-

CWS Market Review – November 13, 2015

Posted by Eddy Elfenbein on November 13th, 2015 at 7:08 am“We’re blind to our blindness. We have very little idea of how little we know.

We’re not designed to know how little we know.” – Daniel KahnemanLast week’s jobs report was, to put it mildly, a huge honking deal. The U.S. economy created 271,000 net new jobs last month. That’s the most this year, and it demolished expectations. Unemployment is down to 5.0%, which is a seven-year low.

Mind you, there are still weak spots, like the participation rate and sluggish wage growth, but the key takeaway for investors is that the Federal Reserve has the cover it needs to start raising interest rates next month. Think about that: For the first time in nearly a decade, rates will be going up.

If you recall, the Fed said that it will base a December rate hike on several factors, but we all know what they meant: more jobs. The stock market has shifted to reflect these new expectations. This is very important, and I want you to understand what it means. In this issue of CWS Market Review, I’ll cover the details.

I’ll also cover the recent Buy List earnings report from Moog (MOG-A). The stock is up 17% from its September low. I’ll also highlight upcoming earnings reports from Ross Stores (ROST).

Also this week, we got a nice 15% dividend increase from Snap-on (SNA). The stock then broke out to a fresh 52-week high. I love those steady winners. I’ll have all the details in a bit. But first, let’s take a closer look at the jobs report and how it’s altered the investment outlook for next year.

A Worldwide Commodity Crackup

Two weeks ago, I said that if the October and November job reports average 180,000, the Federal Reserve will go ahead with a rate increase in December. Well, the October report of 271,000 jobs is a darn good indicator that we’ll cover that.

According to bets placed in the futures market, there’s a 70% chance that the Fed will raise rates at their meeting scheduled for December 15-16. Watch for that to gradually increase. Interestingly, the futures market is pretty gun shy about rate increases after that. This supports my “one-and-wait” theory. I don’t think the Fed can make any more moves until there’s more evidence of inflation.

Investors reacted to the new expectations, but the initial results aren’t in the stock market. At Thursday’s close, the six-month Treasury got up to 0.35% and the one-year is up to 0.51%. Of course, those are still very low yields, but it’s the highest we’ve seen in a long, long time. The long-end of the market has also been impacted as the 10-year yield just crossed over 2.3%.

What’s happening is that the U.S. economy is out of sync with much of the world. We’re doing better while they’re stuck in neutral. That’s why the dollar has been doing so well. In fact, some folks are talking about the dollar soon reaching parity with the euro. That hasn’t happened in 13 years. Of course, we’ve seen the impact of the strong dollar on the earnings reports of several of our stocks, even ones you wouldn’t normally think of as having forex exposure.

Overall, our Buy List has not been as severely impacted by the strong dollar as other areas. In particular, I’m thinking of commodity-related areas. Copper, for example, just fell to a six-year low. Copper is often jokingly referred to as having a Ph.D. in economics. The metal’s movements have been a much better indicator of the world economy than many highly-paid forecasters’ calls. With the case of copper, it’s probably not signaling weakness here but rather in China. The world’s largest country consumes about 45% of the world’s copper output.

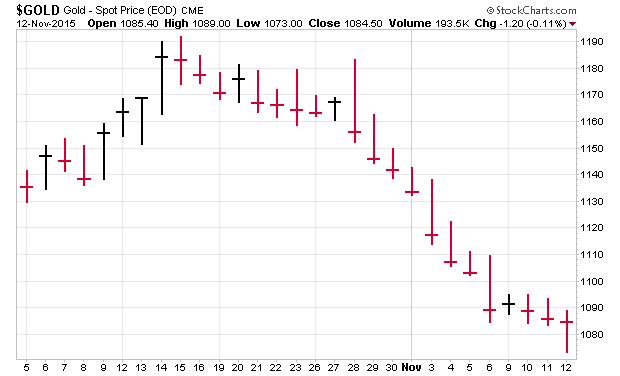

That’s not the only the commodity feeling the heat. Gold has dropped 17 times in the last 20 sessions (see below). Gold is now at a six-year low and platinum is at a seven-year low. Those guys are actually doing well compared with silver. Silver has fallen for the last 12 days in a row. We’re witnessing a worldwide commodity crackup.

