-

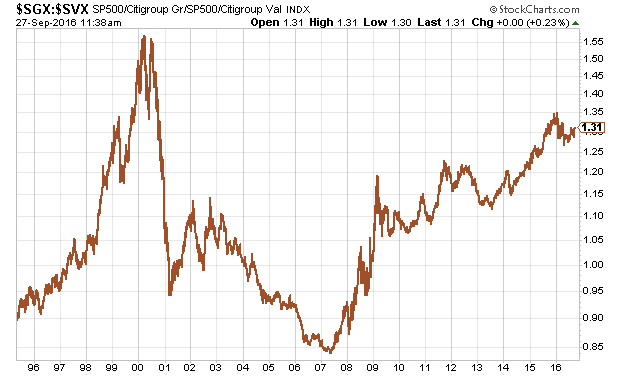

The Growth/Value Cycle

Posted by Eddy Elfenbein on September 27th, 2016 at 11:43 amEvery so often, I like to see where we are in the Growth/Value Cycle. Here’s a look at the S&P 500 Growth Index divided by the S&P 500 Value Index. As you can see, Growth has been leading Value for over nine years.

I expect Value to have its day, but I’m not about to declare a turning point. In fact, it may have already happened. Value has outperformed Value since January.

One issue for Value is that it’s been weighed down by many bank stocks. Despite their depressed valuations, banks have not done well as a group.

-

Consumer Humility Plunges

Posted by Eddy Elfenbein on September 27th, 2016 at 10:10 amThe Conference Board just reported that Consumer Confidence jumped up to its highest level since the recession.

The latest reading on consumer confidence from the Conference Board came in a 104.1 for September, up from the prior month’s 101.8.

Meanwhile, economists had forecast that the index dropped to 99.0 this month, according to the Bloomberg consensus.

“Consumers’ assessment of present-day conditions improved, primarily the result of a more positive view of the labor market,”said Lynn Franco, Director of Economic Indicators at The Conference Board.

“Looking ahead, consumers are more upbeat about the short-term employment outlook, but somewhat neutral about business conditions and income prospects. Overall, consumers continue to rate current conditions favorably and foresee moderate economic expansion in the months ahead.”

Earlier today, the Case-Shiller report said that home prices continue to rise. Taken together, these reports suggest to me that we’re still not near a recession.

-

FactSet Down 6% this Morning

Posted by Eddy Elfenbein on September 27th, 2016 at 9:53 amA former Buy List stock, FactSet Research Systems (FDS), is down about 6% this morning after their latest earnings report missed expectations by one penny per share. For their fiscal Q4, FactSet earned $1.69 per share.

The results missed Wall Street expectations. The average estimate of 11 analysts surveyed by Zacks Investment Research was for earnings of $1.70 per share.

The financial data firm posted revenue of $287.3 million in the period, which also missed Street forecasts. Six analysts surveyed by Zacks expected $290.9 million.

For the year, the company reported profit of $338.8 million, or $8.19 per share. Revenue was reported as $1.13 billion.

For the current quarter ending in December, FactSet expects its per-share earnings to range from $1.68 to $1.72.

Even with the reduced price, FDS is still going for 22 times next year’s estimate.

-

Morning News: September 27, 2016

Posted by Eddy Elfenbein on September 27th, 2016 at 7:12 amWTO Says Global Trade In Its Worst Year Since Financial Crisis

Saudis, Iran Dash Hopes for OPEC Oil Deal in Algeria

China Industrial Profits Rise Most in Three Years as Economy Shows Signs of Stabilizing

Russia Revises Ban on Imports of Egyptian Plant Products

Trump Slams Yellen’s Fed Again, This Time on a Much Bigger Stage

When Is A $160 Profit Just A $100 Profit? When You Include Taxes That You Don’t Pay

Deutsche Bank Is Too Big To Fail – Too Big To Fail Means It Will Not Fail

Wells Fargo Workers Claim Retaliation for Playing By The Rules

Facebook Ordered to Stop Collecting Data on WhatsApp Users in Germany

Drugmaker Pfizer Decides Not to Break Up Business

How Twitter Could Change Under the Umbrellas of Disney, Salesforce, or Google

American Express Can Stop Merchants From Steering Clients to Other Cards

Eight-Cent Eggs: Grocery Prices Are Plunging

Roger Nusbaum: What Did the BOJ Actually Do?

Josh Brown: Chart o’ the Day: A Dead Heat

Be sure to follow me on Twitter.

