-

Three Earnings Reports

Posted by Eddy Elfenbein on April 21st, 2016 at 1:38 pmThis is a busy day for earnings reports. We had three before the open and a fourth is due after the bell.

First off, Snap-on (SNA) reported Q1 earnings of $2.16 per share. That topped Wall Street’s estimate by nine cents per share, but sales came in below expectations. I’m still targeting $9 in EPS for this year. The shares are down a bit today, but not too much.

Biogen (BIIB) is our big winner today. The biotech firm reported Q1 earnings of $4.79 per share, which beat expectations by 32 cents. Revenues rose 6.7% to $2.73 billion which was just below expectations. The shares are up about 4% today.

Alliance Data Systems (ADS) is again our problem child. For Q1, the company earned $3.84 per share which beat Wall Street’s estimate by two cents per share. The company had given guidance of $3.83 per share.

The problem was guidance. For Q2, ADS sees earnings of $3.58 per share which is 20 cents below Wall Street’s forecast. Traders didn’t like that at all. The shares have been down as much as 9% today. But the company said they’re on track to earn $16.75 per share for this year.

Microsoft’s (MSFT) earnings are due after the close. Wall Street is expecting earnings of 64 cents per share.

-

Morning News: April 21, 2016

Posted by Eddy Elfenbein on April 21st, 2016 at 7:39 amECB Keeps Up Unprecedented Stimulus as Draghi Assesses Impact

The $2 Trillion Project to Get Saudi Arabia’s Economy Off Oil

Sweden’s Central Bank Expands Bond-Buying Program

Oil Higher as IEA Expects Biggest Non-OPEC Output Fall in 25 Years

Verizon Profit Rises, But Misses Estimates

Mitsubishi’s Efficiency Scandal Point to Big Competition Among Japan’s Tiny Cars

GM Beats Estimates on Truck Sales in U.S., Break-Even in Europe

Southwest Tops Estimates on Higher Traffic, Lower Fuel Costs

Biogen Profit Beats on Higher Tecfidera Sales

Novartis Profit Falls as Blockbuster Cancer Drug Sales Drop

Travelers Profit Drops 17% on Hedge Funds, Texas Hail Storms

Qualcomm Profit Rises 11%, Dispute With LG Resolved

Uber Overtakes Rental Cars Among Business Travelers

Cullen Roche: 2 Concerns About the U.S. Government’s Debt

Howard Lindzon: Let’s Talk About Web Video…Again

Be sure to follow me on Twitter.

-

Stryker Earns $1.24 per Share

Posted by Eddy Elfenbein on April 20th, 2016 at 5:18 pmQ1 earnings for Stryker (SYK) are out. The company earned $1.24 per share which beat estimates by four cents per share. Net sales grew 4.9% to $2.5 billion. That’s 6.1% constant currency.

We are pleased by our first quarter performance and expect the momentum to continue,” said Kevin A. Lobo, Chairman and Chief Executive Officer. “As a result, we have raised our full year guidance for both sales and adjusted net earnings.”

Indeed they did. Stryker now sees full-year organic sales growing between 5.5% and 6.5%. The pervious range was 5% to 6%.

Stryker sees full-year earnings ranging between $5.65 and $5.80 per share. The previous range was $5.57 to $5.77 per share. For Q1, they see earnings coming in between $1.33 and $1.38 per share.

Regarding the impact of the dollar, Stryker said:

If foreign currency exchange rates hold near current levels, we expect net sales in both the second quarter and full year to be negatively impacted by approximately 1.0% and adjusted net earnings per diluted share to be negatively impacted by approximately $0.03 in the second quarter and $0.10-$0.12 in the full year.

-

Express Scripts Responds to Anthem

Posted by Eddy Elfenbein on April 20th, 2016 at 10:09 amEarlier this year, Anthem sued Express Scripts (ESRX) claiming that they were being cheated out of billions of dollars. Now Express Scripts has responded.

Express Scripts filed a response to the suit Tuesday in the U.S. District Court for the Southern District of New York. Express Scripts said it denied Anthem’s allegations “in their entirety” and listed its own counterclaims against Anthem, including the allegations of failing to negotiate in good faith.

Express Scripts is seeking a judgment stating that Anthem does not have a contractual right to any change in pricing under its agreement nor does it have a right to terminate the agreement with Express Scripts.

In addition, Express Scripts claims that Anthem has been “unjustly enriched” by a $4.7 billion cash payout it accepted in 2009 at the beginning of its agreement with Express Scripts.

“Notwithstanding Anthem’s conduct — ESI has at all times been committed to negotiating in good faith in an effort to satisfy its largest commercial client,” Express Scripts said in a federal filing about the lawsuit. The company said it made five separate counter-proposals to Anthem between June 2015 and March 2016, each of which offered “substantial pricing concessions that were well within the range of what Anthem publicly told the market it expected to receive,” according to the filing.

Express Scripts said it is “confident in the strength of its legal position.”

