-

Unemployment Claims Lowest Since the 1960s

Posted by Eddy Elfenbein on March 1st, 2018 at 12:00 pmThis morning the unemployment claims report came in at 210,000. This number tends to bounce around a lot so economists prefer to look at the four-week moving average. That number is down to 220,500 which is the lowest since December 27, 1969. For the raw number, it’s the lowest since December 6, 1969.

(Yeah, I know. I said lowest since the 1960s, but I’m technically right.)

We also learned that the ISM manufacturing index for February rose to 60.8. Expectations were for 58.6. That’s the highest since 2004.

I like the ISM report because it comes out on the first business day of the month. The day after the GDP report we get the personal income and spending report for the prior month. Since the GDP was revised yesterday, this morning we get personal income and spending for January. Personal income rose by 0.4% in January while spending increased by 0.2%.

-

Morning News: March 1, 2018

Posted by Eddy Elfenbein on March 1st, 2018 at 6:59 amWhy an Unpleasant Inflation Surprise Could Be Coming

Trump Expected to Announce Stiff Steel, Aluminum Tariffs

Powell Shoots for Soft Landing That’s Eluded Seasoned Fed Chiefs

Exxon Abandons Russian Projects Brokered by Tillerson

Walmart, Dick’s Say They Will Stop Selling Guns to Those Under 21

Lowe’s Update: After 25% Surge, Discount To Home Depot Narrowed Dramatically

Best Buy to Close Mobile-Phone Stores

Spotify Is Getting Paid to Save the Music Industry

World’s Biggest Ad Agency Suffers Worst Stock Drop Since 1999

Cryptocurrency Firms Targeted in SEC Probe

Is Bitcoin a Waste of Electricity, or Something Worse?

Bill Ackman Surrenders in His Five-Year War Against Herbalife

Cullen Roche: Tremors Was a Very Bad Movie

Roger Nusbaum: Game Planning Another Lost Decade

Ben Carlson: Questions For the Next Bear Market & The Closet Indexer

Be sure to follow me on Twitter.

-

The MOAT ETF

Posted by Eddy Elfenbein on February 28th, 2018 at 3:13 pmThere’s an ETF which focuses on competitive advantages, otherwise known as moats. The VanEck Vectors Morningstar Wide Moat ETF has the symbol MOAT.

I don’t own any shares in it but their strategy is close to what we do with our Buy List. MOAT currently has 44 stocks while we have just 25.

Here are the MOAT holdings as of January 31:

AMAZON AMZN

TWENTY-FIRST CENTURY FOX FOXA

LOWE’S LOW

EXPRESS SCRIPTS ESRX

AMERISOURCEBERGEN ABC

VEEVA SYSTEMS VEEV

SALESFORCE.COM CRM

EMERSON ELECTRIC EMR

UNITED TECHNOLOGIES UTX

VISA V

CARDINAL HEALTH CAH

VF VFC

BRISTOL-MYER SQB BMY

TRANSDIGM GROUP TDG

WELLS FARGO WFC

WALT DISNEY DIS

WESTERN UNION WU

L BRANDS INC LTD

PFIZER INC PFE

MONDELEZ INTERNATIONAL INC-A MDLZ

MONSANTO CO MON

MCKESSON CORP MCK

AMGEN INC AMGN

ZIMMER HOLDINGS INC ZMH

STARBUCKS CORP SBUX

MEDTRONIC PLC MDT

ELI LILLY & CO LLY

MERCK & CO. INC. MRK

STERICYCLE INC SRCL

COMPASS MINERALS INTERNATION CMP

BIOGEN IDEC INC BIIB

CVS CAREMARK COR CVS

ALLERGAN PLC AGN

GENERAL ELECTRIC CO GE

SCHWAB (CHARLES) SCHW

CBRE GROUP INC – A CBG

MICROSOFT CORP MSFT

GUIDEWIRE SOFTWARE INC GWRE

NIKE NKE

BANK OF NEW YORK MELLON BK

GILEAD SCIENCES GILD

WILEY (JOHN) & SONS JW-A

MICROCHIP TECHNOLOGY MCHP

POLARIS INDUSTRIES PII

AMERICAN EXPRESS AXP

PATTERSON PDCOI can’t say I like all these names, but I see several former Buy Listers here. It’s interesting how similar strategies can yield different names.

I couldn’t find a precise methodology for the fund. Judging what’s a long-lasting competitive advantage must involve some human guesswork.

