-

CWS Market Review – August 15, 2014

Posted by Eddy Elfenbein on August 15th, 2014 at 7:05 am“Carpe diem. Seize the day, boys. Make your lives extraordinary.”

– Dead Poets SocietyThe stock market’s July swoon sure didn’t last long. From closing high to closing low (July 24 to August 7), the S&P 500 lost a grand total of 3.94%. That small bit of turbulence unnerved a lot of folks who should have known better. But since there’s been so little volatility of late, that minor dustup seemed larger than it truly was.

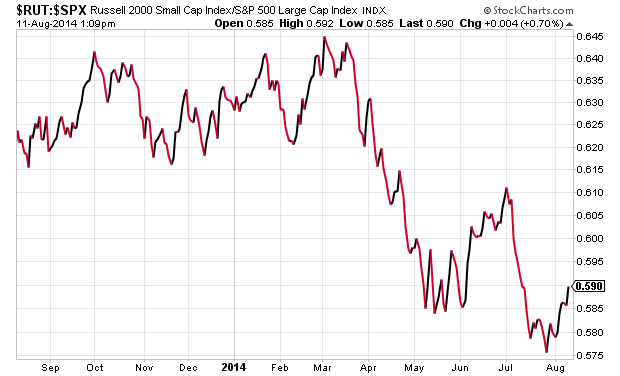

Last week, the Russian military called off some exercises near the Ukrainian border. I can’t say those exercises specifically caused the market’s tumble, but ever since they ended, the stock market has rallied. The S&P 500 has advanced in four of the last five sessions, and we’re not too far from another new high. Since August 7, the S&P 500 has gained 2.39%. Another sign that tensions have chilled out is that small-cap stocks have led the bounce-back rally, and the VIX is back down again.

Now that second-quarter earnings season is past us, this is a good time to run through all 20 stocks on our Buy List and review their prospects for the rest of the year. I’ll also take a look at the recent bond market rally. Long-term yields have been dropping, and I think the time has finally come for bonds to take a rest. We’ll also preview two Buy List earnings reports for next week. But first, let’s look at the stretched market for bonds.

It’s Time for Bonds to Sit Down

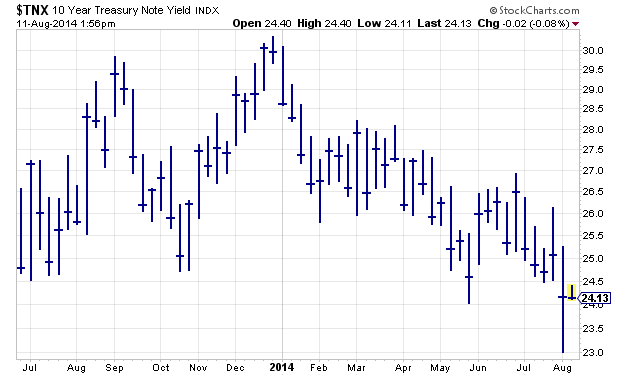

As well as the stock market’s done lately, the bond market has been a rock star this year. The yield on the 10-year Treasury closed at 2.40% on Thursday. That’s a 14-month low. If you had told me on New Year’s Day that the 10-year would go for 2.40% by August, I would have thought you were out of your mind. The yield has dropped more than 60 basis points since the start of the year.

It’s interesting how few people saw this big bond rally coming. Jeffrey Gundlach, the bond kingpin, was one of the few who got it right. There seems to be an insatiable appetite for all things bond. This week, the Treasury auctioned off some 30-year bonds, and yields were the lowest in more than a year.

Why the demand for fixed-income? I think this represents misplaced concerns about stock prices. Given where we are in the economy, it’s safe to say that the bond rally has run too far. The idea that investors are willing to lock in their capital for 10 years to get a measly 2.4% seems a bit crazy to me. That’s almost exactly what the stock market has gained in the last five years.

Several of our blue-chip Buy List stocks yield more than the 10-year, such as Wells Fargo ($WFC), Ford ($F) and Microsoft ($MSFT). Not only do they yield more, but they’re also thriving businesses. As much as I love bonds, they just sit there.

You can really see the absurdity of the bond market by looking at the TIPs—the inflation-protected bonds. The 10-year TIP currently yields 0.2%. That’s down from 0.8% late last year. I understand why investors are nervous about stocks, but I don’t see why anyone would invest in a bond that barely beats inflation for the next 10 years. In 2012 and 2013, the 10-year TIPs turned negative, but the fear was more understandable, given the dramatic events in Europe. The 10-year Spanish bond now yields less than American bonds. In Germany, the 10-year bond dropped below 1%. The 1% Club is very exclusive; the only other members are Japan and Switzerland.