Defensive areas of the stock market like utilities and healthcare haven’t done very well. More aggressive sectors like tech have been out in front, and consumer discretionary stocks have been rock stars.

We’re soon going to get a better view of the holiday shopping season. This is a vital time for many businesses. It’s true that more people are working, but we want to see more people buying.

I want to caution investors against feeling the need to gobble up any stock that’s had a bad day. Be patient and focus on superior companies. I especially like stocks that pay solid dividends. Investors just got a nice pay raise from Snap-on (SNA). I expect we’ll get one from Stryker (SYK) soon. Some of the best names on our Buy List are Cognizant (CTSH), Express Scripts (ESRX) and Wabtec (WAB). Now let’s look at the final earnings report for Q3.

Moog Is a Buy up to $64 per Share

Last Friday, we got our final Buy List earnings report for Q3. Moog (MOG-A) reported earnings of 75 cents per share (this was for the fourth quarter of their fiscal year). That was well below the company’s guidance of 91 cents per share and Wall Street’s consensus of 92 cents per share.

But once we dig into the details of the report, Moog said they lost 13 cents per share due to “incremental restructuring and impairment costs.” The company also said that they were hit by four cents due to a higher-than-expected tax bill.

Overall, this was a tough year for Moog.

Fiscal ’15 was a challenging year for our company across multiple fronts,” said John Scannell, Chairman and CEO. “In the face of these challenges, we delivered solid earnings and record cash flow. We are projecting a stronger fiscal ’16 with earnings per share of $4.00, up 19% on sales growth of about 2%.”

For the fiscal year, Moog earned $3.35 per share which is down from $3.52 last year. Annual sales fell 4.6% to $2.53 billion. I’m pleased to see Moog forecasting earnings of $4 per share for FY 2015.

Technically the report counts as an earnings miss, but traders were hardly bothered. Actually, Moog has been behaving well lately. The shares bounced off a low of $52.33 in late September and have been rallying ever since. This week, the stock broke briefly above $64 per share. I’m raising my Buy Below to $64 per share.

Earnings Preview for Ross Stores

I’m a big fan of Ross Stores (ROST). Some investors are put off by companies that cater to “low-end” consumers. That’s silly. Ross has served its customers well, and it’s been a winner for us this year.

That’s why I was puzzled by the tepid guidance the company gave after its last earnings report. Ross is due to report earnings again on Thursday, November 19. For fiscal Q3, which ended in October, Ross sees earnings ranging between 48 and 50 cents per share. That’s barely above the 47 cents per share they made in last year’s Q3.

Ross said they see same-store sales rising by 1% to 2%. Perhaps they’re low-balling us; it wouldn’t be the first time. For Q4, which is the big holiday quarter, Ross sees earnings between 60 and 63 cents per share with same-store sales growth of 0% to 1%.

Those numbers just don’t make sense. What’s going on? Barbara Rentler, the CEO, explained the guidance: “While we hope to do better, we are maintaining a cautious outlook for the second half, when we face more challenging sales and earnings comparisons. In addition, the macroeconomic and retail landscapes remain uncertain.” That doesn’t tell us much.

Adding it all up, Ross sees earnings this year coming in between $2.40 and $2.45 per share. They made $2.21 per share last year.

In August, the stock got nailed after the weak guidance. Ross got hit again this week when Macy’s (M) reported lousy results. That’s standard thinking on Wall Street: “if one company in a sector is doing poorly, then they all must be.” Another Buy List stock, Bed Bath & Beyond (BBBY), was dragged down as well. But Macy’s is a very different store from ROST or BBBY. In fact, next week, I think Ross will bump up its guidance for Q4.

Snap-on Raises Dividend by 15.1%

On Monday, Snap-on (SNA) announced it’s raising its quarterly dividend from 53 to 61 cents per share. That’s an increase of 15.1%. Snap-on has paid quarterly dividends without interruption since 1939.

