-

Moynihan Wins Vote

Posted by Eddy Elfenbein on September 22nd, 2015 at 11:04 amThe New York Times report

Brian T. Moynihan gets to keep his job as both chief executive and chairman of Bank of America after shareholders on Tuesday backed the board’s decision to grant him both titles.

Roughly 63 percent of the shareholders’ votes cast approved a proposal allowing the board to decide whether its top executive should hold a dual leadership role at the bank.

Critics said their opposition to the measure was less a judgment on Mr. Moynihan’s stewardship of the bank and more a rejection of the way he and the bank’s board went about combining the chief executive and chairman titles last October. The board unilaterally overturned a shareholder vote in 2009 that required the two roles be separated.

Tuesday’s vote had become a rallying cry for shareholder activists, who said too many companies like Bank of America had run roughshod over the wishes of their investors. Some of the nation’s largest pensions funds in California, New York and Illinois came out against keeping the jobs together, saying two separate positions would provide more oversight at the bank.

There should be far more shareholder challenges against management. Consider this fact. Twenty years ago today, shares of Bank of America (BAC) closed at $17. Today, the stock is going for about $15.50. Isn’t that worth shaking up?

-

Happy Gann Day!

Posted by Eddy Elfenbein on September 22nd, 2015 at 9:41 amToday is September 22, or Gann Day. What’s Gann Day you ask? Six years ago, Randall Forsyth wrote in Barron’s:

It doesn’t appear on any calendar, but Sept. 22 is known among aficionados of various and arcane market indicators as the day pinpointed by the late technical analyst, W. D. Gann, when markets are more likely to reverse than any other day of the year.

For some reason, stocks, commodities and currencies have a curious tendency to make major tops or bottoms on this day, as Paul Macrae Montgomery points out in a special study edition of Universal Economics newsletter entitled, “A Date Which Will Live in Infamy.”

While it is a bit of hyperbole to equate Sept. 22 with FDR’s characterization of the Dec. 7, 1941 attack on Pearl Harbor, the number of huge reversals that took place on or about that date is stunning.

Montgomery recalls living through the October “massacres” of 1978 and 1979, the crash of 1987, the mini-crash of 1989, the 1997 Asian collapse and the Long-Term Capital Markets plunges, which started to cascade downward in late September. And while gold bullion topped in January 1980, gold stocks made their highs on Sept. 22 of that year, he adds. That date also saw the peak in many oil stocks.

Looking back farther, on Sept. 22, 1929, the Dow Jones Utility Index became the final major average to make its high before the Great Crash. And in 1873, a panic forced the New York Stock Exchange to shut down, Montgomery further details.

And who can forget 2008, when markets went into freefall in the days following the collapse of Lehman Brothers? What’s remembered less well now is the market chaos in the subsequent days after the House of Representatives initially rejected legislation that created the Troubled Asset Relief Program.

Currencies have seen historic changes around this date as well, he adds. The British pound was taken off the gold standard and was devalued a huge 28% on Sept. 21, 1931. Exactly 54 years later, the Group of Five produced the Plaza Accord, which brought a sharp decline in the dollar and expansion of global liquidity. Black Wednesday, when Britain was forced to withdraw from the European Exchange Rate Mechanism, came a few days early on Sept. 16, 1992.

I also recollect that Treasury note and bond yields made their historic highs in late September, 1981, with shorter maturities hitting 17% and long bonds reaching 15%. That marked the end of a 35-year bear bond market from the end of World War II.

Why the apparent coincidence of these market upheavals beginning around Sept. 22? Montgomery posits a possible link to the Autumnal Equinox, which takes place Tuesday afternoon in the Northern Hemisphere. And he also observes an increasing incidence of market reversals around the time of Vernal Equinox in the Spring.

I think it’s all nonsense, but these “facts” are fun. Since that was written, the stock market touched an important low on October 3-4, 2011. Last year, the S&P 500 reached an all-time intra-day high on September 19 and fell sharply until mid-October.

(Via Gary Alexander at Navellier Market Mail.)

