-

Optimistic Beige Book

Posted by Eddy Elfenbein on June 3rd, 2015 at 2:20 pmThe Fed’s “Beige Book” report is one of those wonky things put out by the Fed that’s actually fairly interesting. The one that came out today had mostly good things to say about the economy.

The informal survey of anecdotal business contacts’ views is conducted by each of the central bank’s 12 regional districts, and paints a fairly rosy picture of the outlook. The latest beige book report finds “overall economic activity expanded during the reporting period from early April to late May.”

Growth was characterized as “moderate” in the Chicago, Richmond, Minneapolis and San Francisco districts; “modest” in New York, Philadelphia and St. Louis regions; mixed in the Boston district; “slight” in Cleveland and Kansas City; holding steady in Atlanta; and slowing “slightly” in Dallas. The latter could be associated with falling business spending in the energy sector.

In a hopeful sign for the housing market, the Fed reported “residential and commercial real estate activity and construction improved since the last report.”

Overall loan demand increased, the report said, particularly in the New York district.

-

Quiet Rotation Today

Posted by Eddy Elfenbein on June 3rd, 2015 at 1:02 pmThe big jobs report comes out Friday but we got a sneak preview this morning. ADP said that the economy created 201,000 private sector jobs last month. For Friday’s report, the consensus on Wall Street is for 220,000 net new jobs.

Also, the Department of Commerce reported that the trade deficit fell to $40.9 billion in April. That was less than consensus. Bill McBride notes that exports are 14% higher than their pre-recession peak, while imports are right at their pre-recession peak.

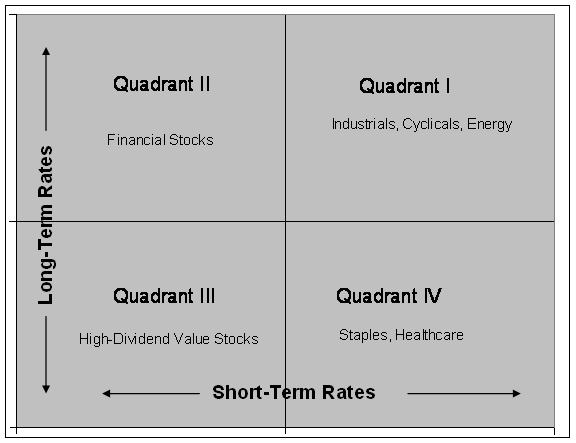

This is an interesting day in the markets and it’s a continuation of what I discussed before; interest rate-sensitive stocks are lagging. This is a classic Quadrant I day. Industrial cyclicals are up, especially transports. The top-performing sector so far today is trucking.

What’s interesting is that the broader market is up modestly so it’s masking the dramatic rotation that’s happening under the surface.

-

Morning News: June 3, 2015

Posted by Eddy Elfenbein on June 3rd, 2015 at 7:07 amOECD Gives Global Economy ‘B Minus’ As Cuts Forecast

OECD Calls US Dip A Blip But Chops World Growth Forecast

Greece in Last-Ditch EU Talks To Break Debt Deadlock

The Secret Money Behind Vladimir Putin’s War Machine

US Congress Pushed China Into Launching AIIB, Says Bernanke

Korean E-commerce Leader Coupang To Raise $1 Billion From SoftBank At $5 Billion Valuation

Amazon Debuts Free Shipping on Small Goods, No Minimum Order

In Bid to Cut Costs, J.P. Morgan Cuts Voicemail For Some Employees

Fitbit IPO Could Top $500 Million When it Makes NYSE Debut

Perrigo Plays European Defense

Huffington Post In Limbo At Verizon

Deutsche Bank Partners With Microsoft, HCL, IBM in Tech Lab Launch

Cullen Roche: Does A “Liquidity Trap” Ever End?

Jeff Miller: How To Think About Risk

Be sure to follow me on Twitter.

-

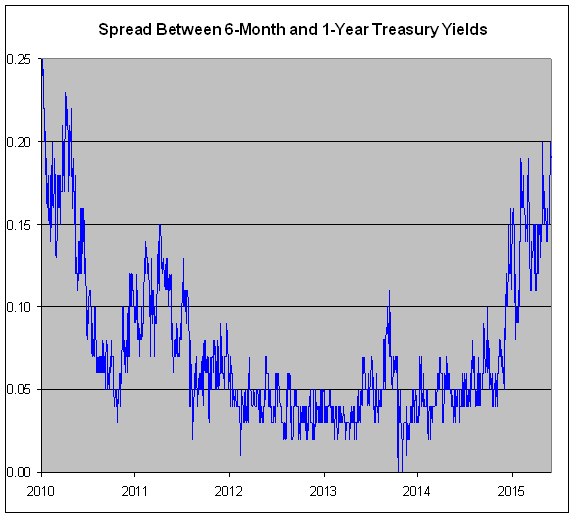

6-Month/1-Year Spread Rises

Posted by Eddy Elfenbein on June 2nd, 2015 at 6:27 pmThe spread between the six-month and one-year Treasury yields recently hit 0.20% for the first time in more than five years. That’s up from four basis points in November.

