-

Microsoft on Barron’s

Posted by Eddy Elfenbein on December 21st, 2015 at 11:55 amThis weekend’s Barron’s had some kind words for Satya Nadella and his leadership of Microsoft (MSFT). The company’s turnaround has been impressive. I encourage you to read the whole thing but I wanted to highlight this section which argues that analysts maybe underestimating MSFT’s earnings potential:

For the present, however, investors are still treating Microsoft like a traditional software company. The stock trades at 19.5 times fiscal 2016 earnings estimates, versus 80 for cloud-based Salesforce.com (CRM). And the forecasts are conservative. Analysts expect Microsoft’s sales and profits to be flat this year at $93 billion and $22 billion, respectively. Boosted by an aggressive buyback program, earnings per share could still grow 5%. Wall Street expects EPS to rise another 13% in fiscal 2017, to $3.13.

Moerdler is far more bullish. He says that $3.84 is more likely in fiscal 2017 and that analysts are underestimating the growth of Azure and overlooking Microsoft’s Office transition.

The Street’s more conservative numbers are an opening for stock gains. “It creates a big opportunity for Microsoft to ‘beat and raise,’ ” says Moerdler. Indeed, the stock jumped 10% in October after Microsoft reported September-quarter EPS of 67 cents, versus a 58-cent estimate. In April, Microsoft also gained 10%, on a better-than-expected quarter.

Aside from Azure, analysts are also missing the boat on Office, the popular productivity software that includes Word, Excel, PowerPoint, and Outlook. Office has been moving to a subscription model called Office 365, which already has 18 million consumer subscribers. About a quarter of the company’s corporate users have transitioned to the program, too.

(…)

By some math—counting the subscription Office business, Skype, Xbox, and Azure—Microsoft is already the world’s largest cloud company, with annualized revenue close to $10 billion. Microsoft has said its “commercial cloud”—Azure plus commercial Office and other business applications—will be a $20 billion annual business by 2018.

Bullish Microsoft investors, including Bonavico, think the opportunity is best viewed through the lens of free cash flow. Free cash accounts for the fact that, with subscriptions, the recognition of revenue trails the actual receipt of cash. David Pearl, co-chief investment officer at Epoch Investment Partners, thinks Microsoft will generate $3.49 in free cash flow in 2017 and $3.98 by 2018. At 18 times, he gets to a price of $72 in less than two years. And that’s without giving Microsoft any credit for the roughly $8 in net cash per share on its balance sheet. Epoch, which has $42 billion in assets, owns Microsoft stock worth $830 million.

Microsoft’s fiscal year ends in June, but we can translate their earnings into calendar year figures. The company will probably earn about $2.60 per share for 2015 which is up from $2.48 per share last year. However, that can ramp up to $2.92 per share for calendar year 2016. Their earnings have basically flatlined for the past few years but now appear to be heading upward.

-

Morning News: December 21, 2015

Posted by Eddy Elfenbein on December 21st, 2015 at 5:29 amThe Big Short Was Only One Reason 2015 Was The Year of the Bears

Brent Oil Slides to 11-Year Low as Producers Seen Worsening Glut

Yellen Says Economic Expansions Don’t Die of Old Age. Neither Do Bull Markets

Toshiba Sees Record $4.5 Billion Loss, Plans More Job Cuts

China Vanke Moves to End Potential Takeover Battle Within Weeks

Pandora Sees 7.5% Drop Day After CRB-Driven Surge; Analysts Positive on New Rates

’Star Wars: The Force Awakens’ Shatters Box Office Records

Regulations, Doubts and Concerns May Thwart Railway Mergers

Indonesia, Already Squeezed, Braces for Higher Interest Rates

Puerto Rico Deal Is Only a Small Fix for $70 Billion Debt Crisis

Panasonic to Buy Refrigeration Firm Hussmann for Over $1.2 billion

Martin Shkreli Says Drug Price Hikes Led to Arrest

Howard Lindzon: Martin Shkreli…Just Another Putz.

