-

Are We in a Bubble?

Posted by Eddy Elfenbein on November 11th, 2013 at 10:44 amThe latest rage on Wall Street is to pronounce that stocks are in a bubble. This is rather unusual in that true bubbles are very rare. This is, of course, different from stocks dropping in a routine lousy market. That happens every few years.

Do I think that stocks are in a bubble? Honestly, I don’t know. And more importantly, I don’t much care. Let me explain.

For one, it’s odd to make a judgment about the aggregation of 6,000 publicly traded stocks. Our Buy List is pretty well diversified and that’s just 20 stocks. Where the entire S&P 500 is headed isn’t that important for a disciplined stock picker.

Also, even if the market is about to plunge, it’s very difficult to get the timing just right. Lots of people saw the housing bubble but they were very early. The bubble kept on going. Recently I noted that if an investor bought an S&P 500 index fund just prior to the Financial Crisis, say in March 2008, and held on to today, they would have made a decent return by historical standards. Time may not heal investing wounds, but it sure can help a lot.

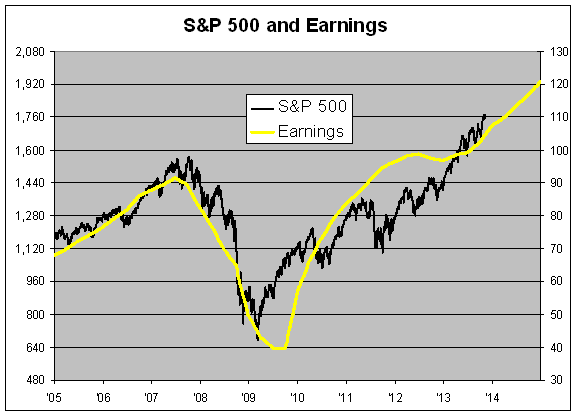

When looking at valuation metrics, I urge investors to look at as many as they can, but never be a slave to just one. I’m particularly leery of metrics like the Cyclically Adjusted P/E ratio, also known as CAPE. The CAPE looks at the stock market’s current value weighted against the last ten years of earnings. The idea is to smooth out the economic cycles. I think this is a bad idea because stocks and earnings are themselves cyclical.

Also, the inclusion of so much prior data is, in my opinion, an unfair anchor to carry. The historic plunge in corporate earnings in 2008-09 will still be a part of CAPE for another five years. If we look at operating earnings or dividends, we can see what an outlier that profit data is. Interestingly, the market’s dividend yield has remained fairly consistent for the last decade, except for the worse parts of the Financial Crisis.

After two of the biggest bear markets in history is precisely when so many people are scared of another bubble. I’m reminded of people saying that shortly after 9/11 was actually the safest time to fly. Bubbles are now, apparently, everywhere.

I think the best way to look at the issue is to divide bear markets into two categories. One is where price shoots far above value. That’s your classic bubble ala 1987 or 2000. The second is when value crumbles beneath price. That happened in 1990 and 2008.

You might be surprised to hear me say that 2008 wasn’t a bubble. That’s right; stock valuations really weren’t that excessive. It was the fundamentals that turned out to be terrible. Believe it or not, stock valuations were above average in 1929, but not out of sight. The frothiest part of the bull market occurred in the last six months. The 1920s was not a decade of stock euphoria.

I think there’s a natural tendency to reverse engineer a narrative that the world was enthralled to greed and everyone bought stocks without thought. That describes the feeling about Tech stocks in 1999, but it’s not an accurate description of today’s environment. The S&P 500 is going for about 17 times this year’s earnings. That’s about normal. The P/E Ratio has risen over the last two years, but it’s really gone from low to average, not from normal to nose-bleed territory.

Analysts currently estimate that the S&P 500 will earn $120 per share next year. Now’s the time for skepticism. For one, analysts don’t have a great forecasting track record. The critical question is, could fundamentals soon fall apart? Are there hidden factors that might make the S&P 500 earnings, say, $90 or even less next year? This is the question to worry about.

It’s also hard to predict things that are unexpected because, well, they’re not expected. If they were expected, they probably would be much less interesting. Also, it’s the unexpectedness of an event that makes it important.

