-

CPI and Retail Sales Knock the Market

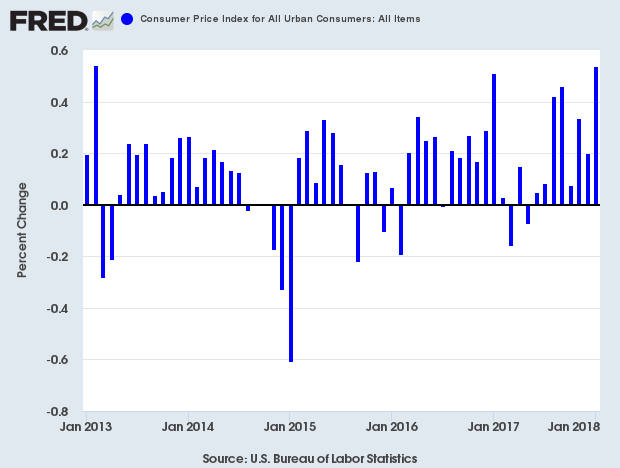

Posted by Eddy Elfenbein on February 14th, 2018 at 8:50 amWall Street had been nervous going into this morning because today brought the CPI report for January and the retail sales report.

As it turned out, both were bad. The Dow futures lost 500 points in the blink of an eye. The dollar surged and Treasury yields dropped.

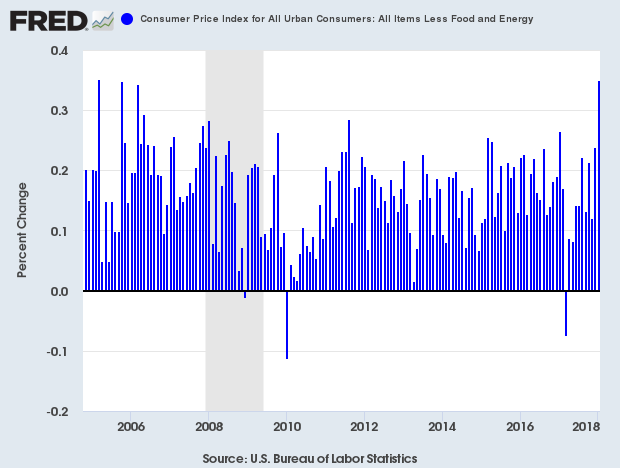

Consumer prices rose 0.5% last month while the core rate was up 0.3%. Both numbers were 0.1% higher than expectations.

The WSJ:

The increase in inflation last month was largely driven by higher prices for gasoline, shelter costs like rent, medical care, food and apparel.

Wednesday’s report showed wage inflation was broadly muted. Real average weekly earnings fell a seasonally adjusted 0.8% in January and were up 0.4% from January 2017.

The report showed overall inflationary pressures are intensifying, and it comes five weeks before Federal Reserve officials’ next scheduled policy meeting in Washington on March 20-21.

Central bank officials have been monitoring the inflation picture closely, looking for signs that a tightening labor market and continued economic growth are generating stronger wage and price increases after years of weak inflation.

This was the highest monthly headline inflation in five years.

The Japanese yen is at an 18-month high:

This was the highest core inflation report in close to 13 years.

Retail sales fell 0.3% last month. That was the biggest drop in 11 months.

The Commerce Department said on Wednesday that retail sales decreased 0.3 percent last month, the largest decline since February 2017. Data for December was revised to show sales unchanged instead of rising 0.4 percent as previously reported.

Economists polled by Reuters had forecast retail sales climbing 0.2 percent in January. Retail sales in January rose 3.6 percent from a year ago.

Excluding automobiles, gasoline, building materials and food services, retail sales were unchanged last month after a downwardly revised 0.2 percent drop in December. These so-called core retail sales correspond most closely with the consumer spending component of gross domestic product.

