-

Morning News: July 9, 2014

Posted by Eddy Elfenbein on July 9th, 2014 at 6:47 amWhy UBS Says Brazil’s 7-1 Trouncing Is Bearish for Stocks

Wall Street Aims to Clear Low Bar For Earnings Season

Why Alcoa Gained and The Container Store Tumbled As Earnings Season Kicks Off

Trucks Left In The Dust as China Vehicle Market Races Ahead

Chinese Teens Beat U.S. Peers in Money Smarts

Vatican Bank Profits Tumble as Pope Francis Orders an Overhaul

Carlos Slim to Dismantle Mexican Empire

Fed’s Kocherlakota Gives Lukewarm Welcome to U.S. Unemployment Drop

Citigroup Is Said to Be Close to Settling Inquiry Into Mortgage Securities

Amazon Offers Authors 100% of Sales Amid Dispute

European Companies See Opportunity in the ‘Right to Be Forgotten’

GM Korea Workers Approve Strike as Wage Talks Stall

Joshua Brown: 361 Capital Weekly Research Briefing

Jeff Carter: How to Kill Your Company

Be sure to follow me on Twitter.

-

Capitalism – Born in England, Nourished in America

Posted by Eddy Elfenbein on July 8th, 2014 at 11:25 pmCapitalism – Born in England, Nourished in America

By Gary Alexander

Navellier MarketmailThe Bank of England was born 320 years ago, in July 1694. Here’s a short description of that important event from “War and Gold: A 500-Year History of Empires, Adventures and Debt,” by Kwasi Kwarteng:

“The setting up of the Bank of England allowed the government to borrow more cheaply. The initial amount raised was 1.2 million pounds at a time when total government spending in any given year was not much more than this sum. This money was raised by individuals pledging or ‘subscribing’ to lend certain amounts…There was an initial cap of 20,000 pounds for each individual subscription.

“The subscription books were opened in the Mercers’ Chapel on 21 June, 1694. A total of 300,000 pounds, a quarter of the initial sum, was subscribed on the first day. By noon on 2 July, in less than 11 days, the whole of the amount had been raised. There were over 1,200 subscribers and the very first names on the list were those of the King and the Queen, who subscribed 10,000 pounds jointly.”

The Bank of England, in turn, paid 8% a year interest, a relatively high rate even then. The Bank of England was privately owned for over 250 years, until it was nationalized by Atlee’s Labor Party in 1946.

In his 1930 Treatise on Money, British economist John Maynard Keynes wrote that the modern age began with the accumulation of capital in the 16th century, “which resulted from the treasure of gold and silver which Spain brought from the New World to the Old.” Keynes claimed this “profit inflation… created the modern world.” Capital creation “commenced in 1519 when the Aztec spoils arrived, and terminated as early as 1588, the year of the Armada.” However, Spain’s power soon eclipsed because it spent its gold on Armadas, rather than banking it and using the new assets as the basis for loans.

The British and the Dutch were able to build banking and stock market systems, while Spain created sinking assets – wooden ships. France also went the wrong direction. In the same year the Bank of England was founded, 1694, Scotsman John Law fought a duel in London, killing Edward Wilson. Law was sentenced to death, but he mysteriously escaped and fled to Amsterdam, where he picked up some lessons from Europe’s oldest stock exchange, founded in 1609 by the Dutch East India Company. Law then migrated to France where he created one of the great bubbles of all time, the Mississippi Company. His unique idea was to sell paper representing the hope of finding gold or silver in swampy delta land.

John Law consolidated the considerable debts of the spendthrift kings of France by creating shares in this pipedream of gold in America, specifically along the Mississippi River. Shares multiplied 60 fold from 1716 to 1719. Like 1929 or 1999, commoners reaped princely fortunes. Law promised that France would dominate all of Europe, and he could “ruin England and Holland” whenever he pleased, but Law’s Papier-mâché empire fell apart in early 1720 and Law fled Paris to seek his fortune in other European cities.

While France’s fortunes faded – in part due to the despotism which grew out of the French Revolution (225 years ago next Monday) – Britain continued to prosper throughout the 1800s. Between the fall of Napoleon in 1815 and World War I in 1914, Britain’s per capita wealth quadrupled, in real terms.