-

Signature Bank Earns $1.97 Per Share

Posted by Eddy Elfenbein on April 20th, 2016 at 7:42 amSignature Bank (SBNY) reported Q1 earnings of $1.97 per share. That’s their 26th record quarter in a row, and it beat estimates by two cents per share. The bank earned $1.64 per share in last year’s Q1.

For the quarter, loans rose 5.3% to $25.04 billion and Signature’s net interest margin was 3.32%.

“As we kick off 2016, which marks our 15th year in operation, Signature Bank delivered another quarter of solid financial performance. The 2016 first quarter saw record earnings for the 26th consecutive time, as well as both strong deposit and loan growth. We also see this as an opportune time to reflect on the growth of our business since our founding. We are extremely proud of the strong foundation and infrastructure we have built and nurtured over the years, which has helped sustain our consistent, strong organic growth,” explained Joseph J. DePaolo, President and Chief Executive Officer.

The bank has been burned by going into the taxi medallion loan business. The price of those medallions has plunged.

The Bank’s provision for loan losses for the first quarter of 2016 was $19.8 million, compared with $16.7 million for the 2015 fourth quarter and $7.9 million for the 2015 first quarter. The increase was primarily due to additional reserves for taxi medallion loans.

-

Morning News: April 20, 2016

Posted by Eddy Elfenbein on April 20th, 2016 at 7:13 amAfter Doha Bust, Oil Bulls Find Solace in Global Gasoline Boom

Germany Trims 2017 Growth Forecast to 1.5%

Google Charged With Breaking Europe’s Antitrust Rules

The U.S. Begins a Criminal Probe Into the Panama Papers Disclosures

CFPB Sheds Light on Coming Payday Loans Rule

Intel to Slash 12,000 Jobs as PC Demand Plummets

Apex Changes From Foe to Suitor With $3.6 Billion Lexmark Deal

Coca-Cola Zero Is Rebranding Itself in the UK As Britain Adopts a Sugar Tax

Lexmark Shareholders Clear Paper Jam With China Deal

Goldman Posts Weakest Results in Four Years; Revenue Tumbles 40%

Blankfein’s Decade Ending With a Thud on a Humbled Wall Street

Mitsubishi Motors Admits to Manipulating Fuel Economy Test Data

After $90 Billion Deal Flop, Honeywell’s CEO Gets Back on Script

Jeff Carter: The Danger of Theranos

Josh Brown: The Riskalyze Report: Advisors Warm to Gold, TIPS

Be sure to follow me on Twitter.

-

Talking Small-Caps

Posted by Eddy Elfenbein on April 19th, 2016 at 4:28 pm -

Morning News: April 19, 2016

Posted by Eddy Elfenbein on April 19th, 2016 at 7:11 amOK, Now OPEC Is Officially Dead

Oil Market Stumbles But Recovers After OPEC Impasse

German Investor Optimism Rises to 2016 High as China Risk Abates

Former Treasury Officials Urge Lew to Reconsider Inversions Rules

Early Warning Signs of Recession Flash Faintly in U.S. Jobs Data

Visa, Wal-Mart Move to Speed Checkout for Customers With Chip-Enabled Cards

Johnson & Johnson Beats Expectations, Boosts Guidance

Philip Morris Boosts Outlook as Profit Falls

Netflix Drops on Weak-Growth Forecast

UnitedHealth Tops Expectations, Raises Guidance

Verizon Turns to Shadow Workforce Amid Strike

General Mills and 7-Eleven Join the Venture Capital Crowd

Founder of China’s Tencent to Give $2 Billion in Shares to Charity

Cullen Roche: The Myth of Declining American Living Standards

Roger Nusbaum: Risk: Still On?

Be sure to follow me on Twitter.

-

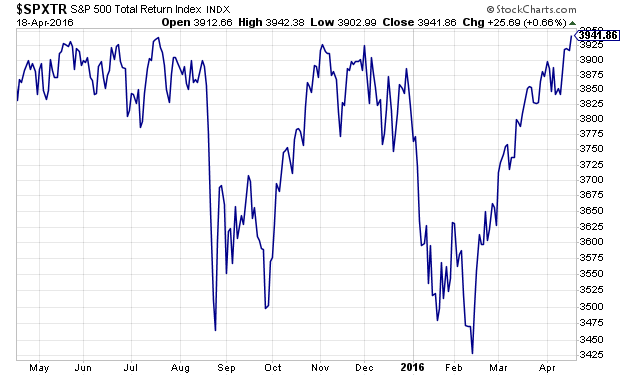

ATH

Posted by Eddy Elfenbein on April 18th, 2016 at 5:18 pm

Not for the S&P 500, but for the S&P 500 Total Return Index, which includes dividends. The S&P 500 Total Return Index closed today at 3,941.86, which is an all-time high. It surpassed the previous peak of 3,939.35 from July 20. Note that the S&P 500’s current high came on May 21. The index needs to rally another 1.7% to make a new high there.

-

This Year’s Blogger Wisdom

Posted by Eddy Elfenbein on April 18th, 2016 at 1:13 pmFor the last few years, Tadas Viskanta has asked a number of financial bloggers their opinions of important questions facing the industry. I was fortunate enough to be included in this year’s edition.

