-

Our Buy List Through November 18

Posted by Eddy Elfenbein on November 18th, 2015 at 5:43 pmThrough today’s trading, our Buy List is up 4.09% for the year while the S&P 500 is up 1.20%. Those numbers don’t include dividends but I will calculate those in our final performance numbers. Very roughly, dividends will add about 2% to the full-year return for the S&P 500, and about 1% for our Buy List.

I’m pleased that our Buy List is beating the market this year, but I wanted to point out that our lead has eroded since the summer. On August 20, our Buy List was up 5.21% on the year while the S&P 500 was down by 1.13%.

Since August 20, the S&P 500 is up 2.35% while we’re down 1.07%. Again, sans dividends. That’s hardly earth-shattering underperformance, but I always want to present the complete picture of our performance.

So what’s been dragging us down? It’s pretty easy to identify because four stocks stand out. Since August 20, Bed Bath & Beyond is down 13.84%, Ross Stores is off by 15.98%, Wabtec is down 19.76% and Qualcomm is down 20.20%. Ouch! Outside those four, the rest of the portfolio has been doing well.

I’m confident that we’ll beat the market again this year, but we’ve lagged a bit over the last three months.

-

The Fed Minutes Are Out

Posted by Eddy Elfenbein on November 18th, 2015 at 2:52 pmThe Fed just released the minutes from their October meeting. Here’s the important part:

During their discussion of economic conditions and monetary policy, participants focused on a number of issues associated with the timing and pace of policy normalization. Some participants thought that the conditions for beginning the policy normalization process had already been met. Most participants anticipated that, based on their assessment of the current economic situation and their outlook for economic activity, the labor market, and inflation, these conditions could well be met by the time of the next meeting. Nonetheless, they emphasized that the actual decision would depend on the implications for the medium-term economic outlook of the data received over the upcoming intermeeting period. Some others, however, judged it unlikely that the information available by the December meeting would warrant raising the target range for the federal funds rate at that meeting.

A number of participants pointed to various reasons why the Committee should avoid a delay in policy firming. One concern was that such a delay, if the reasons were not well understood by market participants, could increase uncertainty in financial markets and unduly magnify the perceived importance of the beginning of the policy normalization process (I’m sorry but that’s just silly – Eddy). Another concern mentioned was the increasing risk of a buildup of financial imbalances after a prolonged period of very low interest rates. It was also noted that a decision to defer policy firming could be interpreted as signaling lack of confidence in the strength of the U.S. economy or erode the Committee’s credibility (Oh, please – Eddy). Some participants emphasized that progress toward the Committee’s objectives should be assessed in light of the cumulative gains made to date without placing excessive weight on month-to-month changes in incoming data.

Several participants indicated that, despite lessening concerns about the implications of recent global economic and financial developments for domestic economic activity and inflation, appreciable downside risks to the outlook remained. They were concerned about a potential loss of momentum in the economy and the associated possibility that inflation might fail to increase as expected. Such concerns might suggest that the initiation of the normalization process may not yet be warranted. They also noted uncertainty about whether economic growth was robust enough to withstand potential adverse shocks, given the limited ability of monetary policy to offset such shocks when the federal funds rate is near its effective lower bound, and concern that the beginning of policy normalization might be associated with an unwarranted tightening of financial conditions. They believed that in these circumstances, risk-management considerations called for a cautious approach. They judged it appropriate to wait for additional information providing evidence of further improvement in the labor market and increasing their confidence that inflation was on a path to return to 2 percent over the medium term before raising the target range for the federal funds rate. In addition, a couple of participants cited concerns that a premature tightening might damage the credibility of the Committee’s inflation objective if inflation stayed below 2 percent for a prolonged period.

Several participants indicated that, in the current low interest rate environment, it would be prudent for the Committee to consider options for providing additional monetary policy accommodation if the outlook for economic activity were to weaken to a degree that seemed likely to undermine continued progress in labor market conditions and impede the movement of inflation back to the Committee’s 2 percent objective over the medium term. It was also noted that the Committee would need to reformulate its communications regarding the near-term outlook for monetary policy if the economic outlook weakened significantly.

During their discussion of the likely path for the federal funds rate after the time of the first increase in the target range, participants generally agreed that it would probably be appropriate to remove policy accommodation gradually. Participants also indicated that the expected path of policy, rather than the timing of the initial increase, would be the more important influence on financial conditions and thus on the outlook for the economy and inflation, and they noted the importance of underscoring this view at the time of liftoff. It was noted that beginning the normalization process relatively soon would make it more likely that the policy trajectory after liftoff could be shallow. It was also emphasized that, while participants’ most recent economic projections suggested that a gradual increase in the target range for the federal funds rate will likely be appropriate to support progress toward the Committee’s dual objectives, monetary policy adjustments ultimately would be dependent on economic and financial developments. These adjustments thus could be either more or less gradual than the Committee currently anticipates, responding to the Committee’s assessment of the implications of incoming information for the medium-run outlook.