-

Earnings Look to Fall Again

Posted by Eddy Elfenbein on September 26th, 2016 at 9:19 amThe Q3 earnings seasons will start in a few days. Not too long ago, it looked like the S&P 500’s profit drought was set to end in Q3. That may be in doubt now. This could for the sixth quarter in a row of declining earnings for the S&P 500.

Many of the factors pressuring U.S. corporate earnings in recent quarters—including a stronger dollar and falling oil prices—have abated in 2016. The WSJ Dollar Index, which measures the U.S. dollar against a basket of 16 currencies, is down 4% this year, versus up 8.6% for all of last year, and the price of U.S.-traded crude oil has risen 20% in 2016, rebounding from its extreme lows.

Still, those moves haven’t been enough to project an end to the earnings recession.

The battered energy sector of the S&P 500 had the largest downward earnings revision for the third quarter. Exxon Mobil Corp., for instance, was expected to report 80 cents a share of earnings for the third quarter as of the end of June, but as of Friday that expectation had worsened to 66 cents a share.

Analysts are currently forecasting a 2.3% drop in earnings compared with one year ago. The Energy sector is expecting to drop by 66%. This would be Energy’s eighth drop in a row. If you were to exclude Energy, then earnings growth for the S&P 500 would have been positive for four of the last five quarters.

-

Morning News: September 26, 2016

Posted by Eddy Elfenbein on September 26th, 2016 at 7:13 amBank of Japan’s Kuroda Sees No Big Rise or Fall in Bond Buying For Now

UK CEOs Consider Pulling Up Stakes Because of Brexit

German Business Morale Shrugs Off Brexit to Hit 28-Month High

Turkish Lira, Markets Slump After Moody’s Cuts Rating to Junk Status

Protesters in Spain Jeer Ex-IMF Boss as Bank Card Trial Starts

Treasury Market’s Biggest Buyers Are Selling as Never Before

Germany Sees ‘No Grounds’ for Speculation Over Deutsche Bank Aid

The Banking Sales Culture Is Behind the Wells Fargo Scandal

Wenner to Sell 49% of Rolling Stone to Singapore’s BandLab

Chemtura Rises in Premarket on $2.5 Billion Buyout

Salesforce Weighs Twitter Bid to Spur Growth

Instant Lending Made This College Dropout a Billionaire

Howard Lindzon: Salesforce and Twitter?

Jeff Miller: Will Election News Change the Course of Markets?

Be sure to follow me on Twitter.

-

Today with Joe Weisenthal and Scarlet Fu

Posted by Eddy Elfenbein on September 23rd, 2016 at 10:59 pm -

CWS Market Review – September 23, 2016

Posted by Eddy Elfenbein on September 23rd, 2016 at 7:08 am“If being the biggest company was a guarantee of success, we’d all be using IBM computers and driving GM cars.” – James Surowiecki

On Wednesday, the Federal Reserve decided, yet again, to forego raising interest rates. This is what the market had expected, and more importantly, it’s what the market wanted. Stocks responded by rallying Wednesday afternoon, and the buying continued into Thursday. The S&P 500 is once again not far from a new all-time high.

However, the Fed hinted that higher rates are coming. In fact, I think there’s a very good chance that we’ll see a rate hike in December. Not everyone is pleased that rates are still so low. In this week’s policy statement, three members of the FOMC dissented. They want rates to go up right now.

What does this mean for us as investors? Continued low rates means that the stock market remains a good place to be. This week, we got a nice dividend increase from Microsoft. The software giant is also going to buy back $40 billion of its stock. Also on Wednesday, Bed Bath and Beyond released a blah blah and blah earnings report. The silver lining is that the stock rallied after management stuck by its full-year guidance. I’ll have all the details in a bit, but first, let’s look at what Fed did by not doing nothing.

The Fed Holds for Now, but May Raise in December

Let’s review the events leading up to this week’s Fed meeting.

On August 17, the Fed released the minutes from its July meeting. These minutes showed that the Fed was divided over the need for a rate hike. At the time, I said I was baffled that Wall Street took these minutes as a “dovish” sign. To me, it was clear that the Fed was leaning toward a rate hike. The only question was when. I wrote, “I think it’s possible that the Fed will raise rates in December or early next year.”

