-

CWS Market Review – January 26, 2018

Posted by Eddy Elfenbein on January 26th, 2018 at 7:08 am“Nobody ever lost money taking a profit.” – Bernard Baruch

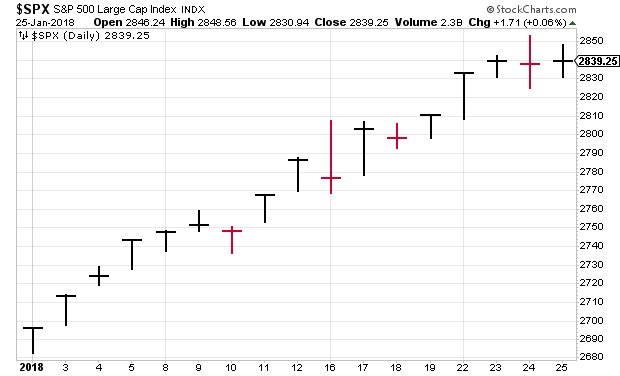

How good is this market? Consider than in 17 trading days this year, the S&P 500 has fallen just four times. Our fifth-worst day this year was a gain! On Thursday, the S&P 500 closed at another record high. The index is already up over 6% this year.

The Dow Jones Industrial Average also closed at a record high. The index is less than 200 points away from being 20,000 points above its March 2009 low. In less than nine years, the Dow nearly added 20,000 points.

I’m pleased to report that our Buy List is also doing well. Signature Bank, which gave us a great earnings report last week, is already up 13% this year. We have a total of four 10% gainers on the year, and the fifth one (Cognizant) is very close.

This week, we had two earnings reports. One was pretty good and the other was kinda blah. I’ll give you all the details. Plus, we have five more earnings reports next week. We also got a nice 15% dividend increase from Moody’s. Get ready, because earnings season is about to kick into high gear.

Earnings from Alliance Data and Sherwin-Williams

We had two Buy List earnings reports on Thursday morning. (Let me remind you that we have a Buy List earnings calendar.)

Alliance Data Systems (ADS) had a very strong fourth quarter. Revenue rose by 15% to $2.11 billion, and core EPS rose 34% to $6.26 per share. The recent tax-reform law boosted ADS’s Q4 bottom line by $1.02 per share. Even adjusting for that, Alliance’s results were still well above Wall Street’s consensus of $5 per share.

Also due to tax reform, Alliance raised its full-year guidance for 2018. Earlier, ADS said to expect full-year earnings of $21.50 per share. Now the company says core EPS should range between $22.50 and $23 per share. Alliance also boosted its quarterly dividend by 10% to 57 cents per share. That’s good to see.

Unfortunately, the stock lost about 2.6% in Thursday’s trading. That may be due to their lower revenue guidance. I’m not sure what the market is thinking, but I’m impressed by these results. I’m dropping my Buy Below on ADS down to $272. This is a good stock.

The numbers for Sherwin-Williams (SHW) are a little complicated due to the recent acquisition of Valspar. Not including that, Sherwin’s sales were up 6.9% last quarter. Adjusting for several items, the company made $2.95 per share for Q4 which was below Wall Street’s consensus of $3.12 per share.

Commenting on the financial results, John G. Morikis, Chairman, President and Chief Executive Officer, said “2017 was a year of record sales, net income, earnings per share, cash and EBITDA, but it will best be remembered as the year in which we joined forces with Valspar. The enormous amount of effort and energy invested over the past seven months in bringing these two great companies together, strengthening our customer relationships, defining the right organizational structure and building momentum in every line of business is transforming Sherwin-Williams into a faster-growing, financially stronger and more profitable enterprise. These efforts will continue throughout 2018 with similar effect.

I’m not too concerned by the earnings miss since the company is still adjusting to the big merger. For 2018, Sherwin-Williams expects earnings in the range of $16.05 to $16.45 per share. The shares lost about 1% in Thursday’s trading. I’m raising my Buy Below on Sherwin-Williams to $442 per share.

