-

Bloomberg on Cognizant

Posted by Eddy Elfenbein on December 7th, 2015 at 3:18 pmBloomberg had a nice article on Cognizant Technology Solutions (CTSH):

On the penthouse floor of an office building in Midtown Manhattan, Cognizant has furnished a suite of rooms with hardwood floors and vintage furniture that wouldn’t look out of place in East Egg. Dotting the walls are framed photos of Elvis Costello, Charles Darwin, Martha Graham, and Pablo Picasso, and the office’s two terraces have views of the East River and the Chrysler Building. It’s a long way from the meeting rooms at Cognizant’s headquarters in Teaneck, N.J., and even farther from the cubicles that fill the company’s offices in India, where three-quarters of its 220,000 employees work.

The Manhattan setup is part of Cognizant’s effort to remake itself as a technology consultant instead of a cheap data-processing workhorse. In India, wages are rising and competition for labor is growing, so hiring tens of thousands of employees each year is no longer a guaranteed way to expand the business. In the U.S., congressional efforts to reduce the number of temporary visas outsourcing companies receive each year would further complicate Cognizant’s traditional business model. And worldwide, corporate clients that once relied on outsourcers to manage big SAP and Oracle databases have begun shifting the work to cloud services that require less hands-on management. New demand for the traditional outsourcing work “has ground to a halt,” says Bloomberg Intelligence analyst Anurag Rana. “IT budgets at best are flat to slightly up.”

And so Cognizant is working to create an image of quality over quantity. The company has 5,500 consultants, up from fewer than 1,000 in 2010, pitching strategic advice on IT, mergers, and customer service to clients such as the New England Health Exchange Network and Singaporean retailer NTUC FairPrice. The company is still adding workers to its outsourcing business but says it plans to slow hiring. “Five years ago it was more, ‘Tell us what to do, and we’ll do it well,’ ” says Cognizant President Gordon Coburn. “Today, we’re sitting at the table helping to generate ideas on how you can improve your processes.”

So far, Cognizant, which was spun off from credit reporter Dun & Bradstreet in the 1990s, has focused on advising clients concerned that digital upstarts could take away their customers. “Our clients are asking the question, ‘Will I be Ubered?’ ” says Malcolm Frank, executive vice president for strategy and marketing. Thanks to the investments Cognizant has made in consulting, he says, the company’s become a good judge of which businesses are at risk.

Cognizant, which posted $10.3 billion in revenue last year, is still small compared with consulting heavyweights Accenture ($30 billion) and IBM’s services division ($51 billion). But Cognizant’s shift toward consulting appears to be paying off: Profit is expected to approach $2 billion next year, up from $1.7 billion this year, $1.4 billion in 2014, and $884 million in 2011, according to data compiled by Bloomberg.

-

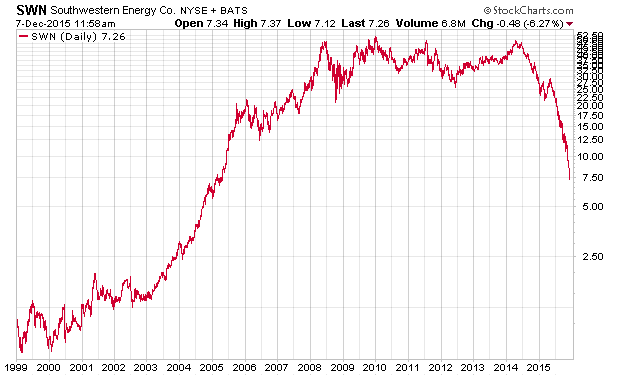

The Rise and Fall of SWN

Posted by Eddy Elfenbein on December 7th, 2015 at 12:26 pmRelated to my previous post on oil, check out the long-term chart on Southwestern Energy (SWN).

This was one of the super-star stocks of the last decade. Note that the graph is logarithmic so those are massive gains. In three years, the stock jumped nearly 15-fold. In 2005, SWN split 2-for-1 twice.

Eighteen months ago, SWN was at $47 per share. The stock just made another 52-week low today of $7.12 per share.