-

Morning News: February 14, 2018

Posted by Eddy Elfenbein on February 14th, 2018 at 7:08 amCash is King No More in German as Cards Gain Ground

Billions in VIX-Rigging Profits? Bruised Index Takes New Hit

New Hedge-Fund Tax Dodge Triggers Wild Rush Back Into Delaware

IRS Issues Urgent Warning On New Tax Refund Scam – And It’s Not What You’d Expect

Six Top US Intelligence Chiefs Caution Against Buying Huawei Phones

AT&T Is Said to Seek Antitrust Chief as Witness, NYT Reports

Chipotle Turns to Taco Bell’s ‘Doritos Locos’ Chief as New CEO

Credit Suisse Trims Loss, Cites Upside of US Tax Reform

Sam’s Club Makes E-Commerce Push With Amazon Prime Competitor

Blankfein Says Marcus Will ‘Move the Needle’ in Coming Years

Under Armour Struggles to Turn the Page

Uber Posts $1.1 Billion Fourth-Quarter Loss as Revenue Rises to $2.2 Billion

Michael Batnick: A Worthwhile Timesuck

Ben Carlson: The New Permanent Portfolio for Millennials

Be sure to follow me on Twitter.

-

AFLAC Is Splitting 2-for-1

Posted by Eddy Elfenbein on February 13th, 2018 at 4:20 pmAflac Incorporated (NYSE: AFL) announced today that its Board of Directors has declared a two-for-one stock split of the company’s common stock in the form of a 100% stock dividend payable on March 16, 2018 to shareholders of record as of the close of business on March 2, 2018.

Commenting on the announcement, Aflac Incorporated Chairman and Chief Executive Officer Daniel P. Amos said: “I am pleased with the Board’s action to split Aflac Incorporated’s stock. As you’ll recall, this follows a year of strong share price performance and is on top of our announcement of the Board’s action to approve an increase in the first quarter cash dividend of 15.6%. This is the ninth split of the company’s common stock since listing on the NYSE in 1974 and the first in 17 years. This split enhances the liquidity of our shares, which is in addition to our efforts to increase shareholder value.”

-

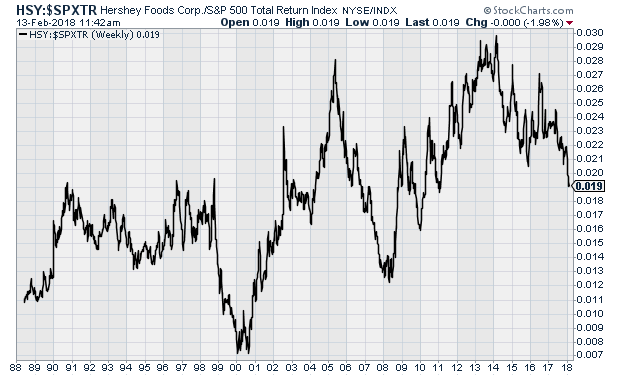

Hershey Looks Good Here

Posted by Eddy Elfenbein on February 13th, 2018 at 11:46 amOne of the signs that we’re late in a stock cycle is that defensive stocks start to underperform the market. This makes perfect sense.

You can really see the effect by looking at a long-term chart of Hershey (HSY), a classic defensive stock. This is Hershey’s share price divided by the S&P 500 Total Return Index.

You can see that HSY has been a very good long-term winner. You can also see how the shares badly lagged in 1999-2000 and again in 2007-08. They’re doing so again. HSY has underperformed for four years, and it recently touched a seven-year low for relative strength.

Of course, that’s not the only analysis required, but it’s a good starting point. HSY is going for 17.2 times next year’s earnings and the stock’s yield is up to 2.6%.

