IDEXX has more than 10,000 employees and it serves over 175 countries.

IDEXX mostly stays out of the headlines although it has faced anti-trust lawsuits. This is common among companies with strong positions in their market. IDEXX usually runs its gross margin near 60% and its operating margin around 30%. I also really like the recurring revenue model.

For its Q2, IDEXX had reported earnings of $3.63 per share. That was 33 cents per share better than Wall Street’s consensus, and 49% better than last year’s result. Quarterly sales rose 11% to $1.11 billion which beat estimates of $1.07 billion.

CEO Jay Mazelsky said, “We saw exceptional momentum with IDEXX InVue Dx™ placements, exceeding expectations as veterinarians adopted this slide-free technology to streamline workflows and gain faster, more accurate clinical insights. This growth builds on the successful launch of IDEXX Cancer Dx™ in North America. Our focus on helping veterinarians gain deeper diagnostic insights to inform patient care continues to drive customer loyalty and sets a solid foundation for sustained long-term growth.”

IDEXX raised its full-year guidance to a range of $12.40 to $12.76 per share. The previous guidance was $11.93 to $12.43 per share.

IDEXX also raised its 2025 sales guidance from the $4.10 billion to $4.21 billion range up to $4.21 billion to $4.28 billion.

I can’t say that IDEXX is a bargain at these prices, but it’s an innovative company that’s not well-known and it has very sound finances. Over the last 34 years, its total return has exceeded 67,000%.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: August 5, 2025

Posted by Eddy Elfenbein on August 5th, 2025 at 7:06 amRussia’s Secret War and the Plot to Kill a German CEO

White House Shouldn’t Let Putin Off the Hook Now

Israel’s Financial Markets Are Soaring Despite 22 Months of Brutal War

India Shifts to Damage Control After Trump Ratchets Up Threats

Swiss President Dashes to Washington in Attempt to Sway Trump

EU Continues to Press for Tariff Exemption on Wine, Spirits as Part of U.S. Deal

What’s the De Minimis Tariff Loophole and Why Is Trump Closing It?

Wall Street Bonus Pool to Grow as Stock Rally Defies Tariff Woes

Fed Voting Structure Raises the Bar for Trump’s Favored Rate

Trump’s Fed Pick Likely to Find Colleagues Cautious on Rate Cuts

Trump Says Bessent Doesn’t Want to Be Considered for Fed Chair

Trump Questions Discrimination Claims, Even One His First Administration Brought

Trump’s BLS Firing Tests Wall Street’s Reliance on Government Data

Real Strains Inside the BLS Made It Vulnerable to Trump’s Accusations

The Jobs Market Is Showing Signs of a ‘He-cession’

Earning More but in Worse Shape: Hardship Overwhelms Many American Families

Luckin’s Arrival In the U.S. Is Bad News For the Birthrate-Obsessed

Our President Is Economically Illiterate

Wharton’s ‘Collusion’ Paper Is Just How Markets Work

Global M&A Hits $2.6 Trillion Peak Year-to-Date, Boosted by AI and Quest for Growth

Norway’s Hedged Bet on Europe’s Energy Future: A Garbage Disposal for Emissions

In Battle to Save Sacred Land From Mining Giants, Apaches Hope for a Miracle

US Explores Location Trackers for AI Chips, Official Says

Taiwan Arrests Six in Probe of TSMC Chip Technology Leak

Palantir Surges on First $1 Billion Revenue Quarter

It’s Time for the DOJ to Declare Victory, Settle Google Lawsuits

On a YouTube Show, Making Machine Parts for Glory and $100,000

French Industry Gets Boost From Soaring Aviation Output

Harley-Davidson Names Topgolf Leader as New CEO

Pfizer Raises Profit View as Cost Cuts Offset Poor Sales Growth

Marriott Profit Beats Estimates, Fueled by International Hotels

Why Burgers Cost So Much Right Now

Yum Brands Earnings Miss Estimates as Pizza Hut, KFC Struggle in the U.S.

Molson Coors Cuts Outlook Again on Weak US Beer Demand, Tariffs

Be sure to follow me on Twitter.

-

Morning News: August 4, 2025

Posted by Eddy Elfenbein on August 4th, 2025 at 7:04 amTurkish Inflation Keeps Edging Down as Central Bank Primes More Rate Cuts

Swiss Inflation Edged Higher in July

Trump’s ‘Slap in the Face’ Puts Neutral Switzerland in Trade-War Crossfire

What’s It Like to Deal With Brutal U.S. Tariffs? Ask Malaysia.