The things that worry me are the things we aren’t thinking about. For one, corporate profit margins are very high. I think it’s reasonable to expect that earnings growth will be below economic growth over the next several years. Though the high profit margins probably aren’t a reflection of corporate greed, rather they’re a natural byproduct of slow growth and low interest rates.

Earnings recessions generally don’t announce themselves beforehand, but there are some useful warning signs. One good indicator is the yield curve. When short-term rates rise above long-term rates, the economy often runs into trouble soon after. For now, the yield curve is far from inverted.

Another late cycle indicator is rising inflation. According to the latest numbers, that’s not a problem either. I also like to follow the monthly ISM reports. A reading below 45 is often a sign of trouble. Once again, we’re in the safe zone.

(You can sign up for my free newsletter here.)

-

Scattered Thoughts on Twitter

Posted by Eddy Elfenbein on November 11th, 2013 at 10:21 amJust about everything that could be said about Twitter’s IPO has been said. Still, I wanted to add a few scattered thoughts.

Twitter is another good example of a stock where fundamental analysis is basically useless. By any reasonable valuation metric, Twitter is vastly overpriced. That’s not a novel insight. However, that doesn’t mean Twitter’s stock won’t do well.

The reason is that fundamental analysis assumes a level of environmental consistency that doesn’t exist in Twitter’s business. Who knows what their business will look like in a few years? Yet I have a pretty good idea what Harris’s business will look like. This is why I’m staying away from Twitter. I simply can’t offer a reasonable estimate as to what their profit will be. But I do wish them well.

After a big IPO like Twitter, you often hear that the company “left money on the table.” Perhaps. But I think that misses a few key points.

Remember that Twitter floated a relatively small amount of shares. Look at it from their point of view. One issue is that the company has a lot of people working for them who were paper millionaires, and their wealth was very illiquid. The company doesn’t want to alienate long-time employees. Now that Twitter is public, those people are much wealthier, and even factoring in a lock-up period, their wealth is far more liquid than it was before.

We also have to consider the major benefit of an inflated stock price. Twitter can now print money for free which they can use for acquisitions. In other words, their shares are a currency. Every central bank in the world longs for this. Expect to see Twitter roll up a lot of small tech firms, and they’ll use their stock to close the deal.

When looking at stocks, we often talk about price versus value. But this is a good example of the two concepts blurring. An elevated stock price is itself a boost to value because it can aid your financial strategy. I wouldn’t say that a rich valuation can turn a bad company into a good one, but it has helped many good companies become better.

There isn’t much better defense than owning stocks of firms that know what they’re doing.

-

Morning News: November 11, 2013

Posted by Eddy Elfenbein on November 11th, 2013 at 6:14 amEuro Zone’s Fizzling Growth Seen to Back Draghi Cut Case

German Bonds Climb Before Growth Report as Yield Curve Steepens

Online Shopping Marathon Zooms Off the Blocks in China

Brent Rises After Iran Talks Fall Short of Agreement

Yellen to Get Quizzed as Taper-Timing Debate Rages

Supreme Court to Take Up Challenges to Union Practices

Postal Service to Make Sunday Deliveries for Amazon

Shire Buys U.S. Drug Firm ViroPharma for $4.2 BIllion

Grifols to Acquire a Novartis Diagnostics Business Unit for U.S. $1,675 Million

Transocean Reaches $1.1 Billion Dividend Accord With Icahn

Panasonic Says Ready to Spend $1 Billion on New Deals

If You Believe in Bitcoin, You Should Never Buy Anything in Bitcoin

Jeff Miller: Weighing the Week Ahead: Do Sidelined Investors Face Upside Risk?

Roger Nusbaum: The Dude Who Came Up With 4% Rule Tells Barron’s It Might Not Work and Allowing For The Possibility of Risk

Be sure to follow me on Twitter.