Five Upcoming Buy List Earnings Reports

Earnings season starts to heat up next week as five of our Buy List stocks are due to report. On Tuesday, January 30, Danaher and Stryker kick things off.

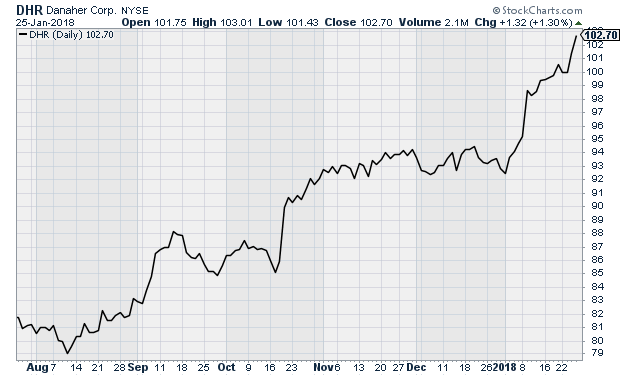

In October, Danaher (DHR) reported Q3 earnings of $1.00 per share. That beat Wall Street’s forecast by five cents per share. Previously, the company told us to expect Q3 earnings to range between 92 and 96 cents per share.

Back in July, Danaher raised its full-year guidance range to $3.85 to $3.95 per share. Before the last earnings report, I said “there’s a decent chance they’ll revise that higher next week,” and I was right. Danaher raised its full-year guidance to a range of $3.96 to $4.00. Working out the math, that means they expect $1.12 to $1.16 per share for Q4. Danaher’s CEO recently said he sees earnings coming in at the higher end of that range.

The stock recently broke $102 per share and touched yet another new high. In 1982, you could have picked up DHR for a nickel (adjusted for splits). Danaher now expects 2018 earnings to range between $4.25 and $4.35 per share.

In October, Stryker (SYK) reported Q3 earnings of $1.52 per share, two cents better than estimates. For Q4, they expect $1.92 to $1.97 per share. Stryker sees full-year earnings in the range of $6.45 to $6.50 per share. Forex costs will be about 10 cents per share for the year.

Stryker recently raised its quarterly dividend by 11%. The payout went from 42.5 to 47 cents per share. The orthopedics company has raised its dividend every year since 1993.

Remember when that nasty article knocked AFLAC (AFL) for a big loss? I told you not to worry. It’s two weeks later, and AFLAC has regained more than 70% of what it lost. The duck stock will report earnings on Wednesday, January 31. The CEO said that if the yen averages between 110 and 115 to the dollar, they expect Q4 earnings between $1.42 and $1.66 per share. Wall Street expects $1.55 per share. For 2018, they see operating earnings between $6.65 and $6.95 per share. That’s based on the yen averaging 112 to the dollar this year.

Shares of Check Point Software (CHKP) got clobbered when the last earnings report came out. The Q3 earnings were fine, but the outlook wasn’t so hot. In fact, it was the selloff that helped convince me to add CHKP to this year’s Buy List. For Q4, Check Point sees earnings between $1.45 and $1.55 per share and revenue between $485 million and $525 million. I’m not expecting a blowout report on Wednesday, but the long term looks very good for Check Point.

On Thursday, February 1, Ingredion (INGR) is set to report Q4 results. Three months ago, they had big earnings and raised guidance. Frankly, the company didn’t have a strong year in 2017, but it looks like things are improving. I was especially impressed to see them hike their dividend by 20% in September. INGR sees Q4 ranging between $1.67 and $1.82 per share. On Thursday, INGR reached a new 52-week high.

One more note: After the bell on Wednesday, Moody’s (MCO) announced a 16% dividend hike. The quarterly payout will rise from 38 to 44 cents per share. The dividend will be payable on March 12 to stockholders of record at the close of business on February 20.

