-

Growth Takes the Lead

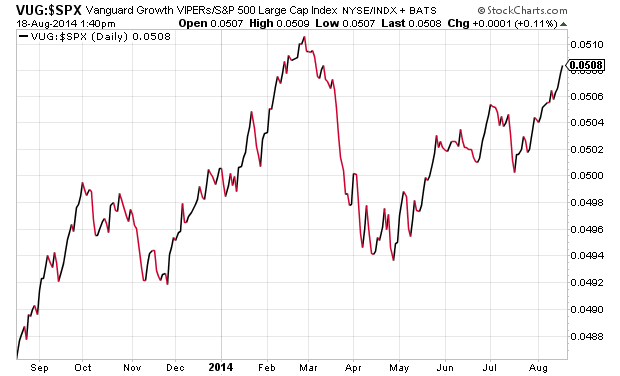

Posted by Eddy Elfenbein on August 18th, 2014 at 1:52 pmIn March and April of this year, the stock market sharply turned against Growth stocks in favor of Value stocks. Bear in mind, we’re talking about relative strength, not absolute performance. Lately, however, Growth stocks have taken the lead again.

Here’s a look at the Vanguard Growth ETF ($VUG) divided by the S&P 500.

Growth has beaten the market consistently since mid-July.

-

Stock Prices and the Titantic Theory

Posted by Eddy Elfenbein on August 18th, 2014 at 1:37 pmAs I’ve written before, I’m not a fan of Robert Shiller’s “CAPE” valuation metric, which is the stock market’s P/E ratio based on the last ten years of earnings. I don’t see why we need to go back that far. Also, the CAPE has been above average almost consistently for the last 20 years. A good rule of thumb is that if some valuation metric reveals a big mispricing, the problem probably lies with the metric, not the price. In this weekend’s New York Times, Professor Shiller writes on stock market valuations:

It’s possible that bond prices account for today’s stock market valuations. But that raises another question: Why are bond prices so high? There are short-term explanations: the role of central banks, for example. But is there a compelling reason for prices of stocks and bonds (and maybe houses, too) to remain high indefinitely?

I’ve looked for untraditional answers. Perhaps today’s prices have something to do with anxiety about the future. I suspect that after the financial crisis, working people are much more worried about their future pay. Many are concerned that they might lose their jobs to cost-cutting, or that they might eventually be replaced by a computer or robot or website. Such anxiety might push them to try to make up for these potential shortfalls by investing in stocks and bonds — even if they worry that these assets are overvalued.

Extrapolating from a theory of Robert E. Lucas Jr. of the University of Chicago, one might well expect lofty stock prices amid such worries: When there aren’t enough good investing opportunities, people wishing to save more for the future may succeed only in bidding up existing assets even if they think they’re overpriced. Call it the “life preserver on the Titanic” theory.

This explanation, though, is probably not the whole story. The problem, as shown in my work with Sanford Grossman, founder of QFS Asset Management, and in work by Lars Peter Hansen of the University of Chicago and Kenneth Singleton of Stanford, is that the market just moves up and down more than Professor Lucas’s theory would suggest.

So nothing I’ve come up with is a slam-dunk explanation for the continuing high level of valuations. I suspect that the real answers lie largely in the realm of sociology and social psychology — in phenomena like irrational exuberance, which, eventually, has always faded before. If the mood changes again, stock market investments may disappoint us.

I don’t accept the notion that stock prices are elevated. For one, the market’s dividend yield is near 2% as it’s been for the last decade (except for the worst of the financial crises). The stock market’s one-year P/E Ratio has been fairly stable over the last 15 months. That may come as a shock to many people, but it’s true.

Consider that the S&P 500 is up 6.65% so far this year and earnings are projected to grow 11.14%. The calendar year is 63% over which means valuations are basically the same now as they were at the start of the year.

-

Quick Hits

Posted by Eddy Elfenbein on August 18th, 2014 at 10:25 amHere are three quick updates to some of our Buy List stocks.

In the last CWS Market Review, I talked about Fiserv (FISV) being the first Buy List stock to recover and make a new all-time high. That just happened. The shares have been as high as $63.22 today.

Renaissance Technologies, the famous hedge fund outfit, started a new position in Bed Bath & Beyond (BBBY). In late July, BBBY topped $64 per share, which was up nearly $10 from its big low in June. The stock pulled back again but held at $61 and is now quietly drifting higher.