I like this company a lot. Last month, Snap-on gave us another solid earnings report. For Q3, they earned $1.98 per share which was four cents better than expectations.

Annually, the new dividend comes to $2.44 per share which gives SNA a yield of 1.46% based on Thursday’s close. This year, Snap-on should earn about $8.06 per share, give or take. That’s up from the $7.11 per share they made last year, which keeps their payout ratio around 30%. This week, I’m raising my Buy Below on Snap-on to $175 per share.

The 2016 Buy List Will Be Unveiled on December 18

Circle December 18 on your calendars. That’s when I’ll unveil the 2016 Buy List. The new Buy List will take effect on January 4, 2016, the first day of trading in the new year. Once the names are out, the Buy List is locked and sealed, and I can’t make any changes for the next 12 months.

I like to reveal the new names early so no one can claim I’m somehow manipulating the stocks. I also want to show investors that there’s no need to rush out and madly buy up a stock.

Thanks to the PayPal (PYPL) spin-off, there are now 21 Buy List stocks. So this year, I’ll be deleting six names and adding our usual five. I always feel that if I’m doing the newsletter right, the decisions I make shouldn’t be a big surprise to readers.

I can tell you now that some stocks in my doghouse include Oracle (ORCL), Qualcomm (QCOM) and Ball (BLL). That’s not a promise. I still have time to change my mind, but I want to let you know what I am thinking. It looks like our Buy List is on its way towards beating the S&P 500 for the eighth time in the last nine years.

Buy List Updates

Signature Bank (SBNY) has responded very well to the prospect of higher interest rates. The stock got dinged toward the end of the summer for reasons I don’t get. No matter: SBNY recovered all of its loss. The stock recently touched another new high. This week, I’m raising my Buy Below on Signature Bank to $160 per share.

Shares of Express Scripts (ESRX) got dinged for 4% on Wednesday after the company cut its ties with Horizon Pharma (HZNP). Specifically, Express sent a termination letter to Linden Care, which is claimed to be a “captive” pharmacy of Horizon. Linden responded by suing Express.

This is part of the fallout from the mess at Valeant (VRX). No one wants to do business with these mail-order dispensaries, and I don’t blame them. On Wednesday, shares of Horizon plunged 20%. Don’t worry about ESRX. They made the right decision.

Shares of PayPal (PYPL) dropped late Wednesday and into Thursday after news broke that Apple (AAPL) is talking with some banks about setting up their own payment service. The service would let folks zap money from their bank account simply by using their iPhone. PayPal is already doing this with their Venmo platform.

There are no details on this story outside of Apple being “in talks.” I hardly think this is any of type of PayPal killer. I do think it’s part of a longer trend towards a cashless society. A PayPal spokesman said, “We welcome any development that encourages people to address the awkwardness of dealing with cash when paying friends or family back.”

That’s all for now. There are a few key economic reports coming our way next week. On Tuesday, the government will report on consumer inflation for October. I’m not expecting much, but if there’s any indication of incipient inflation, it will be more evidence for the monetary “hawks” to go ahead with a rate increase. On Tuesday, we’ll get a look at the minutes from the Fed’s recent meeting. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: November 13, 2015

Posted by Eddy Elfenbein on November 13th, 2015 at 6:12 amHalf of Russia’s Richest People Are Planning to Cash Out

French Economic Rebound Suggests Best Year Under Hollande

Hong Kong Posts Modest Third-Quarter Growth, Braces for China Slowdown

Fischer Says Strong Dollar Delayed Rate Rise, but Fed Could Move in December

U.S. Budget Deficit Edges Higher in October

After Budget Deal’s Surprise Cuts, Can Boomers Really Count on Social Security?

Hulu Service Said in Talks to Sell Stake to Time Warner

Kentucky Fried Chicken Real Meals Just Got Easier with DoorDash On-Demand Delivery

Fossil Group to Buy Misfit for $260 Million

Cisco Forecasts Miss Estimates as Currency Erodes Growth

Syngenta Shares Rise on Report of Chinese Takeover Interest

Liberty Media Lets Investors Bet On Radio, Baseball, With Tracking Stocks For Sirius, Atlanta Braves

Volkswagen, Offering Amnesty, Asks Workers to Come Forward on Emissions Cheating

Joshua Brown: Aggressive Financial Salespeople and Test Scores

Roger Nusbaum: Myopia & Market Function

Be sure to follow me on Twitter.

