-

The Long View for Stocks

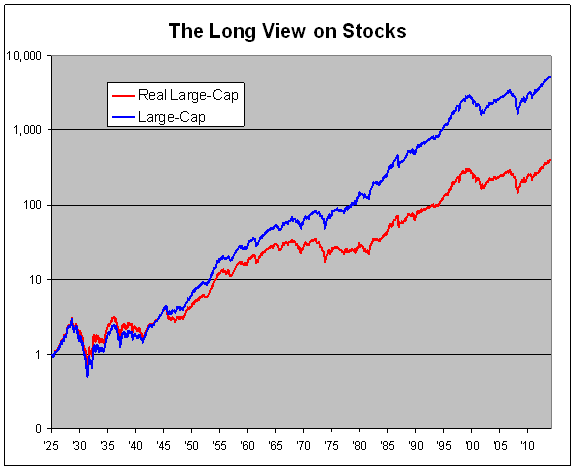

Posted by Eddy Elfenbein on January 22nd, 2015 at 1:21 pmIbbotson Associates is known for their collection of long-term financial returns data. Their latest yearbook isn’t out yet, but I was able to bring the data up to date by using numbers from Standard and Poor’s.

Here’s what the chart looks like of long-term stock returns from December 31, 1925 to December 31, 2014.

The blue line is stocks and dividends but is not adjusted for inflation. Starting with $1, it turns into $5,300 by the end of 2014. That’s an annualized total return of 10.12%.

The red line is the blue line adjusted for inflation. Stocks have averaged a total real return of 6.98% annualized over the last 89 years. That’s roughly stocks doubling in real value every decade.

Of course, there’s a lot of variation in that. Over the last 15 years, real stock returns have averaged less than 2% per year.

Jeremy Siegel often talks about how stocks have returned 7% in real terms over the long haul. I’ve even heard this referred to as the Siegel Constant.

Personally, I don’t think investors should expect 7% real returns going forward. The problem with this past data is that it’s based on the American Century. I’m still a long-term bull but we can’t replicate the success of 20th Century America.

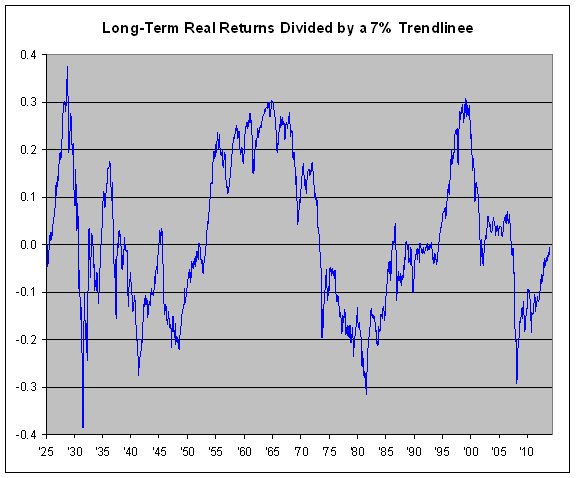

Now let’s have more fun with the data. I took the red line and divided it by a 7% trend line, meaning a line that just rises by 7% per year, every year. So when we divide the two, it means that whenever the line is rising, stocks are outperforming their long-term average. When it’s falling, they’re trailing it. (Even a mildly declining line is still making money for you.) I then made it a logarithm chart so it would be easier to read. Here’s what I got:

A few thoughts: First, notice how cyclical the chart is. Stocks don’t return 7% per year consistently. Rather there are long periods of outperformance followed by long stretches of underperformance.

Second, the 1949 to 1956 bull market was one of the greatest in history. No one talks about that one. I think it’s because it never crashed.

Third, the 1929, mid-1960s and 2000 peaks are all roughly similar. The mid-1960s peak was a rolling one. Things didn’t really fall apart until the 1973-74 crash.

Similarly, the 1932, 1982 and 2009 troughs aren’t too far apart.

Fourth, 1929 to 1932 sucked. Seriously.

Fifth, as strong as the last six years have been for stocks, we’re merely back to our long-term average. Actually, we’re still a bit short of it. Stocks would have to gain about 20% in 2015 for us to be back at the mid-point.

Finally, if you use a little imagination, this chart somewhat resembles the long-term chart of P/E Ratios. This makes sense since earnings have tended to increase at a fairly steady pace over the long haul. Not quite like a 7% trend line, but not too far off, either.