Last week, Moog (MOG-A) announced that it’s expanding its share buyback program. The company said it’s going to buy back four million shares this year. Now it’s adding another five million to that figure. Moog’s CEO said, “Given our continued strong cash flow we believe continuing our buyback program in 2015 is a prudent use of capital and will create further value for our shareholders. In addition to our buyback program, we will continue our R&D investments to drive organic growth and look for adjacent acquisitions which complement our organic strategy.” I’ve been down on Moog recently, but this is good news.

-

The S&P 500 Jumps Above 1,965

Posted by Eddy Elfenbein on August 18th, 2014 at 9:47 amThe stock market is up again today. The S&P 500 has been as high as 1,966 this morning, and it’s not that far from its all-time closing high of 1,987.

The larger story is that a decent earnings season was hurt by several troubling geopolitical events. Now it appears that tensions are falling, especially in Gaza and Ukraine.

We had some very good economic news on Friday when the Federal Reserve said that Industrial Production rose by 0.4% last month. That was twice the rate economists were expecting. In the last year, Industrial Production is up by 5%, and since the recession low, it’s up about 25%.

-

Morning News: August 18, 2014

Posted by Eddy Elfenbein on August 18th, 2014 at 9:06 amGlobal Central Bankers Out of Sync, Head to Jackson Hole

Yellen Dashboard Warning Light Glows as Millions Work Part Time

Why Draghi’s Cheap Cash Offer to Banks May Lack Appeal

EU Offers $167 Million Produce Aid After Russia’s Ban

Thai GDP Grows in Second Quarter

China Home Prices Fall for Third Straight Month in July

Apaache Makes Big Oil Find Off Western Australia

Palladium Advances to a 13-Year High as Gold Declines

Dollar General Makes Rival Bid for Family Dollar Stores

China Finds Mercedes-Benz Guilty of Price Fixing

Sensata Technologies Announces The Acquisition Of Schrader International

Ingersoll-Rand Buys Cameron Unit for $850 Million

More Than One-Third of Americans Have No Savings

Credit Writedowns: Abenomics – What Could Possibly Go Wrong?

Jeff Miller: Weighing the Week Ahead: Time for the Central Bankers to Unwind?

Be sure to follow me on Twitter.

-

CWS Market Review – August 15, 2014

Posted by Eddy Elfenbein on August 15th, 2014 at 7:05 am“Carpe diem. Seize the day, boys. Make your lives extraordinary.”

– Dead Poets SocietyThe stock market’s July swoon sure didn’t last long. From closing high to closing low (July 24 to August 7), the S&P 500 lost a grand total of 3.94%. That small bit of turbulence unnerved a lot of folks who should have known better. But since there’s been so little volatility of late, that minor dustup seemed larger than it truly was.

Last week, the Russian military called off some exercises near the Ukrainian border. I can’t say those exercises specifically caused the market’s tumble, but ever since they ended, the stock market has rallied. The S&P 500 has advanced in four of the last five sessions, and we’re not too far from another new high. Since August 7, the S&P 500 has gained 2.39%. Another sign that tensions have chilled out is that small-cap stocks have led the bounce-back rally, and the VIX is back down again.

Now that second-quarter earnings season is past us, this is a good time to run through all 20 stocks on our Buy List and review their prospects for the rest of the year. I’ll also take a look at the recent bond market rally. Long-term yields have been dropping, and I think the time has finally come for bonds to take a rest. We’ll also preview two Buy List earnings reports for next week. But first, let’s look at the stretched market for bonds.

It’s Time for Bonds to Sit Down

As well as the stock market’s done lately, the bond market has been a rock star this year. The yield on the 10-year Treasury closed at 2.40% on Thursday. That’s a 14-month low. If you had told me on New Year’s Day that the 10-year would go for 2.40% by August, I would have thought you were out of your mind. The yield has dropped more than 60 basis points since the start of the year.

It’s interesting how few people saw this big bond rally coming. Jeffrey Gundlach, the bond kingpin, was one of the few who got it right. There seems to be an insatiable appetite for all things bond. This week, the Treasury auctioned off some 30-year bonds, and yields were the lowest in more than a year.

Why the demand for fixed-income? I think this represents misplaced concerns about stock prices. Given where we are in the economy, it’s safe to say that the bond rally has run too far. The idea that investors are willing to lock in their capital for 10 years to get a measly 2.4% seems a bit crazy to me. That’s almost exactly what the stock market has gained in the last five years.

