-

The Impact of Bad Weather on Analysts

Posted by Eddy Elfenbein on November 9th, 2015 at 2:32 pmI wouldn’t read too much into this fun, but I think it’s fun nonetheless:

To investigate the influence of weather on analysts, the team looked at 636,000 market observations by 5,456 brokerage-firm analysts known as sell-side analysts from 1997-2004. Because the researchers knew where the analysts were located, they could check the weather during each of the 636,000 observations.

Based on the calculations, comparing responses of analysts in good weather and bad when earnings announcements were made, analysts experiencing bad weather were 9% to 18% less likely to issue an annual earnings forecast; a recommendation to buy, hold or sell; or a target-price recommendation. Dr. deHaan says the calculations were designed to measure only the effect of weather, and canceled out such influences as characteristics of the firm, analyst or market conditions.

-

Snap-on Raises Dividend by 15%

Posted by Eddy Elfenbein on November 9th, 2015 at 10:28 amThis morning, Snap-on (SNA) announced a 15.1% dividend increase. The quarterly payout will rise from 53 to 61 cents per share.

Annually, that comes to $2.44 per share. This year, Snap-on should earn about $8.06 per share. Last year, they earned $7.11 per share. That keeps their payout ratio around 30%.

There have been a few times when SNA has skipped raising its dividend so it doesn’t have a long streak like some others. Still, the company has a long trend of raising dividends.

-

The Small-Cap Premium is Bunk

Posted by Eddy Elfenbein on November 9th, 2015 at 10:10 amThe other day, I wondered if the value premium was a thing of the past. Today, I’ll set my sights on the small-stock premium.

This is the observation that smaller-cap stocks have historically outperformed their larger peers over the long haul. I’m very suspicious on this point. It could be that smaller companies are more nimble and have a greater ability to adapt to a changing marketplace.

The problem, however, is how this is measured. We have to remember how unbalanced the stock market is. There are a small number of giant companies, and thousands of tiny ones.

When divided into size deciles, the smallest 10% of stocks comprise about 3% of the total market. That’s about the size of one mega-cap stock. It would be like looking at the long-term outperformance of one particular S&P 25 stock and claiming a premium for it.

There’s also an issue of how volatile this premium is. Here’s a look at the Russell 2000 divided by the Russell 3000. This shows that over the last 37 years, small-caps have underperformed.

For it to be a premium, I think it needs better performance than that.

There’s also a larger problem methodology. Michael Batnick relates the poor statistical foundation that the long-term returns are based on.

-

Morning News: November 9, 2015

Posted by Eddy Elfenbein on November 9th, 2015 at 7:15 amOECD Warns of Global Trade Slowdown, Trims Growth Outlook Again

China’s Trade Drop Means More Stimulus Measures Are Coming

Yergin Joins OPEC in Seeing Oil Market Balanced as Soon as 2016

Dollar Bulls are Vulnerable as Currency’s Strength May Cap Rates

Banking Giants Learn Cost of Preventing Another Lehman Moment

Regulators Urge Broader Health Networks

Dish Tops Profit Expectations Despite Pay-TV Subscriber Losses

Ericsson, Cisco Pool Telecom, Internet Savvy in Wide-Reaching Alliance

Snapchat Triples Video Traffic As It Closes the Gap With Facebook

PrairieSky Agrees to Acquire Canadian Natural Royalty Assets

Boeing Ends Dubai Drought With $8 Billion 737 Deal From Jet

Bonus Pay on Wall Street Is Likely to Fall, a Report Says

Jeff Miller: What Will Higher Interest Rates Mean for Financial Markets?

Be sure to follow me on Twitter.

-

Moog Earned 75 Cents per Share

Posted by Eddy Elfenbein on November 6th, 2015 at 1:29 pmThis morning, Moog (MOG-A) became our final Buy List stock to report earnings for this season. The company reported fiscal Q4 earnings 75 cents per share. However, 13 cents went to “incremental restructuring and impairment costs.” The company also said that they were hit by four cents due to a higher-than-expected tax bill. Wall Street had been expecting 92 cents per share, and the company gave us a forecast of 91 cents per share.

