-

ADT Being Bought for 56% Premium

Posted by Eddy Elfenbein on February 16th, 2016 at 12:35 pmOne big finance story today is that ADT (ADT) is being bought out by Apollo Global Management for $7 billion. That’s a cool 56% premium. You may recall that ADT was spun-off from Tyco a little over three years ago.

There’s an interesting backstory to ADT. In 1863, Edward A. Calahan was working for the American Telegraph Company. He noticed that Wall Street employed boys as “runners,” kids who would dash around with the latest stock price news.

Calahan’s idea was to use a telegraph machine to do the same job, and presto, the stock ticker was born. The small paper used by the ticker machine was called ticker tape, and that was used for New York’s famous ticker tape parades. (Thomas Edison didn’t invent the stock ticker, but he pioneered an early version.)

Calahan formed the Gold and Stock Telegraph Company. Now I’ll turn it over to Wikipedia:

Three years later, the president of Gold and Stock Telegraph Company woke up to a burglar in his home, which inspired him to create a telegraph-based alert system. This system eventually connected 50 of his neighbors to a central station where all the alert boxes were monitored. There were many small telegraph delivery companies in the United States in the 19th century. In 1874, 57 district telegraph delivery companies affiliated and became “American District Telegraph”.

-

Hormel Foods Earns 43 Cents per Share

Posted by Eddy Elfenbein on February 16th, 2016 at 12:18 pmThis morning, Hormel Foods (HRL) reported fiscal Q1 earnings of 43 cents per share. That’s for November, December and January. Hormel’s earnings were six cents better than estimates. Revenues fell 4.3% to $2.29 billion which was a bit below consensus.

The good news is that Hormel raised their full-year 2016 forecast. The original range was $1.43 to $1.48 per share. Now it’s $1.50 to $1.56 per share. In other words, that largely seems to incorporate the six-cent earnings beat.

“We are pleased to report a double-digit earnings increase for the quarter, with four of our five segments posting earnings growth,” said Jeffrey M. Ettinger, chairman of the board and chief executive officer. “This marks our eleventh consecutive quarter of achieving record earnings results.”

“Our commitment to investing in the sustained growth of the business is evident in our results. Our business performance continues to be influenced by our company-wide spirit of innovation, increased brand support, prudent capital investment, and portfolio-expanding acquisitions,” commented Ettinger. “While sales were muted this quarter by turkey supply constraints and lower pricing due to declining pork markets, we enjoyed strong performance from many great products across our portfolio, such as HORMEL GATHERINGS® party trays, APPLEGATE® natural breakfast sausage, HORMEL® FIRE BRAISEDTM meats, MUSCLE MILK®PRO SERIES protein beverages, and WHOLLY GUACAMOLE® refrigerated dips.”

(…)

“Our strong earnings performance in the first quarter, led by Refrigerated Foods, Grocery Products, and Specialty Foods, along with the positive momentum at Jennie-O Turkey Store, has given us confidence to raise our fiscal 2016 earnings guidance range from $1.43 to $1.48 per share to $1.50 to $1.56 per share,” stated James P. Snee, President and Chief Operating Officer.

“We expect favorable input costs to continue for Refrigerated Foods, Grocery Products, and Specialty Foods, while we look for pork operating margins to moderate as the year progresses,” commented Snee. “Our turkey production is on pace to return to normalized levels by the end of the second quarter, positioning Jennie-O Turkey Store for strong growth in the back half of fiscal 2016 with our on-trend portfolio of JENNIE-O® turkey products. We expect International to achieve improved results with increased sales of our SKIPPY® peanut butter and SPAM® family of products.”

“As part of our efforts to drive revenue growth, we are currently investing in our brands through impactful new advertising campaigns for innovations such as our SKIPPY® PB BITES, and core items including HORMEL® pepperoni and MUSCLE MILK® protein products, ” added Snee.

This was a very good earnings report and the market gods are pleased. HRL shares are currently up 6.6% today. At one point this morning, the stock was up more than 10% on the day. Bloomberg notes that this is Hormel’s largest intra-day move in over 10 years.

