-

The FRED Cult

Posted by Eddy Elfenbein on August 5th, 2014 at 11:08 amRegular readers know that I’m a big fan of FRED, the St. Louis Federal Reserve’s Economic Data. This database contains huge numbers of economic data series that are easily searchable.

A user can effortlessly transform FRED data into a usable chart, the kind of which you’ve seen many times on this site (for example, see the ISM chart from yesterday). I’m not alone in my admiration of FRED. The Washington Post writes:

Nobel Laureate economist Paul Krugman is a huge FRED fan. Harvard economist Greg Mankiw uses it. Former Fed chairman Ben Bernanke cited it in a textbook. The site Business Insider called it “the most amazing economics Web site in the world.”

“It definitely has a cult following,” said Eddy Elfenbein, a financial analyst in Washington and editor of CrossingWallStreet.com. For him, FRED has emerged as the central hub for finding and sorting through the reams of financial data. He can spend hours looking up trivia such as the historical price of copper in Britain. “It’s addictive,” Elfenbein said.

There are well over 200,000 different series at FRED. A personal favorite is brick production in England and Wales, 1785 to 1815.

-

Morning News: August 5, 2014

Posted by Eddy Elfenbein on August 5th, 2014 at 6:45 amWhat Crisis? EU Rules on Banks Lauded as Right After All

Crédit Agricole Takes $950 Million Charge on Portuguese Bank

WH Group Makes Solid Hong Kong Debut

Time Warner Taking Hard Stance on a Bid By Fox

Telefonica Launches USD 9 Billion Bid for Vivendi’s Brazilian Unit GVT

Focusing on G.M. Unit, U.S. Starts Civil Inquiry of Subprime Car Lending

McClatchy Announces Agreement To Sell Its 25.6% Stake In Cars.com To Gannett

Toyota Reports Surprise Record Profit on U.S. SUV Demand

BMW Sees 2nd-Quarter Earnings Jump as Sales Grow, Better Model Mix Boosts Profitability

Apple Buybacks Pay Most Ever as CEOs Spend $211 Billion

Valeant’s Deal With Ackman May Be Too Clever to Be Legal

LinkedIn Pays $6 Million Over Employee Wage Violations

Ecclestone Offers $100 Million to Settle Munich Case

Jeff Carter: Do You Bet on Teams, Or Ideas?

Joshua Brown: If Everyone Wants Their Money Back at the Same Time…

Be sure to follow me on Twitter.

-

The Junk Scare

Posted by Eddy Elfenbein on August 4th, 2014 at 2:10 pmCheck out the recent performance of the High-Yield bond ETF ($HYG). If you look at the right scale, it’s really not that big of a move, but it’s plenty big compared with the junk bond market’s recent history.

So why are people fleeing junk? I suspect it’s part of a larger pattern where investors are clamoring for safer assets. That’s understandable given the news out of places like Syria, Argentina and Ukraine. What’s also interesting is that Industrial stocks have badly lagged the market over the past two months while Technology has been a leader.

-

July ISM = 57.1

Posted by Eddy Elfenbein on August 4th, 2014 at 11:02 amOne more news item from Friday. The ISM Index for July came in at 57.1. That’s the highest figure in more than three years.

The ISM came very close to expanding for six months in a row but there was a 0.1 drop from May to June.

-

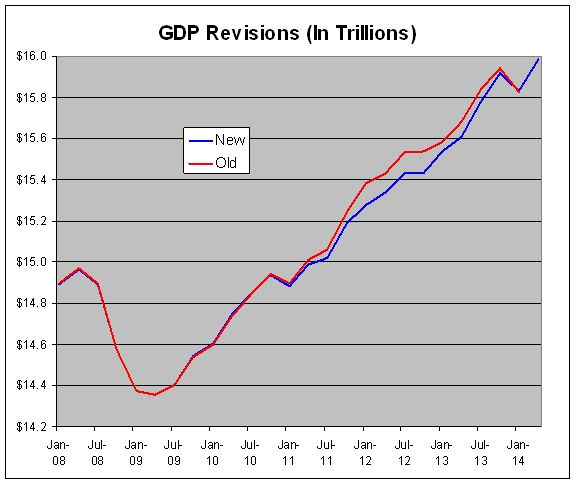

GDP Series Revised

Posted by Eddy Elfenbein on August 4th, 2014 at 10:02 amOn Friday, the government released their first estimate of Q2 GDP growth. They also revised their historical data as well. Here’s a side-by-side look at the old and new numbers.

It turns out that the economy did worse during 2011-12 than we originally thought, but the bounce back since then has been better than we thought.