Jeff Miller: A Parade of Pontificating Pundits

Be sure to follow me on Twitter.

-

CWS Market Review – December 18, 2015

Posted by Eddy Elfenbein on December 18th, 2015 at 7:08 am“The expectation of an event creates a much deeper impression

on the exchange than the event itself.” – Jose de la Vega, 1688Ladies and gentlemen, here’s the 2016 Crossing Wall Street Buy List.

AFLAC (AFL)

Alliance Data Systems (ADS)

Bed Bath & Beyond (BBBY)

Biogen (BIIB)

Cerner (CERN)

Cognizant Technology Solutions (CTSH)

CR Bard (BCR)

Express Scripts (ESRX)

Fiserv (FISV)

Ford (F)

HEICO (HEI)

Hormel Foods (HRL)

Microsoft (MSFT)

Ross Stores (ROST)

Signature Bank (SBNY)

Snap-on (SNA)

Stericycle (SRCL)

Stryker (SYK)

Wabtec (WAB)

Wells Fargo (WFC)

The five new stocks are Alliance Data Systems, Biogen, Cerner, HEICO and Stericycle. I’ll have more to say about them next week. Don’t worry, I’ll go into full detail. I’ll also explain why I’m removing the deletions.

The six deletions are Ball, eBay, Moog, Oracle, PayPal and Qualcomm. Remember that we have an extra stock leaving this year due to the PayPal spinoff.

To recap, I assume the Buy List is equally weighted among the 20 stocks. The buy price for each stock will be the closing price as of December 31, 2015. The new Buy List goes into effect on January 4, 2016, the first day of trading of the new year.

The Buy List is now locked and sealed, and I won’t be able to make any changes for the entire year. I’ll have a complete recap of 2015 at the end of the year. I’ll also have more to say about our new buys, and I’ll give you new Buy Below prices.

As far as this year’s Buy List goes, there are only nine trading days left in 2015, and it appears that our Buy List will return to its market-beating ways. Through Thursday, our Buy List is up 4.09% while the S&P 500 is down 0.83% (not including dividends). This will be the eighth time in the last nine years that we’ve beaten the S&P 500.

The Federal Reserve Raises Interest Rates

This week, for the first time in nearly a decade, the Federal Reserve raised interest rates.

(Dramatic pause.)

To a still very, very low level. On Wednesday, the Fed did as we expected and raised the Fed funds’ target range to 0.25% – 0.50%. In my opinion, the Fed is probably a wee bit premature in doing this, but I can’t say it’s very damaging.

On one hand, there’s no sign of inflation. In fact, the government just said that inflation was flat last month. On top of that, commodity prices are still crashing. On Monday, spot oil dropped below $35 per barrel. Natural gas is now down to $1.74 per million BTU, and gold is at a six-year low.

But Janet Yellen said that the Fed wanted to move before there were signs of inflation. My opinion is that it’s impossible to get monetary policy exactly right. You’re bound to err on one side or the other. But I don’t think the Fed is being reckless in its policy. In fact, I think the central bank is right to convey the idea that it’s going to be guided by events.

It raised rates by 0.25%. For every $100,000, that works out to about 68 cents per day. I just don’t think that’s going to wreck the economy.

During the Fed’s last tightening cycle, it raised rates by 0.25% at 17 straight meetings. In retrospect, that was a big mistake. This time, the Fed has made it clear that there’s no predetermined path. I wouldn’t be surprised if the Fed only hikes rates once or twice all next year.

The Fed also released the economic projections from the FOMC members. These are the “blue dots” you may have heard about. I think the current projections are far too hawkish. The median dot sees four hikes this year followed by another four next year. No way. I expect to see the blue dots sing a different tune as the year goes on (I think I’m mixing metaphors.)