And another thing. The Federal Reserve meets again next week. I’ll spare you my lengthy, penetrating and typically brilliant analysis and tell you—they ain’t changing rates. Not at this meeting. But there’s a very good chance they’ll hike rates in March. Rate hikes aren’t yet a threat to the economy, but we’re slowly moving closer.

That’s all for now. Next week will be a big one for investors. We’ll have lots more earnings reports, plus the Fed meeting. This is a two-day affair that begins on Tuesday. This meeting is also Janet Yellen’s finale. The policy statement will come out at 2 pm on Wednesday. We may get some clues as to what the central bank is thinking. Then on Friday, we’ll get the jobs report for January. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve recently teamed up with the folks at Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

3 Stocks to Sell Under Trump’s New Tax Law

It seems like most U.S. financial media cannot quit gushing about the new tax laws. The coverage is universally positive – I’m waiting to hear that the tax cut will cure the common cold.

However, the media ignores the fact that some companies will end up paying higher tax bills. All thanks to the provision in the law that limits deductions on interest payments.

The law limits deductions for interest payments to 30% of EBITDA earnings (earnings before interest, tax, depreciation and amortization) between 2018 and 2021. The restriction become even tighter from 2022 onward with deductions limited to 30% of earnings before interest and taxes.

This is a major negative for any companies with a heavy debt load.

As David Fann, CEO of the private equity advisory firm Torrey Cove Capital Partners LLC, told Reuters, “It [the new tax law] is a deviation from what has been allowed in the last 50 years. This is a radical change.”

The new restrictions on interest deductibility will mean that companies that have EBITDA less than double their interest payments will see “little or no benefit” from the tax reform package, according to Standard & Poor’s, the credit rating agency. And some firms will suffer under the new rules. S&P Global Ratings estimates that about 70% of companies whose debt amounts to more than five times EBITDA would be negatively affected by the interest deductibility cap.

Prime among the companies affected will be those shaped by private equity which loves to saddle companies with lots of debt. According to Moody’s around a third of all leveraged buyouts will be worse off under the new tax system.

3 Stocks for Real Blockchain Investors, Not Speculators

The latest buzzword on Wall Street is blockchain. There is a logic to the interest since the research firm Markets & Markets forecasts that the market for blockchain-related products and services will reach $7.7 billion in 2022. The market for such products was a mere $242 million in 2016.

That has led investors to jump on anything and everything even remotely connected to blockchain technology. That can be seen in the soaring stock prices for companies that have said they are “investing” into blockchain and therefore have added blockchain to their name.

I shouldn’t have to tell you this, but I will anyway… do not buy any of these companies – one of the biggest red flags you will ever see surrounding companies in the stock market is waving now! Instead, look at companies that have legitimate blockchain businesses. Or that at least are legitimately pursuing practical applications of blockchain technology.

For a hint about what companies you should be looking at, see what firms have either applied for, or have already received patents on blockchain technology. Not surprisingly (since blockchain can make transactions faster and more efficient), banks are among the leaders here.

-

Morning News: January 26, 2018

Posted by Eddy Elfenbein on January 26th, 2018 at 7:02 amBitcoin Is Dropping Again. This Time, Look to Japan

Solar Tariff Shapes Up As Speed Bump, Not Wall, For Development

Dell Technologies Considering IPO, Other Options

Qualcomm Signs $2 Billion Sales MOUs with Lenovo, Xiaomi, Vivo and OPPO

American, Southwest Post 4Q Profits; Airline Execs Seek To Calm Investors’ Fear Of A New Fare War

Walmart To Launch Online Grocery Delivery In Japan

A Kroger-Alibaba Deal Could Thwart Amazon’s Whole Foods Ambitions

‘Riots’ Break Out in France Over Supermarket Chain’s Nutella Promotion

Ackman’s Pershing Square Takes Stake in Nike

FDA Panel Rejects Philip Morris’s Claim That Tobacco Stick Is Safer Than Cigarettes

Howard Lindzon: Robinhood Goes Crypto

Joshua Brown: Bang! & Living That Coin Lyfe

Mark Hines: What Can Traders Learn From Poker AI?