-

Morning News: February 16, 2016

Posted by Eddy Elfenbein on February 16th, 2016 at 7:08 amPutin’s Reward for Doing a Deal With OPEC Overshadowed by Risks

BOJ Launches Negative Rates, Already Dubbed a Failure By Markets

China Turns on Taps and Loosens Screws in Bid to Support Growth

Swiss Won’t Rethink 1,000-Franc Note as Draghi Hails Crime Fight

German Investor Confidence Falls Amid Equity and China Woes

At Puerto Rico’s Power Company, a Recipe for Toxic Air, and Debt

Goldman Channels FDR’s `Nothing to Fear’ With Sell Gold Call

Anglo CEO Sees $1 Billion Brazil Niobium Sale Within Two Months

SoftBank Announces $4.4 Billion Share Buyback

A French Lesson For Li Ka-Shing

Apollo Global Management Nears Acquisition Deal for ADT

Anadarko Anoints `Brand Ambassadors’ to Fight Off Drilling Bans

Jeff Carter: The Flow; How Do You Get In The Zone?

Cullen Roche: What Have We NOT Learned Since 2008?

Be sure to follow me on Twitter.

-

Morning News: February 15, 2016

Posted by Eddy Elfenbein on February 15th, 2016 at 5:44 amJapan’s Nikkei Jumps 7.2 Percent, Leads World Stocks Higher

Severe Contraction and Falling Prices in Japan Signal Tough Test for Abenomics

Japan’s Banks Unready for Negative Rates Mean Cash Seen at Zero

Chinese Start to Lose Confidence in Their Currency

OPEC Members Increasingly Keen to End Oil Glut: Nigeria Oil Minister

Oil Trades Near $30 as Iran Loads for Europe, China Imports Fall

HSBC Keeps London Base in Victory Over Asia; Shares Gain

SoftBank Announces $4.4 Billion Share Buyback

Airbus, Boeing Count on China as Southeast Asia Slows Down

Greens Say Ikea Avoided at Least $1.1 Billion in Taxes to EU

Freeport Agrees $1 Billion Mine Stake Sale With Sumitomo

Don’t Blindly Follow Jamie Dimon, Deutsche Bank Says

Trial Illuminates Porches’ Rise to Power at Volkswagen

Jeff Miller: What Is The Biggest Market Worry?

Jeff Carter: The Real Reason Losing A Judge Like Antonin Scalia Hurts

Be sure to follow me on Twitter.

-

Talking Stocks on Bloomberg

Posted by Eddy Elfenbein on February 12th, 2016 at 9:55 pmI had a chance to discuss this hectic market on Bloomberg today with Scarlet Fu and Alix Steel:

-

CWS Market Review – February 12, 2016

Posted by Eddy Elfenbein on February 12th, 2016 at 7:08 am“Know what you own, and know why you own it.” – Peter Lynch

This was another dramatic week on Wall Street. On Thursday, the S&P 500 first tested, and later broke below, the “Tchaikovsky Low” of 1,812. At its lowest point, the index touched 1,810 which it hasn’t seen in two years.

Financial stocks were hit particularly hard. Big banks like Citigroup are now going for around six times next year’s earnings estimate. The price of oil also fell to $27.39 per barrel which is a 12-year low.

In this week’s CWS Market Review, I’ll try to make sense of the chaos. Basically, there are several factors that are converging all at once, and some of them seem to make little sense. For example, in Japan, the central bank has cut interest rates to negative territory, yet the yen is rallying. That’s not what the textbooks said will happen, but confounding conventional wisdom has pretty much been the theme of 2016.

Later on, I’ll cover this week’s earnings report from Cognizant Technology Solutions. I’ll also preview four more earnings reports coming our way next week. But first, let’s take a step back and look at the macro picture.

The Macro View

Since this has been such an unusual time for the markets, I want to list a number of different trends that are shaping the financial world.

Negative Interest Rates. In an effort to get their economies moving again, a number of central banks have cut interest rates to less than 0%. So far, the market response has not been very positive. As I mentioned before, in Japan, the yen has actually strengthened under negative rates (which is good for AFLAC).

At the European Central Bank, Mario Draghi seems especially frustrated. On top of that, there’s an emerging banking crisis in Europe. A number of banks got burned by bad loans to the energy sector. This has particularly impacted Deutsche Bank, but they’re not alone. Shares of Credit Suisse just slid to a 27-year low. With the economy still fragile there, Draghi may have to come up with some more magic tricks.