Thanks to improved economic numbers, we can expect long-term yields to drift higher as the year goes on. By this time next year, the Federal Reserve may have already started raising interest rates. Now let’s take a look at our Buy List.

Rundown of the Buy List

I was puzzled by the market’s negative reaction to AFLAC’s ($AFL) Q2 earnings report. I thought the earnings were fine. After all, they beat expectations by seven cents per share, but the shares fell as low as $58.50, and two weeks ago, I said the stock was an especially cheap buy below $60. The good news is that AFLAC ticked up above $60 per share on Thursday. AFLAC remains a good buy up to $66 per share.

Bed Bath & Beyond ($BBBY) continues to recover, but unevenly. BBBY broke above $64 per share in late July. That’s nearly $10 more than its July low. Investors clearly overreacted to BBBY’s bad news. Remember that this is one of our off-cycle stocks, so they’ll report their Q2 earnings in about six weeks. They see Q2 earnings ranging between $1.08 and $1.16 per share. That’s not bad. Bed Bath & Beyond remains a good buy up to $65 per share.

Last week, I mentioned that CA Technologies ($CA) was in danger of being knocked off next year’s Buy List. I’m free to change my mind before then, but I need to see more signs of improvement from CA. The part I really like is the generous yield. Going by Thursday’s close, CA yields 3.52%, but I’m not crazy about them. CA Technologies is a moderate buy up to $31 per share.

Cognizant Technology ($CTSH) seemed to be our only bomb from last earnings season. Now that I’ve looked at the numbers, I’m not worried about CTSH at all. I apologize if you were caught in the sell-off, but the company is still doing well. If you don’t own CTSH, this is a good time to start a position, especially if you can get it below $45 per share. Cognizant Technology remains a good buy up to $48 per share.

CR Bard ($BCR) is one of those quiet stocks that you tend to forget about because they’re so quiet. That’s unfair, because this is a solid company. Bard beat earnings last month and raised their full-year guidance. They now expect $8.25 to $8.35 per share for the full year. I held off on changing our Buy Below on Bard, but I think this is a good time for an increase. I’m raising our Buy Below on CR Bard to $160 per share.

I also mentioned DirecTV ($DTV) last week as a possible deletion from next year’s Buy List. The difference is that I love DTV. It’s the AT&T deal that makes them less attractive as an investment. Their business continues to do well. I’ll let you know as we hear more about the AT&T deal. My decision will come down to how close the shares are to $95 by year’s end. There’s no point in holding on to a stock for a few more percent. Until then, DTV is a buy up to $95 per share.

eBay ($EBAY) got knocked around for most of the spring. I’m pleased to see the shares are making their way back. They beat earnings by a penny per share last month, and the stock has continued to rally. eBay sees full-year earnings ranging between $2.95 and $3.00 per share. I’m going to keep a tight Buy Below for eBay at $55 per share.

Express Scripts ($ESRX) was our surprise star from last earnings season. The shares jumped 7.15% over two days. The pharmacy-benefits manager now expects full-year earnings of $4.84 to $4.92 per share. I also like that ESRX has a fairly clean balance sheet. I’m going to keep our Buy Below at $74 per share for now, but I may raise it soon.

After the market’s July slide, I was curious which Buy List stock would be the first to make a new high. I remember thinking that picking Fiserv ($FISV) would be “too easy.” The stock rarely disappoints. On Thursday, Fiserv got as high as $62.47 per share, which is only 63 cents below the high from three weeks ago. This week, I’m raising our Buy Below on Fiserv to $66 per share.

You should never fall in love with a stock, but I have to admit that I have a serious crush on Ford Motor ($F). The stock had a strange sell-off that brought it below $17 for a few days. Don’t let that scare you. Things are going very well for Ford. I think we can expect another run at $18 per share. Ford currently yields 2.87%. Ford Motor is a buy up to $19 per share.

IBM ($IBM) was the stock that everyone loved to hate. I think that’s softened a bit, but Big Blue has many problems ahead. Fortunately, the shares are pretty cheap here. I don’t know if they’ll hit their highly touted earnings target of $20 per share for next year. I’m assuming they will. The company has been spending enormous amounts of money buying back their own shares—$3.7 billion in Q2! I don’t think this is the wisest strategy. I’d rather see that money go back to shareholders. IBM is a buy up to $197 per share.