British historian Niall Ferguson wrote in The Cash Nexus that “Between 1816 and 1899, the UK government ran a deficit in excess of 1% of GNP in only four years.” This was the golden era, literally. Historian A.J.P. Taylor wrote in The Origins of the Second World War that the British people “reared in the stable economic world of the later nineteenth century” assumed that “a country could not flourish without a balanced budget and a gold currency.” The terrors of World War I put an end to that belief.

-

Reynolds and Lorillard Look to Merge

Posted by Eddy Elfenbein on July 8th, 2014 at 2:23 pmOne of my former Buy List stocks, Reynolds American ($RAI), is looking at a major merger with Lorillard ($LO). No deal has come forth yet, but both companies seem to be seriously interested. There’s been talk about some sort of deal for a long time, but now, it’s getting serious. I think we can expect some news by the end of the month.

Tobacco has been a great sector for investors and both stocks have done very well over the last several years. There are a lot of hurdles to a potential RAI-LO deal (legal, anti-trust, divestitures, etc.) Right now, the tobacco industry is very profitable. They’re not exactly monopolies, but some of the dynamics are the same. RAI pays a big fat dividend of 4.3%.

Overall, I’m not a big fan of deals like this. I think both companies would rather not do this deal. Mergers done out of fear are often bad omens. My other concern is that after years of above-market gains, these stocks are no longer the bargains they used to be.

-

The Bond Market Is Holding Up

Posted by Eddy Elfenbein on July 8th, 2014 at 10:18 amThe stock market is down again today. The S&P 500 is currently holding around 1,966. What’s interesting is that the small-caps have been in serious retreat. The little guys have been trailing the market since the beginning of the month. The Russell 2000 broke 1,200 last week. It’s now close to 1,170. Remember that that index tends to be weighted towards domestic manufacturers.

I continue to be surprised by the strength of the bond market. Despite more evidence of a stronger jobs market, and a wee bit more inflation, Treasury yields are holding firm. The yield on the 10-year had bounced up to 2.7% last week, but it’s now back down to 2.57%.

There’s not much going on in the market until earnings season begins later this month. Alcoa ($AA) is the first major company to report after today’s close. But after that, there’s not much until Wells Fargo ($WFC) reports on Friday.

Shares of Amazon ($AMZN) are weak today. The stock plunged from $408 in January to $284 by May. It’s been trying to rally since then. I’ve always thought Amazon was way overpriced and I’ve been consistently wrong about that.

-

Morning News: July 8: 2014

Posted by Eddy Elfenbein on July 8th, 2014 at 6:46 amEuro’s Reserve Appeal Fades as ECB Prompts Decline

Macro Horizons: More Bad News From Germany

Commerzbank Said Next to Face Penalties in U.S. Probe

Here’s What Temasek Bought Over the Past Year

Brent Oil Erases Iraqi Rally in London as Futures Retreat

Gold Shines Again as Hedge Funds Boost Wagers on Advance

Soybeans Slide for Seventh Session on Harvest Prospects

Smartphones Weigh on Samsung Elec as Guidance Disappoints

GM Korea CEO Warns of Output Cut as Strike Vote Looms

BMW Brand Auto Sales up 7.3% in June in China, US

Air France-KLM Shares Hit by Profit Warning

Crumbs, The Cupcakery That Couldn’t, Closes Up Shop

Box Raises $150 Million In Cash And Reports 2014 Sales Growth As It Crawls Toward IPO

Epicurean Dealmaker: You Go First

Howard Lindzon: Web Video Mega Trend Continues, The Future of (Digital) TV… and a TubeMogul Update

Be sure to follow me on Twitter.