-

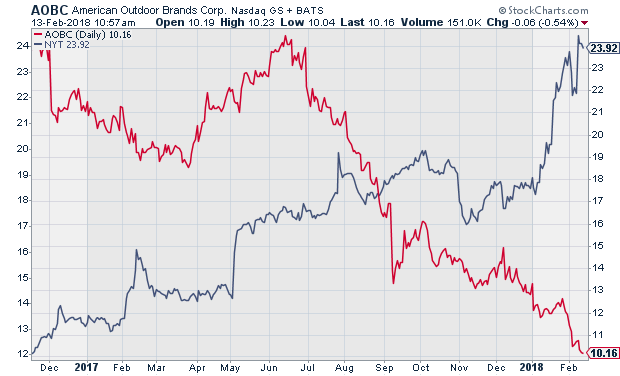

NYT vs AOBC

Posted by Eddy Elfenbein on February 13th, 2018 at 11:00 amHere’s an interesting stock chart. This shows the price of the New York Times (in blue) along with American Outdoor Brands (in red). That’s the new name for Smith & Wesson.

What gun stocks are for Democratic presidents, large media stocks are for Republican presidents.

-

Morning News: February 13, 2018

Posted by Eddy Elfenbein on February 13th, 2018 at 7:07 amFacebook Broke German Privacy Laws, Court Rules

U.S. CPI Report Takes on Bigger Importance After Markets Plunge

Trump’s Infrastructure Plan Puts Burden on State and Private Money

Treasury Yields Will Climb to 3.5% on Fed, Goldman Sachs Asset Management Says

5G Is Making Its Global Debut at Olympics, and It’s Wicked Fast

PepsiCo Leans More Heavily on Snacks as Beverages Fizzle

What Is AmerisourceBergen and Why Does Walgreens Want to Buy It?

Carl Icahn and Darwin Deason are trying to stop the Xerox Fujifilm deal

YouTube Revamped Its Ad System. AT&T Still Hasn’t Returned.

Remington Is Planning to File for Bankruptcy

Barnes & Noble Is Laying Off Workers Amid Declining Sales

Harley CEO Asks Investors for Patience as Sales, Stock Slide

Roger Nusbaum: Volatility Is Back In Town And It’s Angry

Joshua Brown: Larry Bonds & Passive My A**

Jeff Carter: Betting On Same Horse, Different Race

Be sure to follow me on Twitter.

-

Some Market Stats

Posted by Eddy Elfenbein on February 12th, 2018 at 1:59 pmThe market is having nice rebound today. The Dow is currently up 500 points. Measuring from Friday’s low, it’s up 1,350 points.

Here are several great stats from this Bloomberg article. Normally, I would use blockquotes, but there are so many good nuggets here:

Even after the rout, the math shows the S&P 500 remains less attractive than it has been 82 percent of the time since the index bottomed in 2009 when compared with yields on U.S. Treasuries.

Currently, the S&P 500’s earnings yield is around 6 percent, 3.1 percentage points more than the 10-year note. The post-crisis average has been 4 points.

So far, the S&P 500 has tumbled in seven of the 10 past days, and plunged into a correction (loosely defined as a 10 percent drop) faster than any time since 1950. In doing so, the index has blown through three round-number milestones, as well as technical support levels indicated by its 50-, 100- and (briefly) 200-day moving averages.

At 16.8 times forecast earnings, the S&P 500’s valuation multiple is now down from a high of 20 in late December. That’s one of the fastest declines since 2009, but it has yet to bring P/Es in line with the average ratio of 15.5 that marked the bottom of the last two corrections. To get there, the S&P 500 would have to fall to 2,417. That’s roughly 8 percent below Friday’s closing level.

Stocks still look cheap to Treasuries when viewed from a wider lens. The current yield spread is more than double the average since 1990 and compares with 2.66 percentage points since 2000. But a rise in 10-year yields to just 3.65 percent (from about 2.85 percent now) would reduce the equity advantage to the 20-year average.

The S&P 500 would have to fall to 2,417 for the P/E Ratio to reach 15.5, which marked the low of the last two corrections.

And this from MarketWatch:

“There have been 16 drawdowns of 10%+ since 1976. Of the 16 corrections, only five occurred around a recession,” Goldman wrote. “Of the remaining 11 non-recession episodes, 1987 was the only one that turned into a bear market.”