-

McDonald’s Is Coping With Several Issues

Posted by Eddy Elfenbein on August 4th, 2014 at 9:55 amI’ve not been pleased with the performance of McDonald’s ($MCD) this year. I added MCD to this year’s Buy List at what I thought was a very good price. The problems at the fast food joint, however, have been more serious than I anticipated.

MCD missed earnings by three cents in April and by four cents last month. The company is on pace to earn about $5.65 per share this year. What’s also troubling is that MCD has also been plagued by issues that aren’t much under their control, such as possible sanctions in Russia.

Investors, analysts and franchisees are clamoring for the company to stop trying to be “all things to all people”. They want it to simplify its unwieldy menu and point to the success of rivals like Chipotle Mexican Grill Inc and In-N-Out Burger, which have won passionate fans by selling just a few items.

McDonald’s was caught up in the latest China food safety scare after a July 20 television expose showed workers allegedly mishandling meat at Shanghai Husi Food Co Ltd, a factory owned by OSI Group LLC, a major supplier to the chain.

When the story broke, McDonald’s China business had been rebounding from the double whammy of a food safety scare and a bird flu outbreak that crushed sales in 2013.

McDonald’s roughly 2,000 restaurants in China suffered meat shortages after it ended its relationship with OSI China. Executives from the chain’s long-struggling Japanese unit, McDonald’s Holdings Co Ltd, who were forced to find alternate chicken McNugget supplies, said the scare sent sales down as much as 20 percent.

(…)

The bigger concern, she said, are McDonald’s troubles in Russia, where the company has about 400 restaurants.

Against the backdrop of the political tussle over U.S. sanctions imposed on Russia because of Moscow’s intervention in Ukraine, Russia’s chief sanitary inspector Anna Popova on July 25 accused the company of violations “which put the product quality and safety of the entire McDonald’s chain in doubt.”

Europe contributes about 35 percent of McDonald’s operating profit. The company does not break out country-specific contributions, but Russia “up until recently had been one of the stronger markets for them in Europe,” Senatore said.

I still think that most of the issues at McDonald’s are fixable, but I’m not sure if the current management team is up to the task. The stock is down to $94 compared with $104 in May.

-

Morning News: August 4, 2014

Posted by Eddy Elfenbein on August 4th, 2014 at 6:48 amGermany Blocks Rheinmetall Sale of Russian Combat Center

Banco Espirito Santo Junior Bonds Slide as Bailout Forces Losses

UK House-Building PMI Grows at Fastest Rate Since 2003

China’s Stocks Rise to Eight-Month High as Chalco Rallies

Chinese Group Bids $441 Million for Roc Oil of Australia

Booming African Lion Economies Gear Up to Emulate Asians

HSBC’s Profit Declines on Slowdown in Asia and Markets

McDonald’s to Resume Full Menu in China Cities This Week

A Glance at New Changes at Walmart.com

P&G to Sell Up to 100 Brands to Revive Sales, Cut Costs

Auto Sales Head for Best Since ’06 on Confidence, Jobs

Tycoon Li Ka-Shing’s Cheung Kong Eyes on AWAS Assets

Evercore Partners to Buy ISI Group

Jeff Miller: Weighing the Week Ahead: Will the Fed’s Experiment End Badly?

Epicurean Dealmaker: Where Did He Learn to Negotiate Like That?

Be sure to follow me on Twitter.

-

Follow-Up on Q2 GDP

Posted by Eddy Elfenbein on August 1st, 2014 at 7:04 pmHere’s a small footnote to this week’s Q2 GDP report.

If we work out the decimals, the economy grew by 3.9501881957% during Q2. That’s the annualized after-inflation rate. Of course, that rounds up to 4.0% which was reported just about everywhere.

But how close did we come to being rounded down to 3.9%? By my calculations, we crossed the rounding-up threshold in the final 6 minutes and 7.4 seconds of the quarter.

-

July NFP +209,000

Posted by Eddy Elfenbein on August 1st, 2014 at 11:29 amThe government reported this morning that the U.S. economy created 209,000 net new jobs last month. This was actually below Wall Street’s estimate of 230,000. Still, this is the sixth month in a row that we’ve cleared 200K.

The NFP number for June was revised higher by 10,000, and May’s was revised upward by 15,000. The unemployment rate ticked up to 6.2%.

-

CWS Market Review – August 1, 2014

Posted by Eddy Elfenbein on August 1st, 2014 at 7:10 am“I’m only rich because I know when I’m wrong…I basically

have survived by recognizing my mistakes.” – George SorosI’m currently enjoying a lovely vacation in Mont-Tremblant, Quebec, but I wanted to update you on the latest events on Wall Street, the economy and most importantly, our Buy List. The stock market evidently chose my vacation time to give us one of its worst days this year.