-

OPEC Has Surrendered

Posted by Eddy Elfenbein on December 7th, 2015 at 11:12 amThe news today is that oil prices are down again. But I think the more important news is that OPEC no longer effectively exists. They’ve surrendered. Of course, there’s still something called OPEC and it will continue to be influential. But at a very basic level, if a cartel can’t or won’t control prices, then it’s not a cartel. There’s really not much else to say.

The new production limits are limitless. Plus, there’s the issue of Iranian oil coming back online at some point. The giant as always is Saudi Arabia, and if they wanted, they could unleash a massive supply of oil onto the world. We’re seeing a rift grow between the core members of OPEC and the more marginal players (the ones like Ecuador or Venezuela which I always forget are in OPEC.) The marginal players are losing and badly.

In the U.S., the junk bond market is closely tied to oil production. As oil has fallen, junk bond spreads have increased. Again, it’s very basic. As long as the money flows, the oil will flow. As far as the U.S. is concerned, that funding will continue to dry up.

-

SBNY May Be the Best Bank in the World

Posted by Eddy Elfenbein on December 7th, 2015 at 10:13 amFriday was an interesting day for the market. Thanks to the strong jobs report and comments from Mario Draghi, investors lifted the S&P 500 back over 2,090. I was invited to be on CNBC’s Trading Nation on Friday afternoon, but the televised part was bumped due to the dramatic news conference held by police in San Bernardino. (The other clips we did are on CNBC’s website here, here and here.

A few items from our Buy List. On Thursday, Express Scripts (ESRX) increased the authorization of its stock buyback program by 60 million shares. The company now has approval to buy back 265 million shares of its own stock.

Oracle (ORCL) said it will report earnings December 16. That will be the final Buy List earnings report of this calendar year.

I also liked this piece on why Signature Bank (SNBY) may be the best bank in the world.

The kind folks over at Expecting Alpha took a closer look at our 2016 shopping list.

-

Morning News: December 7, 2015

Posted by Eddy Elfenbein on December 7th, 2015 at 7:07 amOPEC’s Divisions Keep Oil Low and Volatile

China Adds Most Gold in November in 5 Months as Price Slumps

A Revolving Door Helps Big Banks’ Quiet Campaign to Muscle Out Fannie and Freddie

Citigroup Said to Fall Under ECB Supervision After Units Combine

The DOJ Just Put Electrolux Shares Into a Spin Cycle

French Shipping Company CMA CGM, Buying Neptune Orient for $2.4 Billion

Why Reckitt Wants Part of Pfizer

AIG Offering Up to $1 Billion Stake in Chinese Insurer PICC P&C

Despite Low Oil Prices, Gates Looks to Gulf in Anti-Poverty Campaign

Toshiba Accounting Scandal Draws Record Fine From Regulators

Martin Shkreli, the Bad Boy of Pharmaceuticals, Hits Back

Sarcasm and Doubt Precede VW’s Update on Chearting Inquiry

Cullen Roche: How Much Can The Fed Raise Rates?

Joshua Brown: 10 Million Finance Jobs Lost Since 2000

Be sure to follow me on Twitter.

-

November NFP +211,000; UR 5.0%

Posted by Eddy Elfenbein on December 4th, 2015 at 8:32 amThe November jobs report is out. Non-farm payrolls rose by 211,000. The unemployment rate held steady at 5.0%.

The September NFP was revised higher by 8,000 and October was revised up by 27,000. Average hourly earnings rose four cents to $25.25.I think this pretty much guarantees a December rate hike.

-

CWS Market Review – December 4, 2015

Posted by Eddy Elfenbein on December 4th, 2015 at 7:08 am“There are two kinds of people who lose money: those who know

nothing and those who know everything.” – Henry KaufmanMark your calendars for two weeks from today! That’s when the 2016 Crossing Wall Street Buy List will be unveiled. Tens of millions of investors all over the world are eagerly awaiting our new list.

With only 19 trading days left this year, it looks like we’re going to beat the market yet again. The 2015 Buy List is currently up 4.04% for the year compared with a loss of 0.45% for the S&P 500 (not including dividends). And remember, we haven’t made a single trade all year.