-

Morning News: July 7, 2014

Posted by Eddy Elfenbein on July 7th, 2014 at 6:52 amEuropean Stocks Drop With Treasuries as Commodities Fall

Lagarde: Global Economic Recovery Could Be ‘Less Robust Than Expected’

China Q2 GDP Seen Steady at 7.4%, Recovery In Sight As Stimulus Kicks In

Oil Slips Towards $110 as Supply Fears Fade

Defense Trade Coming Undone in $2 Trillion S&P 500 Rally

Carney’s Hawkish Turn Seen Setting Fashion for Yellen

Gowex, The Spanish Wi-Fi Firm, Admits to False Accounts For Four Years

Still-Divided Washington Readies for Start of Recreational Marijuana Sales

Helvetia Agrees to Buy Nationale Suisse for $2 Billion

TeliaSonera Agrees to Buy Tele2 Norway for $744 Million

ADM Expands Food-Ingredient Offering with Acquisition of WILD Flavors

Lafarge, Holcim Lay Out Asset Sales Needed for Merger

In Discounter War, Will Aldi’s Coke Rush Fall Flat?

Credit Writedowns: The Euro Crisis: Muddling Through, or The Way To a More Perfect Euro Union?

Jeff Miller: Weighing the Week Ahead: Time for a Mid-Course Correction?

Be sure to follow me on Twitter.

-

Happy Birthday, America!

Posted by Eddy Elfenbein on July 4th, 2014 at 9:48 am

-

CWS Market Review – July 4, 2014

Posted by Eddy Elfenbein on July 4th, 2014 at 7:07 am“We hold these truths to be self-evident, that all men are created equal.”

I hope everyone is having a wonderful Fourth of July weekend. The stock market is closed today in honor of Independence Day, but we had an eventful—albeit shortened—trading week.

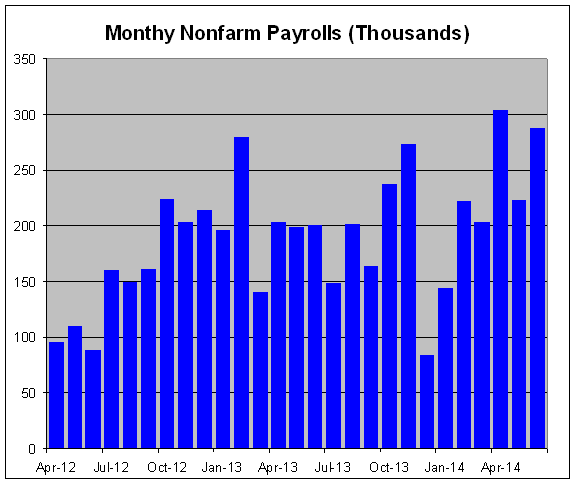

The big news was Thursday’s excellent jobs report. The economy added 288,000 jobs last month. That was far more than expected, and it marked the first time the U.S. economy has added more than 200,000 for five straight months since the Tech Bubble (check out the chart below). The unemployment rate dropped to 6.1%, which is its lowest level since September 2008, the same month that Lehman Brothers went kablooey.

The good economic news helped power the stock market to more new highs. On Thursday, the Dow Jones Industrial Average topped 17,000 for the first time. The index needed only 227 days to rise from 16,000 to 17,000. For some context, the Dow first broke 1,700 on February 21, 1986, so we’re up 10-fold in a little over 28 years. The S&P 500 also broke into record territory. The index finished the week at 1,985.44 for its 25th all-time closing high this year.

In this week’s CWS Market Review, we’ll take a closer look at the jobs report and focus on what it means for us and our portfolios. I’ll also run down how our Buy List did during the first half of the year. I also want to discuss a few of our Buy List stocks. Second-quarter earnings season begins in a few days, and I expect to see good results from our stocks. Wells Fargo ($WFC) will be our first Buy List stock to report next Friday. I’ll have more on that in a bit. But first, after a long winter, the U.S. jobs market is finally showing some strength.

The U.S. Economy Created 288,000 Jobs Last Month

Since the market is closed today, Jobs Day fell on a Thursday this month. Jobs Day, of course, is very important on Wall Street. Investors around the world stop what they’re doing to see what the government has to say. The monthly jobs report is probably the best month-to-month barometer of how well the economy is doing. It’s also the report that the Fed watches most closely. We know that Fed policy is largely determined by the jobs market, or at least where they think the jobs market is going.

Yesterday, the Department of Labor said that the U.S. economy created 288,000 net new jobs last month. That’s a very impressive number. Economists were expecting an increase of 215,000. (I was much closer with my guess.) On top of that, the jobs gains for April and May were revised higher.