-

Buy List YTD

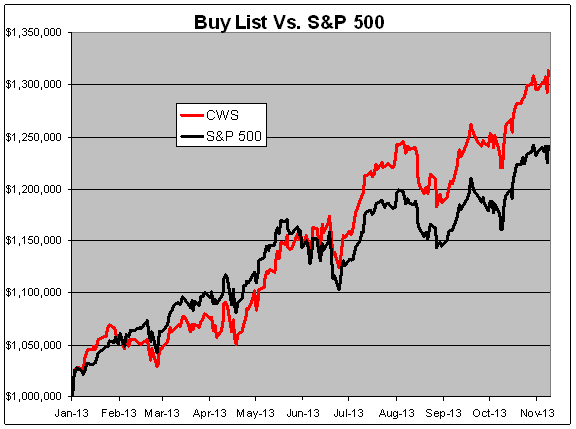

Posted by Eddy Elfenbein on November 9th, 2013 at 4:01 pmThe end of the year is in sight. Through Friday, our Buy List is up 31.34% for the year compared with 24.15% for the S&P 500 (not including dividends). That lead of 7.19% is our largest of the year. At one point in April, we were trailing the S&P 500 by 3.61%.

Company Symbol YTD Return Moog MOG-A 51.16% CA Technologies CA 45.27% Ross Stores ROST 44.37% Medtronic MDT 41.47% Microsoft MSFT 41.45% CR Bard BCR 40.80% Bed Bath & Beyond BBBY 35.50% Stryker SYK 33.77% Fiserv FISV 33.65% Ford Motor Company F 30.12% Harris Corporation HRS 29.94% DirecTV DTV 27.37% Nicholas Financial NICK 26.77% FactSet Research Systems FDS 25.12% Wells Fargo WFC 24.96% AFLAC AFL 23.78% WEX Inc. WEX 23.36% JPMorgan Chase JPM 22.72% Cognizant Technology Solutions CTSH 22.13% Oracle ORCL 3.09% S&P 500 24.15% Spitfire 944

Posted by Eddy Elfenbein on November 8th, 2013 at 4:00 pmReal GDP Per Capita

Posted by Eddy Elfenbein on November 8th, 2013 at 11:45 amHere’s a quick look at Real GDP Per Capita. We’re still below the all-time from 2007.

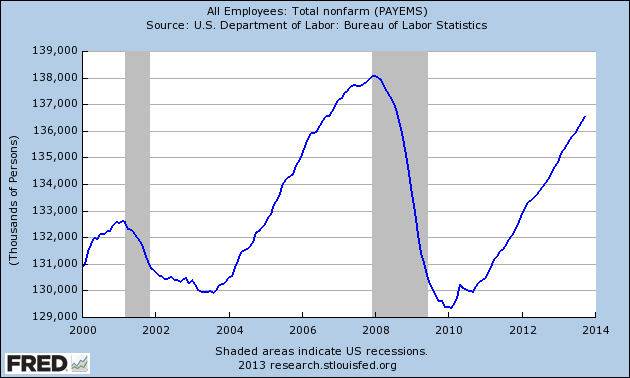

October NFP +204K, Unemployment 7.3%

Posted by Eddy Elfenbein on November 8th, 2013 at 8:58 amThe October jobs report is out. The economy created 204,000 new jobs last month. Plus, the report for September was revised higher by 60,000 and the report for August was revised higher by 45,000.

The unemployment rate ticked up to 7.3%, but if we work out the decimals, the increase was only 0.045%. We now have the lowest jobs-to-population ratio in 27 months.

From peak to trough, NFP fell by 8.736 million in 25 months. In 44 months since the low, we’ve gained back 7.234 million. In seven years, NFP has increased by 1,000.

In October, the number of Americans either unemployed or out of the workforce entirely came to 102.813 million. That’s an all-time high and it’s up 22.3% in 10 years.

CWS Market Review – November 8, 2013

Posted by Eddy Elfenbein on November 8th, 2013 at 7:11 am“Wisely and slow; they stumble that run fast.” – Romeo and Juliet, Act II, Scene 3

Third-quarter earnings season is just about over, and it’s been a fairly good one for Wall Street. The latest numbers show that 442 of the S&P 500 companies have reported so far. Of those, 74% have beaten earnings estimates. It looks like the final numbers will show that earnings grew by 4.1% for Q3. Analysts currently expect to see 6.8% growth for Q4. This continues the earnings-acceleration trend we’ve seen this year.