In this week’s CWS Market Review, I’ll give you a sneak preview of some names that I’m considering for next year’s Buy List. I’ll also bring you up to speed on the latest announcements from the Federal Reserve. (I think a December rate hike is a foregone conclusion.)

Later on, I’ll cover the outstanding earnings report we got from Hormel Foods (HRL). The Spam stock not only raised its dividend for the 50th year in row but it also announced a 2-for-1 stock split. Hormel is now a 45.4% winner on the year for us! That’s more than Starbucks (SBUX) and Google (GOOGL). I’ll give you all the good news in a bit, but first, let’s see where Mr. Market stands right now.

The ECB Disappoints Investors

We’re now in the final trading month of the year, and going by recent history, December has been quite good for stocks. While the S&P 500 lost ground last December, it had rallied for 25 of the 30 Decembers previous to that including the last six in a row.

Thanks to losses on Wednesday and Thursday, the S&P 500 is now slightly negative for the year. It just dipped below its 200-day moving average (see below). The Dow is down 2% this year, and it may soon snap a very impressive streak. The index has rallied during the third year of an election cycle for the last 18 cycles in a row.

Personally, I would call 2015 a flat year for the market. Neither the bulls nor bears could hold center stage for very long this year. What happens after flattish years? History is on the side of the bulls. The S&P 500 has gained an average of 19% after years when it finished between -3% and +3%.

On Thursday, the European Central Bank announced its latest stimulus plans and Wall Street was not impressed. The economy in the Old World is still a mess, so everyone was expecting Mr. Draghi and his friends at the ECB to announce some seriously easy money policies. The ECB cut interest rates, which are already negative, from -0.2% to -0.3%. It also plans to step up its bond-buying program, but investors had expected more. In reaction, stocks sold off, and the euro did something it hasn’t done much lately—it rallied against the dollar.

At the same time, the Federal Reserve in the U.S. is getting ready to raise interest rates at its meeting on December 15-16. This week, Janet Yellen gave a fairly upbeat assessment of the economy. Personally, I think a rate hike this month is a done deal, but Wall Street still has some doubts. The futures market currently puts the odds at 79%.

What’s important for investors is that I doubt the Fed will go on a rate-hiking binge. Even a year from now, I think the real Fed funds rate, meaning adjusted for inflation, will still be negative. That’s a very good thing for stocks. As always, the name of the game is competition. As long as you can lock in a solid dividend (Ford at 4.3%, Microsoft at 2.7%), there’s not much to worry about from a one-year Treasury paying you 0.55%—and that’s up from 0.2% just a few weeks ago. That’s still the highest one-year yield in several years.

As I’ve explained before, at the center of world financial markets is the fact that the U.S. economy is out of sync with the rest of the world. From that fact radiates nearly everything we’re seeing—stocks, bonds, commodities, you name it. In fact, I could amend that statement by noting that the worsening of the Chinese economy leaves them out of sync with the rest of the world, but at the opposite end.

The economic reports out of China are notoriously unreliable, so we have to look at other indicators. Commodity prices, for example, have been quite weak. Gold recently fell to a six-year low. The price of iron dropped by $40 per metric ton. The government is finally cracking down on many shady brokers and insider trading. I expect the negative reaction to the ECB’s tepidness to carry over into Asian markets.

I was surprised that Draghi’s move disappointed the U.S. bond market as much as it did. The 10-year yield jumped to 2.33%. Of course, that’s not that high, but it’s certainly a big increase from several weeks ago. We need to keep an eye on this, because once those yields become competitive with stocks, stocks will lose their appeal.

The yield on the two-year Treasury is up to 0.94%, which is a five-year high. The 10-year TIP’s yield (that’s the inflation-protected security) is up 0.72%. Again, that’s still quite low. I would say that the 10-year TIP isn’t competitive with stocks until its yield gets up to 2.4% or so. In other words, we’re a long way from that. Now let’s take a look at some names I’m considering for next year’s Buy List.