I’ll also credit the Fed for clearly communicating its actions to the public. The Fed said, “if X happens, we’ll do Y.” X happened. So they did Y. It’s really that simple. I have to address a common misconception. There’s a strong tendency to see the Fed as being much more powerful than it truly is. In reality, it’s reacting to the same forces we all are. I also don’t for a moment believe that the Fed’s actions are impacted by what goes on in China or the junk bond market or even the dollar. That’s just noise. The Fed pays attention to jobs and prices and that’s about it.

The stock market initially rallied after the Fed’s statement came out on Wednesday, but it gave back much of that gain on Thursday. Yields at the short end of the yield curve moved higher which you would expect. The two-year yield broke 1% for the first time since 2010 (see above). But long-term yields didn’t move much. That tells me that the Fed news was a yawner.

As a general rule of thumb, if your central bank isn’t making much news, then it probably has the right policy.

The main driver of the economy in 2016 will be the housing market, and that’s in pretty good shape. The good news is that it’s not a soaring but a steadily growing one. Expect to see a moderately expanding economy next year with growing corporate profits and still-low short-term interest rates. This is a good environment for stock investors.

Oracle Earns 63 Cents per Share

We had one earnings report this week, and it was our final one for the calendar year. It’s also from Oracle (ORCL), a stock which will not be returning with us next year. Oracle reported fiscal Q2 earnings of 63 cents per share, which was three cents more than expectations. Revenue fell 6% to $9.0 billion, but adjusted for currency, it was flat.

“We’re very pleased with our non-GAAP EPS of $0.63, beating the mid-point of guidance by 4 cents despite a stronger-than-expected currency headwind,” said Oracle CEO, Safra Catz. “We grew our SaaS and PaaS revenue 38% in constant dollars this past quarter, and we expect that revenue-growth rate to accelerate to nearly 50% in Q3 and close to 60% in Q4. This rapid increase in our cloud revenue will help drive our SaaS and PaaS cloud gross margins from 43% in Q2 to approaching 60% in Q4 and drive significant EPS growth in Q4.”

“It was a very strong growth quarter for our cloud business, with SaaS and PaaS bookings up 75% in constant currency and billings up 68% in U.S. dollars,” said Oracle CEO, Mark Hurd. “We did 100 Fusion HCM deals and over 300 Fusion ERP deals in the quarter. We now have more than 1,500 ERP customers in the cloud — that’s at least ten times more ERP customers than Workday.”

“We are still on target to sell and book more than $1.5 billion of new SaaS and PaaS business this fiscal year,” said Oracle Executive Chairman and CTO Larry Ellison. “That is considerably more SaaS and PaaS new business than any other cloud services provider, including salesforce.com.”

It’s not easy for me to let Oracle go, but I’ve felt that I’ve given them enough time to turn the ship around. The company has continuously said that things will start to improve, and I hope they do, but I’m done waiting.

On the conference call, Oracle gave fiscal Q3 guidance of 63 to 66 cents per share. For Q4, they gave guidance of 83 to 86 cents per share. The shares dropped 5.1% on Thursday to close at $36.93.

That’s all for now. The stock market will close at 1 p.m. on Thursday, December 24, and it will be closed all day on Friday for Christmas. On Tuesday, the government will release the second update for Q3 GDP growth. Last month, they revised the initial report of 1.5% growth up to 2.1%. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: December 18, 2015

Posted by Eddy Elfenbein on December 18th, 2015 at 7:02 amJapan Earmarks Billions to Help Prod Its Companies

Ukraine Defaults on $3 Billion Bond to Russia

Nigerian Farmers Cleared to Sue Shell in Dutch Court

I.M.F. Chief Faces Trial in Case Dating to Time as French Finance Minister

Hedge-Fund Casualties Jump to 257 in Third Quarter Amid Rout

Glaxo to Pay Bristol-Myers Up to $1.46 Billion for HIV Drugs

China’s Qihoo 360 Strikes New Buyout Deal

Apple to Launch Apple Pay in China, Take on Alibaba, Tencent

Zurich Buys Wells Fargo Crop Insurer for Up to $1.05 Billion

Dell’s Cybersecurity Unit SecureWorks Files to Go Public

P&G’s Gillette Sues Dollar Shave Club

LifeLock to Pay $113 Million to Settle FTC Charges

Drug C.E.O. Martin Shkreli Arrested on Fraud Charges

Cullen Roche: Yellen Fears the Boom, Part Deux

Be sure to follow me on Twitter.