-

Morning News: September 22, 2015

Posted by Eddy Elfenbein on September 22nd, 2015 at 7:04 amUK Finance Minister Voices Support For China’s Commitment to Reforms

Hacking Allegations Threaten to Overshadow Xi-Obama Summit

Goldman Has Come Up With (Yet) Another New Name for ‘Smart Beta’

How US Biotech Valuations Got Stretched

Streaming Music Service Deezer Plans IPO to Challenge Spotify, Apple

Oyster to Exit E-Book Subscription Business

Pressure Builds on Volkswagen CEO

Asian Development Bank’s Regional Gloom Deepens

Big Price Increase for Tuberculosis Drug is Rescinded

Apple Presses Ahead With Efforts to Create Car, Though Big Issues Remain

How UBS Spread the Pain of Puerto Rico’s Debt Crisis to Clients

Win or Lose, Bank of America Vote Shows New Shareholder Muscle

What If the Richest Person in Every Country Gave All Their Money to the Poor?

Cullen Roche: The Misguided Interest Rate Obsession

Roger Nusbaum: Fed Day Resolves Nothing

Be sure to follow me on Twitter.

-

Hillary Crushes Biotechs

Posted by Eddy Elfenbein on September 21st, 2015 at 8:41 pmA fairly average day in the market disrupted when Hillary Clinton tweeted this:

Price gouging like this in the specialty drug market is outrageous. Tomorrow I'll lay out a plan to take it on. -H https://t.co/9Z0Aw7aI6h

— Hillary Clinton (@HillaryClinton) September 21, 2015

The market reacted swiftly. Check out the Biotech ETF (IBB):

Don’t feel too bad for biotechs. That ETF is currently at $340. Four years ago, it was going for $94. Biotechs have done incredibly well.

There are a few points to highlight. The first is that anything can impact your stock. The entire biotech sector was hit just from this one tweet.

This is also why I’m leery of stop-losses. Stops can be a useful tool, but bear in mind that you can get knocked out of good positions for silly reasons.

We can also see how one sector can depart from the rest of the market. The overall stock market did fairly well today. Here’s how the ten S&P sectors performed today. See how big the gap is between Health Care and everybody else.

Financials 1.07%

Technology 1.00%

Staples 0.85%

Discretionary 0.75%

Energy 0.57%

Industrials 0.45%

Utilities 0.43%

Materials 0.29%

Telecom 0.26%

Health Care -1.38% -

11 Straight Alternating Weeks

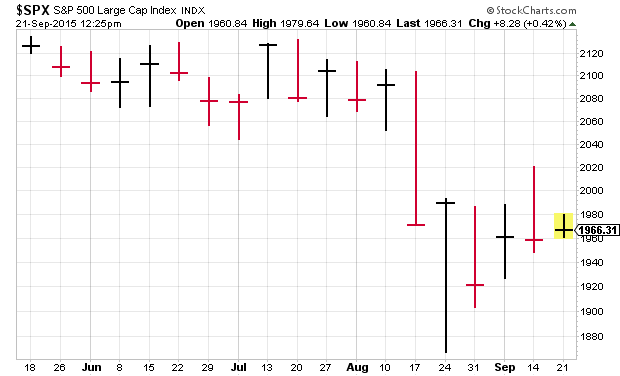

Posted by Eddy Elfenbein on September 21st, 2015 at 12:28 pmIt was a close call, but the S&P 500 closed slightly lower for the week last week. That makes 11 straight “alternating” weeks for the S&P 500.

-

Morning News: September 21, 2015

Posted by Eddy Elfenbein on September 21st, 2015 at 7:08 amChina Beige Book Says Pessimism `Thoroughly Divorced From Facts’

Trading Meat for Tires as Bartering Economy Grows in Greece

Putin Faces Growing Exodus as Russia’s Banking, Tech Pros Flee

Crude Oil Moves Lower After The Fed Does Nothing

Oil Speculators Most Bullish in Two Months as OPEC Calls for $80

Insurance Deals Are Starting to Make Less Sense

Why You Can’t Trust the Advice You Get from Social Security

Volkswagen Drops 23% After Admitting Diesel Emissions Cheat

Bank of America, Funds Lobby Hard to Sway Vote on Moynihan

Lennar Profit and Revenue Beat Expectations as Home Sales, Prices Rise

Dialog Shares Slump After $4.6 Billion Deal to Acquire Atmel

How Warner Bros. Battled Its Way to No. 1 in Video Games

Howard Lindzon: The Fantasy Sports Boom…It’s For Real

Jeff Miller: Has the Fed Assumed a Third Mandate?

