-

The Great Salad Oil Swindle

Posted by Eddy Elfenbein on November 7th, 2013 at 3:02 pmFifty years ago this month, one of the most ingenious Wall Street frauds unraveled. It was the Great Salad Oil Swindle.

Before Bre-X, there was Allied Crude Vegetable Oil Refining Corporation. In 1962, Anthony “Tino” De Angelis set about to corner the soybean oil market through a combination of futures and fraud. De Angelis’s company was heavily involved in the shipping of foodstuffs between the U.S. and Europe following WWII. During the following decades, Allied focused on the soybean oil used to make salad dressings. Along with a checkered past in the meat business, De Angelis gained notoriety for shipping substandard or uninspected vegetable oil to government contractors and then overcharging them.

As a result of his shipping operations, De Angelis learned that consumer credit giant American Express was entering the field warehousing business. This appealed to De Angelis because American Express, following inspections, would vouch for the goods of clients that stored inventory shipments in its warehouses. Clients then could use American Express’s warehouse receipts to take out loans, putting up the authenticated value of their inventories as collateral. De Angelis became one of American Express’s first big clients.

Moving from dubious business practices to outright product fraud, De Angelis began filling his oil tanks with water and then adding thin layers of oil to the tops of each tank in an attempt to deceive inspectors. Liter upon liter of watered down inventory piled up in warehouses while De Angelis took out millions in loans from banks. He used much of the money to buy up soybean oil futures so that he could completely corner the market. Problems started to crop up, however, when the soybean oil being stored at American Express warehouses vastly exceeded soybean producers’ output. Somebody blew the whistle and American Express inspectors swooped in to discover the tanks of oil-sprinkled water that De Angelis had been storing. In total, the tanks in De Angelis’s inventory represented more than $175 million worth of faked soybean oil.

On November 19, 1963, Allied Crude Vegetable Oil Refining Corporation filed for bankruptcy. De Angelis filed for personal bankruptcy as well, leaving American Express to foot the bill on the bad loans. In addition to American Express, the scandal weakened other Wall Street firms, which contributed to the financial chaos that followed the Kennedy assassination a few days later. With massive losses, American Express shares dropped sharply and Warren Buffett, value investor extraordinaire, scooped up a 5% interest in the ensuing fire sale. De Angelis was sentenced to seven years in prison. However, the ultimate losses from the salad oil scandal were difficult to separate from the general bloodletting on Wall Street in 1963.

Norman Miller won a Pulitzer Prize for his reporting on the scandal and later wrote the book, The Great Salad Oil Swindle.

-

The Fiscal Year Numbers Are In

Posted by Eddy Elfenbein on November 7th, 2013 at 12:49 pmToday’s third-quarter GDP report also gave us our first look at the GDP for the entire 2013 fiscal year. Nominal GDP totaled $16.62 trillion for the FY 2013 which was an increase of 3.26% over FY 2012. (This is, of course, our first look; there numbers will be updated many more times.)

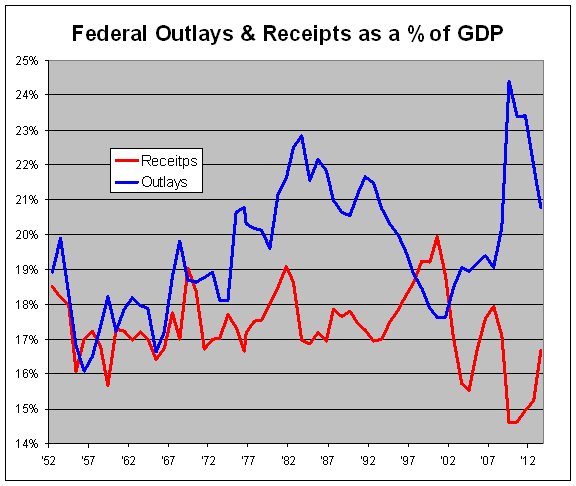

With the recent budget data, we now have the latest data point on the government’s taxing and spending as a percent of GDP. You often see this chart in policy debates so you may be familiar with it, but I have to explain that three months ago, the BEA updated the entire GDP data series. As a result, many of the versions of this chart you see on the web are incorrect.