Trump’s Trade War Targets Data as the New Enemy

The Stock Market Just Got a Sobering Reality Check

Wavering US Consumer and Job Market Show Risks to Economy

American Consumers Are Getting Thrifty Again

The Fed Was Right to Say No on Interest Rates

Trump Fired America’s Economic Data Collector. History Shows the Perils.

Trump Seeks Bigger Overhaul at Labor Statistics Bureau, Adviser Says

Job Description — Find Better Numbers, or Else

Why Mortgage Lenders Are Ignoring Trump’s Rollback on Home Appraisal Reviews

Dudley: The Fed’s Under Siege. It’ll Be Just Fine

Brokerages Retain September Rate Cut Bets After Soft Jobs Report

UBS to Pay $300 Million to Resolve US Mortgage Securities Cases

Jane Street India Trades Show Blurry Line Between Arbitrage and Market Manipulation

OPEC Plus Will Increase Oil Output

OPEC+ Supply Finale Teases a New Mystery for Oil Markets

China Is Choking Supply of Critical Minerals to Western Defense Companies

Boeing Defense Workers Go on Strike

Electric Air Taxi Company Plans to Acquire a Helicopter Business

Silicon Valley Enlists in the Business of War

Amphenol Strikes Big Broadband Deal in AI Boom

Is It Still Disney Magic If It’s AI?

The 20-Somethings Are Swarming San Francisco’s A.I. Boom

What Happens to AI Startups When Their Founders Jump Ship for Big Tech

Harley-Davidson Names Topgolf Leader as New CEO

For a Few CEOs, Pay Keeps Growing—by the Billions

Tesla Awards ‘Good Faith’ Shares to Musk Worth $29 Billion

Lilly’s Push to $1 Trillion Derailed by Trade Risks and Obesity Drug Speedbumps

The ‘Troublemaker’ Behind Netflix’s Biggest Gamble

Be sure to follow me on Twitter.

-

Morning News: August 1, 2025

Posted by Eddy Elfenbein on August 1st, 2025 at 7:03 amHow the US Weaponized Pakistan Against India

Eurozone Inflation Holds Steady at Target, Leaving ECB in ‘Good Place’

Asia Manufacturing Outlook Marks Five-Year Low as Tariff Concerns Linger

Trump Tariff Blitz Unleashes Delayed Shock to Global Economy

Trump’s Tariffs: Where He Started, What He Threatened, Where He Ended Up

Switzerland Is Stunned by 39% U.S. Tariff, Among the Highest in the World

Cambodia Agrees to a Reduced Tariff and Breathes a Sigh of Relief

In a Country Trump Says Nobody’s Heard Of, Tariffs Bring Chaos

Tariffs Land on Taiwan Amid Tension With Washington

With New 40% Tariff, Trump Takes Aim at U.S. Dependence on China’s Factories

Stocks Tumble as Investors Grapple With the Rising Cost of Trade

The Anti-US Axis Isn’t Dead, Just Resting

Ritholtz: Might Tariffs Get “Overturned”?

Harm or Help? Why Companies Are Battling Tariffs Meant to Benefit Them.

Mere Permanency In the Tax Code Will Encourage Economic Growth

Trump Urges Fed Board to ‘Assume Control’ If Rates Not Cut

For Trump’s Harvard Deal, $500 Million Is Only a Starting Point

The Sanctuary Cities Ruling Is a Win for States’ Rights

Bitcoin Pulls Back to Three-Week Low After Record-Breaking July

Bridgewater Founder Dalio Sells His Remaining Stake in Firm

AXA Shares Slide After Currency Fluctuations Bite

The Nimbleness of Corporate America Is on Full Display

How Trump Let $1 Trillion Worth of Imports Escape His Tariff Hammer

Exxon, Chevron Surpass Estimates With Record Oil Production

Where Human Labor Meets ‘Digital Labor’

A.I. Researchers Are Negotiating $250 Million Pay Packages. Just Like N.B.A. Stars.

Amazon Falls as Profit Outlook, Cloud Growth Spook Investors

What Microsoft’s $4 Trillion Market Value Really Means

Apple Surprises Investors Worried That It Had Lost Its Touch

L3Harris Partners With Air Taxi Maker Joby on Military Aircraft

Etsy Turns From TV Ads Toward Search, With AI as the Wild Card

Be sure to follow me on Twitter.

-

Morning News: July 31, 2025

Posted by Eddy Elfenbein on July 31st, 2025 at 7:06 amChina’s Small Workshops Are Hurting. Trump’s Tariffs Are Only One Reason.