Then on August 26, Janet Yellen spoke at the Fed’s big conference in Jackson Hole. She conceded that the argument for higher rates was getting stronger, but she didn’t try to soothe the market’s nerves either. We often forget that the C in FOMC stands for committee, and that a Fed chair needs to build a consensus. At the time, I wrote, “I think the Fed is leaning towards raising rates, but they want more evidence that it’s safe to do so.”

After that, the data started talking. On September 1, the ISM report for August came in at just 49.4. Any reading below 50 means that the manufacturing sector is contracting. The next day was Jobs Day. The government said that the U.S. economy created 151,000 net new jobs in August, which was below forecasts.

If I had to guess, I’d say it was these two reports that tipped the balance inside the FOMC toward the dovish side. That is, for September, but not for the rest of the year.

On September 12, Fed Governor Lael Brainard spoke. This was the last speech before the Fed’s September meeting. Brainard has long been known to be a dove, and it was believed that if she had turned towards favoring a rate hike, then it was definitely on. Instead, Brainard gave a very dovish address.

One important part of her talk jumped out at me. She noted that the strong dollar had already acted as a rate increase on the economy. Of course, a strong dollar isn’t the same thing as a rate hike, but the economic effects can be nearly identical. She said that the 20% rise in the U.S. dollar from June 2014 to January 2016 could have been the equivalent of a 200-basis-point rate increase! That’s a remarkable statistic.

After Brainard’s speech, Goldman Sachs cut their odds of a rate hike from 40% to 25%. I still thought that was too high. Interestingly, at the same time, Goldman raised their odds of a December hike from 30% to 40%.

So it wasn’t much of a surprise for me to learn that the Fed passed on raising rates this week. The vote was 7-3. All three dissenting votes were from reserve bank presidents, as opposed to Fed governors. (Governors rarely dissent. The last one was eleven years ago.) We can assume that the “hike now” caucus is at three and growing. I would guess that Bill Dudley may become the next member.

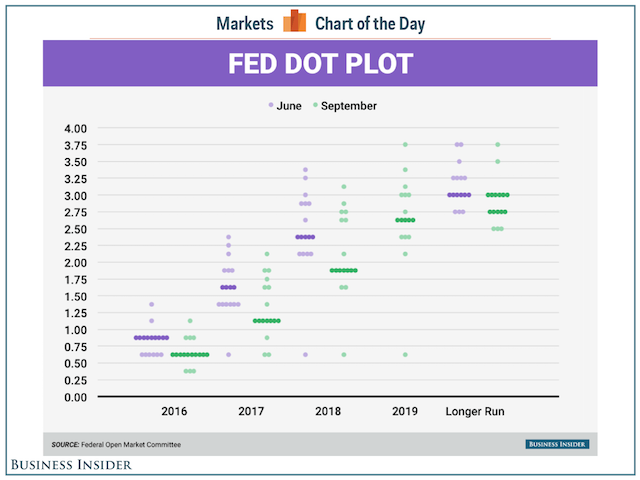

In the Fed’s economic projections, 14 of the 17 FOMC members (not everyone votes) said they expect rates to go up before the end of the year (the dots plots below). The median dot now expects one more rate hike this year, plus two more next year, three more in 2018 and another three in 2019. If that’s right, that would give the Fed funds a target range of 2.5% to 2.75% by the end of 2019.

The policy statement said, “The committee judges that the case for an increase in the federal funds rate has strengthened but decided, for the time being, to wait for further evidence.” Note that that’s nearly identical to what I said a few weeks ago.

There’s another Fed meeting in November. While Janet Yellen has stressed that all meetings are “live” meetings, it’s very doubtful they’ll raise in November. For one, it’s only a few days before the election. Also, it’s a one-day meeting. The December meeting is a two-day affair, and it will be followed by a Yellen press conference.

I want to stress to you how much the thinking inside the Fed has changed. Consider this. One year ago, the FOMC members thought interest rates would be at 3.4% by the end of 2018. Now, one year later, that forecast is down to 1.9%. So if they’re going to start raising rates soon, they don’t expect to be doing it for very long.

The immediate effect of low rates is that it helps the stock market. Nearly half the stocks in the S&P 500 yield more than 2%. Compare that with a two-year Treasury, which gets you 0.77%. Don’t mistake that for a prediction that stocks will go up; it’s looking at the numbers and realizing that a balanced portfolio of high-quality is the smart play. Now let’s look at some recent news from our Buy List stocks.