Here’s a list of the questions, along with my answers and the answers from some of my fellow finance bloggers.

Question: Venture capital has likely dried up for stand-alone robo-advisors. If so, where does the business of rob-advising go? Or said another way, is robo-advising simply going to be the way advisors manage client accounts going forward?

I skipped that one because I felt I don’t have anything profound to add but here’s Ben Carlson:

The competition for robo-advisors will continue to heat up because almost every wealth management or fund firm is going to have their own version of robo-advisor software at some point. I think the best way for robo-advisors to continue their growth will be to make a huge push into the workplace retirement business (something Betterment is already doing). The 401(k) and 403(b) markets are ripe for disruption by a low-cost provider as most of these plans are filled with terrible fund choices and high costs to plan users. Plus, the 401(k) market is much stickier in terms of clients because you have money automatically going into client accounts out of every pay check. Most companies don’t have the expertise to understand these plans on their own so offering a simple, low-cost solution would seem like an obvious way for robo-advisors to gain market share. This is especially true among small businesses who are the most over-charged group in need of a better solution.

Question: The ‘smart beta’ or factor-investing bubble seems to be in full bloom. Is ‘smart beta’ simply the new active investing? If so, what happens to the entire fund industry which was built on the high fees associated with active management?

Here’s me: I’m honestly not terribly impressed with Smart Beta. It’s mostly driven by marketing pitches. To my mind, it’s another form of chasing return. To the extent that any of these strategies work, it tends to be small and fleeting. (Make no mistake, I believe some are real.) The bottom line is that straight vanilla indexing is probably better for most investors, and simply buying and holding great stocks is even better than that.

Here’s David Merkel: Smart beta is a form of enhanced indexing. It is not active management. As in the quant quake in August 2007, “smart beta” will have its own episode of failure when too much money pursues it. It will be uglier due to the lack of human intervention. Active management will continue to shrink, but those who do it will have better opportunities. Fees will be under pressure, but less so than most imagine.

Question: Like just about every other blogger I have been writing on the rise on index investing. Should we care that the percentage of assets in indexes is on the rise, or should we just sit back and enjoy the (low cost) ride?

Here’s me: No, I’m not worried about the rise of indexing. The investment world loves to find things to be “concerned” about. Indexing is a great benefit for investors. I find the efficient versus inefficient debate to be pretty tedious. If you’re willing to accept what the market does, then indexing is a fine strategy. Still, with a little work, you can do better.

Here’s Josh Brown: Enjoy the ride. And know that the cure for “too much indexing” is already in progress in the form of a flat, choppy market that rises and falls but ultimately goes nowhere, which is the story of the MSCI All Country World Index heading into its third year of nothing. A few more and you’ll see a lot of the enthusiasm for low cost, passive dim.

Question: It does not escape me that the entire distribution list on this “Blogger Wisdom” e-mail chain is entirely male. I have written extensively on why this is an issue for the investment industry. What, if anything, can be done to make the investment industry more inclusive?

I didn’t have an answer but here’s Cullen Roche: If the men on this planet don’t exterminate each other in the future I am certain that the women will come to their senses one day and do it for us. A perfectly efficient stock market will be the result.

Question: Think back to the last edition of this series a couple of years ago. Have you changed your mind about something (big or small) over that time period? If so, what and why?

Here’s me: This may be an odd response, but I’ve recently changed my mind about volatility. Specifically, I think it’s incorrect to see volatility as some kind of gnome that stands above and apart from the market. To put it bluntly, the market doesn’t fall on volatility. Instead, volatility is up because the market is down. It falls when the market rises. The correlation between the VIX and the distance the market is from its six-month high is about 70%. I was surprised to see that it’s true.

Here’s Michael Batnick: I can’t think of anything that I’ve done an about face on, but one thing I am sticking with is my conviction to minimize the home country bias. I do not believe that investing in companies that generate a majority of their sales overseas is the same thing as investing in international stock markets. These giant multinationals are highly correlated with their domestic index and do not provide the same diversification benefits.

Question: What are you jazzed about that no one else is talking about? That could include a book, blog, Twitter feed, song, movie, app, online series, etc….

Here’s me: A few things. It looks like an ETF based on the Buy List will become a reality. We’re still in the planning stages, but it looks promising so far.

Another idea that’s bouncing around my head is the relationship of different market groups to each other. For example, why do bonds follow stocks for a while then break apart?

There’s been some quant work here (multi-dimensional scaling, etc). I think this is an unexplored vein, and it could reveal some important insights on the market.

Here’s Conor Sen: As I believe with rate hikes underway we’re in the late cycle in the US, I’m trying to think ahead to what the next cycle’s boom will be. At the moment from a tops-down perspective in the cycle from…I don’t know…2018-25? — I’d love to be in companies that are using some combination of data/analytics/information/automation/robotics, sensors, solar energy, and transportation to solve problems for consumers. More capex-heavy, less trivial app-conomy stuff.

Lastly, here are Tadas’ answers.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His