-

Morning News: January 22, 2015

Posted by Eddy Elfenbein on January 22nd, 2015 at 7:14 amDavos 2015: Banks Call For Free Rein to Fight Cyber Crime

Draghi Is Pushing Boundaries of Euro Region with QE Program

The Drivers And Implications Of The Bank Of Canada’s Oil-Driven Rate Cut

Fed Officials Reassess U.S. Outlook Amid Global Weakness

Speculators Looking for Havens from Slowing Growth are Piling Into Silver

Talk of Wealth Gap Prods the G.O.P. to Refocus

‘Fast Money’ Recap: eBay Could Be Undervalued but Not After PayPal Spinoff

American Express To Slash 4,000 Jobs On Heels Of Strong Quarter

Kinder Morgan: A Splendid Quarter To Kick Off A New Era

Uber Raises Another $1.6 Billion With Convertible Debt Sale

Netflix Soars Most Since April 2013 on Profit Talk, Rollout

Hyundai Motor’s Biggest-Ever Dividend Greeted With Outlook Concern

EBay’s Breakup Plans May Open Door for e-Commerce M&A

Joshua Brown: The Riskalyze Report: Advisors Spread the Wealth

Jeff Carter: What To Do About Dead Equity On The Cap Table

Be sure to follow me on Twitter.

-

eBay Earned of 90 Cents per Share

Posted by Eddy Elfenbein on January 21st, 2015 at 4:54 pmAfter the closing bell, eBay ($EBAY) reported Q4 earnings of 90 cents per share. That was one penny better than expectations. Three months ago, eBay said that Q4 earnings would range between 88 and 91 cents per share. For all of 2014, eBay earned $2.95 per share. That compares with $2.71 per share in 2013.

Now the bad news. For Q1, eBay said they expect earnings to range between 66 and 71 cents per share. Wall Street had been expecting 76 cents per share. They expect full-year 2015 earnings of $3.05 to $3.15 per share.

The stock is up a bit after hours. Why? The company announced layoffs of 2,400 jobs in order to get ready for the PayPal spinoff. This isn’t really news since the company had already said that layoffs were planned. Today is the day we got the details. But eBay had other news:

EBay also said it would be exploring strategic options for eBay Enterprise, including a sale or initial public offering.

“Enterprise is a strong business,” the company said, but “it has become clear that it has limited synergies with either business and a separation will allow both to focus exclusively on their core markets.”

The company also announced today that it has entered into a standstill agreement with investor Carl Icahn , the company’s largest active shareholder. In addition to certain corporate governance provisions to be adopted by PayPal as an independent company at the time of its spin-off from eBay, the agreement also appointed Icahn Capital executive Jonathan Christodoro to eBay’s current board.

Mr. Icahn, in a statement on its website, said the corporate governance provisions includes limits on any so-called poison pills and prevents a staggered board at PayPal. The provisions were aimed at giving shareholders a greater ability to weigh in on any offers made for the company.

“In the end, it should be the shareholders’ decision. This fundamental belief was the underlying philosophy of many of the corporate governance principles for which we advocated at PayPal,” Mr. Icahn said. “We applaud eBay’s board for making this agreement possible.”

Icahn pushed for this spinoff and he was right. eBay is up 2.66% in after-hours trading.

-

The Super Bowl Indicator

Posted by Eddy Elfenbein on January 21st, 2015 at 2:21 pmFrom Gary Alexander at Navellier Market Mail:

Will Seattle Save the Stock Market Again This Year?

Last January, the S&P fell 3.56%, but then Seattle saved the market. On Sunday, February 2, the Seattle Seahawks (the NFC Super Bowl team) thrashed Denver (the AFC team), 43-8. The market immediately turned around. The S&P gained 4.31% in February, erasing all of its January losses, eventually delivering double-digit gains for all of 2014. From Super Bowl Sunday to New Year’s Eve, the S&P gained 15.5%!

The Super Bowl Indicator basically says that the market will go down in a year in which the AFC team wins, and it will go up if an “old-line NFL” team wins. Being from Seattle, I hope our team wins the first back-to-back Super Bowl victories in a decade (since New England turned the trick in 2004-5 – which were both good market years, by the way). But I know better than to mix football and stock analysis.

The first problem with the Super Bowl Indicator is the squishy term “old line NFL.” Seattle is in the NFC now, but it was in the AFC for most of its tortured path to football supremacy. Seattle joined the National football conference in 1976, but then it struggled in the AFC from 1977 to 2001 before rejoining the NFC.

This kind of tortured team history is now common in the NFL. Some other recent Super Bowl winners are currently aligned with the AFC but they are also old-line NFL teams: The Indianapolis Colts (2007 winners) were once the Baltimore Colts, while the Baltimore Ravens (the 2013 champs) were once the Cleveland Browns. The Pittsburgh Steelers (winners in 2006 and 2012) are also from the old-line NFL.

The statistical secret of this correlation is that the stock market goes up more than it goes down. Since 1967 (Super Bowl 1), the Dow has risen in 35 of 48 years. In the first 48 Super Bowls, an “old-line NFL” team won 34 contests, so there is bound to be a lot of overlap. But the statistical reality is that if a coin comes up heads 30 of 31 times, the chances it will come up heads on the next toss will always be…50%.

-

RIP: Melvin Gordon

Posted by Eddy Elfenbein on January 21st, 2015 at 12:31 pmMelvin Gordon has died at the age of 95. He was the CEO of Tootsie Roll ($TR).