China Official PMIs Signal Impending Slowdown

Bank of Japan Raises Price Forecasts, Fueling Rate-Hike Hopes

Eurozone Proves Robust as Joblessness Stays at Record Lows

French Inflation Stays Steady as ECB Holds Rates

Thailand and Cambodia Reach Trump Trade Deals, U.S. Official Says

Trump’s Tariff Authority Is Tested in Court as Deadline on Trade Deals Looms

Murky Pledges of Investment Cast Shadow on Trump’s Trade Deals

Countries Promise Trump to Buy U.S. Gas, and Leave the Details for Later

Trump Just Crashed the Copper Market

Wheat Holds Near May Low, Weighing Strong Dollar and US Exports

$30 Potatoes and $300 Flour in Gaza: Prices So High They’re ‘Meaningless’

When Does Capitalism Become Predatory?

One Way to Ease the US Debt Crisis? Productivity

A Worthless Number (GDP) Rises Not Due to Growth, But Because It’s Worthless

Powell Bucks Pressure, Dissents in Showing Resolve on Inflation

Trump’s Fight With the Fed Won’t End With Rate Cuts

How Podcast-Obsessed Tech Investors Made a New Media Industry

StanChart CEO Says ‘Shame on’ Big Banks Quitting Net Zero Group

The Condo Market Is Floundering: Four Charts That Explain the Downturn

Blackstone Is Not Making Housing More Expensive

China Summons Nvidia Over ‘Backdoor Security’ Risks of A.I. Chips

Meta Shares Soar as Ad Business Continues to Fuel AI Ambitions

Microsoft’s Cloud Unit, Bolstered by AI Demand, Supercharges Earnings

Coal-Powered AI Robots Are a Dirty Fantasy

How an ‘Entrepreneur of the Year’ Brought the First Big Bust to AI Boom

Texas Highways Have a New Nighttime Creature: Autonomous Trucks

Mercedes and Porsche Squeezed by U.S. Tariffs and Slowdown in China

Ford Is Latest Carmaker to Blame Tariffs for Profit Slump

Lilly’s Mounjaro as Effective on Heart-Attack Risk as Older Drug

AB InBev Shares Plunge as Sales Volumes Miss Forecasts

British American Tobacco Backs Guidance on Better-Than-Expected Earnings

Be sure to follow me on Twitter.

-

Morning News: July 30, 2025

Posted by Eddy Elfenbein on July 30th, 2025 at 7:13 amXi Ties His Legacy and China’s Economy to $167 Billion Dam

China Politburo Holds off on Further Stimulus

Singapore’s Central Bank Stands Pat as U.S. Tariffs Loom

Cooling Australian Inflation Locks In August Rate Cut

Eurozone Economy Shows Signs of Resilience Even as Tariffs Bite

Trump’s Trade Deals Come With Few Details to Flesh Out Big Numbers

World Bank Plans Securitization, Debt Swaps to Boost Development

Trump Keeps Pressuring the Fed to Cut Rates. Here’s Why Its Independence Matters

Fed to Avoid Clear Signal on Rate-Cut Timing

Fed Governors Could Break Ranks as Trump Intensifies Powell Pressure

S&P 500 Breaks Winning Streak After U.S.-China Meeting Ends Without a Deal

UBS Profit Beats Estimates as Ermotti Sees Brighter Outlook

HSBC Profit Tumbles as China Losses Mount

Conspiracy Theorists Found a New Boogeyman: Payroll Data

Harvard Created Windfall From Bringing Executives Back to School

Lina Khan: A Secret to Zohran Mamdani’s Success

Copper Market in Tumult Waiting for Details of Trump’s 50% Tariff

Even Nuclear Experts Are at a Loss Right Now

Top F.D.A. Official Resigns Under Pressure

Ozempic Maker’s Stock Plunges 20% After Profit Warning

Palo Alto Networks Nears Over $20 Billion Deal for Cybersecurity Firm CyberArk

Russia Builds a New Web Around Kremlin’s Handpicked Super App

TikTok Asks Users to Help Police Misinformation

America’s First Transcontinental Railroad Will Boost Our Supply Chain

How a Railroad Mega-Merger Years in the Making Came Together

Boeing Takes Slow Approach to Expansion

Mercedes and Porsche Squeezed by U.S. Tariffs and Slowdown in China

Adidas Shares Tumble After Sales Miss, Guidance Confirmation

How a Chinese Brand Reshaped Hong Kong’s Food Delivery Scene

Starbucks Abandons Mobile Order, Pickup-Only Stores

Kraft Heinz Raised Prices More Than Expected to Beat Estimates

Hershey Trims Profit Guidance on Tariffs, Higher Cocoa Costs

The New ‘Perfect Combination’: The Reese’s Oreo Cup? The Oreo Reese’s Cookie?

Be sure to follow me on Twitter.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His