-

South Korea Looks to Fine Qualcomm

Posted by Eddy Elfenbein on November 18th, 2015 at 1:01 pmYes, there’s even more bad news for Qualcomm (QCOM). More anti-trust issues. This time from South Korea:

Qualcomm Inc. said the staff of South Korea’s antitrust agency has alleged that some of the U.S. chip maker’s patent-licensing practices are illegal and recommended that the company be fined.

The company, which has battled antitrust cases in multiple countries, said a case examiner’s report generated by the staff of the Korea Fair Trade Commission, known as the KFTC, also recommended modifications to its business practices. A Qualcomm spokeswoman said the company hasn’t been informed of the size of any potential fine

The shares, which were already down 29% going into today, are down another 8.5% today. What a mess!

-

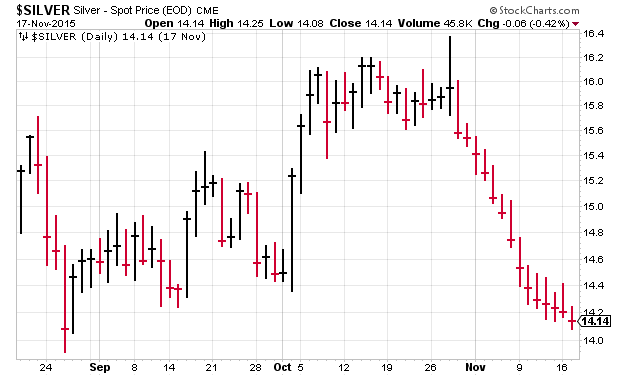

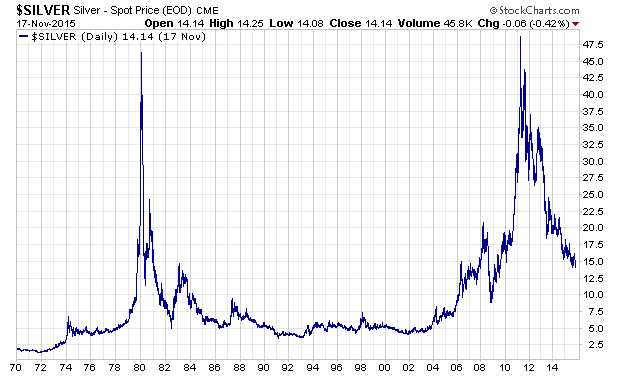

The Plunge in Silver

Posted by Eddy Elfenbein on November 18th, 2015 at 12:47 pmThe decline in silver has managed to do something impressive — it’s gotten even worse. The price of silver has fallen for the last 15 days in a row, and it looks to make it #16 today.

I once heard that slot machines are specifically designed to fall in the psychological sweet spot for the human brain. You win just often enough to keep playing but lose just enough to make the game a loser for you. I think commodity investing works the same way. Commodity investing seems to be defined by very large spikes followed by long, slow declines.

Check out the silver chart going back to 1970:

Thirty-five years after the Hunt brothers tried to corner the world silver market, the metal is still going for much less than it did at its peak in 1980.

-

Morning News: November 18, 2015

Posted by Eddy Elfenbein on November 18th, 2015 at 7:06 amSecurity Jitters Drive European Investors Back to Safe Havens

Greece and Eurozone Creditors in Deal to Unlock $13 Billion

Iran to Boost Oil Exports After Sanctions Are Lifted

South Africa Inflation Rate Rises to 4.7%, in Line With Estimate

Another AIG-Style Fed Bailout Is About to Become Less Likely

Amazon Ups the Ante on Black Friday With Deals Every Five Minutes

Marriott Merger Has Starwood Lovers Nervous

ConAgra Foods (CAG) Will Separate into Two, Pubicly-Traded Companies

ON Semiconductor to Buy Fairchild Semiconductor for $2.4 Billion

Lowe’s Profit Tops Estimates as Home-Price Gains Spur Sales

Lyft’s $1B Gross Run Rate In Context

How Airgas More Than Doubled By Fighting A Takeover

Square IPO Pricing Will Test Investors’ Appetite for Unicorns

Jeff Carter: A Discussion on Bitcoin/Blockchain

Roger Nusbaum: Wait, What Happened to the Rally?

Be sure to follow me on Twitter.

-

Will Utility Stocks Rebound?