Be sure to follow me on Twitter.

-

In Case You Missed It, Here’s What’d You Miss?

Posted by Eddy Elfenbein on September 19th, 2015 at 6:43 pm -

CWS Market Review – September 18, 2015

Posted by Eddy Elfenbein on September 18th, 2015 at 7:08 amThe market is fond of making mountains out of molehills and exaggerating

ordinary vicissitudes into major setbacks.” – Benjamin GrahamFed Decision Day has come and gone, and the Federal Reserve decided to leave rates unchanged. I can’t say that this was a big surprise. It’s what I told you to expect in last week’s CWS Market Review.

The stock market initially rallied after the Fed’s decision. Perhaps investors finally had the clarity they wanted. The S&P 500 rallied as high as 2,020, which, if you’re looking for visibility, certainly sounds like a good number. But it was not to last. Stocks soon turned southward and closed lower on the day.

As proof that the market gods have a sense of humor, or a deep sense of irony, the S&P 500 fell 0.26% on the day the Fed decided against raising rates by 0.25%. Maybe they’re just messing with us?

If there’s one key takeaway from the Fed’s “do nothing,” it’s that the central bank has taken a clear dovish stance. In fact, we might not see a rate increase this year. In this week’s CWS Market Review, I’ll break down what it means for us. We’ll also look at Oracle’s (ORCL) latest earnings report. The House of Ellison beat by a penny, but Wall Street was not pleased with their guidance. I’ll have more in a bit.

We also got a nice 16% dividend increase from Microsoft (MSFT). Later on, I’ll preview next week’s earnings report from Bed Bath & Beyond (BBBY). But first, let’s look at the Fed’s decision to keep 0% interest rates a little while longer.

The Fed Stays at 0%

Ever since China shocked the financial world by devaluing its currency, investors grew doubtful that the Fed would increase rates in September. It wasn’t that long ago that the smart crowd thought Yellen & Co. were about to raise rates for the first time in nine years. James Bullard, the head honcho at the St. Louis Fed, said there’s a better-than-50% chance of a September hike. That was in July!

Nope. The Fed decided not to move. Why? I think the big reason is that inflation simply isn’t there. In fact, this week we got the inflation report for August, and it was the weakest report all year. Prices actually fell!

How can anyone raise interest rates with deflation? It’s not just commodities. “Core inflation,” which excludes food and energy prices, rose by just 0.074% in August. That was also the lowest rate all year. In Thursday’s policy statement, the Fed noted that inflation has consistently trended below their target.

The other reason for the pause is that the Federal Open Market Committee is just that—a committee. I would think that they would want to have broad consensus for their first rate hike since 2006. I think some members are leaning towards a rate hike, but they’re not going to act in a close, especially in opposition to Janet Yellen.

With this week’s statement, there was just one dissenting voice, Jeffery Lacker of the Richmond Fed. If there’s anything that surprised me about the Fed’s policy statement, it’s how “dovish” it was.

The Fed’s statement included this interesting nugget: “Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.” Fortunately, I’m well-versed in econospeak, so I’ll translate for you, “China’s like, wow, a total mess, so commodity prices are dropping like a rock, and that’s going to hold down prices here.”

That’s obviously true, but a lot of observers thought it was interesting that the Fed should comment on global financial activity. But the Fed has a dual mandate—full employment and low inflation.

As I mentioned before, the stock market initially reacted very positively. The S&P 500 broke above 2,000 for the first time in four weeks. The Volatility Index also came crashing down (see chart above). At one point, the VIX dipped below 18. I’ve said that I’m ready to sound the “all clear” once the VIX closes below 20. We’re close. On Thursday, the VIX closed at 21.14, which is its lowest close in four weeks.