On Thursday, the S&P 500 dropped 2% to 1,930.71. That’s the index’s biggest loss since April 10th. Of course, by historical standards, a 2% drop is hardly a big drop, but it’s quite unusual for 2014. This is the third time in the past two weeks that the S&P 500 has moved by more than 1% in a single day. That didn’t happen at all in the 62 trading days prior to that. The Dow Jones Industrials have now given back their entire gain for the year.

So what caused the traders to freak out this time? It’s always hard to say exactly what event triggers any sell-off. Of course, there are several lingering concerns like Russia, Argentina and Syria, but it seems that investors were unnerved by, of all things, a 0.7% rise in the employment cost index for the second quarter. Expectations were for an increase of 0.5%.

This seems like an unusual event to cause such a big reaction. However, the employment cost report could foreshadow more inflation. Personally, I’d like to see a modest increase in inflation, but traders are hypersensitive on the issue, and given inflation’s historic impact on equity prices, it’s hard to blame them. I think it’s far too premature to worry over this issue. In fact, isn’t it good news for business that people are getting raises?

Fortunately for us, our Buy List only lost 1.51% on Thursday. Of course, our goal is to make money, not suck less than the overall market. However, Thursday’s reaction tells us that investors aren’t fleeing high-quality names as much as they are the more speculative stocks. The good economic news for this week was a stronger-than-expected GDP report for Q2. We also had a Fed meeting and several more Buy List earnings reports, but first, let’s take a closer look at the surprisingly good GDP report for Q2.

Second-Quarter GDP Grows by 4%

Over the past few months, we’ve gotten lots of evidence indicating that the economy shook off a poor start to the year. A few weeks ago, I said that real GDP growth for Q2 even had a chance of being as high as 4%. Well, that’s exactly what happened.

On Wednesday, the Commerce Department reported the U.S. economy grew in real terms at an annualized rate of 4% for the second quarter. That makes it the third-strongest quarter in the last eight years. This is very good news, and it’s a nice follow-up to the lousy performance for Q1. Technically, the strong number for Q2 was aided by inventory rebuilding. Interestingly, the opposite effect is what hindered GDP during Q1. Stripping out the impact of inventories, the turnaround in the economy from Q1 to Q2 wasn’t quite so dramatic.

The positive GDP news shouldn’t be that much of a surprise, since it confirms lots of other data we’ve seen, like jobs and corporate earnings. It’s interesting to note that one of the most accurate forecasters has been stock prices. Now we know why the market has been so happy!

Also on Wednesday, the Federal Reserve announced, as expected, yet another tapering. Slowly but surely, the economy is returning to something resembling normal. Starting in August, the Fed will purchase $25 billion worth of bonds each month. That’s $15 billion in Treasuries and $10 billion in mortgage-backed securities. There was one dissenter from this week’s FOMC statement: Charles Plosser, the head of the Philly Fed. Plosser thinks the Fed will have to keep rates low for a significant time after QE is done. I think he may be right, but honestly, that’s looking out pretty far ahead.

The earnings news for Q2 continues to be quite good. Of the S&P 500 companies that have reported so far, 76% have beaten analysts’ expectations, while 66% have topped their sales expectations. Unlike previous quarters, we didn’t need dramatic low-balling going into earnings season to get their earnings surprises. We’re not seeing blistering growth. Rather, it’s a lot of steady growth that’s been heavily aided by share buybacks.

Now let’s take a look at some of our recent Buy List earnings reports.

Moog Is a Buy up to $71 per Share

Last Friday, shortly after I sent you last week’s CWS Market Review, Moog ($MOG-A) reported fiscal Q3 earnings of $1.08 per share. That was four cents better than expectations. The problem was guidance. For all of 2014, Moog now says it expects earnings of $3.65 per share. Since we know that Moog has already made $2.59 for the first three quarters of their fiscal year, that translates to expected earnings of $1.06 per share for fiscal Q4, which ends in September. Wall Street had been expecting $1.15 per share. For 2015, Moog now expects EPS of $4.25. Wall Street had been expecting $4.56 per share.

That’s not good, and shares of Moog took a big tumble last Friday, but the stock has found a floor around $66 per share. I still like Moog a lot. The stock has done well for us, but I’m trimming our Buy Below to $71 per share. Let’s not lose sight of the fact that Moog’s “disappointing” guidance is still for earnings growth of more than 16%, and the shares are going for about 15.5 times next year’s estimate. Moog is a good stock.