In the last five months, the U.S. economy has created 1.241 million jobs. I was also pleased to see that the jobs-to-population ratio finally topped 59%. The ratio had been stuck between 58% and 59% for a staggering 57 months in a row. The story had been that any gains in the employment rate were caused by folks leaving the job market. That’s still a factor, but make no mistake, there’s real hiring going on as well.

The unemployment rate fell to 6.1%, which is its lowest level in more than five years. In March, the Federal Reserve released its economic projections for 2014. The central bank saw unemployment between 6.1% and 6.3% by the end of this year. Well, things have been running ahead of schedule. Last month, the Fed revised its year-end range to 6.0% to 6.1%. The economy looks to beat that soon. The year’s only halfway done, and we’re already at 6.1%. After years of consistently overestimating the economy, the Fed has apparently underestimated the strength of the jobs market.

This week, we also had another good ISM report. For June, the ISM Manufacturing Index came in at 55.3, which was 0.1 below May’s report. The manufacturing sector came very close to increasing its growth rate for five months in a row. On Wednesday, the factory-orders report for May was sluggish (-0.5%); however if you exclude military hardware, then orders rose by 0.2%.

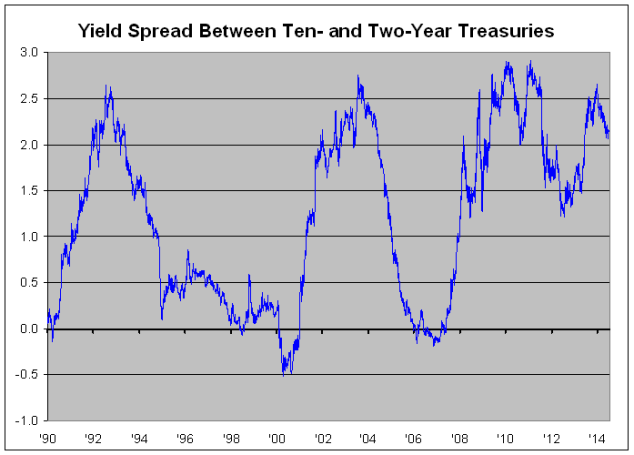

Of course, the ultimate judge of the economy is the notoriously ornery bond market. However, to be fair, the bond market has been well behaved. We all know how the bond market can act like World Cup soccer players—writhing around in spurious agony when they’ve been lightly grazed by another player. The strong jobs report pushed the yield on the 10-year Treasury up to 2.65%, which is still quite modest. After all, the yield is 28 basis points lower than where it started the year.

Watching the bond market is important because that, combined with the Fed’s plans, is the key to the stock market. With the economy running ahead of the Fed’s projections, I think Janet Yellen could alter her plans. I still think the Fed will taper QE at each meeting this year. That way, it will be completely wrapped up by January 1st. Previously, Chairwoman Yellen said to expect the first rate increase “something on the order of six months” after QE is done. That would be about one year from today. Now I think that date will be pushed up to the first quarter of 2015. As I’ve mentioned before, there are now signs that inflation is starting to heat up.

Here’s my take: As long as the yield curve is wide, meaning the difference between long-term and short-term interest rates is big, that’s good news for stocks. But that’s not going to last forever. Long-time readers know that I’m a fan of Dr. Twotenspread, one of the greatest economic forecasters of all time. The spread between the ten- and two-year Treasuries has been far more accurate than a lot of higher-paid folks on Wall Street (see the chart above). On Thursday, the two-year yield got to 0.52% for the first time since last September, and it’s very close to making a three-year high. But the spread between the two and ten is still a very bullish 213 basis points.

The bottom line is that this is a very good environment for stocks. Valuations have climbed, but they’re not excessive. Earnings are growing, and we’ll see more evidence of that once Q2 earnings season starts. We should also remember that stock prices have chilled out in a major way. Volatility is the lowest it’s been in years. The S&P 500 has now gone 34 days in a row without a gain or loss of more than 0.8%.

Buy List First-Half Review

This past Monday was the final trading day of the first half of 2014, and I wanted to update you on the Buy List’s performance. The good news is that we’re in the black. The bad news is that we’re trailing the market, but not by much.