McDonald’s ($MCD) is another stock that I listed last week as a candidate to stay home next year. I want to see signs from management that they get how serious the problems are. I don’t consider MCD to be a speculative play since the dividend is quite solid at 3.46%. McDonald’s is a buy up to $101 per share.

Medtronic ($MDT) is due to report on Tuesday, August 19. Wall Street currently expects earnings of 92 cents per share. My numbers say that’s about right. The medical-device maker is currently working through its big deal with Covidien. This is another stock that may not be back next year. Again, it’s not because I don’t like Medtronic, but the new company will be quite different. They see full-year earnings ranging between $4.00 and $4.10 for this year. Medtronic is a buy up to $67 per share.

Satya Nadella, Microsoft’s ($MSFT) new CEO, is still enjoying his honeymoon on Wall Street. Investors clearly love Steve Ballmer’s replacement. The irony is that much of the company’s recent success is due to Ballmer as much as to Nadella. If you recall, the stock fell in the after-hours market after the last earnings report came out. Then, once folks had a second to actually read what the company had to say, investors realized they had a good quarter. I think MSFT will make a run at their 52-week high soon. It’s our second-best performer this year. Microsoft continues to be a solid buy up to $48 per share.

Moog ($MOG-A) is the final company I listed last week as a potential candidate to be culled from the Buy List. I didn’t like their recent guidance. I’m keeping a tight Buy Below at $71 per share.

Oracle’s ($ORCL) last two earnings reports were not particularly inspiring. But the more I look at the company, the more impressed I am. Thanks to the sell-off, I think Oracle is an especially good bargain here. Oracle will report fiscal Q1 earnings in mid-September. In June, they gave guidance of 62 to 66 cents per share. They should be able to get that easily. Oracle is a very good buy below $40. My Buy Below is at $44 per share.

Qualcomm ($QCOM) got wrecked after its last earnings report, but here’s the hitch—the earnings were outstanding. Qualcomm also raised their full-year guidance, but investors were worried about their legal conflict with China. Unfortunately, there’s not much QCOM can do. I think they may wind up paying a hefty fine which may be the easiest route. Qualcomm remains a buy up to $79 per share.

Shares of Ross Stores ($ROST) have not done well this year, but that’s mostly due to the lousy environment for retail, not their performance. This week’s poor retail report also hurt the deep discounter. Ross is due to report fiscal Q2 earnings next Thursday, August 21. The company expects earnings between $1.05 and $1.09 per share. They also gave full-year guidance of $4.09 to $4.21 per share. If Ross can land in the upper end of that forecast, then the current share price is quite good. But I want to see next week’s results before I can say I’m more confident. Ross Stores is a buy up to $71 per share.

Stryker ($SYK) is one of those steady stocks that rarely surprises us. However, they surprised last month when they lowered guidance. Stryker lowered the top end of their full-year forecast by 10 cents per share. The shares pulled back from $86 at the beginning of July to $81 recently. Nevertheless, this isn’t one I worry about. Stryker remains a good buy up to $87 per share.

Wells Fargo ($WFC) is simply the best-run big bank in the country. Wells is having a good year for us (+11%). The bank isn’t quite the bargain it used to be, but I hope to see another dividend increase soon. For now, earnings growth has slowed down, but Wells is also a much safer stock than it used to be. Wells Fargo remains a buy up to $54 per share.

That’s all for now. Next week should be another slow week. There’s not a lot of economic news or earnings reports due, so traders may be especially sensitive to headline risk. On Tuesday, the Labor Department reports on consumer inflation. The recent up trend has been very modest, and it may have peaked. On Wednesday, the Fed releases the minutes from its most recent meeting. I think it’s clear what path they’re on. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 15, 2014

Posted by Eddy Elfenbein on August 15th, 2014 at 6:40 amU.K. Keeps Momentum in Second Quarter With 0.8% GDP Growth

Germany’s Foreign Engagement Is Very Light-Fingered

Modi Promises Bank Accounts for All Families in India

Jobless Claims in U.S. Rise to Highest Level in Six Weeks

Investors Pour $680 Million Into U.S. Junk Bonds in Latest Week

Bill Ackman to Sue U.S. Over Fannie, Freddie Mortgage Profits

Alibaba Merger Machine Stumbles as Movie Arm’s Books Questioned

J.C. Penney Company Earnings: Third Time’s the Charm

IAC’s Ask.com Buys Ask.fm And Hires A Safety Officer To Stem Bullying

BHP Favors Demerger as It Tidies Portfolio

Amazon ‘Stomping on Its Own Feet’ in Disney, Hachette E-Commerce Spats

Joshua Brown: Warren Buffett’s First Investing Lesson

Cullen Roche: Three Reasons Europe is Struggling

Be sure to follow me on Twitter.