-

Morning News: February 28, 2018

Posted by Eddy Elfenbein on February 28th, 2018 at 5:22 amStock Selloff Widens After Powell Boosts Expectations of Rate Rises

Senate Democrats Push for Support to Reinstate Net Neutrality

Amazon Acquires Ring, Maker of Video Doorbells

Papa John’s Is No Longer the NFL’s Official Pizza

Takata Airbag Scandal: Australia Recalls 2.3 Million Cars

Baidu’s Netflix-Style App Marks Bumper Year for China Tech IPOs

Comcast’s Roberts Has Anti-Murdoch Card to Play in Bid for Sky

Bill Gates Says Cryptocurrency is `A Rare Technology That Has Caused Deaths in a Fairly Direct Way’

Macy’s Just Confirmed the End of Department Stores as We Know Them

Weight Watchers Looking to Expand Beyond Dieting

How Defective Guns Became the Only Product That Can’t Be Recalled

In N.R.A. Fight, Delta Finds There Is No Neutral Ground

Cullen Roche: Here’s a (Not So) Pretty Picture – Buffett vs the S&P 500

Joshua Brown: Where the S&P 500 Will Spend Their Cash This Year

Michael Batnick: Why Doesn’t More Money Make Us Happy?

Be sure to follow me on Twitter.

-

Four Rate Hikes this Year

Posted by Eddy Elfenbein on February 27th, 2018 at 7:27 pmAccording to the futures market, the odds of the Fed raising interest rates four times this year is 33.5%. That’s up from 25% a week ago. In my opinion, it’s closer to 5%. Alas, I’m not on the FOMC.

I also wanted to mention that HEICO (HEI), a former Buy List all-star, reported earnings after today’s close. I like this stock a lot but I don’t like the price.

As usual, the earnings report was very good. Q1 sales rose 18% to $404.4 million, and EPS hit 45 cents per share. That’s five cents more than estimates. Last month, HEICO also split its stock 5-for-4.

HEICO is raising its full-year forecast. Before, they saw net sales and income rising by 10% to 12%. Now they see net sales rising by 12% to 14% and net income rising by 30% to 32%. That’s thanks to tax reform.

HEI is up 3.1% after hours. I would love to have HEICO back on the Buy List, but it’s way too pricey.

-

“A 40% Chance”

Posted by Eddy Elfenbein on February 27th, 2018 at 11:13 amRolfe Winkler and Justin Lahart have a biting piece in today’s WSJ on how market gurus go about making their claims non-falsifiable.

This is one of my pet peeves. You can see my Buy List all the time. My track record goes back more than a decade. Yet there are lots of famous market gurus who weasel their way out of one terrible call after another. Peter Schiff and Nouriel Roubini are prime examples.

Winkler and Lahart say that when in doubt, claim that your forecast had a 40% probability. That’s the sweet spot. If you’re right, you’re a genius. If you’re wrong, then you never said it was absolutely going to happen.

The nice thing about 40% is that you never have to say you were wrong, says Peter Tchir, a market strategist at Academy Securities. Say you predict the Dow Jones Industrial Average has a 40% chance of hitting 30000 before year-end.

“Get it right and you can say ‘See, I was telling everyone it could happen,’ ” he says. “Get it wrong and you can weasel your way out: ‘I didn’t say it was likely, I just said it was a strong possibility.’ ”

(…)

“Pundits and gurus master the art of going out on a limb without going out on limb,” says Philip Tetlock, a professor at the University of Pennsylvania who has made a career analyzing which people forecast well, and why. One of his pet peeves is how gurus use vague terms like “distinct possibility” instead of percentage odds when they describe probabilities. That makes it easy to wiggle out of, or take credit for a forecast, since it isn’t clear at all what a distinct possibility is.

But one drawback of percentage odds, Mr. Tetlock says, is that people are often unclear on what they actually mean.

(…)

Courageous contrarian calls are the best way forecasters capture the public’s attention, and get television time. New York University Professor Nouriel Roubini was dubbed “ Dr. Doom ” for correctly predicting the financial crisis. Then in 2010 he projected a 40% chance of a “double-dip recession” in the U.S. It didn’t happen.

Mr. Roubini says he doesn’t remember the projection, but that he takes pride in sticking his neck out, as with his latest call that Bitcoin is the biggest bubble in history and will go to zero.

“I would not rule out that I’ve committed the sin of the 40% rule,” said Prof. Roubini. “Everybody has done so.”

-

Powell Speaks and Durable Goods

Posted by Eddy Elfenbein on February 27th, 2018 at 11:01 amWe had two key economic reports this morning. The Case-Shiller Index said that home prices rose 6.3% in 2017. Also, orders for durable goods fell 3.7% compared with expectations of a 2% drop.

Orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, dropped 0.2 percent last month after declining 0.6 percent in December.