Several of our blue-chip Buy List stocks yield more than the 10-year, such as Wells Fargo ($WFC), Ford ($F) and Microsoft ($MSFT). Not only do they yield more, but they’re also thriving businesses. As much as I love bonds, they just sit there.

You can really see the absurdity of the bond market by looking at the TIPs—the inflation-protected bonds. The 10-year TIP currently yields 0.2%. That’s down from 0.8% late last year. I understand why investors are nervous about stocks, but I don’t see why anyone would invest in a bond that barely beats inflation for the next 10 years. In 2012 and 2013, the 10-year TIPs turned negative, but the fear was more understandable, given the dramatic events in Europe. The 10-year Spanish bond now yields less than American bonds. In Germany, the 10-year bond dropped below 1%. The 1% Club is very exclusive; the only other members are Japan and Switzerland.

Thanks to improved economic numbers, we can expect long-term yields to drift higher as the year goes on. By this time next year, the Federal Reserve may have already started raising interest rates. Now let’s take a look at our Buy List.

Rundown of the Buy List

I was puzzled by the market’s negative reaction to AFLAC’s ($AFL) Q2 earnings report. I thought the earnings were fine. After all, they beat expectations by seven cents per share, but the shares fell as low as $58.50, and two weeks ago, I said the stock was an especially cheap buy below $60. The good news is that AFLAC ticked up above $60 per share on Thursday. AFLAC remains a good buy up to $66 per share.

Bed Bath & Beyond ($BBBY) continues to recover, but unevenly. BBBY broke above $64 per share in late July. That’s nearly $10 more than its July low. Investors clearly overreacted to BBBY’s bad news. Remember that this is one of our off-cycle stocks, so they’ll report their Q2 earnings in about six weeks. They see Q2 earnings ranging between $1.08 and $1.16 per share. That’s not bad. Bed Bath & Beyond remains a good buy up to $65 per share.

Last week, I mentioned that CA Technologies ($CA) was in danger of being knocked off next year’s Buy List. I’m free to change my mind before then, but I need to see more signs of improvement from CA. The part I really like is the generous yield. Going by Thursday’s close, CA yields 3.52%, but I’m not crazy about them. CA Technologies is a moderate buy up to $31 per share.

Cognizant Technology ($CTSH) seemed to be our only bomb from last earnings season. Now that I’ve looked at the numbers, I’m not worried about CTSH at all. I apologize if you were caught in the sell-off, but the company is still doing well. If you don’t own CTSH, this is a good time to start a position, especially if you can get it below $45 per share. Cognizant Technology remains a good buy up to $48 per share.

CR Bard ($BCR) is one of those quiet stocks that you tend to forget about because they’re so quiet. That’s unfair, because this is a solid company. Bard beat earnings last month and raised their full-year guidance. They now expect $8.25 to $8.35 per share for the full year. I held off on changing our Buy Below on Bard, but I think this is a good time for an increase. I’m raising our Buy Below on CR Bard to $160 per share.

I also mentioned DirecTV ($DTV) last week as a possible deletion from next year’s Buy List. The difference is that I love DTV. It’s the AT&T deal that makes them less attractive as an investment. Their business continues to do well. I’ll let you know as we hear more about the AT&T deal. My decision will come down to how close the shares are to $95 by year’s end. There’s no point in holding on to a stock for a few more percent. Until then, DTV is a buy up to $95 per share.

eBay ($EBAY) got knocked around for most of the spring. I’m pleased to see the shares are making their way back. They beat earnings by a penny per share last month, and the stock has continued to rally. eBay sees full-year earnings ranging between $2.95 and $3.00 per share. I’m going to keep a tight Buy Below for eBay at $55 per share.

Express Scripts ($ESRX) was our surprise star from last earnings season. The shares jumped 7.15% over two days. The pharmacy-benefits manager now expects full-year earnings of $4.84 to $4.92 per share. I also like that ESRX has a fairly clean balance sheet. I’m going to keep our Buy Below at $74 per share for now, but I may raise it soon.

After the market’s July slide, I was curious which Buy List stock would be the first to make a new high. I remember thinking that picking Fiserv ($FISV) would be “too easy.” The stock rarely disappoints. On Thursday, Fiserv got as high as $62.47 per share, which is only 63 cents below the high from three weeks ago. This week, I’m raising our Buy Below on Fiserv to $66 per share.