Posted by Eddy Elfenbein on November 17th, 2015 at 9:13 pmUtilities have not been doing well this quarter nor this year. Part of the reason is that investors have factored in an interest rate increase from the Federal Reserve. Investors flock to utility stocks for their generous dividends, but with higher rates, utes will be somewhat less attractive.

Many utilities have also had to spend a large amount of money upgrading their systems. That ain’t cheap. The problem is that the utes have faced a lot of pushback from regulators when they’ve attempted to pass those costs on to their customers. In a low inflation environment, it’s hard to justify those higher costs. Today’s industrial production report showed a 2.5% drop for utility production.

If that’s not enough, utilities are starting to face real competition from solar. Some utilities are trying to diversify and many are moving into solar as well. Whenever a sector has pricing difficulty, you often see the push for mergers. A few weeks ago, Duke Energy (DUK) said it’s going to buy Piedmont Natural Gas for $4.9 billion in cash.

I was on CNBC earlier today to discuss the outlook for utility sector.

-

October IP = -0.2%

Posted by Eddy Elfenbein on November 17th, 2015 at 11:09 amOne negative report this morning came from the Federal Reserve. Industrial production for October dropped by 0.2%. Wall Street had been expecting an increase of 0.1%. On the plus side, the numbers for August and September were revised higher.

The stock market is largely unchanged today. We’re seeing some strength in homebuilding-related areas. Home Deport and Lowe’s, for example, are solid gainers today. Walmart is also up. The giant retailer beat estimates by five cents per share.

Interestingly, the Walmart earnings report might as well be a quarterly government report on consumer spending and inflation.

-

October CPI = +0.2%

Posted by Eddy Elfenbein on November 17th, 2015 at 10:24 amThe government reported today that consumer prices rose 0.2% last month. This is important because it’s more argument for the Federal Reserve to start raising interest rates next month. Some people thought that the terrible events in Paris might serve as convenient cover for the Fed to delay some more.

The “core rate,” which excludes volatile food and energy prices, also rose by 0.2%. Food and energy prices have significantly weighted on inflation in the past year. Consider that over the last 12 months, headline inflation is up by a mere 0.17%. But core inflation is up by 1.91%.

Here’s a look at the monthly core rate in annualized terms:

The odds of a rate hike next month are now up to 73.6%. The next big test will be the November jobs report.

-

Morning News: November 17, 2015

Posted by Eddy Elfenbein on November 17th, 2015 at 7:09 amWhat Wall Street’s Return to Central Banking May Mean for Policy

Oil Approaching $40 Deepens Investor Pessimism on Recovery

Druckenmiller, Bacon Among Top Managers Cutting Back U.S. Stocks

Encrypted Messaging Apps Face New Scrutiny Over Possible Role in Paris Attacks

Microsoft, Once Infested With Security Flaws, Does an About-Face

Amazon’s Holiday Shopping Target: The Procrastinator

Valeant’s Newest Problem: The Female Libido Pill Isn’t Selling

For-Profit College Operator EDMC Will Forgive Student Loans

Wal-Mart Earnings Beat Expectations

Home Depot Same-Store Sales Beat Estimates

Billionaire’s Supersonic Jet Advances With Factory Plans, Airbus

Joshua Brown: The Riskalyze Report: Advisors ♥ Small Caps

Cullen Roche: ISIS is About to Make the Euro Crisis a Lot More Challenging

Be sure to follow me on Twitter.

-

Morning News: November 16, 2015

Posted by Eddy Elfenbein on November 16th, 2015 at 7:08 amFrance Widens Crackdown at Home as Bombs Rain on Islamic State

Putin Goes From G-20 Pariah to Player at Obama Turkey Talk

Japan Falls Into Recession for Second Time Under ‘Abenomics’

Inflation Returned to Eurozone in October

After Outcry, Ireland Adjusts Its Corporate Tax Draw

Efforts to Rein In Arbitration Come Under Well-Financed Attack

Weak Retail Sales Suggest Moderate Fourth-Quarter Economic Growth

Oil Theft Soars as Downturn Casts U.S. Roughnecks Out of Work

Americans’ New Shopping Habit Hurting Some Retailers

Marriott to Buy Starwood to Create World’s Biggest Hotel Chain

China’s Tsinghua Unigroup to Invest $47 Billion to Build Chip Empire

German Watchdog Investigates Apple and Amazon Audiobooks Agreement

Microsoft, Code.org Will Use Minecraft to Teach Kids Programming

Jeff Carter: Are You For Free College? Free Drugs? High Minimum Wage?

Jeff Miller: What is the Message from Falling Commodity Prices?

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His