Below is the updated version. This may be the only place you’ll find it:

Also, I’m a big fan of the St. Louis Fed’s FRED database, so it pains me to say that their numbers are out-of-date as well. Their Fiscal Year GDP (FYGDP) series is based off the old GDP data. Also, their Receipts, Outlays and Deficit as a percent of GDP series (FYFRGDA188S, FYONGDA188S, FYFSDFYGDP) are based on calendar year GDP, not fiscal year. I’ve also included the 1976 “transitional quarter.”

Now let’s look at the numbers:

Uncle Sam spent $3.45 trillion last year which works out to 20.79% of the economy. That’s the second year in a row that spending as a percent of GDP has fallen and it’s well below the recent peak of 24.41% set in 2009.

The Feds took in $2.77 trillion in revenue which works out to 16.69% of GDP. That’s the fourth increase in a row, though it’s working off a very low bottom. The oft-heard talking point about “the lowest taxes in 60 years” is no longer operative.

The deficit came out to $680 billion which is 4.09% of GDP. I thought we had a shot of dropping below 4% but we couldn’t do it. Still, it’s an enormous decrease from the prior four years.

-

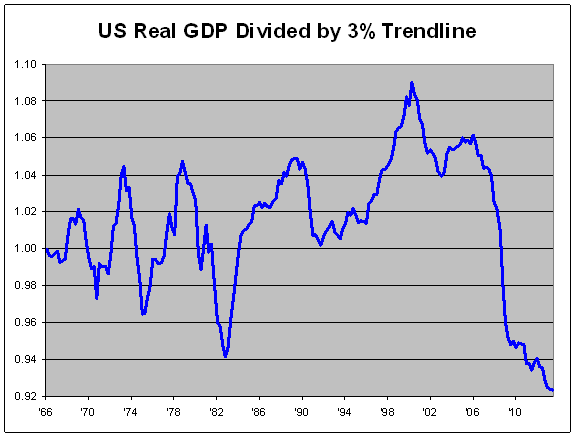

Q3 GDP Growth = 2.8%

Posted by Eddy Elfenbein on November 7th, 2013 at 10:42 amThe government reported that the economy grew by 2.8% in the third quarter. That was better than expectations of 2%. Unfortunately, much of the increase was driven by inventory restocking.

While this was the third quarter in a row of rising growth, it was also the 20th time in the last 25 quarters that GDP growth failed to crack 3%. What makes this interesting is that 3% growth was about the average growth rate for 40 years for the U.S. economy.

Below is a chart I made and I think it shows you just how poorly the economy has performed. I took real GDP and divided it by a 3% trendline. I used $4.2 trillion in Q1 of 1966 as my base.

Whenever the blue line rises, that means the economy is growing faster than 3%. A falling line indicates slower than 3%. We tracked 3% pretty well for a long time. But lately, the economy has nose-dived. We’re currently at 92.3% of the trend.

I don’t see us reverting to the mean. This may be the new normal.

-

Morning News: November 7, 2013

Posted by Eddy Elfenbein on November 7th, 2013 at 6:07 amDraghi Weighs Whether Rate Cuts Too Valuable as ECB Meets

S&P Affirms India’s Rating at BBB-/A-3; Outlook Remains Negative

Société Générale and Crédit Agricole Aim for Swap on Derivatives Venture

Cautious Consumers Seen Curbing U.S. Economic Growth

Revenue Growth Hopes Feather Twitter’s Nest

Twitter IPO Price Indicates Asian Players Are Undervalued

Square Exploring 2014 IPO With Banks

ArcelorMittal Core Profit Better Than Expected at $1.71 Billion

Lenovo Profit Up 36% As Smartphone Sales Grow

Investors Slam The Brakes On Tesla, Time To Stay On The Shoulder?