Ten Possible Additions for Next Year’s Buy List

For next year’s Buy List, I’m going to add five new stocks. Here are ten stocks I’m strongly considering for next year’s Buy List:

Alliance Data Systems (ADS)

Cerner (CERN)

Church & Dwight (CHD)

FactSet Research Systems (FDS)

F5 Networks (FFIV)

Footlocker (FL)

HEICO (HEI)

Sherwin-Williams (SHW)

VF Corp. (VFC)

Zimmer Biomet (ZBH)

I still haven’t finalized my decision, but I wanted you to know some names that are under serious consideration. Now let’s look at one of our new stocks for 2015.

Hormel Foods Soars

Since I took off last week, I need to fill you in on Hormel Foods (HRL). The Spam stock has taken off recently. First, the company reported outstanding results for its fiscal fourth quarter. Hormel earned 74 cents per share which beat expectations by five cents per share.

“I am proud of the excellent fourth quarter delivered by our team, achieving record earnings for the tenth straight quarter. We reported record bottom-line results for the full year, with fiscal 2015 adjusted net earnings up 19 percent over last year and all five segments registering earnings growth,” said Jeffrey M. Ettinger, chairman of the board and chief executive officer.

For the year, Hormel earned $2.64 per share, which topped its announced range of $2.57 to $2.63 per share. That’s a 19% increase over last year. For 2016, Hormel projects a range of $2.85 to $2.95 per share. That was above Wall Street’s consensus of $2.83 per share.

Best of all, the Spam company raised its quarterly dividend by 16% to 29 cents per share. That comes to $1.16 per share for the year. This is Hormel’s 50th-straight annual dividend increase. If that’s not enough, Hormel also said it’s going to split the stock 2 for 1 early next year. The split will take effect on February 8 for shareholders of record as of January 26.

Hormel is now our top-performing stock this year with a YTD gain of 45.4%. This week, I’m raising my Buy Below on Hormel to $81 per share.

Buy List Updates

In the last issue of CWS Market Review, I covered the strong earnings report from Ross Stores (ROST). The deep discounter beat earnings for Q3 but didn’t raise guidance for Q4 as I expected. However, the shares jumped 10% the day after the earnings report and continued to rally from there. Ross has had a very impressive turnaround. From the low on November 13 to the high on December 2, the stock has gained more than $10 per share. On Wednesday, Ross came within two pennies of matching my $54 Buy Below price before pulling back on Thursday. For now, I’m going to keep the Buy Below on Ross at $54 per share.

Ball Corp. (BLL) is prepared to do whatever it takes to get regulator approval for its big Rexam merger. Ball said last week that it plans to sell 11 plants in order to appease the EU. Ball and Rexam are the two largest beverage-can makers in the world.

Shares of AFLAC (AFL) have been recovering nicely over the past few weeks. The duck stock broke $66 this year after being below $57 as recently as early October. On Wednesday, the stock got to its highest point since early 2014.

Unfortunately, AFLAC got stung for a 3.8% loss on Thursday after its presentation at the Goldman Financial Services conference. The company said it’s going to expand into commercial loans and equities. I don’t know why that would be seen as a negative for its business. The simple fact is that global interest rates are very low, so you need to adapt to the new environment. AFLAC isn’t the only insurer doing this.

AFLAC also said it expects to see currency-neutral EPS growth of 3% to 7% for next year. We don’t have the final numbers for 2014 yet, but that probably translates to a range of $6.30 to $6.50 per share. AFLAC remains a solid buy up to $67 per share.

While the controversy of high drug prices has affected other stocks, Express Scripts (ESRX) has largely been unharmed. This week, the drug-benefit manager is working on a deal to get patients a $1 alternative for Daraprim. That’s the stock that was marked up 50-fold this year by Martin Shkreli, the CEO of Turing Pharmaceuticals. For his part, Shkreli said he messed up by not raising the price even higher. Express Scripts is a buy up to $92 per share.

Shares of Wabtec (WAB) have been very weak lately. Since mid-September, the shares are off by more than 22%. I’m not worried about this one. The last earnings report missed by a little bit, but it wasn’t that bad. Stick with Wabtec. This week, I’m lowering my Buy Below on Wabtec to $82 per share.