-

Morning News: November 12, 2015

Posted by Eddy Elfenbein on November 12th, 2015 at 6:08 amDraghi Stimulus Hint Underpins Stocks, Knocks Euro

Greece Comes to a Standstill as Unions Turn Against Tsipras

Russia’s Oil Rivalry With Saudis Masks the Bigger Iranian Threat

CICC Keeps It `Conservative’ With 300% China IPO Return Forecast

Apple, Banks in Talks on Mobile Person-to-Person Payment Service

Rolls Royce Plunges in London as Executive Jet Market Sags

Lenovo Posts Narrower-Than-Expected Loss Amid Phone Restructure

Macy’s Fights Downward Spiral With Bet on Off-Price Backstage Stores

Wal-Mart Goes ‘Deep’ on Holiday Inventory in Bid to Boost Sales

Kroger/Roundy’s Tie-Up Is A Win-Win For Both Parties

Airbnb Pledges to Work With Cities and Pay ‘Fair Share’ of Taxes

Merck KGaA Raises Forecast as Quarterly Profit Tops Estimate

The Next Internet? Marijuana Delivered as Easy as Pizza

Cullen Roche: Why No One Should Support the Gold Standard

Jeff Carter: What’s SnapChat Worth?

Be sure to follow me on Twitter.

-

Why Active Managers Lose

Posted by Eddy Elfenbein on November 11th, 2015 at 3:41 pmInteresting article at Bloomberg View. The authors address the puzzling reason why so many active managers lose to the indexes, even before fees.

The reason, they contend, is that stock returns are very unevenly distributed. The big winners are really, really big. So big that they skew the whole sample. So while the total index reflects that, it’s very hard for an active manager to select one of those few big winners.

Here is a simple illustration of our main idea:

Consider an index of five securities. Four (though we don’t know which) will return 10 percent and one will return 50 percent.

Suppose active managers choose portfolios of one or two securities and each investment is weighted equally. There are 15 possible one or two security “portfolios.” Of these, 10 will earn returns of 10 percent, because they will include only the 10 percent securities. Just five of the 15 portfolios will include the 50 percent winner, earning 30 percent if part of a two-security portfolio and 50 percent if it is the sole asset in a one-security portfolio. The mean average return for all possible actively managed portfolios will be 18 percent; the median actively managed portfolio will earn 10 percent. The equally weighted index of all five securities will earn 18 percent.

In other words, the average active-management return will be the same as the index, but two-thirds of the actively managed portfolios will underperform the index because they will omit the 50 percent winner.

It should be noted that there are some stock-pickers who have done quite well.

-

The TED Spread and Equity Returns

Posted by Eddy Elfenbein on November 11th, 2015 at 11:54 amI was curious to see if there’s a connection between the TED Spread and equity returns. The answer seems to be no, but there are some notable exceptions. That’s one of the issues in doing research—you spend a lot of time crunching the numbers only to reach a dead end. Still, I thought I’d share my results with you.

The TED Spread got a lot of attention during the financial crisis and it’s faded away since then. The TED Spread is the difference between the short-term Treasury yield and the Eurodollar yield (TED standing for Treasury-Eurodollar).

In short, this measures the level of panic within the financial system. For the most part, the TED Spread bounces between 0.1% and 0.5%. When folks get nervous, it spikes up to 0.7% and can even go as high as 1%. During the financial crisis, it spiked over 2% and got as high as 4.58%. That shows you just how scary those days were.

I went to the Federal Reserve’s database and took all the TED Spread numbers going back to 1986 and compared them with the Wilshire 5000 Total Return Index. I then divided the Ted Spread numbers into 10 buckets of increasing value (0.09% to 0.2%, 0.21% to 0.25%, etc.). I then saw how the market performed on those days, and I annualized those results.

Here’s what I got.

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His