You should never fall in love with a stock, but I have to admit that I have a serious crush on Ford Motor ($F). The stock had a strange sell-off that brought it below $17 for a few days. Don’t let that scare you. Things are going very well for Ford. I think we can expect another run at $18 per share. Ford currently yields 2.87%. Ford Motor is a buy up to $19 per share.

IBM ($IBM) was the stock that everyone loved to hate. I think that’s softened a bit, but Big Blue has many problems ahead. Fortunately, the shares are pretty cheap here. I don’t know if they’ll hit their highly touted earnings target of $20 per share for next year. I’m assuming they will. The company has been spending enormous amounts of money buying back their own shares—$3.7 billion in Q2! I don’t think this is the wisest strategy. I’d rather see that money go back to shareholders. IBM is a buy up to $197 per share.

McDonald’s ($MCD) is another stock that I listed last week as a candidate to stay home next year. I want to see signs from management that they get how serious the problems are. I don’t consider MCD to be a speculative play since the dividend is quite solid at 3.46%. McDonald’s is a buy up to $101 per share.

Medtronic ($MDT) is due to report on Tuesday, August 19. Wall Street currently expects earnings of 92 cents per share. My numbers say that’s about right. The medical-device maker is currently working through its big deal with Covidien. This is another stock that may not be back next year. Again, it’s not because I don’t like Medtronic, but the new company will be quite different. They see full-year earnings ranging between $4.00 and $4.10 for this year. Medtronic is a buy up to $67 per share.

Satya Nadella, Microsoft’s ($MSFT) new CEO, is still enjoying his honeymoon on Wall Street. Investors clearly love Steve Ballmer’s replacement. The irony is that much of the company’s recent success is due to Ballmer as much as to Nadella. If you recall, the stock fell in the after-hours market after the last earnings report came out. Then, once folks had a second to actually read what the company had to say, investors realized they had a good quarter. I think MSFT will make a run at their 52-week high soon. It’s our second-best performer this year. Microsoft continues to be a solid buy up to $48 per share.

Moog ($MOG-A) is the final company I listed last week as a potential candidate to be culled from the Buy List. I didn’t like their recent guidance. I’m keeping a tight Buy Below at $71 per share.

Oracle’s ($ORCL) last two earnings reports were not particularly inspiring. But the more I look at the company, the more impressed I am. Thanks to the sell-off, I think Oracle is an especially good bargain here. Oracle will report fiscal Q1 earnings in mid-September. In June, they gave guidance of 62 to 66 cents per share. They should be able to get that easily. Oracle is a very good buy below $40. My Buy Below is at $44 per share.

Qualcomm ($QCOM) got wrecked after its last earnings report, but here’s the hitch—the earnings were outstanding. Qualcomm also raised their full-year guidance, but investors were worried about their legal conflict with China. Unfortunately, there’s not much QCOM can do. I think they may wind up paying a hefty fine which may be the easiest route. Qualcomm remains a buy up to $79 per share.

Shares of Ross Stores ($ROST) have not done well this year, but that’s mostly due to the lousy environment for retail, not their performance. This week’s poor retail report also hurt the deep discounter. Ross is due to report fiscal Q2 earnings next Thursday, August 21. The company expects earnings between $1.05 and $1.09 per share. They also gave full-year guidance of $4.09 to $4.21 per share. If Ross can land in the upper end of that forecast, then the current share price is quite good. But I want to see next week’s results before I can say I’m more confident. Ross Stores is a buy up to $71 per share.

Stryker ($SYK) is one of those steady stocks that rarely surprises us. However, they surprised last month when they lowered guidance. Stryker lowered the top end of their full-year forecast by 10 cents per share. The shares pulled back from $86 at the beginning of July to $81 recently. Nevertheless, this isn’t one I worry about. Stryker remains a good buy up to $87 per share.

Wells Fargo ($WFC) is simply the best-run big bank in the country. Wells is having a good year for us (+11%). The bank isn’t quite the bargain it used to be, but I hope to see another dividend increase soon. For now, earnings growth has slowed down, but Wells is also a much safer stock than it used to be. Wells Fargo remains a buy up to $54 per share.