AFLAC Is a Bargain below $60

We had three earnings reports on Tuesday. AFLAC ($AFL) reported Q2 operating earnings of $1.66 per share, which was seven cents more than consensus. Remember that with insurance stocks, it’s better to look at their operating earnings to get a better sense of how the underlying business is doing.

The problem for AFLAC continues to be the dollar/yen exchange rate. Fortunately, the damage was far less than it’s been in previous quarters. AFLAC said they lost three cents per share due to forex. The company was also hurt by poor sales of new insurance premiums. That’s a bit more troubling, but I think AFLAC can close the gap.

As for guidance, CEO Dan Amos said, “If the yen averages 100 to 105 to the dollar for the third quarter, we would expect earnings in the third quarter to be approximately $1.38 to $1.47 per diluted share. Using that same exchange-rate assumption for the remainder of 2014, we would expect full-year reported operating earnings to be about $6.16 to $6.30 per diluted share.” Wall Street had been expecting $1.44 per share for Q3 and $6.24 per share for all of this year.

Even though AFL’s guidance range covered expectations, the stock got punished this week. On Thursday, the stock closed below $60 for the first time in nearly a year. I still like AFLAC; it’s a solid stock. But due to the recent pullback, I’m lowering my Buy Below to $66 per share; the stock is especially cheap below $60.

Express Scripts Rallies after Good Earnings

The big winner this week was Express Scripts ($ESRX). The stock rose 2.1% on Tuesday, ahead of the earnings report. ESRX then jumped another 5% on Wednesday after the report. What’s interesting is that ESRX has been a pretty poor performer for us over the past five months. The lesson here is that good stocks will have their day; it just takes some patience.

Now let’s look at earnings. The pharmacy-benefits manager reported Q2 earnings of $1.23 per share, which was one penny better than expectations. Express Scripts also slightly narrowed their full-year range. The previous range was $4.82 to $4.94 per share. Now it’s $4.84 to $4.92 per share. The good news was that sales only fell 4.8% to $25.11 billion. Wall Street was expecting a 7.6% slide to $24.38 billion.

I said last week that our $74 Buy Below for ESRX was probably too high, but I didn’t want to change it just yet. I’m glad we didn’t, because I now think $74 is just right. Express Scripts is a very good stock.

Fiserv Beats by a Penny

Fiserv ($FISV) is one of those fairly dull stocks that regularly churns out impressive earnings. If you’re not familiar with Fiserv, they do a lot of outsourcing for the financial-services industry. Three months ago, the company had a great earnings report, so I tempered my expectations this time. Fortunately, Fiserv came through again. On Tuesday, Fiserv reported Q2 earnings of 81 cents per share, which was a penny better than expectations.

CEO Jeffery Yabuki said, “Our second quarter’s results are in line with expectations, and helped fuel a meaningful increase in our adjusted internal revenue growth in the first half of the year compared to 2013.”

I had a feeling that Fiserv was going to alter their full-year guidance, and indeed they did. Fiserv raised the low end of their full-year forecast by three cents per share. The company now expects 2014 earnings to range between $3.31 and $3.37 per share. To give you some context, FISV made $2.99 per share for last year. Fiserv remains a solid buy up to $64 per share.

DirecTV Is a Conservative Buy up to $95 per Share

On Thursday, DirecTV ($DTV) reported earnings of $1.59 per share for the second quarter. That was six cents better than expectations. As we’ve come to expect, DTV’s business in Latin American is en fuego. Last quarter, they added 543,000 subscribers in the region. That’s up more than threefold from a year ago. DirecTV now has 12.5 million subscribers in Latin America.

As good as these results are, don’t expect much action out of DTV. The stock is largely a bet that the AT&T deal will go off at $95 per share. Unfortunately, I can’t say when or if the deal will be completed, but I would say it’s quite likely. Direct remains a conservative buy up to $95 per share.

Next Wednesday, August 6, Cognizant Technology Solutions ($CTSH) will be the final Buy List stock to report for the June reporting cycle. (Medtronic and Ross Stores are our only two Buy List stocks with quarters ending in July, so they’ll report later in August.)

In May, Cognizant told us to expect Q2 earnings of 62 cents per share. Their full-year estimate is for EPS of at least $2.54. Shares of CTSH have traded in a very narrow range over the last six weeks. Look for a modest earnings beat, but I would be especially glad to see higher full-year guidance. Cognizant is a buy up to $52 per share.

That’s all for now. We get a few turn-of-the-month economic reports next week. Factory orders and ISM Services are on Tuesday. The trade report is on Wednesday, which could impact any revisions to the GDP report. Cognizant also reports on Wednesday. Consumer credit is on Thursday, and the Productivity report is on Friday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His