-

Morning News: August 14, 2014

Posted by Eddy Elfenbein on August 14th, 2014 at 6:49 amGerman GDP Signals Euro-Zone Recovery May Be Stalling

Qualcomm Denies Direct Financial Links With Chinese Antitrust Expert

Gold Demand Falls in Q2 as Jewelry, Bar Sales Slide

Billionaire Found in Middle of Bribery Case Avoids U.S. Probe

Fed’s Rosengren, Dudley Say Broker Regulations Need Overhaul

Cisco to Take $700 Million in Restructuring Charges in 2015

Cisco Systems to Cut 6,000 Jobs

Wal-Mart Revenue Rises But U.S. Same-Store Sales Flat

Kinder Morgan Deal Ushers In A Golden Age Of MLP Investing

After China Smartphone Success, Lenovo Plans Leap Forward Overseas

Avago Agrees to Sell LSI’s Axxia Networking Business and Related Assets to Intel for $650 Million

Burger King Drops Lower-Calorie Fry ‘Satisfries’

Roger Nusbaum: You’re Gonna Need a Bigger Bucket

Be sure to follow me on Twitter.

-

Morning News: August 13, 2014

Posted by Eddy Elfenbein on August 13th, 2014 at 7:21 amCarney Cites Recovery Risks as BOE Sees ‘Gradual’ Rate Increases

Japan GDP Slump Stirs Stimulus Talk

European Firms Express Concern Over China Antitrust Probes

Chinese Lending Slowed Drastically in July

China Data Raises Doubts Over Growth

SEC Launches Examination of Alternative Mutual Funds

In Colorado, Tax Revenue From Recreational Pot Lower Than Expected

Introducing Amazon Local Register

Amazon Vs. Hachette: Which Side Should You Cheer For?

King Digital Lowers 2014 Forecast as Candy Crush Weakens

Alibaba Could Reap $9.4 Billion From New Alipay Deal

FleetCor Agrees to Acquire Comdata for $3.45 Billion

Market Basket a Rare Case in Labor World

Cullen Roche: We Are All Active Investors – Part 2

Joshua Brown: Corporations, Institutions Buy the Dip

Be sure to follow me on Twitter.

-

Berkshire Hathaway Nears $200K

Posted by Eddy Elfenbein on August 12th, 2014 at 10:58 amToday is the 32nd anniversary of the stock market’s mega-low. On this day in 1982, the Dow closed at 776.92. That’s below where it was 18 years before. The Dow would go on to grow by 15-fold over the next 17 years.

To give you some perspective, the classic 80s teen comedy, “Fast Times at Ridgemont High” opened the next day. Warren Buffet’s Berkshire Hathaway didn’t trade a single share on August 12, 1982. It had previously closed at $450.

Today, the A shares of Berkshire are knocking on the door of $200,000 which would be another all-time high. (Buffett adamantly doesn’t believe in splitting his stock.)

Over the last 15 years, shares of Berkshire have followed a steady pattern. They keep pace with bull markets, but strongly outperform in bear markets (2000 and 2008).

-

Morning News: August 12, 2014

Posted by Eddy Elfenbein on August 12th, 2014 at 7:30 amGerman Investor Confidence Slumps on Ukraine Crisis

More Evidence Singapore Restructuring Taking Hold

Postal Service’s Net Loss Increases to $2 Billion in Quarter

Consumer-Finance Regulator Puts Digital Currencies in Its Sights

Derivatives Reincarnate Boosting Debt Wagers in New Era

Henkel Sees Slowing Profit Growth in H2 on Russia, Middle East

Amazon Misrepresents Orwell and Takes on Disney, As the Pricing War Intensifies

Rich Kinder Just Made $1.5 Billion In A Morning By Outsmarting All Of Wall Street

3 Reasons Family Dollar’s Stock Could Rise

Chiquita Banana Brand Receives a Counter to Its Inversion Plan

Buzzfeed Seeks to Move Beyond Its Famous Lists

Uber Accused of Playing Dirty in Competition With Lyft

Keystone XL Pipeline May Fail but Investors Can Still Profit

Cullen Roche: GDP Isn’t Designed to Measure Happiness

Joshua Brown: With Bulls Like These, Who Needs Bears?