That was the first back-to-back drop in these so-called core capital goods orders since May 2016. Economists polled by Reuters had forecast these orders rising 0.5 percent last month. Orders increased 8.0 percent on a year-on-year basis.

Shipments of core capital goods edged up 0.1 percent after an upwardly revised 0.7 percent rise in December. Core capital goods shipments are used to calculate equipment spending in the government’s gross domestic product measurement. They were previously reported to have increased 0.4 percent in December.

We also learned this morning that consumer confidence hit a 17-year high.

Fed Chairman Jay Powell is testifying today on Capitol Hill. Here’s part of his testimony:

The U.S. economy grew at a solid pace over the second half of 2017 and into this year. Monthly job gains averaged 179,000 from July through December, and payrolls rose an additional 200,000 in January. This pace of job growth was sufficient to push the unemployment rate down to 4.1 percent, about 3/4 percentage point lower than a year earlier and the lowest level since December 2000. In addition, the labor force participation rate remained roughly unchanged, on net, as it has for the past several years–that is a sign of job market strength, given that retiring baby boomers are putting downward pressure on the participation rate. Strong job gains in recent years have led to widespread reductions in unemployment across the income spectrum and for all major demographic groups. For example, the unemployment rate for adults without a high school education has fallen from about 15 percent in 2009 to 5-1/2 percent in January of this year, while the jobless rate for those with a college degree has moved down from 5 percent to 2 percent over the same period. In addition, unemployment rates for African Americans and Hispanics are now at or below rates seen before the recession, although they are still significantly above the rate for whites. Wages have continued to grow moderately, with a modest acceleration in some measures, although the extent of the pickup likely has been damped in part by the weak pace of productivity growth in recent years.

Turning from the labor market to production, inflation-adjusted gross domestic product rose at an annual rate of about 3 percent in the second half of 2017, 1 percentage point faster than its pace in the first half of the year. Economic growth in the second half was led by solid gains in consumer spending, supported by rising household incomes and wealth, and upbeat sentiment. In addition, growth in business investment stepped up sharply last year, which should support higher productivity growth in time. The housing market has continued to improve slowly. Economic activity abroad also has been solid in recent quarters, and the associated strengthening in the demand for U.S. exports has provided considerable support to our manufacturing industry.

Against this backdrop of solid growth and a strong labor market, inflation has been low and stable. In fact, inflation has continued to run below the 2 percent rate that the FOMC judges to be most consistent over the longer run with our congressional mandate. Overall consumer prices, as measured by the price index for personal consumption expenditures (PCE), increased 1.7 percent in the 12 months ending in December, about the same as in 2016. The core PCE price index, which excludes the prices of energy and food items and is a better indicator of future inflation, rose 1.5 percent over the same period, somewhat less than in the previous year. We continue to view some of the shortfall in inflation last year as likely reflecting transitory influences that we do not expect will repeat; consistent with this view, the monthly readings were a little higher toward the end of the year than in earlier months.

After easing substantially during 2017, financial conditions in the United States have reversed some of that easing. At this point, we do not see these developments as weighing heavily on the outlook for economic activity, the labor market, and inflation. Indeed, the economic outlook remains strong. The robust job market should continue to support growth in household incomes and consumer spending, solid economic growth among our trading partners should lead to further gains in U.S. exports, and upbeat business sentiment and strong sales growth will likely continue to boost business investment. Moreover, fiscal policy is becoming more stimulative. In this environment, we anticipate that inflation on a 12-month basis will move up this year and stabilize around the FOMC’s 2 percent objective over the medium term. Wages should increase at a faster pace as well. The Committee views the near-term risks to the economic outlook as roughly balanced but will continue to monitor inflation developments closely.

-

Morning News: February 27, 2018

Posted by Eddy Elfenbein on February 27th, 2018 at 7:05 amDalio Says Central Banks Face Challenge After ‘Goldilocks’ Phase

After Anbang Takeover, China’s Deal Money, Already Ebbing, Could Slow Further

German Court Rules Cities Can Ban Vehicles to Tackle Air Pollution

In a Blow to AT&T, Federal Judges Have Rejected ‘The Loophole That Could’ve Swallowed the Internet’

5 Key Questions for New Fed Chair Powell That Will Be Crucial for Stocks

California Scraps Safety Driver Rules for Self-Driving Cars

Comcast Just Bid $31 Billion to Buy Sky Out From Under Rupert Murdoch and Fox

This Big Cryptocurrency Acquisition Could Create a Wall Street-Style Financial Giant

Qualcomm, Broadcom Drama Enters New Act

Sam’s Club Jumps Into Same-Day Grocery Delivery With Instacart’s Help

Howard Lindzon: The Market Does Not Care

Roger Nusbaum: Did Dennis Gartman Really Get Blown Up? & Hedging; Are You Doing It Wrong?