Through Monday, our Buy List was up 1.99% for the year, while the S&P 500 was up 6.05%. If we include dividends, then the Buy List gained 2.70% through Monday, compared with 7.14% for the S&P 500.

At the end of the first quarter, our Buy List was ahead of the S&P 500. But during Q2, we had a small loss (-0.09%), while the market rallied 4.69%. Part of the reason is our big losers like Bed Bath & Beyond and Ross Stores. All by itself, our BBBY position knocked 1.6% off our YTD gain. Another weakness is that we don’t have any energy stocks, and that sector has heated up since March.

For the first half, our biggest winner was DirecTV (+23.1%), followed by Wells Fargo (15.8%) and Stryker (12.2%). Our biggest loser was, not surprisingly, Bed Bath & Beyond (-28.5%), followed by CA Technologies (-14.6%) and Ross Stores (-11.7%).

As I’ve mentioned many times, our Buy List has beaten the market for the last seven years in a row. Even though we’re trailing the market now, I have no plans to depart from our proven strategy. We’re not even close to being out of it, and I’m confident we can catch the S&P 500 before the year is up. Now let’s look at some recent news affecting our stocks.

Buy List Updates

Wells Fargo ($WFC) will start earnings season for us next week. The bank is due to report Q2 earnings on July 11, before the opening bell. The stock just made another new 52-week high yesterday. Wall Street expects quarterly earnings of $1.01, which WFC should be able to top. The shares have done well for us this year, but Wells is far from fully priced. The bank is currently going for less than 13 times this year’s earnings estimate. Plus, it yields more than 2.6%. For now, I’m going to keep our Buy Below somewhat tight. Wells Fargo remains a very good buy up to $54 per share.

Oddly enough, Bed Bath & Beyond ($BBBY) showed some life on Thursday as the shares gained 2.7%. There’s been some talk of a potential buyout, but it seems to be only rumors for now. For now, I’m keeping our Buy Below at $61 per share.

On Thursday, shares of Ford ($F) closed at $17.32, which is its highest closing price since October. On Tuesday, the auto maker reported a monthly sales decline, but that’s due to some technical factors as Ford retools its production facilities. Overall, sales fell by 5.8%, but that was less than expected. The good news is that Fusion sales were up 14%. Ford is due to report Q2 earnings on July 24. Wall Street currently expects earnings of 38 cents per share. Ford remains a solid buy up to $18 per share.

That’s all for now. Next week will probably be fairly quiet. Most of the Wall Street big shots are chilling at the Hamptons. Alcoa will kick off earnings season on Tuesday. Our own Wells Fargo is due to report on Friday morning. On Wednesday, the Fed will release the minutes of its last meeting. Traders will scour the minutes for any hint of tight money, but I doubt they’ll find it. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: July 4, 2014

Posted by Eddy Elfenbein on July 4th, 2014 at 6:35 amDecline In German Factory Orders Exceeds Expectations

European Shares Pause After Bumper Week; Erste Sinks on Warning

China’s Top Paper Dismisses Fears Hong Kong Autonomy Being Eroded

China Stocks Cap Second Weekly Gain on Economic Growth Optimism

Win or Lose, It’s Where the Game Is Played That Matters in Britain

Gold Advances as German Orders Seen Denting Optimism

Central Bankers Fire Back at Their Own Club Over Bubbles

U.S. Jobs Report: 288,000 Positions Added

US Trade Deficit Drops to $44.4 Billion in May

GM Suspends South Africa Production as Striking Union Rejects Offer

China Approves Lenovo, IBM $2.3 Billion Server Deal

SunTrust Reaches U.S. Settlement Over Mortgage Modifications

Cullen Roche: Where Did All the Keynesians Go?

Roger Nusbaum: Downsizing = Empowerment

Be sure to follow me on Twitter.

-

Booze at the Fed

Posted by Eddy Elfenbein on July 3rd, 2014 at 5:44 pmDavid Wessel notices this factoid from the Inspector General’s report on the Fed:

The policy states that alcohol cannot be served at events where only Board employees are present. Further, for events where alcohol is served, service is limited to a 90-minute period and cannot begin before 5:30 p.m. These requirements apply to events held at Board and non-Board facilities.

So they really do take away the punchbowl.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His