This is yet another sign that the market thinks higher rates are coming soon.

The one-year Treasury closed today at 0.26% while the six-month bill stood at 0.07%. That implies that the six-month bill will yield 0.45% six months from now.

-

Auto Sales Reach 10-Year High

Posted by Eddy Elfenbein on June 2nd, 2015 at 3:37 pmU.S. auto sales were very strong last month:

The U.S. auto industry remained on track for the best sales year in almost a decade as consumers bought cars and trucks at the fastest monthly pace since early 2006.

Sales of pickup trucks and SUVs in May again led the way, which bodes well for profit margins of the major automakers. Consumers are shying away from cars and snapping up trucks and sport utility vehicles as the national average price of gasoline, at $2.75 a gallon, is nearly a dollar less than at this time last year.

As has been the case since the 2008-2009 recession, the auto industry’s recovery continues to outpace that of the overall economy, which is on course to grow 0.8 percent in the second quarter, according to Federal Reserve forecasts.

Consumers are finding it easier to obtain auto loans – another factor in boosting sales, analysts have said. Experian reported the average length of U.S. loans for new and used vehicles in the first quarter hit record highs, and nearly 30 percent of new-vehicle loans have payback periods longer than six years.

This probably represents a rebound from the cold winter. Sales at Ford (F) dropped by 1.3% (Wall Street had been expecting a bigger drop), and the F-Series trucks fell by 10%. Demand is still high for the F-150 as Ford is ramping up production.

-

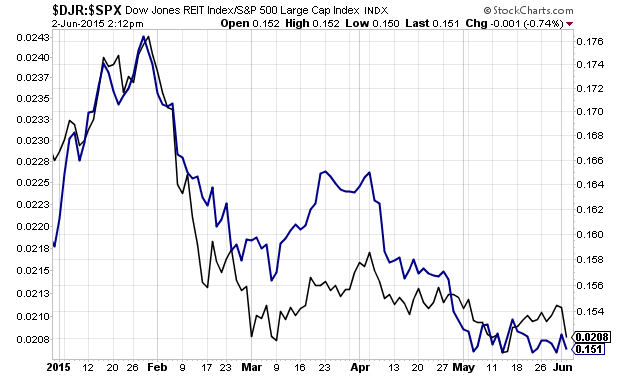

Tough Times for Dividend Stocks

Posted by Eddy Elfenbein on June 2nd, 2015 at 2:16 pmThe WSJ recently noted that high-dividend stocks have been losing out in the market recently. Utility stocks badly lagged the market in February and haven’t done much since. REIT stocks, which tend to have generous yields, have followed a similar path.

Utilities, real-estate investment trusts and master limited partnerships have been lifted since the financial crisis by a flood of money from portfolio managers and retirees starved for steady investment income amid low bond yields. Investors plowed $48.4 billion into mutual and exchange-traded funds tracking utilities and REITs from 2010 through 2014, according to Morningstar Inc.

But portfolio managers are pulling back from these shares in 2015, as the prospect of the first short-term interest-rate increase by the Federal Reserve in nine years makes high-dividend stocks less attractive. Investors reason that higher rates will boost the payout—and therefore the appeal—of more stable income-paying investments, like government and corporate debt.

Check out this chart. This shows the REIT index divided by the S&P 500 (in blue) along with the utility index divided by the S&P 500 (in black).

This is a good example of what I described two weeks ago in my “Elfenbein Theory” on the market. What we’re seeing is an anti-Quadrant III rotation.

The underlying message of this rotation is that the market is preparing itself for higher interest rates.

-

Morning News: June 2, 2015

Posted by Eddy Elfenbein on June 2nd, 2015 at 7:13 amGreece Calls on Lenders to Accept ‘Realistic’ Plan Sent on Monday

Paul Krugman: That 1914 Feeling

Raghuram Rajan: We Are Under No Illusion That The Economy Is Up And Running

Justices Curb Bankruptcy Filers’ Ability to Have Second Mortgages Canceled

The Potential $1.5 Trillion Stimulus Plan Investors Are Missing

Manufacturing Growth Speeds Up for First Time in 6 Months

Seeking Rate Increases, Insurers Use Guesswork

For UAW Members, Two-Tier Wage Issue Is Personal

Mega Deals Send Merged Companies Up the Ranks of World’s Largest

Intel Agrees to Buy Altera for $16.7 Billion

Ford to Make 40,000 More Vehicles By Cutting Summer Downtime

Takata Says It Will No Longer Make Side Inflater Linked to Airbag Defect

Pinterest Just Revealed How It Is Going To Start Making Some Serious Money

Jeff Carter: All Markets Are Frothy

Roger Nusbaum: Working In Retirement Is A Hope?