Back in the U.S.A., Janet Yellen testified before Congress this week and was asked about the possibility of negative interest rates. She didn’t say she was for it, but she didn’t rule it out. Of course, that’s what central bankers say about most anything. Frankly, I think the negative-rates talk for the Fed is very premature. Things would have to get a lot worse before that becomes a serious possibility. There’s also the question of whether that policy is even legal or feasible, given our financial system. My view is that they could do it if they wanted to, but that possibility is a long way off.

No Fed Rate Increases. A big change this year has been the outlook for interest rates. Not that long ago, the market had been expecting three or four rate increases this year. Now, almost no one believes that will happen though the Fed has so far stuck to its forecasts. The futures market sees the Fed largely standing pat.

You can see the impact of this revised outlook on certain sectors of the stock market. For example, utility stocks have rallied this year. That makes sense if rates stay low for longer. Conversely, financial stocks have done quite poorly. Those banks would have liked higher rates.

Many big banks are down by 20% or 30% in the last few weeks. That explains a lot of the weakness we’ve seen at Wells Fargo (WFC) and Signature Bank (SBNY). Bear in mind that those two banks are much stronger than many other banks. The S&P Bank Index is currently about where it was in August 1996. That’s nearly 20 years of no gains.

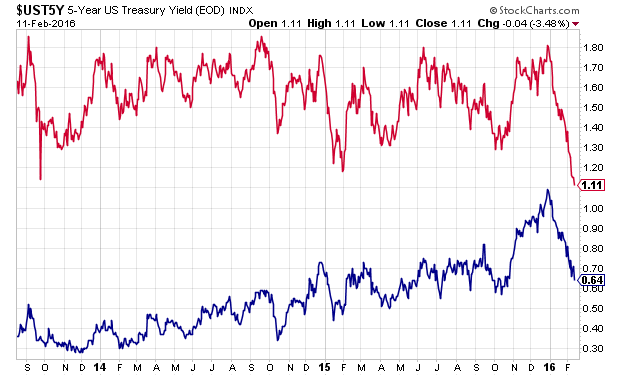

The Flattening Yield Curve. The new outlook for interest rates has also had a big impact on the yield curve. The middle part of that curve has become much flatter in recent weeks. For example, the yield on the five-year Treasury is down to 1.11%. That’s down from 1.80% on the second-to-last day of 2015. That’s a pretty stunning turnaround.

The spread between the two- and five-year Treasuries is now 47 basis points. That’s down from 70 basis points at the start of the year. Again, this reflects a belief that rates will stay low for longer. Interestingly, the spread at the longer end of the curve is largely unchanged. So I don’t think the flattening of the middle of the curve is a warning of a recession. When you see the 10-year above the 30-year, then it’s time to worry. We’re a long way from that.

Plunging Oil. The oil market continues to be in free fall. This is stunning. Every prediction of a bottom has failed. What’s interesting is that since late October, oil and the stock market have been strongly correlated. It used to be accepted wisdom that lower oil was good for our economy because it put more money in consumers’ pockets. That’s still true, but it overlooks the unpleasant side effects. For example, energy companies have cut back on hiring. Also, the junk-bond market got beaten up by some bad energy loans. In fact, that was also a factor Wells Fargo (WFC) discussed in its last earnings report. Although it’s not a major factor for Wells, it will be for other banks.

Valuation. The drop in medium-term rates has been a strong signal for prudent investors to focus on stocks with generous dividends. Let’s work some simple math. A five-year Treasury currently pays you 1.11%. That’s above half the dividend yield for the S&P 500. For the return of stocks to match the return of the five-year, stocks would have to decline by 1.11%, on average, for the next five years (this assumes dividends remain the same). That would bring the S&P 500 about 100 points lower by February 2021.

Obviously, this is a very basic analysis, but my point is to highlight the gap between the stock and bond market. The yield curve is demanding that investors buy dividend-friendly stocks. Microsoft, for example, currently yields 2.9%. They’re in little danger of cutting their dividend. The software giant generates $2 billion every month of cash flow. Wells Fargo yields 3.3%, and they’re in far better shape than they were a few years ago. In fact, it’s possible Wells will increase their dividend payout in April.