For our Buy List, this has been an exceptionally strong earnings season. This past week, we saw excellent earnings reports from Cognizant Technology Solutions ($CTSH) and DirecTV ($DTV). CTSH not only beat earnings: they raised guidance, and the shares broke out to a new all-time high on Thursday (see chart below). DirecTV smashed earnings by 26 cents per share. Through Thursday, our Buy List is up 29.25% for the year, which is 6.75% more than the S&P 500. That’s our largest lead of the year. If our lead holds up for eight more weeks, it will be the seventh year in a row that we’ve beaten the market.

In this week’s CWS Market Review, I’ll cover our recent earnings reports. I also want to highlight Ford Motor ($F), which is going for a very attractive price. Later on, I’ll focus on some earnings reports due later this month. But first, let’s look at the great earnings report from Cognizant Technology.

Cognizant Technology Beats and Guides Higher

In last week’s CWS Market Review, I said that I expected Cognizant Technology ($CTSH) to beat Wall Street’s earnings estimate—and that’s exactly what happened. On Tuesday, the IT consulting firm reported Q3 earnings of $1.13 per share, which was four cents higher than Wall Street’s consensus. Quarterly revenues rose 21.9% to $2.31 billion, $50 million more than consensus.

This was a very good quarter. Cognizant’s president said, “Our performance during the quarter was stronger than anticipated due to a faster ramp up in demand for outsourcing services and strong discretionary spending on consulting and technology services.” Interestingly, Cognizant benefited from the rollout of the Affordable Care Act, often known as Obamacare. What happened is that a lot of companies and state governments spent money to improve their networks, and that’s very good news for CTSH. Their healthcare business grew by 11% last quarter, which was more than double the rate of their financial-services segment.

But the best news for us is that Cognizant raised their full-year guidance from $4.32 to $4.37 per share. Oh, how I love a beat-and-raise announcement! Full-year revenue is expected to be at least $8.84 billion, which is an increase of 20.3% over last year.

In the CWS Market Review from June 28, I wrote, “One stock on our Buy List that looks particularly attractive at the moment is Cognizant Technology Solutions.” We got that one right. CTSH is up more than 41% since then, and it hit a new all-time high on Thursday. This is still a good buy, although not a super buy like it was in June. This week, I’m raising my Buy Below on Cognizant to $94 per share.

DirecTV Smashes Estimates

Our other big winner this week was DirecTV ($DTV). DTV reported Q3 earnings of $1.28 per share, which was 26 cents more than consensus. Now that’s an earnings beat! In the U.S., DirecTV added 139,000 subscribers, which doubled expectations. Bear in mind that this is happening at the same time that Time Warner and Comcast are hemorrhaging subscribers.

To use the business jargon, DTV is benefiting from a low “churn rate,” which is a fancy way of saying that they’re not giving folks a good reason to cancel. I think a lot of that is due to their NFL Sunday Ticket package. They’ve also benefited from the mini-war between CBS and Time Warner. DTV’s churn rate is especially impressive considering that they’ve been able to raise their prices.

DirecTV’s quarterly revenue rose 6.3% percent to $7.88 billion, which barely topped expectations. I should add that their bottom line included some special items and a fee settlement, but even taking those into consideration, DirecTV handily beat expectations.

Latin America continues to be a strong growth area for DirecTV. They added 260,000 subscribers in that region, which is less than I was expecting. After the earnings report, the stock jumped, then plunged, but soon stabilized. Don’t let the short-term volatility scare you. This is a good stock. I’m raising my Buy Below on DirecTV to $67 per share.

Ford Is an Exceptionally Good Buy Here

Every so often I like to highlight stocks that are exceptionally good buys, as I did with Cognizant this summer. Right now, Ford Motor ($F) is one of the best bargains on our Buy List.

The stock has pulled back recently, and on Thursday Ford closed at $16.55 per share. That’s less than 10 times this year’s earnings estimate. I usually recommend a dose of skepticism when dealing with Wall Street estimates, but in this case, that estimate includes three quarters of results, so it’s not exactly a wild guess.