That’s all for now. Next week should be another slow week. There’s not a lot of economic news or earnings reports due, so traders may be especially sensitive to headline risk. On Tuesday, the Labor Department reports on consumer inflation. The recent up trend has been very modest, and it may have peaked. On Wednesday, the Fed releases the minutes from its most recent meeting. I think it’s clear what path they’re on. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 15, 2014

Posted by Eddy Elfenbein on August 15th, 2014 at 6:40 amU.K. Keeps Momentum in Second Quarter With 0.8% GDP Growth

Germany’s Foreign Engagement Is Very Light-Fingered

Modi Promises Bank Accounts for All Families in India

Jobless Claims in U.S. Rise to Highest Level in Six Weeks

Investors Pour $680 Million Into U.S. Junk Bonds in Latest Week

Bill Ackman to Sue U.S. Over Fannie, Freddie Mortgage Profits

Alibaba Merger Machine Stumbles as Movie Arm’s Books Questioned

J.C. Penney Company Earnings: Third Time’s the Charm

IAC’s Ask.com Buys Ask.fm And Hires A Safety Officer To Stem Bullying

BHP Favors Demerger as It Tidies Portfolio

Amazon ‘Stomping on Its Own Feet’ in Disney, Hachette E-Commerce Spats

Joshua Brown: Warren Buffett’s First Investing Lesson

Cullen Roche: Three Reasons Europe is Struggling

Be sure to follow me on Twitter.

-

Morning News: August 14, 2014

Posted by Eddy Elfenbein on August 14th, 2014 at 6:49 amGerman GDP Signals Euro-Zone Recovery May Be Stalling

Qualcomm Denies Direct Financial Links With Chinese Antitrust Expert

Gold Demand Falls in Q2 as Jewelry, Bar Sales Slide

Billionaire Found in Middle of Bribery Case Avoids U.S. Probe

Fed’s Rosengren, Dudley Say Broker Regulations Need Overhaul

Cisco to Take $700 Million in Restructuring Charges in 2015

Cisco Systems to Cut 6,000 Jobs

Wal-Mart Revenue Rises But U.S. Same-Store Sales Flat

Kinder Morgan Deal Ushers In A Golden Age Of MLP Investing

After China Smartphone Success, Lenovo Plans Leap Forward Overseas

Avago Agrees to Sell LSI’s Axxia Networking Business and Related Assets to Intel for $650 Million

Burger King Drops Lower-Calorie Fry ‘Satisfries’

Roger Nusbaum: You’re Gonna Need a Bigger Bucket

Be sure to follow me on Twitter.

-

Morning News: August 13, 2014

Posted by Eddy Elfenbein on August 13th, 2014 at 7:21 amCarney Cites Recovery Risks as BOE Sees ‘Gradual’ Rate Increases

Japan GDP Slump Stirs Stimulus Talk

European Firms Express Concern Over China Antitrust Probes

Chinese Lending Slowed Drastically in July

China Data Raises Doubts Over Growth

SEC Launches Examination of Alternative Mutual Funds

In Colorado, Tax Revenue From Recreational Pot Lower Than Expected

Introducing Amazon Local Register

Amazon Vs. Hachette: Which Side Should You Cheer For?

King Digital Lowers 2014 Forecast as Candy Crush Weakens

Alibaba Could Reap $9.4 Billion From New Alipay Deal

FleetCor Agrees to Acquire Comdata for $3.45 Billion

Market Basket a Rare Case in Labor World

Cullen Roche: We Are All Active Investors – Part 2

Joshua Brown: Corporations, Institutions Buy the Dip

Be sure to follow me on Twitter.

-

Berkshire Hathaway Nears $200K

Posted by Eddy Elfenbein on August 12th, 2014 at 10:58 amToday is the 32nd anniversary of the stock market’s mega-low. On this day in 1982, the Dow closed at 776.92. That’s below where it was 18 years before. The Dow would go on to grow by 15-fold over the next 17 years.

To give you some perspective, the classic 80s teen comedy, “Fast Times at Ridgemont High” opened the next day. Warren Buffet’s Berkshire Hathaway didn’t trade a single share on August 12, 1982. It had previously closed at $450.

Today, the A shares of Berkshire are knocking on the door of $200,000 which would be another all-time high. (Buffett adamantly doesn’t believe in splitting his stock.)

Over the last 15 years, shares of Berkshire have followed a steady pattern. They keep pace with bull markets, but strongly outperform in bear markets (2000 and 2008).

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His