Tesla’s Valuation Drives Me Crazy

Deutsche Telekom Sales Exceed Estimates on T-Mobile US

Nestle Sheds Bulk of Jenny Craig in Effort to Slim Down

An Offer From Amazon to Its Most Bitter Rivals

Cullen Roche: Shiller: Is Economics a Science?

Be sure to follow me on Twitter.

-

Twitter Priced at $26 per Share

Posted by Eddy Elfenbein on November 6th, 2013 at 9:56 pmTwitter ($TWTR) will start trading tomorrow. The company will debut on the NYSE under the symbol TWTR. The underwriters have announced a price of $26 per share. That values the company at $14.2 billion.

Everyone on Wall Street has their fingers crossed on this one since the Facebook ($FB) IPO was a bit of a flop. Trading was delayed and the stock didn’t do well for several weeks. I suspect that FB wasn’t well advised by their bankers. Also, I think they got greedy. Twitter seems to be avoiding these mistakes.

Twitter is selling 70 million shares to the public so it will raise $1.82 billion for the company. I strongly suspect that the price will pop once the shares hit the market.

So is Twitter a good buy? The heck if I know.

With investing, I rely on the fundamentals of a business. One of the limits of fundamental analysis is that it assumes the general stability of the business environment. With a company like Twitter, that environment is far from stable. I can make a pretty good guess as to what Harris will look like in three years. But with Twitter, I have no earthly idea.

Twitter is currently losing money, and it will continue to do so. If things go well, they may turn a profit by 2015. Again, that’s if things go well. At $26 per share, twitter is being valued at 12.4 times next year’s estimated sales. Facebook currently trades at 11.6 times 2014 sales, and LinkedIn is at 12.2 times. That’s a rich valuation.

Until I can see a consistent positive cash flow stream from Twitter, I’m staying far away from this stock. That’s not a moral judgement against the stock. I wish them well. But for my kind of investing, I never take risks I don’t have to.

-

Maybe Mulally Is Going to Microsoft

Posted by Eddy Elfenbein on November 6th, 2013 at 3:29 pmMicrosoft ($MSFT) has been doing well lately and Ford ($F) hasn’t. Apparently, there’s an obvious connection: speculation that Ford CEO Alan Mulally will depart the automaker for the top spot at MSFT.

I’ve been a doubter on that story, but it got a major boost today when Rick Sherlund, an influential analyst at Nomura, said it’s likely.

From Jay Yarow at Business Insider (h/t @soonerstocks):

Inside Microsoft, Sherlund is well-respected as one of the few analysts that really understands the company.

In his report today, he says it’s likely that Alan Mulally, the CEO of Ford, will be named as Microsoft’s CEO by December.

While internal candidates like Stephen Elop and Tony Bates are being kicked around, Sherlund says he does not believe they are seriously in the running.

He says other top candidates likely include Boeing CEO James McNerney, Jr. and ex-Motorola COO Edward Breen. Those are two names we’ve never heard before.

Additionally, he reports Microsoft has been trying to woo Paul Martiz, a former Microsoft employee who was running VMWare.

Sherlund says Mulally/Maritz would be a dream team. Maritz would be Microsoft’s head of software/products and Mulally as CEO/operator. If it helps, think of Tim Cook and Jony Ive. A similar division between operator and visionary.

Furthermore, Sherlund thinks MSFT should sell off Bing and Xbox, buy out Ballmer’s stock for $12 billion, and finally:

Build out Azure, the cloud platform that rivals Amazon.

Make sure its enterprise software works across platforms. Office needs to work on Android and iOS to compete with Google’s apps which are growing.

Skype and Yammer are not being taking advantage of. Microsoft should do more with both.