The bond market, especially the middle part of the yield curve, was very pleased with the Fed’s news. The two-year Treasury, which is probably the best gauge of Fed policy, dropped 12 basis points on Thursday. The yield fell from a four-year high on Wednesday of 0.82% to 0.70% by the end of the day on Thursday.

Like I’ve been saying in past issues, this decision has been vastly overhyped. For long-term investors, it simply doesn’t mean much. The key takeaways are that rates will be going up soon, probably in December. Maybe early next year. But more importantly, short-term interest real rates (meaning, after inflation) are expected to stay negative for several more months. That’s not just my opinion. That’s the view of both the Fed and the market. According to Thursday’s projections, the Fed sees real interest rates at 0.7% by the end of 2017. That’s still quite low, and it’s more than two years away. That’s a strong positive for stocks.

What to Do Now

We’ve ridden out this storm quite well. The S&P 500 has already made back half of what it lost. Plus, third-quarter earnings season is only a month away, and I expect to see good results for our stocks.

Some stocks on our Buy List, like Hormel Foods (HRL), have barely been dented. Others are recovering quite well. Since August 25, shares of Ford Motor (F) are up 13%. Signature Bank (SBNY) is up close to 10% since September 1.

If you’re looking to put some new money to work, there are a few particularly good bargains on our Buy List at the moment. Cognizant Technology Solutions (CTSH) looks especially attractive below $64 per share. CTSH had a very positive earnings report last month. Snap-on (SNA) is a nice addition if you can get it below $160 per share. My Buy Below on CR Bard (BCR) is $204, but it’s a very nice pick-up below $200 per share. I also really like Express Scripts (ESRX) below $85 per share. I’m not sure how long that bargain will last.

I also want to lower my Buy Belows on two of our stocks. I’m lowering Qualcomm’s (QCOM) Buy Below to $59 per share. I’m also bringing down Moog (MOG-A) to $66 per share. I wanted our Buy Belows to reflect the market’s recent activity. Now let’s look at this week’s earnings report from Oracle.

Oracle Earns 53 Cents per Share

After the bell on Wednesday, Oracle (ORCL) reported fiscal Q1 earnings. The short version is that what’s been happening is still happening. The enterprise software giant earned 53 cents per share for Q1 which was one penny ahead of expectations. That’s down from 62 cents per share for last’s year’s Q1. Still, Wall Street was not pleased.

Once again, the strong dollar was a significant headwind to Oracle’s business. More than half of Oracle’s sales come from outside the U.S. so they’re vulnerable to forex movements. Net sales fell 1.7% to $8.45 billion, but in constant currency terms, Oracle’s sales rose by 7%. That’s how exposed they are to the dollar.

Oracle was late to the game in the cloud business, but they’re closing the gap and they’re doing it fast. Oracle’s cloud sales rose 29% last quarter and 34% in constant currency. Larry Ellison, now the CTO, has stressed that Oracle is close to catching up to Salesforce.com (CRM). Ellison also notes that Oracle should see big profit-margin improvements in its cloud business.

Here’s my take: Oracle has been going through a tough transition period, and we’ve just passed the low point (Q4 was a total disaster). Bookings have been strong for Oracle, and I think we’ll see much better results from them in the future. Similar to our experience with Microsoft, we knew things were going to get better, but we didn’t know when the stock would wake up. With Microsoft, eventually, it did.

On the conference call, Oracle said it sees Q2 earnings, which end in November, ranging between 63 and 66 cents per share and revenue (in constant currency) coming in between -1% and +2%. But they project cloud growth of 50%. Wow! It’s early, but my estimate is that Oracle will earn $2.60 per share this fiscal year.

Oracle’s been a frustrating stock to own. The shares dropped 4% on Thursday, but there are reasons to be optimistic. The current price is a good value (about 14 times this year’s earnings). Oracle remains a buy up to $40 per share.