Be sure to follow me on Twitter.

-

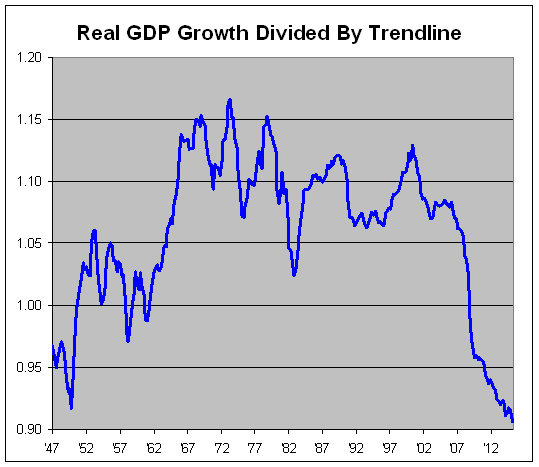

The Trendline of Real GDP

Posted by Eddy Elfenbein on June 1st, 2015 at 3:24 pmFriday’s GDP report was not a good one. The government revised its estimate of Q1 GDP growth to non-growth, down 0.7%. In the 23 quarters of expansion, this is the third time growth has been negative. They’ve all been Q1s.

This expansion has been far below average. In the last 23 quarters, the economy has averaged 2.2% annualized growth. The economy used to average 4% or 5% growth during expansions followed by -2% or 3% in sharp pullbacks during recessions. Now it’s sluggish growth all the time.

Here’s a good way of expressing just how poorly the economy has done. This is real GDP and I divided it by a trendline that grew at a constant rate of 3.28% per year.

It’s been 15 years since the economy expanded faster than its long-term growth rate. To be fair, I think slower population growth also plays a role.

-

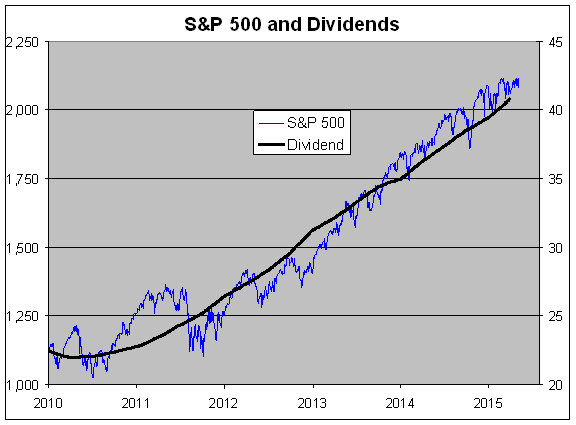

The Dividend Bull Market

Posted by Eddy Elfenbein on June 1st, 2015 at 10:54 amI get annoyed at much of the sloppy talk about the stock market incessantly being “in a bubble.” Here’s Robert Shiller making yet another noncommittal forecast. It seems sophisticated to say that stock prices are too high when in fact, true bubbles are quite rare.

Here’s another way to look at the current market. This is the S&P 500 (blue, left) along with its dividends (black right). I scaled the two lines at a ratio of 50-to-1. In other words, whenever the lines cross, the S&P 500’s dividend yield is exactly 2%.

The chart shows that the market has tracked a 2% dividend yield for a few years. My point is that this has been a bull run in dividends as much as it’s been one in stock prices. That, it seems, rarely gets mentioned.

The stock line runs through May but I don’t have the Q2 data point yet for dividends. But I expect it will be a continuation of the trend.

Let me be clear on two points. I’m not saying that dividends are the only measure of valuation, nor am I saying that 2% is some platonic fair value. But dividends have the benefit of being steady and reliable. You’re never quite sure how much money a company has earned, but you do know exactly how much they’ve paid out in dividends.

If there’s any distortion, it may be to the low side since the Federal Reserve must approve capital allocation plans for major banks.

-

May ISM = 52.8

Posted by Eddy Elfenbein on June 1st, 2015 at 10:20 amThis morning, the May ISM index came in at 52.8. That’s a bit above expectations. It’s also the first monthly increase since October.

Construction spending rose 2.2% in April to hit $1 trillion. That’s the highest in six years.

The BEA also said that personal income rose 0.4% in April. Spending was flat. That means Americans are saving a little more.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His