What’s interesting is that Ford has fallen back at the same time Microsoft ($MSFT) has rallied. In fact, Microsoft just touched a 12-year high. The two events are connected. For several weeks there’s been speculation that Ford’s CEO Alan Mulally would leave Ford to become the new CEO at Microsoft. A lot of traders have been riding the Mulally play (long MSFT, short F). I’ve downplayed these rumors, and I’m still a doubter, but an influential analyst said this week that it’s very likely. Nomura’s Rick Sherlund said that Mulally will be named MSFT’s CEO by December.

While losing Mulally would be a setback for Ford, I think it’s a mistake to think Ford would be cast adrift. Ford’s turnaround is already well established, and they’re spreading that strategy to Europe. Just two weeks ago, the automaker announced another strong earnings report, and they raised guidance. Also, Ford’s losses in Europe were much better than expected.

Ford has now delivered 17 straight profitable quarters in a row. I also expect the company will raise their quarterly dividend in January. The current dividend is 10 cents per share, and I think it can rise to 12 or 13 cents per share. At 13 cents, or 52 for the year, that gives Ford a yield of 3.1% based on Thursday’s close. My take: Ford is worth $22 per share. I currently rate Ford a buy up to $18 per share, but if you can get it below $16.60, that’s a very good deal.

Earnings Preview for Medtronic and Ross Stores

We’ve had all of our Buy List earnings reports for stocks that end their quarter in September. Now we have two coming soon for stocks with October quarters. Medtronic is scheduled to report earnings on Tuesday, November 19. Then on Thursday, November 21, Ross Stores is due to report.

Medtronic ($MDT) has quietly turned into one of our biggest winners this year. The shares are up nearly 40% for the year. The consensus on Wall Street is for earnings of 90 cents per share, which is very doable. The company has said it expects full-year earnings (ending in April) between $3.80 and $3.85 per share. In June, Medtronic raised its dividend for the 36th year in a row. Business is still going well here, and I think they can easily hit their full-year guidance. The CEO said Medtronic is looking to generate $25 billion in free cash flow over the next five years. Medtronic continues to be a good buy up to $57 per share. Be careful not to chase this one.

In August, Ross Stores ($ROST) said that it expects earnings to range between 75 and 78 cents per share, which I think is a conservative forecast. The Street expects 80 cents per share. Ross has been a very strong performer for us. Last week, I raised the Buy Below to $81 per share. Ross Stores remains a solid buy.

That’s all for now. Next week should be a fairly quiet week on Wall Street. Earnings season is just about over, and there are only a few economic reports scheduled. On Thursday, the Census Bureau will release the trade report. Then on Friday, the Fed will report on Industrial Production. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Morning News: November 8, 2013

Posted by Eddy Elfenbein on November 8th, 2013 at 6:16 amEuro Bulls Crack as Odds of Return to 2013 Lows Jump

Draghi Shows Pledges Backed by Rate Surprise

Standard & Poor’s Cuts France’s Credit Rating to AA

China Exports Rise More Than Estimated After September Drop

U.S. Jobs Market Seen Taking a Hit From Government Shutdown

IRS Refunded $4 Billion to Identity Thieves

Twitter Resists Investor Frenzy to Avert Facebook Flop

UBS Pays $3.76 Billion to Swiss Central Bank In Buy-back of Toxic Assets

Disney 4Q Profit Rises but Pay TV Unit Underwhelms

Nvidia’s Quarterly Forecast Raises Competition Concerns

Penney Monthly Same-store Sales Rise For First Time Since 2011

Richemont Says Luxury-Goods Maker Rules Out Selling Brands

Economist Tyler Cowen Explains Why The Future Will Be Awesome — For About 15% Of Us

Joshua Brown: Twitter IPO Post-Mortem

Jeff Miller: Same Story, Two Headlines

Be sure to follow me on Twitter.

How Much Would You Pay? (UPDATE)

Posted by Eddy Elfenbein on November 7th, 2013 at 6:02 pmWhat if I told you I had a company that last year generated $4 in sales? The problem is that I had $5 in expenses so we actually lost $1.

The good news is that things got better this year. For the first nine months, we generated sales of $5.30. But again, we spent heavily. We had expenses of $7 so we lost $1.70. We have $5 in debt.

How much would you pay for this company?

If you said $179, congratulations. That’s Twitter.

Update: Going by Twitter’s first-day close, make that $305 per share.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His