Be sure to follow me on Twitter.

-

Morning News: February 26, 2018

Posted by Eddy Elfenbein on February 26th, 2018 at 7:06 amLower Oil Prices Force Saudis to Widen Their Circle of Friends

How Today’s Big Supreme Court Case on Public-Sector Unions Could Lead to a Fiscal Crisis

New Fed Chairman Jerome Powell to Testify Before Congress on Capitol Hill

Supreme Court to Hear Microsoft Case on Emails, Customer Data Stored Overseas

Bitcoin Regulation: 5 Facts the SEC Wants You to Know

Warren Buffett: The New GOP Tax Law Benefits Berkshire and Acts as A ‘Huge Tailwind for Businesses’

Goldman Says Stocks May Dive 25% If 10-Year Yield Hits 4.5%

Morgan Stanley Takes on Goldman, Buffett With Bullish Bond Call

How PNB Says It Fell Victim to India’s Biggest Loan Fraud

Chairman of China’s Geely Has 9.7% Stake in Daimler

Why Companies Are Abandoning the NRA

Tortuous Sale Saga to End with Weinstein Company Bankruptcy

Joshua Brown: Rates, REITs and Utes

Michael Batnick: Risk & These Are the Goods

Cullen Roche: WealthFront’s Risk Parity Fund is a Raw Deal & Buffett’s Annual Letter – Some Key Takeaways

Be sure to follow me on Twitter.

-

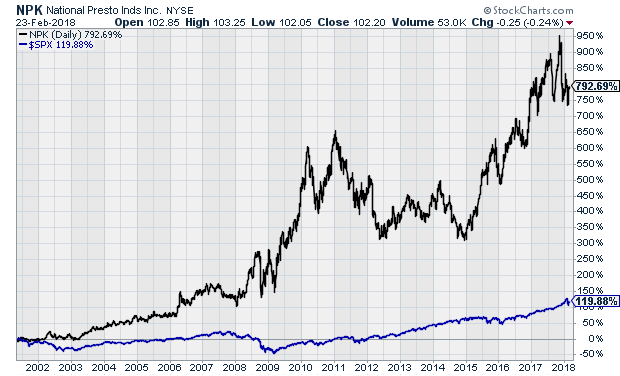

National Presto

Posted by Eddy Elfenbein on February 25th, 2018 at 1:16 pmCheck out the 17-year chart of National Presto (NPK):

This is another great stock with zero analyst coverage. Also, there’s also not much media coverage. I found a Forbes article from 2009. The firm has a rather interesting history:

Presto started life in 1905 as Northwestern Steel & Iron Works, maker of 50-gallon commercial canners. Ten years later it moved into home canning and in 1939 introduced the first saucepan-style pressure cookers. World War II rationing of aluminum had it cranking out munitions. In 1944 Maryjo’s dad, Melvin S. Cohen, joined as a customer service manager; two years later he married the daughter of a large shareholder and soon shot up the ranks.

In 1960 Melvin became president just as conglomerators like Harold Geneen and James Ling were gaining admiration. He scooped up nine companies, including a door-to-door vitamin seller, a pipeline operator, a press-and-lathe refurbisher and a trucking business. Melvin’s appetite was matched by his eye for bargains. He earned praise from Benjamin Graham, who touted Presto in his value-investing bible, The Intelligent Investor.

When leveraged-buyout firms started bidding prices up in 1980s, Melvin put away his wallet and started selling. By the time Maryjo took the corner office in 1993 he had unloaded everything but the kitchen appliance business. By 1999, with the world awash in cheap money, Presto’s cash and securities came to 80% of its assets. The stock was as flat as a pancake on a Presto Tilt ‘n Drain Big Griddle.

Then things got ugly. A study by the New York Society of Security Analysts in 1999 blasted Presto for inept management. FORBES called the Cohen family rule a “farce.” Melvin took out an ad in Inventor’s Digest requesting ideas for new products into which he could pour some cash–565 came back, all rejected. In 2002 the Securities & Exchange Commission demanded that Presto register as a mutual fund company. When Melvin refused, the agency sued in federal court for violation of the Investment Company Act and won (though it lost on appeal).

Shareholders’ salvation: two stock market crashes and a menu of suddenly cheap assets that could balance out Presto’s kitchen appliance unit, which not surprisingly had to send production work abroad in order to stay competitive. After exiting the munitions business in 1992, Presto got back into it in early 2001 with the $5.6 million purchase of Amtec, maker of 40mm bullets for mk19 machines guns now used in Iraq and Afghanistan.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His