Be sure to follow me on Twitter.

-

The Bond Market Abides

Posted by Eddy Elfenbein on August 11th, 2014 at 2:08 pmThis certainly isn’t a novel point, but the bond market has done very well this year, and that’s surprised a lot of folks. The 10-year yield got to 3% at the end of last year, and it was widely expected to climb throughout 2014.

Well, that hasn’t happened. The closing low is near its lowest levels in more than a year.

-

The Stock Market Calms Down, For Now

Posted by Eddy Elfenbein on August 11th, 2014 at 12:45 pmThe stock market is up again today after a very good day on Friday. The S&P 500 hit a near-term low of 1,904.78 on Thursday. Today we’ve been as high as 1,944.90. Several of our Buy List stocks are doing well; Qualcomm, IBM and Bed, Bath & Beyond are all up more than 1% so far.

Small-caps are doing especially well today. The Russell 2000 is currently up 1.2%, which is more than double the S&P 500. Despite repeated predictions of its demise, the bond market continues to do very well. On Friday, the 10-year closed at 2.41% which is the lowest closing yield in 14 months. The yield is currently holding at 2.42%.

The stock market got quite nervous last week due to some geo-political tensions, but it seems that the threat has cooled off since then, though by no means has it gone away. The recent price action seems to be strongly related to a relaxation of tensions.

Check out this relative strength chart of the Russell 2000 divided by the S&P 500.

-

Morning News: August 11, 2014

Posted by Eddy Elfenbein on August 11th, 2014 at 6:59 amWar Risks Slow Company Bond Sales to Least Since July ’13

Food and Flirting; How Firms Learn to Live With China Antitrust Raids

Libor to FX Cases Drive Surge in Teamwork With Regulators

Stalled Gazprom Antitrust Case May Suggest Unease for Energy Sanctions

Wheat Bears Retreat as Black Sea Supply Risks Mount

Kinder Morgan to Consolidate Empire

Keystone XL Could Mean More Carbon Emissions than Estimated, Study Says

Balfour Beatty Rejects Two Merger Offers From Rival Carillion

Amazon Takes on Disney’s Superheroes in Online Fight

In a Fight With Authors, Amazon Cites Orwell, but Not Quite Correctly

Andreessen Horowitz Invests $50 Million in Buzz Feed

How Tiger Woods Becomes Zynga’s Last Hope for Glory

Treasury Wine Says Buyout Firm Matches K.K.R.’s $3.2 Billion Bid

Jeff Miller: Weighing the Week Ahead: The Market Risk from Current Crises

Epicurean Dealmaker: A Cure Worse Than The Disease

Be sure to follow me on Twitter.

-

CWS Market Review – August 8, 2014

Posted by Eddy Elfenbein on August 8th, 2014 at 7:26 am“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” – Peter Lynch

After a very subdued June and July, the stock market has suddenly gotten a lot more interesting. The S&P 500 had gone 62 trading days in a row without a daily move, up or down, of more than 1%. That was the longest streak of its kind in nearly 20 years. Then we had three such days within two weeks, and we came very close to a fourth on Tuesday.

On Thursday, the S&P 500 fell to a two-month low of 1,909.57. In an apparent homage to Black Monday, the index reached its closing high of 1,987.98 on July 24. We’re now down 3.94% from that mark. Last week, the S&P 500 broke below its 50-day moving average last week, and we’re only 2.6% above the 200-DMA. It’s been 21 months since the S&P 500 last closed below its 200-DMA.

There are lots of reasons for the market’s new-found case of anxiety: Ebola, Putin, Hamas, ISIS. From its July low to its August high, the Volatility Index ($VIX) soared 66%. Gold has been creeping up as well. Despite the increase in worrying, the fundamentals of the economy and stock market are sound.

Last Friday, for example, we had another good jobs report: the U.S. economy created 209,000 net new jobs in July. This is the first time in 17 years that the economy has created more than 200,000 jobs for six months in a row, and I think we can expect a seventh. On Thursday, the Labor Department reported that the four-week moving average of jobless claims fell to an eight-year low. We also learned last week that the ISM Manufacturing Index jumped to 57.1, which is its highest level in more than three years. There are lots of problems in the world, but an imminent recession in the U.S. isn’t one of them.