Be sure to follow me on Twitter.

-

Earnings from Alliance Data and Sherwin-Williams

Posted by Eddy Elfenbein on January 25th, 2018 at 12:18 pmWe had two more earnings report this morning.

Alliance Data Systems (ADS) had a very strong fourth quarter. Revenue rose by 15% to $2.11 billion, and core EPS rose 34% to $6.26 per share. The recent tax reform law boosted Q4 by $1.02 per share. Even adjusting for that, Alliance’s results were well above Wall Street’s consensus of $5 per share.

The company also raised its full-year guidance for 2018. Earlier, ADS said to expect full-year earnings of $21.50 per share. Now they say core EPS should range between $22.50 and $23 per share. ADS also boosted its quarterly dividend by 10% to 57 cents per share.

The stock is down about 4% which may be due to lower revenue guidance. I’m not sure what the market is thinking but I’m impressed by these results.

The numbers for Sherwin-Williams (SHW) are a little complicated due to the recent acquisition of Valspar. Not including that, Sherwin’s sales were up 6.9% last quarter. Adjusting for several items, the company made $2.95 per share for Q4. That was below Wall Street’s consensus of $3.12 per share.

Commenting on the financial results, John G. Morikis, Chairman, President and Chief Executive Officer, said “2017 was a year of record sales, net income, earnings per share, cash and EBITDA, but it will best be remembered as the year in which we joined forces with Valspar. The enormous amount of effort and energy invested over the past seven months in bringing these two great companies together, strengthening our customer relationships, defining the right organizational structure and building momentum in every line of business is transforming Sherwin-Williams into a faster growing, financially stronger and more profitable enterprise. These efforts will continue throughout 2018 with similar effect.

I’m not too concerned by the earnings miss since the company is still adjusting to the big merger. For 2018, Sherwin-Williams expects earnings in the range of $16.05 to $16.45 per share. The shares are down about 0.5% in Thursday’s trading.

-

Morning News: January 25, 2018

Posted by Eddy Elfenbein on January 25th, 2018 at 7:05 amWhy Strong Growth Is a Headache for the European Central Bank

Trump Vs. China: Is A Trade War On The Way?

U.S. Efforts to Weaponize the Dollar Are Doomed to Fail

U.S. Heads for 3% Growth Trifecta on Spending, Investment Punch

The Dark Side of America’s Rise to Oil Superpower

Coal’s Decline Seems Impervious to Trump’s Promises

How U.S. Tariffs Will Hurt the Solar Industry

Under Trump Appointee, Consumer Protection Agency Seen Helping Payday Lenders

Ford Says It’s a New Era. Wall Street Isn’t Buying It.

Bank Of America Ends Free Checking Option, A Bastion For Low-Income Customers

GE Woes Deepen as SEC Investigation Throws Wrench in Turnaround

China’s Sinovel Convicted in U.S. of Stealing Trade Secrets

Ben Carlson: 10 Money Revelations in My 30s

Michael Batnick: What’s Wrong With Value?

Howard Lindzon: Meet Your New Ruler – Jack Ma

Be sure to follow me on Twitter.

-

Moody’s Raises Dividend by 16%

Posted by Eddy Elfenbein on January 24th, 2018 at 6:13 pmAfter the bell, Moody’s (MCO) announced a 16% dividend hike. The quarterly payout will rise from 38 to 44 cents per share. The dividend will be payable on March 12, 2018 to stockholders of record at the close of business on February 20, 2018.

-

Buy-and-Hold Is Pretty Darn Good

Posted by Eddy Elfenbein on January 24th, 2018 at 12:12 pmBuy-and-hold investing comes in for a lot of criticism, but I want to present a measured defense of it. Of course, what matters is what you’re after. Buy-and-hold isn’t perfect, and you’ll certainly experience some pain. But by staying in the market, your returns can be good enough.