The market doesn’t seem too upset with the earnings miss. The shares are currently up about 1%.

The good news is that they’re standing by their forecast for next year of $4 per share.

Fiscal ’15 was a challenging year for our company across multiple fronts,” said John Scannell, Chairman and CEO. “In the face of these challenges, we delivered solid earnings and record cash flow. We are projecting a stronger fiscal ’16 with earnings per share of $4.00, up 19% on sales growth of about 2%.”

This was a tough year for Moog. Earnings-per-share fell from $3.52 to $3.35. Sales fell 4.6% to $2.53 billion.

-

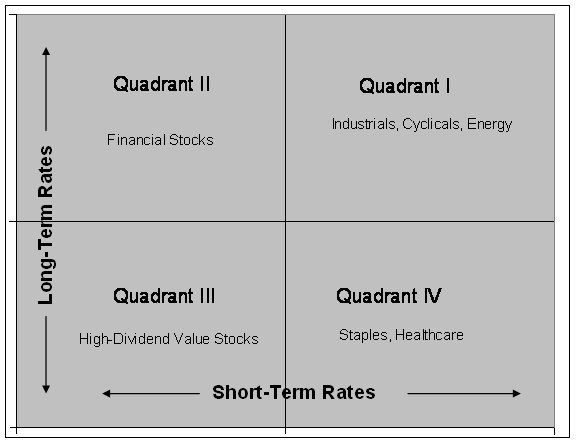

Classic Quadrant II Day

Posted by Eddy Elfenbein on November 6th, 2015 at 1:11 pmEarlier this year, I laid out my “Elfenbein Theory to Explain the Entire Stock Market.” It basically describes how interest rates influence the stock market.

Here’s the key matrix:

I would say that today is a classic Quadrant II day. Bank stocks are doing well, but defensive stocks are in the rear. Short-terms are up not down, but my theory is based on their relative impact.

Again, I’ll stress to not take this as a perfect map of what the market does, but it’s a good way of seeing general market relationships.

-

Q3 2015 Earnings Calendar

Posted by Eddy Elfenbein on November 6th, 2015 at 11:42 amSeventeen of our 21 Buy List stocks report Q3 earnings in the current reporting season. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

Stock Symbol Date Estimate Result Wells Fargo WFC 14-Oct $1.04 $1.05 Signature Bank SBNY 20-Oct $1.82 $1.88 eBay EBAY 21-Oct $0.40 $0.43 CR Bard BCR 22-Oct $2.23 $2.28 Microsoft MSFT 22-Oct $0.59 $0.67 Snap-on SNA 22-Oct $1.94 $1.98 Stryker SYK 22-Oct $1.23 $1.25 Wabtec WAB 22-Oct $1.04 $1.02 AFLAC AFL 27-Oct $1.48 $1.56 Express Scripts ESRX 27-Oct $1.44 $1.45 Fiserv FISV 27-Oct $0.97 $1.03 Ford F 27-Oct $0.47 $0.45 PayPal PYPL 28-Oct $0.29 $0.31 Ball Corp. BLL 29-Oct $0.95 $1.10 Cognizant Technology CTSH 4-Nov $0.76 $0.76 Qualcomm QCOM 4-Nov $0.86 $0.91 Moog MOG-A 6-Nov $0.92 $0.75 What if the Value Premium is Gone?

Posted by Eddy Elfenbein on November 6th, 2015 at 11:17 amWhen I was on CNBC last week, I noted the long underperformance of value stocks. The value guys haven’t led the market in a few years. This is unusual because a large body of academic work has shown that value stocks have historically outperformed the market.

Professor Noah Smith wonders if the value premium no longer exists.

As financial markets improved, we may have seen the entrance of more investors who are willing to do the hard work of digging up obscure and boring companies, and who are willing to go against the herd. If the value premium really was a systematic underpricing rather than a true risk premium, then the gradual development of financial markets would be expected to shrink this premium over time.