-

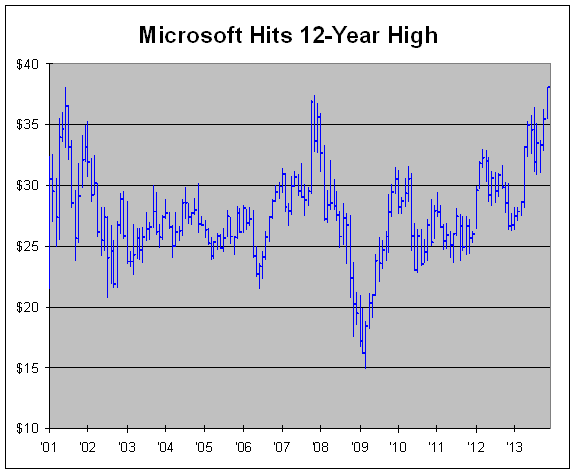

Microsoft Breaks $38

Posted by Eddy Elfenbein on November 6th, 2013 at 12:11 pmFor the first time in 12 years, Microsoft ($MSFT) is trading north of $38 per share. (I should mention their gigantic $3.08 per share dividend in 2004.)

The latest word is that MSFT had narrowed down its list of candidates to be new CEO to five names. Alan Mulally is on the list but I don’t think he’s a serious contender.

-

Cognizant’s CEO on CNBC

Posted by Eddy Elfenbein on November 6th, 2013 at 10:05 am -

Morning News: November 6, 2013

Posted by Eddy Elfenbein on November 6th, 2013 at 6:15 amChina’s Leaders Confront Economic Fissures

Euro Zone Money Markets Returned to Growth in Second Quarter

U.K. Production Rises More Than Forecast on Factory Rebound

24-Hour General Strike Shuts Down Services Across Greece

Brent Crude Traders Claim Proof BFOE Boys Rigged Market

The House GOP Dials a Wrong Number on the Chained CPI

Toyota Raises Profit Forecast After Abe Helps Weaken Yen

Twitter Raises Price Range for Its I.P.O.

Samsung Elec Vows More Aggressive Investment, Targets Tablets

ING to Complete Restructuring in 2016 Ahead of Schedule

Office Depot Announces Third Quarter 2013 Results

Bitcoin Is Going On An Astronomical Tear

Here’s How Companies Are Using Their Massive Piles of Cash

Roger Nusbaum: Helaine Olen (Kind Of) Takes Down Dave Ramsey

Credit Writedowns: Financial Obligations Rising for Renters, Falling for Homeowners

Be sure to follow me on Twitter.

-

DirecTV Earns $1.28 Per Share

Posted by Eddy Elfenbein on November 5th, 2013 at 8:00 amDirecTV ($DTV) just reported Q3 earnings of $1.28 per share, which was 26 cents more than consensus. In the U.S., DirecTV added 139,00 subscribers which doubled expectations. This is happening at the same time that Time Warner and Comcast are hemorrhaging subs.

“DirecTV didn’t give customers any reason to cancel in terms of blackouts or anything like that,” said Brean Capital analyst Todd Mitchell. “DirecTV has been good at picking up customers after blackouts.”

Shares of DirecTV rose 2.5 percent to $66 in trading before the market opened.

ISI analyst Vijay Jayant said the low churn could be because of the company’s exclusive National Football League Sunday Ticket package, which lets DirecTV customers watch out-of-market games every Sunday. Promotion for that product ramped up in the third quarter.

Net income attributable to DirecTV was $699 million, or $1.28 per share, compared with $565 million, or 90 cents share, a year earlier.

Excluding a fee settlement and other special items, earnings came to $1.13 per share, which beat the analysts’ average estimate by 12 cents, according to Thomson Reuters I/B/E/S.

Revenue rose 6 percent to $7.88 billion, narrowly exceeding analysts’ estimates of $7.84 billion.

In Latin America, DirecTV added 260,000 subscribers, while StreetAccount was looking for 371,900.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His