-

Good ADP Report, Bad Factory Orders

Posted by Eddy Elfenbein on July 2nd, 2014 at 10:45 amAnother quiet morning on Wall Street. The S&P 500 is holding just below its all-time high. Interestingly, IBM has been perking up so far in Q3. The stock gained 2.8% yesterday and it’s up another 1% today.

Tomorrow is the big jobs report but we got a preview today with the ADP report. According to the private payroll firm, the economy added 281,000 private sector jobs last month. That easily beat Wall Street’s estimate of 210,000. I think tomorrow’s report could be a big one.

On the downside, the Commerce Department said that factory orders dropped 0.5% in June. Excluding military stuff, factory orders rose 0.2% last month.

-

Morning News: July 2, 2014

Posted by Eddy Elfenbein on July 2nd, 2014 at 7:04 amWorld’s ATM Moves to Frankfurt as Yellen’s Fed Slows Cash

Hong Kong Stocks Close at Year’s High on Factory Data

German, French Defense Companies Plan Alliance

Orange Fails to Reach Deal on French Wireless Consolidation

Puerto Rico Downgrade Raises Default Fears

Google in Deal for Songza, a Music Playlist Service

McDonald’s, Taco Bell, KFC Laggards in U.S. Fast-Food Survey

Nike Is Dominating The World Cup – Here’s Why

Seragon Pharmaceuticals Announces Acquisition Agreement With Genentech

How Can GM, Embroiled in a Recall Crisis, Continue to Post Strong Sales?

BNP Growth Plan at Risk as Penalties to Mar U.S. Expansion

Jamie Dimon Diagnosed With Throat Cancer: What He Can Expect

Coatue Bids Farewell to Noto Before He Starts

Roger Nusbaum: Alternative Investments: The Right Expectations

Jeff Carter: Now Is The Time to Invest in VC

Be sure to follow me on Twitter.

-

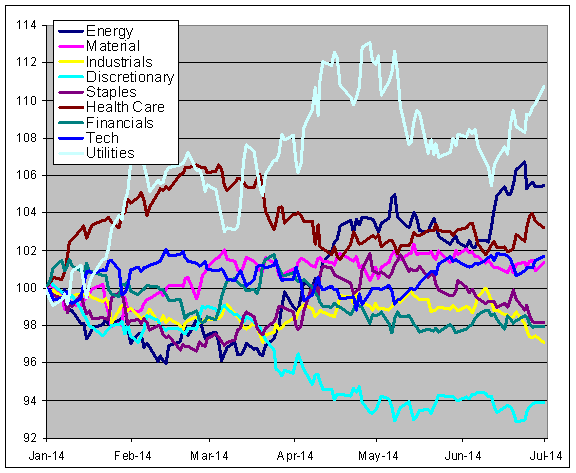

Breaking Down the Year So Far

Posted by Eddy Elfenbein on July 1st, 2014 at 12:03 pmHere’s a look at the relative strength graph so far this year. I took each of the Total Return Indexes for the S&P 500 sectors and divided them by the S&P 500’s Total Return Index. I then set each one to 100 to start the year.

In plainer terms, a rising line means a sector is beating the market and a falling one means it’s losing. I apologize if this chart is hard to read but it’s a good way to see what’s been working this year and what hasn’t. (I didn’t include telecom since it’s only a few stocks and I didn’t want to crowd the graph.)

Healthcare and Utilities ran out for a quick lead at the start of the year, but healthcare has been rather weak since. Materials stocks were strong in February. Starting in March, Energy stocks started coming on strong. That probably explains some of the weakness in our Buy List since we don’t have any Energy stocks. The best performing sector YTD is Utilities (+18.655). The worst is Consumer Discretionaries at +0.6%.

Utility stocks started trailing the market in May, but have been leading the market over the past few weeks. In fact, a quiet theme this year has been the leadership tug-of-war between Utility stocks and Energy stocks. This probably reflects competing theses on the economy.

It’s also interesting to see how poorly Consumer Discretionaries have been doing. Bear in mind that this sector had been crushing the market for more than four years.

-

June ISM = 55.3

Posted by Eddy Elfenbein on July 1st, 2014 at 11:31 amWe had another good ISM Manufacturing number. For June, it was 55.3. This was 0.1 below last month’s number. If we had topped that, it would have been our fifth monthly increase in a row.

The ISM has now been 49.0 or better for 60 months in a row. As I’ve discussed before, this is one of the better recession indicators. We’re still in the safe zone.

-

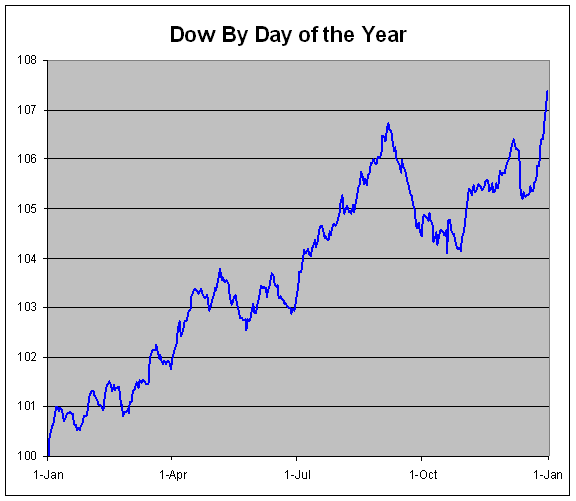

The Mid-Year Rally

Posted by Eddy Elfenbein on July 1st, 2014 at 11:21 amWe’ve all heard about the Santa Claus Rally, but there’s a smaller historical rally that takes place around the middle of the year.