We’re nearing the end of second-quarter earnings season, and it’s mostly been a good one. Of the S&P 500 companies that have reported so far, 75% have beaten their earnings expectations, while 65% have beaten on sales. For Q2, the S&P 500 is on track to report earnings growth of 9.4% and sales growth of 4.2%. Despite all the loose talk of a new bubble, valuations haven’t changed much in the past year.

Our Buy List nearly made it through earnings season without a dud, but Cognizant Technology ($CTSH) had to ruin it for us. On Wednesday, the IT outsourcer beat estimates by four cents per share, but it lowered its sales guidance. Traders didn’t like that at all, and by the closing bell, CTSH lost 12.6%. I’ll have a complete rundown in just a bit (Spoiler Alert: I’m still a Cognizant fan.) I also want to review some Buy List members who may not make it onto next year’s list. We’re still a few months away from making our selections, but I want to share some thoughts with you. But first, let’s look at this newly volatile market.

What Are the Side Effects of QE?

Despite the big loss from Cognizant, our Buy List has been outperforming the overall stock market lately. Since we focus on high-quality stocks, we usually outperform the market during “worrying” stretches like we’ve seen recently.

Through Thursday, our Buy List is trailing the S&P 500 for the year (3.31% for the S&P 500 to -0.32% for us, not including dividends). Part of our underperformance this year is due to the rally being overfed by a lot of low-quality, crappy stocks. Even Janet Yellen recently said, while defending the overall market’s valuation, that “valuation metrics in some sectors do appear substantially stretched, particularly those for smaller firms in the social media and biotechnology industries.”

She’s absolutely right. Look at a stock like Amazon.com ($AMZN) which is down more than 23% from its high, and it’s still trading at 150 times next year’s earnings (the company will probably lose money this year). Last month, I mentioned the outrageous case of Cynk Technology ($CYNK). The shares are down 97% since then.

This is a paradox of the market. On one hand, we want to see lower-quality names do well so capital can reach marginal businesses (and borrowers). But we don’t want to see the trend go overboard and cause investors to leave the good stuff behind. That’s partly what happened during the Credit Bubble. I remember how our Buy List trailed the market in 2006 and kept slightly ahead in 2007. But once the Financial Crisis took hold and all those garbage stocks got called out, our Buy List fell far less than the market. We recovered much more quickly as well. Why? Because we never bought the junk, so when the House of Cards tumbled over, our relative performance was outstanding.

This leads me to one of the big questions on the minds of professional investors: what are the side effects of the Federal Reserve’s unprecedented policies? The Fed has kept short-term interest rates near 0% for a long time. Naturally, any Fed policy will distort the market. I think, too, that some investors view this phenomenon in overly sinister tones, but I tend to view it rather dispassionately. The central bank is powerful, and it’s trying to entice investors to be more confident. That’s not easy to do, and 0% interest rates is a start.

One side effect is that investors grew too fond of junk bonds. Since the start of July, junk bonds have taken a sharp turn for the worse, and that’s probably a healthy sign. This is an important sector for investors to watch, even if you’re not invested there, because it tells us how the marginal borrower is doing. When junk bonds perform as well as other bonds, or even outperform them, that’s usually an optimistic sign for the economy. It hints that business is going well, and will probably continue to improve. But again, it shouldn’t be used to fund shady operations.

I’m also concerned that low rates have made share repurchases too easy to resist. I have no problem with companies borrowing money to fund their operations. But I’m concerned that easy credit has allowed too many companies to boost their EPS, not by growing their earnings but by reducing their share count.

This has also been a lousy year for small-cap stocks, and I can’t help but think it’s related to the Fed’s winding down of QE. Not that smaller companies benefit from the bond buying, but they prosper as the risks have been partly covered by the Fed. Why not, then, go for more aggressive names? But since July 3, the small-cap Russell 2000 is down 7.3%, nearly twice as much as the S&P 500. Investors want more safety, and they’re willing to pay for it.

What does this mean for us? Investors should focus on higher-quality names, especially dividend payers. Some Buy List stocks I like right now include Ford Motor ($F), which is especially good below $17 per share. Oracle ($ORCL) is a bargain below $40 per share. Ross Stores ($ROST) can’t seem to catch a break, but if you’re able to get it under $65, you got a good deal. Earnings are due out soon. Now let’s take a look at our big flop of this earnings season.