People are often surprised that Tootsie Roll is its own stock. They assume it’s owned by major corporation like Cadbury or Hershey. Nope, Tootsie is all by itself and Melvin Gordon was its CEO for 53 years.

The stock was actually a strong performer for many years. It rallied from 20 cents per share in 1980 to $30 by 1998. Since then, it hasn’t done much. It’s mostly rallied up and down between $20 and $30 per share. Tootsie has also issued 3% stock dividends every year for the last 17 years (I believe that’s correct).

Still, I have a special place in my heart for small, oddball companies that do their own thing. I’ll miss you, Melvin.

-

Morning News: January 21, 2015

Posted by Eddy Elfenbein on January 21st, 2015 at 7:08 amCentral Banks Dominate FX Price Action

Is Draghi About to Massively Misfire?

May You Live In Interesting Times – Central Banks On The Loose In 2015

U.K. Zero Inflation Threat Quashes BOE Rate Dissent: Economy

Netflix Shares Surge on Subscriber Growth

The Secret to Amazon’s Success is Streaming TV

Xiaomi Threatens Samsung’s Market Position in Chinese Low-End Smartphone Market

Samsung Drops Qualcomm Chip From Next Galaxy Smartphone

UnitedHealth Earnings Rise 6%, Top Wall Street Expectations

Wal-Mart Launches Cash Pickup Option for Tax Refunds

Morgan Stanley’s Results Miss Estimates

Johnson & Johnson Facing Headwinds From A Stronger Dollar

BHPB Pumping Iron – But Also Oil

Joshua Brown: There’s More to Life Than The S&P 500

Roger Nusbaum: Weekly Market Review – Week Ending 1/16/2015

Be sure to follow me on Twitter.

-

September Fed Funds Futures

Posted by Eddy Elfenbein on January 20th, 2015 at 5:55 pmJust to show you how much things have changed, here’s a chart of the September 2015 Fed funds futures contract (click on the chart for a larger version)

Not that long ago, the market thought the Fed would have interest rates at 0.5% (99.50 on the chart) by this September. Now they think the Fed will be at 0.25% by September.

-

Ritholtz on Forecasting

Posted by Eddy Elfenbein on January 20th, 2015 at 12:22 pmGreat column by Barry Ritholtz and the absurdity of forecasting:

Economists, market strategists and analysts alike suffer from an affinity for making big, frequently bold — and most often, wrong — pronouncements about what is to come. This has a pernicious impact on investors who allow this guesswork to infiltrate their thinking, never for the better.

I have been beating this drum for more than a decade. What say we finally put a fork in Prediction, Inc.?

There is a forecasting-industrial complex, and it is a blight on all that is good and true. The symbiotic relationship between the media and Wall Street drives a relentless parade of money-losing tomfoolery: Television and radio have 24 hours a day they must fill, and they do so mostly with empty-headed nonsense. Print has column inches to put out. Online media may be the worst of all, with an infinite maw that needs to be constantly filled with new and often meaningless content.

Just because the beast must be fed does not mean you must be dragon fodder.

-

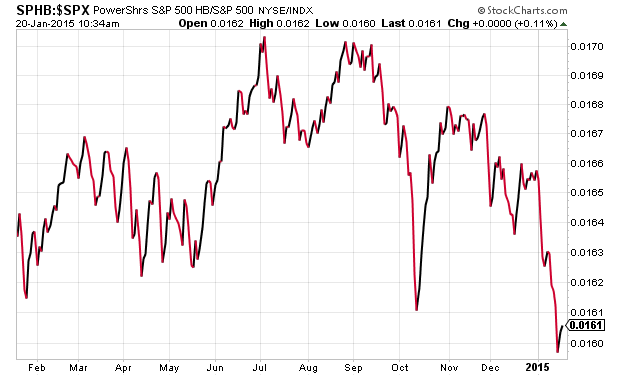

High Beta Pain

Posted by Eddy Elfenbein on January 20th, 2015 at 11:06 amStocks with higher betas have been lagging badly this year. They’re doing a little better today, but it’s been a rough ride since September. Here’s the High Beta ETF ($SPHB) divided by the S&P 500.

-

Denmark Goes More Negative

Posted by Eddy Elfenbein on January 20th, 2015 at 10:49 amThe dramatic move by the Swiss National Bank shook up currency traders. Now it’s Denmark’s turn. After all, they face the same pressures from the ECB. The Nationalbank, Denmark’s Fed, cut rates on CDs to -0.2% from -0.05%.

Both the Swiss and Danish authorities, trying to keep their currencies — and exports — globally competitive, acted pre-emptively before a meeting of the European Central Bank on Thursday in Frankfurt. At that meeting, the bank’s policy makers are widely expected to announce a program of large-scale bond buying, an action that could further push down the value of the euro, which has been weakening for months.

A weakening euro has the effect of making other European currencies, like the Swiss franc and Danish krone, relatively stronger — which effectively raises the prices of products priced in francs or kroner on the global market.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}