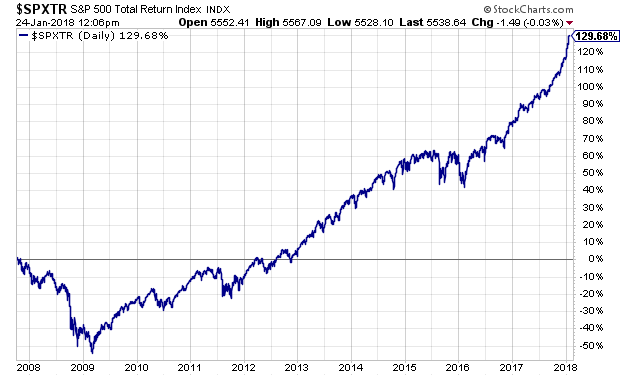

Let’s consider the fate of the world’s unluckiest investor — the person who went all in at the market’s 2007 peak. Within 18 months, they lost half their money. They didn’t even see a profit for nearly five years. (I’m using the S&P 500 Total Return Index.)

Now here we are, more than 11 years later and the S&P 500 Total Return Index is up about 130%. That’s every $1 becoming $2.30. That’s about 7.7% annualized. That’s something to keep in mind the next time you hear someone talk about how they “called the crisis.”

-

Jay Powell Confirmed as Next Fed Chair

Posted by Eddy Elfenbein on January 24th, 2018 at 11:36 amYesterday, the Senate voted to confirm Jay Powell as the 16th Chairman of the Federal Reserve. The vote was 84-13.

Powell, 64, has been a Fed governor for five years and helped shape policy under Janet Yellen, who will leave after a single term as the first woman to lead the world’s most influential central bank. Powell has said his leadership would represent continuity with his predecessors.

Since Powell was nominated by President Trump in November, progressive Democrats like Senator Elizabeth Warren of Massachusetts have raised concerns about whether he would be too aggressive in dialing back post-financial crisis reforms.

“I’m deeply concerned that as soon as Governor Powell unpacks his boxes in the Chairman’s office, he will begin weakening the new rules Congress and the Fed put in place after the 2008 financial crisis,” Warren said according to prepared remarks. “We need someone who believes in tougher rules for banks — not weaker ones. That person is not Governor Powell.”

Despite those objections, Powell easily won confirmation on Tuesday by a vote of 84-13 with strong bipartisan support. Nearly 40 Democrats — with Charles Schumer, Sherrod Brown and Ron Wyden among them — crossed the aisle to support him.

Janey Yellen’s term ends on February 3. Over the last 67 years, we’ve only had seven Fed chairs. Eisenhower, JFK and LBJ never appointed one.

Of the 13 no votes, I can’t help noticing that many of them seem to be senators who wouldn’t mind being president someday: Booker, Cruz, Gillibrand, Harris, Paul, Rubio, Sanders and Warren.

-

Morning News: January 24, 2018

Posted by Eddy Elfenbein on January 24th, 2018 at 7:03 amTrump Team at Davos Backs Weaker Dollar, Sharpens Trade War Talk

Blame Central Banks for the U.S. Dollar’s Dark Days

Senate Confirms Jerome H. Powell as Fed Chairman

CFPB Chief Mulvaney Says Days of ‘Pushing the Envelope’ Are Over

Trump’s Failing War on Green Power

Google Outspends Tech Rivals on Washington Lobbying in 2017

Qualcomm Gets $1.2 Billion EU Fine for Apple Chip Payments

GE Misses Fourth-Quarter Earnings Estimates as Power Sales Fall

Amazon’s AI-Infused Grocery Store Is Open: What Investors Need to Know

Disney to Give Employees $1,000 Bonuses in Wake of Tax Reform

JPMorgan Rolls Out $20 Billion Investment Plan After Tax Gains

About That Joint: Marijuana Startups Pass

Jeff Miller: Is This an Inflection Point for Both Stocks and the Economy?

Be sure to follow me on Twitter.

-

What if the Stock Market Were a Bond?