That’s all for now. The November jobs report is due out later today. Next week, we’ll get the consumer-credit report on Monday. Then on Wednesday is crude inventories. The Treasury budget and initial jobless claims are out on Thursday. On Friday, we’ll get retail. Not one retail-sales report has beaten expectations this year. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: December 4, 2015

Posted by Eddy Elfenbein on December 4th, 2015 at 7:02 amECB Disappointment Halts U.S./Euro Zone Yield Divergence For Now

Why Negative Interest Rates Are Becoming the New Normal

Bonds Tumble by $270 Billion as Draghi, Yellen Batter Markets

German October Factory Orders Rebound After Three-Month Drop

China to Start Stock Circuit Breaker in January to Calm Swings

What to Expect From the Latest Jobs Report

A Full Break-Up Of Yahoo Vs. Swift Completion Of The Aabaco Spin-Off

Finding Treasure in Japan’s Computer Scrap Heap

Brown-Forman Profit Falls 3.8%

IDC Doesn’t Think Apple’s iPhone Business Will Grow in the Fourth Quarter

Lyft Joins With Asian Rivals to Compete With Uber

Avon Surges on Report Cerberus Is Buying North American Unit

Charitable Deductions Like Zuckerberg’s Generate Giving

Cullen Roche: Could the Fed Have Prevented the Financial Crisis?

Howard Lindzon: All Hail Verisign? ….Is The Boom in Internet Security about to Broaden

Be sure to follow me on Twitter.

-

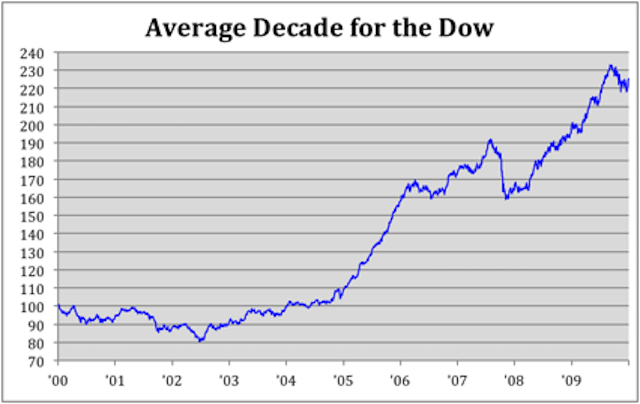

Average Decade for the Dow

Posted by Eddy Elfenbein on December 3rd, 2015 at 12:43 pmI had some spare time today so I’d thought I’d organize the entire 120-year history of the Dow Jones into an average decade.

This is what it looks like.

The chart begins at 100 at the beginning of the average decade. The Dow has historically been flat for nearly the first half of each decade. The Dow is still in the negative by August 6th of the fifth year (year ending in 4).

The back half of the decade is much better, although there’s historically been a spot of trouble during September and October of the eighth year (ending in 7).

The Dow has gained an average of 125% every ten years.

-

Morning News: December 3, 2015

Posted by Eddy Elfenbein on December 3rd, 2015 at 7:12 amAfter Yellen’s Teaser, Markets Hope for Draghi the Easer

Gold Rout Deepens on Yellen Remarks as Investors Flee From Funds

OPEC States Push for Output Cuts in Face of Saudi Opposition

Japan’s JX Holdings and TonenGeneral to Merge, Creating Oil-Refining Giant

Elon Musk: Only a Carbon Tax Will Accelerate the World’s Exit from Fossil Fuels

How Alibaba Can Help Clean Up Yahoo’s Mess

Google’s Latest Steps to Increase Its Use of Renewable Energy

Qualcomm Inks Critical Licensing Deal with China’s Xiaomi

Why Tech is Better Than Barclays

AB InBev Confirms It Wants to Sell Grolsch, Peroni Brands

E.U. Inquiry Into Possible McDonald’s Tax Breaks in Luxembourg

For Facebook’s Zuckerberg, Charity Is in Eye of Beholder

Jeff Carter: We Know How We Will Work, But What The Hell Are We Going To Do?

Roger Nusbaum: Managing ETF Liquidity

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His