During the three months following past corrections, materials have beaten the S&P 500 by a median of 270 basis points. Industrials beat the index in 73% of the periods at a 270-basis point median. Telecom is the worst pick post-correction, lagging the S&P 500 in 64% of periods by a median of 410 basis points, Goldman found.

Low valuation and small-cap stocks historically perform best following a 10% decline, Goldman noted, with its valuation factor handing over a return 63% of the time at 350 basis points on average. Additionally, high volatility beats low volatility in a post-correction environment: low volatility lagged high volatility by 610 basis points on average in 87% of post-correction periods.

-

Morning News: February 12, 2018

Posted by Eddy Elfenbein on February 12th, 2018 at 7:11 amThe Fed is Officially in a Nailbiting Showdown With Wall Street

Mulvaney Says CFPB Under His Direction Is ‘Not Being Aggressive’

Record $23 Billion Flees World’s Largest ETF

Bitcoin Closes in on $9,000 as Regulatory Fears Peter Out

General Dynamics Buying CSRA for $6.8 Billion

Ford Revs Up Large SUV Production to Boost Margins, Challenge GM

Barclays Bank Unit Charged by SFO Over 2008 Qatar Loan Deal

Instacart Adds $200 Million to Defend Against Amazon Delivery

Unilever Threatens Online Ad Cuts to Clean Up Internet

After Settling With Uber, Waymo Faces Bigger Challenges

With Qualcomm in Play, San Diego Fears Losing `Our Flag’

Howard Lindzon: The Shift to Decentralization

Michael Batnick: An Unprecedented Decline

Ben Carlson: Some Random Observations On The Market Correction

Be sure to follow me on Twitter.

-

The S&P 500 Lost 5.16% this Week

Posted by Eddy Elfenbein on February 9th, 2018 at 6:19 pm

The week has come to an end. The S&P 500 gained 1.49% today. This was the second-best day for the index since the election. That fact seems odd because this week was so dramatic. The Dow was down 500 points today and then it was up 500 points.

For the year, the S&P 500 is down 2% which is very much in the normal range for six weeks in.

The relative performance of our Buy List has been very good this week. That’s always odd to say—the message is that we’re doing less awfully. Still, it reflects the fact that we have high-quality stocks and those don’t fall as hard in down markets.

At noon today, we were far ahead of the market, but our lead sagged as stocks recovered in the afternoon. For the week, the S&P 500 fell 5.16% while our Buy List lost 3.84%.

-

Moody’s Earned $1.51 per Share

Posted by Eddy Elfenbein on February 9th, 2018 at 9:48 amI expected Moody’s (MCO) to beat earnings and I was right. This morning, the credit ratings agency reported Q4 earnings of $1.51 per share. That was six cents better than estimates. Moody’s had quarterly revenue of $1.17 billion which topped expectations of $1.08 billion.

For the year, Moody’s made $6.07 per share which is a nice increase over the $4.94 they made in 2016. For 2018, Moody’s expects earnings to range between $7.65 and $7.85 per share. Wall Street had been expecting $6.89 per share.

This from the press release:

Moody’s expects full year 2018 revenue to increase in the low-double-digit percent range. Operating expenses are also expected to increase in the low-double-digit percent range.

Moody’s projects an operating margin of 43% to 44% and an adjusted operating margin of approximately 48%.

The effective tax rate is expected to be 22% to 23%.

Full year 2018 diluted EPS is expected to be $7.20 to $7.40. The Company expects full year 2018 adjusted diluted EPS to be $7.65 to $7.85. Both ranges include an approximate $0.65 benefit resulting from U.S. tax reform, as well as an estimated $0.20 benefit related to the tax accounting for equity compensation, in line with the benefit recognized in 2017. The majority of the latter benefit is expected to be recognized in the first quarter of 2018.

Like the rest of the market, shares of MCO had an eventful day. At its high, the stock was up more than 4% on the day, and two hours later, it was down nearly 2%. By the closing bell, Moody’s stood at $154.64 per share for a gain of 1.6%.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His