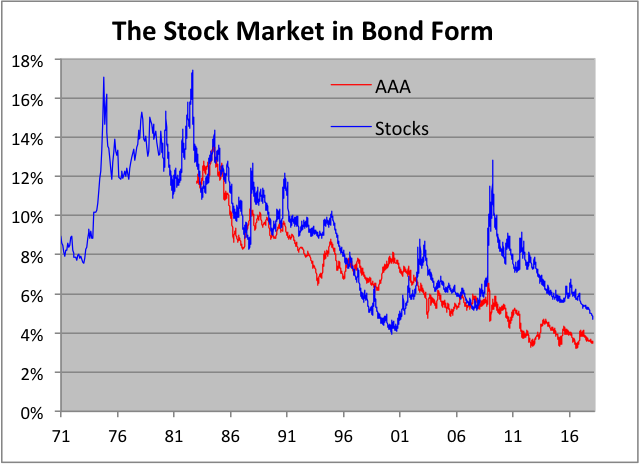

Posted by Eddy Elfenbein on January 23rd, 2018 at 10:03 amHere’s an update to one of my more off-the-wall ideas. I was curious to see what the historical performance of the stock market looks like, but in the form of a bond.

Crazy? Let me explain.

I took all of the historical market performance of the Wilshire 5000 (including dividends) and invented a hypothetical long-term bond that matched the market’s daily gains step-for-step.

I assumed that it’s a bond of infinite maturity and pays a fixed coupon.

There’s one hitch, though. I had to choose a starting yield-to-maturity for the beginning of the data series in December 1970. So this isn’t a completely kosher experiment because the starting point is based on my guess.

If I chose a number that’s too high, the historical performance wouldn’t be able to keep up and the yield-to-maturity would grow higher and higher and soon leave orbit. Conversely, if my starting YTM was too low, the yield would gradually get pushed down to microscopic levels.

Fortunately, the data made my job easy. After four decades, the window I had to work with is pretty narrow. Starting with 10% is too high and 8% is too low. After playing with the numbers, I finally settled on 8.93%.

Even though this “bond” is completely make-believe, it reflects what the actual stock market really did for the past 47 years. It’s the same old stock market but it’s expressed in the form of a bond. Through yesterday, the “bond’s” yield stood at 4.65%.

Here’s what the actual stock market looks like, expressed in the form of a bond. For comparison, I added Moody’s AAA Bond Index (in red). That series starts in 1983.

It’s been more than ten years since the red line was higher than the blue. This is why I often say that the math still favors stocks. When you hear people say that the stock market is expensive, you have to wonder “compared to what?” Lower bond yields are tough competition for stocks and that ought to raise valuations.

-

Morning News: January 23, 2018

Posted by Eddy Elfenbein on January 23rd, 2018 at 7:04 amSingapore Soars Up Innovation Rankings, U.S. Falls Out of Top 10

South Korea to Ban Cryptocurrency Traders From Using Anonymous Bank Accounts

Murdoch’s Fox Takeover of Sky Is Dealt a Blow by U.K. Regulators

U.S. Tariffs, Aimed at China and South Korea, to Hit Targets Worldwide

Montana Governor Signs Order to Force Net Neutrality

Netflix, Inc. Shrugs Off Price Increases to Grab 8.3 Million New Subscribers

Elon Musk’s Pay at Tesla Will Now Have Nothing to Do With Making Cars

Rupert Murdoch Wants Facebook to Pay for the News

Immunotherapy M&A In Focus as Celgene Buys Juno; Good, Bad of Activism

Amazon’s Pointless Obsession With Cashiers

Millennials Brought About the Downfall of One of America’s Most Iconic Beer Brands

Bacardi Moves To Buy Patrón Tequila, Valuing It At $5.1 Billion

Cullen Roche: Why Does Momentum Investing Work?

Ben Carlson: 180 Years of Stock Market Drawdowns

Roger Nusbaum: Isn’t ROC Supposed To Be A Bad Thing?

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His