John Stumpf Heads to Capitol Hill

This week, Wells Fargo (WFC) CEO John Stumpf headed to Capitol Hill to testify at hearings regarding the massive fraud committed by the bank. It was tough to watch. The senators, of course, love to grandstand—it’s what they do—but Stumpf’s leadership thoroughly earned this grilling. Boy was he grilled.

When Stumpf should have been more apologetic, he turned legalistic. I understand the approach, but he needed to make it clear that the bank was sorry and had learned its lesson. Moreover, Wells needs to show how it’s working to regain the public’s trust. Senator Elizabeth Warren called him “gutless.” That’s not what you want to see.

I’ll say it again: Stumpf must go. Wells can survive this, but they need new leadership. The stock also got dinged this week when it was downgraded by JPMorgan (like they’re ones to judge). The overall loss in shares of WFC isn’t overwhelming, but the loss of prestige is distressing. They used to be one of the good guys. Wells is due to report Q3 earnings in three weeks.

Bed Bath & Beyond Disappoints

On Wednesday, Bed Bath & Beyond (BBBY) reported fiscal Q2 earnings of $1.11 per share. That was five cents below Wall Street’s estimates. Frankly, this was a lackluster quarter for BBBY in what’s been a lackluster year. For comparison, the home-furnishings company earned $1.21 per share in last year’s Q2.

For this year’s Q2, net sales fell 0.2% to $2.988 billion. The key to watch is comparable sales, which dropped by 1.2%. The company had been projecting an increase of 0% to 1%. What really helped Bed Bath this quarter was its online presence (remember the One Kings Lane acquisition). Comparable sales from what the company calls “digital channels” were up over 20%. But in-store comparable sales fell “in the low single-digit percentage range” for Q2.

Bed Bath continues to buy back tons of its own stock. Last quarter, they spent $121 million buying 2.7 million shares of BBBY. They still have $2 billion left in the current authorization. Given how the stock has performed, the company has spent a huge amount of money on a stock that hasn’t done much.

The good news is that Bed Bath is standing by its previous full-year earnings forecast of $4.50 to $5.00 per share. The company has already earned $1.91 per share for the first half of the year. Bed Bath & Beyond is not in a strong position this year.

Microsoft Raises Its Dividend by 8%

In the CWS Market Review from two weeks ago, I told you Microsoft (MSFT) would probably soon raise its dividend. I was right. On Tuesday, the software giant raised its quarterly dividend by 8%. The payout rose from 36 cents to 39 cents per share.

Microsoft continues to operate well in a difficult environment. In the last earnings report, Microsoft beat estimates by 11 cents per share. Their cloud business continues to do very well.

Microsoft also announced a $40 billion share-purchase plan. Based on Thursday’s closing price, Microsoft now yields 2.7%. That’s over 100 basis points more than the 10-year Treasury. I’m keeping my Buy Below price on Microsoft at $59 per share.

That’s all for now. Next week is the final week of the third quarter. Can you believe we’re already three-fourths done with 2016? On Thursday, we’ll get the second revision to Q2 GDP. The initial report showed growth of 1.2%. Last month, that was pared back to 1.1%. The Atlanta Fed’s model for Q3 is now down to 2.9%. On Friday, we’ll get data for personal income and spending. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 23, 2016

Posted by Eddy Elfenbein on September 23rd, 2016 at 7:04 amJapan’s Antitrust Watchdog Considers Action Against Apple, Carriers

Former OPEC President Optimistic There Will Be Deal in Algiers

Saudis Offer Oil Cut for OPEC Deal if Iran Freezes Output

LSE’s Rolet Says 100,000 Jobs at Risk If Clearing Leaves London

Treasuries Set for Best Week Since July as Fed Tempers Rate View

Airbnb Raises $555 Million in New Funding

Deutsche Bank is Losing Its Place At The Top Table of Investment Banking

The Man Who May Inherit the Mess at Wells Fargo

Hanjin Should Finally Have Enough Cash to Unload $14 Billion in Cargo

Harvard, Searching for Endowment Manager, Reports a Loss

Rogue Trader to Learn if He’s to Pay Back $5.5 Billion on His Own

Antiques Dealers Charged in Illegal Sale of Ivory Priced at $4.5 Million

Cullen Roche: The Problem With Modern Banking

Jeff Carter: Remaking An Old System

Be sure to follow me on Twitter.

-

Gold Miners Surge After Fed

Posted by Eddy Elfenbein on September 22nd, 2016 at 12:08 pm

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His