-

Morning News: December 17, 2015

Posted by Eddy Elfenbein on December 17th, 2015 at 7:05 amIndia Stocks Rise Most in Month as Fed Rate Increase Eases Worry

Day 1 After Fed Liftoff Shows Move Catapults Money Market Rates

Congressional Leaders Agree to Lift 40-Year Ban on Oil Exports

How Democrats and Republicans Differ on Social Security

General Mills Profit Rises, Helped by Cost Cuts

Rite Aid Revenue, Same-Store Sales Rise

AstraZeneca Buys Most of Acerta for $4 Billion to Add Cancer Drug

Oracle Shift to Cloud Products Hasn’t Yet Spurred Growth

Valeant Makes Distribution Deal With Walgreens

Air France-KLM and BA Biggest Winners as EU Fines Thrown Out

The $500 Million Battle Over Disney’s Princesses

Shkreli, CEO Reviled for Drug Price Gouging, Arrested on Securities Fraud Charges

Finma Bans Six Former UBS Employees Over FX Rigging

Cullen Roche: Rate Hikes and Roulette Wheels

Jeff Carter: You Are In It For The Equity (And To Build Value)

Be sure to follow me on Twitter.

-

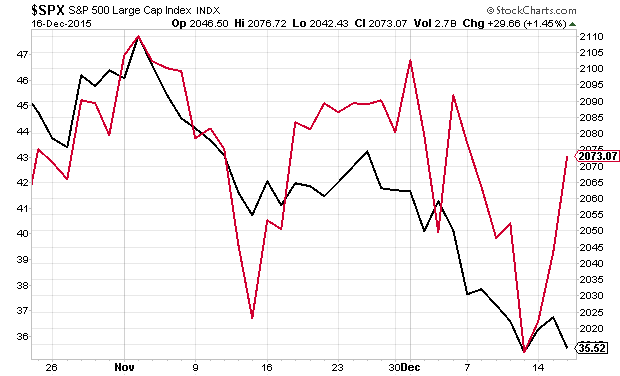

Oil and Stocks Part Ways

Posted by Eddy Elfenbein on December 16th, 2015 at 10:46 pmSince late-October, stocks and oil have been somewhat correlated. But today, on the day of the Fed meeting, there was a big divergence. Stocks did well while oil did not.

Here’s the chart:

What does it mean? That’s hard to say. Odd relationships can last for a few weeks before breaking up. I suspect that as oil starts to fall, it’s good for stocks. But if it falls too far too fast, then maybe it can harm the economy.

-

Yellen on Natural Rates

Posted by Eddy Elfenbein on December 16th, 2015 at 5:33 pmThis is from Janet Yellen’s press conference:

This expectation is consistent with the view that the neutral nominal federal funds rate–defined as the value of the federal funds rate that would be neither expansionary nor contractionary if the economy were operating near potential–is currently low by historical standards and is likely to rise only gradually over time. One indication that the neutral funds rate is unusually low is that U.S. economic growth has been only moderate in recent years despite the very low level of the federal funds rate and the Federal Reserve’s very large holdings of longerterm securities. Had the neutral rate been running closer to its longer-run level, these policy actions would have been expected to foster a much more rapid economic expansion.

The marked decline in the neutral federal funds rate may be partially attributable to a range of persistent economic headwinds that have weighed on aggregate demand. Following the financial crisis, these headwinds included tighter underwriting standards and limited access to credit for some borrowers, deleveraging by many households to reduce debt burdens, contractionary fiscal policy, weak growth abroad coupled with a significant appreciation of the dollar, slower productivity and labor force growth, and elevated uncertainty about the economic outlook. Although the restraint imposed by many of these factors has declined noticeably over the past few years, some of these effects have remained significant. As these effects abate, the neutral federal funds rate should gradually move higher over time.