The Carry Trade. With negative interest rates, investors have crowded into the carry trade. This involves borrowing money in a currency with a low rate and investing in a currency with a high rate. You “carry” the investment across the border. This trade works up to the point where it stops working, and that’s what happened recently. A lot of traders got squeezed on their shorts of the Japanese yen, so they had to cover their trades, which pushed the yen even higher.

The Gold Rally. One surprise this year has been the strength in gold. Late last year, the yellow metal fell to around $1,050 per ounce and seemed to stay there. Lately, however, it’s caught fire. On Thursday, gold closed at $1,247 per ounce, which is an 18% gain the year. So is this a turn for gold? Possibly, but I’m a doubter. Lower real rates are good for gold, but the trade is also impacted by geopolitical events. Several tension spots around the world have flared up recently. Russia and Turkey are exchanging unpleasant looks, and North Korea is up to its usual antics. Gold tends to be the opposite of the stock market—it moves up very quickly, and slides downward very slowly.

Emerging Markets. A lot of emerging stock markets have not done well lately. This is really the effect of the U.S. dollar. This is an important point investors should understand. Since emerging markets are considered riskier, they have to offer more to draw overseas capital. When the dollar rallies, that pulls the rug out from the emerging markets. Furthermore, the money doesn’t leave slowly. It leaves very suddenly. The Emerging Markets ETF (EEM) has been battered for the last year.

Cognizant Technology Solutions Earned 80 Cents per Share

On Monday, Cognizant Technology Solutions (CTSH) reported Q4 earnings of 80 cents per share, which was two cents more than expectations. That’s a pretty good number. The company had previously said it expected earnings of at least 77 cents per share. Quarterly revenue rose 17.9% to $3.23 billion.

“We are pleased with our strong performance in 2015,” said Francisco D’Souza, CEO. “At a time when major technology shifts are disrupting all industries, clients are looking to a partner like Cognizant to work with them to create the winning business models of tomorrow at the intersection of the physical and digital worlds. Our investments in disruptive technologies, new business models and best-in-class delivery uniquely position us to enable clients to drive digital transformation at enterprise scale.”

For the year, Cognizant made $3.07 per share. Revenue rose 21.0% to $12.42 billion. Let me add some context. A year ago, their initial guidance for 2015 was for earnings of at least $2.91 per share and revenue of at least $12.21 billion. In other words, they outperformed their expectations.

Now for guidance. Cognizant sees Q1 earnings between 78 and 80 cents per share. In last week’s issue, I said I was expecting full-year guidance around $3.45 per share. The company, however, was more conservative. Cognizant expects 2016 earnings to range between $3.32 and $3.44 per share.

Wall Street did not like that. Shares of CTSH fell 7.7% on Monday. There’s no need to panic. I think the company is low-balling expectations so they can raise them later on. For now, I’m lowering my Buy Below on Cognizant to $58 per share.

Four Buy List Earnings Reports Next Week

Next week, three of our Buy List stocks will report Q4 earnings. We also have one stock, Hormel Foods (HRL), which is due to report, but they’re actually an early bird from the next cycle, as their fiscal quarter ended at the end of January.

On February 16, Cerner, Express Scripts and Hormel are due to report. Shares of Cerner (CERN) are still hurting from the unexpectedly weak outlook they gave late last year. But I think the selling is overdone. Wall Street expects Q4 earnings of 57 cents per share, which is a healthy increase over the 47 cents per share they made in Q4 of 2014.

In October, Express Scripts (ESRX) said they expect full-year 2015 earnings of $5.51 to $5.55 per share. That implies Q4 earnings of $1.54 to $1.58 per share. The shares dropped sharply last month after the company got into a public spat with Anthem (ANTM). I think these companies can work out their differences.

Not only was Hormel our best stock in 2015, but it’s also been our best stock so far in 2016. Through Thursday, the Spam stock is up 5.44% YTD. Wall Street expects fiscal Q1 earnings of 73 cents per share. That sounds about right.

Hormel also split 2-for-1 this week. That means shareholders now have twice as many shares. For track-record purposes, I assume the Buy List is a $1 million portfolio that starts the year with $50,000 in each stock. For Hormel, that was 632.2711 shares bought at $79.08. With the split, that’s now 1,264.5422 shares at $39.54. Hormel’s new Buy Below is $41 per share.