Cognizant Technology Plunges after Earnings

On Wednesday, shares of Cognizant Technology Solutions ($CTSH) got nailed for a 12.6% loss. At one point, the shares were down 17% on the day. The interesting part is that their Q2 earnings were quite good. Cognizant earned 66 cents per share, which topped Wall Street’s consensus by four cents per share, and quarterly revenues rose by 16.5% to $2.52 billion.

What caused traders so much grief wasn’t the earnings; it was Cognizant’s guidance. Actually, it wasn’t the earnings guidance—that was the same. It was their sales guidance that caused so much grief.

For Q3, Cognizant now expects earnings of at least 63 cents per share. Wall Street had been expecting 65 cents per share. But the company is keeping their full-year guidance at $2.54 per share, which is the same as it’s been. For Q3 sales, Cognizant now expects a range between $2.55 billion and $2.58 billion. Wall Street had been expecting $2.66 billion. For full-year sales, CTSH lowered their growth rate from 16.5% to 14%.

Cognizant’s CEO Francisco D’Souza said, “Due to weakness at certain clients and longer-than-anticipated sales cycles for certain large integrated deals, we are adopting a more conservative stance for the remainder of the year and revising our 2014 revenue guidance to growth of at least 14% over the prior year, while maintaining our full-year non-GAAP EPS guidance of $2.54.”

I can hardly say that I’m worried about a company that’s beating earnings and growing its top line by 14%. After Wednesday’s damage, CTSH is going for about 17.5 times this year’s estimate, which is a very good price. To reflect the selloff, I’m lowering my Buy Below on Cognizant to $48 per share.

Potential Buy List Deletions

According to the rules of our Buy List, the 20 stocks are locked and sealed for the entire year. No matter how much I want to make a move, I can’t touch any of the stocks until the end of the year. As usual, I only add and delete five stocks.

Now that we’re in the middle of summer, I want to share some of my preliminary thoughts on which stocks may not be around next year. Please understand that these are early indications, and I may change my mind before December. This also doesn’t mean that I don’t like these stocks at the moment. They’re simply on the short list to be cut next year. Ideally, when I make the change at the end of the year, the decisions shouldn’t come as a big surprise to regular readers.

At the top of the list is DirecTV ($DTV). It’s here not because it’s done poorly, but because it’s done very well for us. Thanks to the deal with AT&T, it’s not clear how much longer DTV will go on as an independent company. I can’t make any predictions on the AT&T deal falling though, or when it might be completed, but I’d prefer to congratulate DTV, and move on to a new stock. DTV has been a big winner for us.

Unfortunately, CA Technologies ($CA) has been much weaker than I expected. Quarterly revenues have dropped for nine quarters in a row, and will be probably do so again. We’ve been patient with CA, but the company’s problems run deep. I like the rich dividend, but frankly, not much else.

Moog ($MOG-A) dropped sharply in February, but recovered very nicely this spring. The recent guidance, however, was not what I was expecting.

I haven’t given up on McDonald’s ($MCD). The stock is cheap, but the problems for the burger giant are bigger than I expected. I think management realizes this, but turning around a company of this size won’t be easy. I still like MCD, but I want to see signs of improvement.

Medtronic ($MDT) is a long-time favorite of mine, and the stock has done well for us. My concern is that the Covidien deal is a major undertaking, and the new entity will be quite different from the old Medtronic. I understand why Medtronic wants to do this deal, and it probably makes sense, but it may not be the company we want on our Buy List.

All 16 of the Buy List stocks with quarters ending in June have new reported earnings. There are only two Buy List stocks that have quarters ending in July, Medtronic ($MDT) and Ross Stores ($ROST). Medtronic is due to report on August 19, and Ross Stores will follow two days later. I’ll have more to say about both stocks next week. Before I go, I also want to lower my Buy Below on Qualcomm to $79 per share. The stock has continued to drift lower after the earnings report. I like QCOM a lot and expect it to recover.

That’s all for now. Next week will be a fairly slow week for economic reports. I’ll be curious to see Wednesday’s retail sales report. Consumer spending hasn’t been as strong as I’d like to see. On Friday, we’ll get the report on Industrial Production. The last three reports haven’t been that great. I’d like to see some improvement here. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His