There are signs that this is happening. Although value stocks did well in the early 2000s, they have dramatically underperformed since the crisis, even though the market has boomed. Of course, that might simply be a particularly long period of underperformance — we might expect to see value bounce back soon enough. But in fact, the decline has been going on for quite a bit longer than that — the value premium has been falling since the mid-1990s. Coincidentally, that is exactly when the Internet and computerized trading systems made it possible to invest in stocks much more cheaply, and to gather information much more easily.

That would mean that markets are getting more efficient — at least, in this one particular way. But it would also mean that market efficiency takes a very long time to establish itself. If big, systematic mispricings such as the value premium can survive for decades before they are finally traded away, it means that other flaws in the market might be equally long-lived. For example, the momentum factor — another mainstay of standard finance theory — might also be a market flaw that will eventually be shown the exits.

If the market is that inefficient, it also means that stock prices are, in some deep sense, “wrong” — that they are not the best available estimate of a company’s value. That would suggest we should be relying on markets less than we do for things like executive compensation. So watch to see if the value premium comes back. If it doesn’t, it means it might never have been about risk in the first place.

It’s an interesting thought. The only thing I would add is that value investing suggests that the market is both right and wrong. It’s inefficient in that values emerge and efficient in that it recognizes the error.

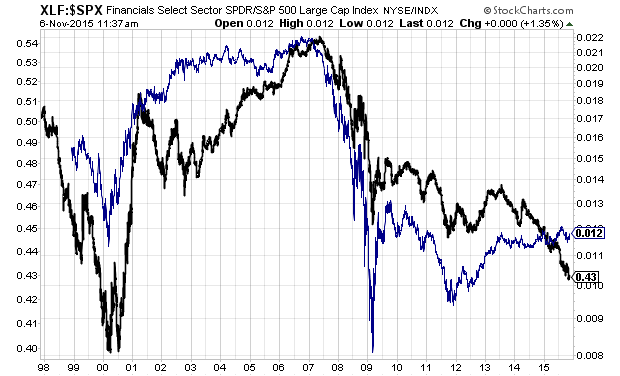

Make that two things. I’m curious how much financial stocks have weighed down value indexes. The sector hasn’t been too strong since, oh, about 2006.

Here’s a look at financial stocks divided by the S&P 500 (in blue) and value stocks divided by the S&P 500 (in black). (I apologize if it looks confusing.)

The point being that the performance of financials seems to be related to the performance of value. Note that that relationship has parted ways in the last two years. Nevertheless, the fallout from the financial crisis may be impacting the long-term performance of value stock indexes.

The Market’s Response

Posted by Eddy Elfenbein on November 6th, 2015 at 9:56 amThis is an interesting day as Wall Street digests the impact of today’s strong jobs reports.

The overall market is down a little bit, but there’s a lot going on under the covers. For example, bank stocks are doing very well today. On our Buy List, Signature Bank (SBNY) and Wells Fargo (WFC) are having very good days.

Utility stocks and some defensive areas like Staples and Healthcare aren’t doing so well. Qualcomm (QCOM) is recovering a bit after yesterday’s debacle.

The bond market is moving lower. The 10-year Treasury is up to 2.32%. On October 14, it had closed at 1.98%. Gold is down for the eighth day in a row. Dan Rosenblum informs me that gold is down 15 times in the last 17 sessions.

Check out the reaction in the six-month Treasury.

Very Strong Jobs Report for October

Posted by Eddy Elfenbein on November 6th, 2015 at 8:52 amThe October jobs report is out and it’s a good one. The U.S. economy created 271,000 net new jobs last month, and the unemployment rate fell to 5.0%. Wall Street had been expecting 183,000. That’s the lowest jobless number since April 2008.

The payroll number for August was revised higher by 17,000 while the number for September was revised lower by 5,000. That’s a combined increase of 12,000. The number for October was the strongest report this year. Average hourly earnings were up 0.36%.

This most likely means that the Fed is ready to raise interest rates at their December 15-16 meeting.

The markets are shifting to this news. The stock market looks to open lower. The two-year yield is up to 0.91% and the six-month yield is up to 0.35%. These are both multi-year highs.

The odds of a rate hike next month are now up to 73%. The odds for another hike in June have moved up from 53.4% to 64.2%.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His