Lastly, Wabtec will report earnings on February 18. Their Q3 report was not good, and the shares have been punished ever since. The company sees Q4 earnings of $1.05. On Wednesday, the shares got a nice bounce after the board authorized a new $350 million share-buyback plan.

That’s all for now. The stock market will be closed on Monday in honor of George Washington’s birthday. (The NYSE, rightly, does not call it President’s Day.) In addition to the earnings reports, we can look forward to the industrial-production report on Wednesday. The latest Fed minutes will come out Wednesday afternoon. Then the CPI report comes out on Friday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: February 12, 2016

Posted by Eddy Elfenbein on February 12th, 2016 at 7:02 amNikkei Plunges Again in Worst Week Since Financial Crisis

Eurozone Economy Grows, but Total Output Still Lags Behind 2008

Greek Farmers Clash With Riot Police in Pensions Protest

Oil Rebounds From Lowest Close in 12 Years to Pare Weekly Loss

The Oil Industry Got Together and Agreed Things May Never Get Better

Federal Reserve Won’t Backpedal on Interest Rates, Janet Yellen Says

Have Millennials Made Quitting More Common?

Deutsche Bank CoCo Ratings Cut by S&P on Earnings Concerns

`Flash Boys’ Market Loses Support From Bats as Opposition Mounts

Pimco Says No Need to Be Greedy as It Bets on Battered Bank Debt

Joshua Brown: What We’re Telling Clients Today

Cullen Roche: Why Would Anyone Buy a Negative Interest Bearing Bond?

Be sure to follow me on Twitter.

-

Morning News: February 11, 2016

Posted by Eddy Elfenbein on February 11th, 2016 at 7:10 amSweden Cuts Rates Deeper Into Negative Territory, Says May Go Further

Indian Gold Demand to Climb in 2016 as Buyers Seek Safe Haven

Oil Is the Cheap Date From Hell

Treasury Yield at 3 1/2-Year Low as Yellen Suggests Rate Delay

Twitter User Growth Stalls, and the Chief Pledges to Make Fixes

SocGen Slumps as Quarterly Profit Hurt by Securities Drop

Rio Tinto CEO Sees Mining Distress Spreading to Majors

Tesla: Talk Is Cheap, Results Are Everything

PepsiCo Profit Up 31% to Top Estimates

Cisco Forecast Shows Spending Holding Up, Easing Concerns

The Bizarre Money Triangle at the Top of Viacom

U.S. Payday Lending Crackdown Brings Race Car Driver’s Arrest

Bear Markets Without Recessions – It’s a Thing

Jeff Carter: Free Enterprise Lifts People Up Better Than Government Socialism

Be sure to follow me on Twitter.

-

Hormel Foods Split 2-for-1

Posted by Eddy Elfenbein on February 10th, 2016 at 11:43 amPlease note that Hormel Foods (HRL) split 2-for-1 this morning. That means shareholders now have twice as many shares.

For track record purposes, I assume the Buy List is a $1 million portfolio that starts the year with $50,000 in each stock. For Hormel, that was 632.2711 shares bought at $79.08. With the split, that’s now 1,264.5422 shares at $39.54.

-

Janet Yellen’s Testimony

Posted by Eddy Elfenbein on February 10th, 2016 at 9:32 amHere’s the text of what Janet Yellen will be saying later this morning on Capitol Hill:

Chairman Hensarling, Ranking Member Waters, and other members of the Committee, I am pleased to present the Federal Reserve’s semiannual Monetary Policy Report to the Congress. In my remarks today, I will discuss the current economic situation and outlook before turning to monetary policy.

Current Economic Situation and Outlook

Since my appearance before this Committee last July, the economy has made further progress toward the Federal Reserve’s objective of maximum employment. And while inflation is expected to remain low in the near term, in part because of the further declines in energy prices, the Federal Open Market Committee (FOMC) expects that inflation will rise to its 2 percent objective over the medium term.