This view is implicitly reflected in participants’ projections of appropriate monetary policy. The median projection for the federal funds rate rises gradually to nearly 1-1/2 percent in late 2016 and 2-1/2 percent in late 2017. As the factors restraining economic growth continue to fade over time, the median rate rises to 3-1/4 percent by the end of 2018, close to its longer-run normal level. Compared with the projections made in September, a number of participants lowered somewhat their paths for the federal funds rate, although changes to the median path are fairly minor.

I think this is very important and I’ll try to explain why. Prior to the recession, it was assumed that the natural rate was about 2% in real terms, meaning after inflation.

That means that the Fed’s job is pretty simple: bring the Fed funds rate below 2% to get the economy going, and then bring it above 2% when the economy is running hot. As such, the trend of real Fed funds should oscillate between about 0% on the low end and 4% or so on the high end. Check out this chart:

After the recession hit, all that went out the window. The Fed believes that the natural rate tanked and probably went negative. I think that’s right.

Now the “sine wave” of real rates may fluctuate between, say, -2% and +2%. According to today’s blue dots, the Fed expects the real Fed funds rate (the blue line in the chart above) to be -0.9% at the end of this year. It will rise to -0.2% at the end of 2016, and to +0.5% by the end of 2017. The Fed believes the long-rate rate is 1.4% which we can assume is the Fed’s guess for the natural rate. I think that’s too high.

To me, what the new numbers are isn’t exactly important. It’s that we live in a new economic world. The old rules no longer apply.

-

Oracle Earns 63 Cents per Share

Posted by Eddy Elfenbein on December 16th, 2015 at 4:40 pmOracle (ORCL) just reported fiscal Q2 earnings of 63 cents per share, three cents more than Wall Street’s consensus. Revenue fell 6% to $9.0 billion, but adjusted for currency, revenue was flat.

“We’re very pleased with our non-GAAP EPS of $0.63, beating the mid-point of guidance by 4 cents despite a stronger than expected currency headwind,” said Oracle CEO, Safra Catz. “We grew our SaaS and PaaS revenue 38% in constant dollars this past quarter, and we expect that revenue growth rate to accelerate to nearly 50% in Q3 and close to 60% in Q4. This rapid increase in our cloud revenue will help drive our SaaS and PaaS cloud gross margins from 43% in Q2 to approaching 60% in Q4 and drive significant EPS growth in Q4.”

“It was a very strong growth quarter for our cloud business, with SaaS and PaaS bookings up 75% in constant currency and billings up 68% in U.S. dollars,” said Oracle CEO, Mark Hurd. “We did 100 Fusion HCM deals and over 300 Fusion ERP deals in the quarter. We now have more than 1,500 ERP customers in the cloud — that’s at least ten times more ERP customers than Workday.”

“We are still on-target to sell and book more than $1.5 billion of new SaaS and PaaS business this fiscal year,” said Oracle Executive Chairman and CTO Larry Ellison. “That is considerably more SaaS and PaaS new business than any other cloud services provider including salesforce.com.”

The shares are up 2.2% in after-hours.

Update: Oracle is now down in the after-hours market. On the conference call, the company gave fiscal Q3 guidance of 63 to 66 cents per share. For Q4, they gave guidance of 83 to 86 cents per share.

-

The Bond Market’s Reaction

Posted by Eddy Elfenbein on December 16th, 2015 at 3:12 pmSo far, the market’s reaction is pretty muted. The two-year yield looks to close above 1% for the first time in several years.

-

The Fed’s Projections

Posted by Eddy Elfenbein on December 16th, 2015 at 2:22 pmHere are the Fed’s projections. This is often referred to as the “blue dots.” Personally, I think the Fed is way off here. They see rates rising much faster than I think is needed. The FOMC members currently project four rate hikes next year, and another four in 2017. I think we’ll see one, or maybe two, next year.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His