I crunched the numbers for the entire Dow’s history going back to 1896 and found that the index gains an average of 1.18% from June 29 to July 9. That may not sound like a lot but consider what it means: 16% of the Dow’s entire capital gain for the year has come over a seven-day span. (The Santa Claus Rally is a more impressive gain of 2.94% from December 20 to January 7.)

Historically, this mid-year seven-day spurt kicks off the big Summer Rally. The Dow has gained, on average, 3.69% from June 29 to September 6. That’s almost exactly half the Dow’s average yearly gain coming in just over two months.

-

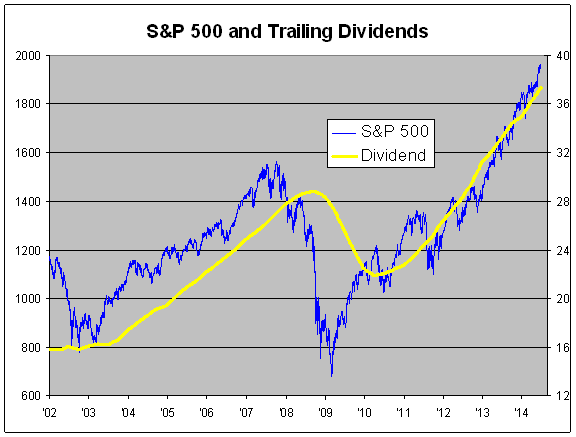

Another Big Quarter for Dividends

Posted by Eddy Elfenbein on July 1st, 2014 at 10:59 amThe numbers are in and it was another good quarter for dividends. The S&P 500 paid out $9.76 in dividends last quarter. That’s the index-adjusted number (each dollar in the index is about $8.9 billion). That’s an increase of 13.4% over a year ago.

Dividends have now grown at a double-digit rate for 13 of the last 14 quarters. It would have been an even 14 for 14, but there was a dividend surge in Q4 of 2012 to beat the tax increase. As a result, dividends rose by 6.6% in Q4 of 2013. But adjusting for that, the dividend trend is still quite strong. Dividends paid out this year will probably be about 75% higher than they were four years ago.

Here’s an interesting stat: First-half dividends are up 14.4% from last year’s first half, while the S&P 500 is up 6.05% YTD. Annualized, that’s about 12.5%. In other words, dividends are growing faster than stock prices.

Believe it or not, the market’s dividend yield is slightly higher now than it was at the beginning of the year. I’m not saying that’s a perfect measure of value because it’s welcome push-back against this silly bubble talk.

The big drag on dividends is still the financial sector. Major banks like Citigroup and Bank of America only pay a penny per share. The Financial Sector ETF ($XLF) will probably pay out around 38 cents per share this year. In 2007, it paid 86 cents per share.

Here’s a look at the S&P 500 and its trailing dividends since 2003. The S&P 500 is the blue line and it follows the left scale. Dividends are in yellow and follow the right. The two lines are scaled at 50-to-1, so whenever the lines cross, the dividend yield is exactly 2%. For such a crude measure, that 2% line has worked pretty well.

-

Morning News: July 1, 2014

Posted by Eddy Elfenbein on July 1st, 2014 at 6:35 amGerman Jobless Rises Unexpectedly in June

Japan Firms See Bigger Spending, Outlook Mixed: BOJ Tankan Survey

Aussie Dollar Parity Talk Resumes

U.S. Imposes Record $9 Billion Fine on BNP in Sanctions Warning to Banks

Eyes on Impact of BNP Paribas Fine For Euro After Flat Inflation

US Farmers Plant Record Soybean Crop, Less Corn

GM’s Record Recall Expands: Is the Brand at Risk?

Symantec Warns of Hacker Threat Against Energy Companies

Samsung’s China Labor Problems Persist

Peltz’s Trian Plants Its Flag in BNY Mellon

CytoSport® To Be Acquired By Hormel Foods Corporation

Ex-American Apparel CEO Dangerously Close to Majority Control

Whopping Fine Could Change the Way Fundraisers for Charity Operate

Cullen Roche: A Cheat Sheet for Understanding the Different Schools of Economics

Epicurean Dealmaker: Touring Test

Be sure to follow me on Twitter.

-

Buy List First-Half Summary

Posted by Eddy Elfenbein on June 30th, 2014 at 5:20 pmThe first half of the year is on the books. Our Buy List managed a small gain of 1.99% compared with the S&P 500’s gain of 6.05%. Including dividends, our Buy List is up 2.70% while the S&P 500 is up 7.14%.

The second quarter was rough for our Buy List. We beat the market in Q1, but during Q2, the Buy List had a small loss of 0.09% while the S&P 500 gained 4.69% (not including dividends). Our “beta” this year is 0.9958.

What’s interesting is that we can see an old lesson with our Buy List this year. The big duds are weighing us down much more than the winners are helping us.

Nine of our 20 stocks are beating the market, and a tenth is very close. Most of our stocks are doing just fine, but it’s the big losers that are causing the most harm. Bed Bath & Beyond is down 28.5% which is more than twice as much as our second biggest loser. All by itself, our BBBY position knocks off 1.6% to our YTD gain.

Here’s our stock-by-stock first-half performance (sans dividends):

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His