In the labor market, the number of nonfarm payroll jobs rose 2.7 million in 2015, and posted a further gain of 150,000 in January of this year. The cumulative increase in employment since its trough in early 2010, is now more than 13 million jobs. Meanwhile, the unemployment rate fell to 4.9 percent in January, 0.8 percentage point below its level a year ago and in line with the median of FOMC participants’ most recent estimates of its longer-run normal level. Other measures of labor market conditions have also shown solid improvement, with noticeable declines over the past year in the number of individuals who want and are available to work but have not actively searched recently, and in the number of people who are working part time but would rather work full time. However, these measures remain above the levels seen prior to the recession, suggesting that some slack in labor markets remains. Thus, while labor market conditions have improved substantially, there is still room for further sustainable improvement.

The strong gains in the job market last year were accompanied by a continued moderate expansion in economic activity. U.S. real gross domestic product is estimated to have increased about 1-3/4 percent in 2015. Over the course of the year, subdued foreign growth and the appreciation of the dollar restrained net exports. In the fourth quarter of last year, growth in the gross domestic product is reported to have slowed more sharply, to an annual rate of just 3/4 percent; again, growth was held back by weak net exports as well as by a negative contribution from inventory investment. Although private domestic final demand appears to have slowed somewhat in the fourth quarter, it has continued to advance. Household spending has been supported by steady job gains and solid growth in real disposable income–aided in part by the declines in oil prices. One area of particular strength has been purchases of cars and light trucks; sales of these vehicles in 2015, reached their highest level ever. In the drilling and mining sector, lower oil prices have caused companies to slash jobs and sharply cut capital outlays, but in most other sectors, business investment rose over the second half of last year. And homebuilding activity has continued to move up, on balance, although the level of new construction remains well below the longer-run levels implied by demographic trends.

Financial conditions in the United States have recently become less supportive of growth, with declines in broad measures of equity prices, higher borrowing rates for riskier borrowers, and a further appreciation of the dollar. These developments, if they prove persistent, could weigh on the outlook for economic activity and the labor market, although declines in longer-term interest rates and oil prices provide some offset. Still, ongoing employment gains and faster wage growth should support the growth of real incomes and therefore consumer spending, and global economic growth should pick up over time, supported by highly accommodative monetary policies abroad. Against this backdrop, the Committee expects that with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in coming years and that labor market indicators will continue to strengthen.

As is always the case, the economic outlook is uncertain. Foreign economic developments, in particular, pose risks to U.S. economic growth. Most notably, although recent economic indicators do not suggest a sharp slowdown in Chinese growth, declines in the foreign exchange value of the renminbi have intensified uncertainty about China’s exchange rate policy and the prospects for its economy. This uncertainty led to increased volatility in global financial markets and, against the background of persistent weakness abroad, exacerbated concerns about the outlook for global growth. These growth concerns, along with strong supply conditions and high inventories, contributed to the recent fall in the prices of oil and other commodities. In turn, low commodity prices could trigger financial stresses in commodity-exporting economies, particularly in vulnerable emerging market economies, and for commodity-producing firms in many countries. Should any of these downside risks materialize, foreign activity and demand for U.S. exports could weaken and financial market conditions could tighten further.

Of course, economic growth could also exceed our projections for a number of reasons, including the possibility that low oil prices will boost U.S. economic growth more than we expect. At present, the Committee is closely monitoring global economic and financial developments, as well as assessing their implications for the labor market and inflation and the balance of risks to the outlook.

As I noted earlier, inflation continues to run below the Committee’s 2 percent objective. Overall consumer prices, as measured by the price index for personal consumption expenditures, increased just 1/2 percent over the 12 months of 2015. To a large extent, the low average pace of inflation last year can be traced to the earlier steep declines in oil prices and in the prices of other imported goods. And, given the recent further declines in the prices of oil and other commodities, as well as the further appreciation of the dollar, the Committee expects inflation to remain low in the near term. However, once oil and import prices stop falling, the downward pressure on domestic inflation from those sources should wane, and as the labor market strengthens further, inflation is expected to rise gradually to 2 percent over the medium term. In light of the current shortfall of inflation from 2 percent, the Committee is carefully monitoring actual and expected progress toward its inflation goal.