Microsoft Raises Its Dividend by 16%

Two weeks ago, I told you that Microsoft (MSFT) was soon going to raise its dividend from 31 cents per share. Specifically, I said, “I think they’ll raise it to 34 cents, give or take.” It turned out to be “give.” Microsoft’s board raises the dividend to 36 cents per share. That’s an increase of 16.1%, which is pretty hefty.

Annually, Microsoft looks to pay out $1.44 per share. Going by Thursday’s close, that gives Microsoft a yield of 3.25%. That means Microsoft yields 1% more than a 10-year Treasury. Bear in mind that a 10-year Treasury won’t grow its dividend over the next decade, but Microsoft has bumped up its dividend at a nice clip. Over the last few years, Microsoft has increased its quarterly dividend consistently: 13, 16, 20, 23, 28, 31 and now 36 cents per share. Microsoft remains a very good buy up to $47 per share.

Earnings Preview for Bed Bath & Beyond

Bed Bath & Beyond (BBBY) has been one of the more frustrating stocks on our Buy List. Through Thursday, the shares are down nearly 19% on the year. The company is due to report next Thursday, September 24. I grant the home- furnishings store a lot of latitude since the management team has a superb track record. Still, I try to look at all our stocks realistically.

Three months ago, BBBY reported fiscal Q1 earnings of 93 cents per share. That was OK, but it was not particularly impressive. Sales rose just 3.1%. The metric I prefer to watch is same-store sales, which rose by 2.2%, which was in BBBY’s range of 2% to 3%. Again, pretty blah. The company’s profit margins have been hurt by the use of promotions.

For Q2, BBBY sees earnings ranging between $1.18 and $1.23 per share. Wall Street had been expecting $1.23 per share. The best news is that Bed Bath reiterated its full-year growth forecast. The company expects earnings to rise from flat to mid-single-digits. For clarity’s sake, let’s say that’s 0% to 5%. They also expect same-store sales to grow by 2% to 3%. BBBY made $5.07 per share last year, so this year’s guidance works out to $5.07 to $5.32 per share. Going by Thursday’s close, the shares are trading at 11.6 to 12.2 times this year’s estimate. By that measure, it’s hard to say that BBBY is too pricey.

I’m keeping my Buy Below on Bed Bath at $65 per share. The stock has done poorly, and I think it’s become a good bargain. Of course, with value investing, finding companies with dings and scratches is part of the game. But I want to see evidence of better sales growth in next week’s report.

That’s all for now. Now that Fed Day has passed, you can expect the market to chill out. In fact, daily volatility has already declined. On Monday, we’re going to get the report on existing home sales and the new-homes sales report will be on Thursday. Also on Thursday, we’ll get reports on durable-goods orders and initial unemployment claims. Initial claims have been below 300,000 for 28 straight weeks. On Friday, we’ll get the second revision to Q2 GDP. The initial figure was 2.3%, which was revised up to 3.7% in August. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 18, 2015

Posted by Eddy Elfenbein on September 18th, 2015 at 6:22 amCan Germany Beat the U.S. to the Industrial Internet?

Federal Funds Rate Unchanged: What Does It Mean for Investors?

House Democrats Keep Door Open to Crude Exports, Seek Sweeteners

An Unexpected Disruptor? Verizon’s Bold Digital Strategy

Deutsche Bank to Pull Investment-Banking Operations Out of Russia

Bitcoin Is Officially a Commodity, According to U.S. Regulator

Social Business In The Background At Dreamforce

Perrigo Board Unanimously Rejects Mylan’s Unsolicited Exchange Offer As Inadequate

Texas Instruments Sets $7.5 Billion Buyback Plan, Raises Dividend

GE to Expand Aviation Operations Overseas Amid Ex-Im Bank Debate

Drahi Wants More U.S. Cable Deals After Buying Cablevision

Alibaba’s Wipeout Leaves Investors Questioning What Comes Next

Be sure to follow me on Twitter.

-

How the New York Stock Exchange Works

Posted by Eddy Elfenbein on September 18th, 2015 at 4:44 am

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His