Of course, inflation expectations play an important role in the inflation process, and the Committee’s confidence in the inflation outlook depends importantly on the degree to which longer-run inflation expectations remain well anchored. It is worth noting, in this regard, that market-based measures of inflation compensation have moved down to historically low levels; our analysis suggests that changes in risk and liquidity premiums over the past year and a half contributed significantly to these declines. Some survey measures of longer-run inflation expectations are also at the low end of their recent ranges; overall, however, they have been reasonably stable.

Monetary Policy

Turning to monetary policy, the FOMC conducts policy to promote maximum employment and price stability, as required by our statutory mandate from the Congress. Last March, the Committee stated that it would be appropriate to raise the target range for the federal funds rate when it had seen further improvement in the labor market and was reasonably confident that inflation would move back to its 2 percent objective over the medium term. In December, the Committee judged that these two criteria had been satisfied and decided to raise the target range for the federal funds rate 1/4 percentage point, to between 1/4 and 1/2 percent. This increase marked the end of a seven-year period during which the federal funds rate was held near zero. The Committee did not adjust the target range in January.

The decision in December to raise the federal funds rate reflected the Committee’s assessment that, even after a modest reduction in policy accommodation, economic activity would continue to expand at a moderate pace and labor market indicators would continue to strengthen. Although inflation was running below the Committee’s longer-run objective, the FOMC judged that much of the softness in inflation was attributable to transitory factors that are likely to abate over time, and that diminishing slack in labor and product markets would help move inflation toward 2 percent. In addition, the Committee recognized that it takes time for monetary policy actions to affect economic conditions. If the FOMC delayed the start of policy normalization for too long, it might have to tighten policy relatively abruptly in the future to keep the economy from overheating and inflation from significantly overshooting its objective. Such an abrupt tightening could increase the risk of pushing the economy into recession.

It is important to note that even after this increase, the stance of monetary policy remains accommodative. The FOMC anticipates that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate. In addition, the Committee expects that the federal funds rate is likely to remain, for some time, below the levels that are expected to prevail in the longer run. This expectation is consistent with the view that the neutral nominal federal funds rate–defined as the value of the federal funds rate that would be neither expansionary nor contractionary if the economy was operating near potential–is currently low by historical standards and is likely to rise only gradually over time. The low level of the neutral federal funds rate may be partially attributable to a range of persistent economic headwinds–such as limited access to credit for some borrowers, weak growth abroad, and a significant appreciation of the dollar–that have weighed on aggregate demand.

Of course, monetary policy is by no means on a preset course. The actual path of the federal funds rate will depend on what incoming data tell us about the economic outlook, and we will regularly reassess what level of the federal funds rate is consistent with achieving and maintaining maximum employment and 2 percent inflation. In doing so, we will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In particular, stronger growth or a more rapid increase in inflation than the Committee currently anticipates would suggest that the neutral federal funds rate was rising more quickly than expected, making it appropriate to raise the federal funds rate more quickly as well. Conversely, if the economy were to disappoint, a lower path of the federal funds rate would be appropriate. We are committed to our dual objectives, and we will adjust policy as appropriate to foster financial conditions consistent with the attainment of our objectives over time.

Consistent with its previous communications, the Federal Reserve used interest on excess reserves (IOER) and overnight reverse repurchase (RRP) operations to move the federal funds rate into the new target range. The adjustment to the IOER rate has been particularly important in raising the federal funds rate and short-term interest rates more generally in an environment of abundant bank reserves. Meanwhile, overnight RRP operations complement the IOER rate by establishing a soft floor on money market interest rates. The IOER rate and the overnight RRP operations allowed the FOMC to control the federal funds rate effectively without having to first shrink its balance sheet by selling a large part of its holdings of longer-term securities. The Committee judged that removing monetary policy accommodation by the traditional approach of raising short-term interest rates is preferable to selling longer-term assets because such sales could be difficult to calibrate and could generate unexpected financial market reactions.

The Committee is continuing its policy of reinvesting proceeds from maturing Treasury securities and principal payments from agency debt and mortgage-backed securities. As highlighted in the December statement, the FOMC anticipates continuing this policy “until normalization of the level of the federal funds rate is well under way.” Maintaining our sizable holdings of longer-term securities should help maintain accommodative financial conditions and reduce the risk that we might need to return the federal funds rate target to the effective lower bound in response to future adverse shocks.

Thank you. I would be pleased to take your questions.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His