-

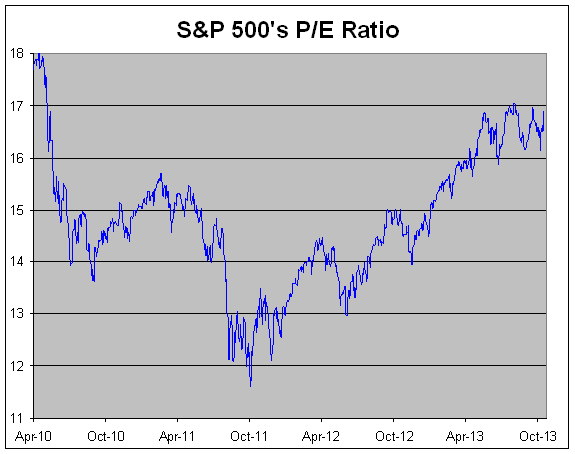

S&P 500’s P/E Ratio Close to 3.5-Year High

Posted by Eddy Elfenbein on October 21st, 2013 at 1:04 pmThe Price/Earnings Ratio for the S&P 500, based on trailing earnings, recently topped 17. It’s very close to reaching its highest point since May 2010.

Just over two years ago, on October 3, 2011, the S&P 500’s P/E Ratio bottomed out at 11.61. That was the lowest ratio in 22 years. Going by Friday’s close, the S&P 500 has advanced 58.7%. But 45.6% of that is solely down to multiple expansion. Earnings are up only 9.4%.

This is a bit misleading because we’re working off a very low P/E Ratio. I think it’s more accurate to say that the P/E Ratio went from being very low back to a more normal range.

-

Harris Breaks $60

Posted by Eddy Elfenbein on October 21st, 2013 at 12:31 pmShares of Harris have been dancing near $60 per share for the last few weeks, but the stock hasn’t been able to break through. That is, until today. HRS is finally trading in the 60s.

We first added the stock on our 2012 Buy List at $36.04. We have a nice 66% gain in less than two years. The next earnings report is due one week from tomorrow. Wall Street currently expects earnings of $1.13 per share.

-

JPMorgan $13 Billion Settlement

Posted by Eddy Elfenbein on October 21st, 2013 at 9:53 amIt looks as if JPMorgan Chase ($JPM) has reached a $13 billion deal with the Federals to settle all of the investigations into their mortgage loan business before the financial crisis. The deal doesn’t release them from any criminal liability.

The record settlement could help resolve many of the legal troubles the New York bank is facing. Earlier this month JPMorgan disclosed it had stockpiled $23 billion in reserves for settlements and other legal expenses to help cover the myriad investigations into its conduct before and after the financial crisis.

The deal is being hammered out by some of the most senior officials at the Department of Justice and the largest U.S. bank. Attorney General Eric Holder and JPMorgan Chief Executive Jamie Dimon spoke on the phone on Friday night to finalize the broad outlines of the broad deal, the first source said.

The bank’s general counsel Stephen Cutler and Associate Attorney General Tony West are negotiating a statement of facts that will be part of a final agreement, the source said.

Long considered one of the best-managed banks, JPMorgan has stumbled in recent years, with run-ins with multiple federal regulators as well as authorities in several states and foreign countries over issues ranging from multibillion-dollar trading losses and poor risk controls to probes into whether it manipulated a power market.

In September, as the Justice Department prepared to sue the bank over mortgage securities that the bank sold in the run-up to the financial crisis, JPMorgan tried to reach a broader settlement with DOJ and other federal and state agencies to resolve claims over its mortgage-related liabilities stemming from the bust in house prices.

Dimon went to Washington to meet with Holder on September 25, and discussed an $11 billion settlement at that point.

Some of the problems relate to mortgage bank Washington Mutual and investment bank Bear Stearns, two failing firms that JPMorgan took over in 2008.

The bank and the Justice Department have been discussing a broad deal that would resolve not only the inquiry into mortgage bonds it sold to investors between 2005 to 2007 that were backed by subprime and other risky residential mortgages, but also similar lawsuits from the Federal Housing Finance Agency, the National Credit Union Administration, the state of New York and others.

The broader settlement is a product of a government working group created nearly two years ago to investigate misconduct in the residential mortgage-backed securities market that contributed to the financial crisis. Officials from the Justice Department, the New York Attorney General and others helped to lead the group.

Reuters reported late Friday that JPMorgan and FHFA had reached a tentative $4 billion deal. That agreement is expected to be part of the larger $13 billion settlement.

Shares of JMP are up 24 cents this morning.

-

Morning News: October 21, 2013

Posted by Eddy Elfenbein on October 21st, 2013 at 6:11 amBIITS Replacing BRICs as Emerging Markets No Longer Blanket Buy

The Man Who’ll Do Triage on Europe’s Banks

New Data Underscore Challenges for Japan

There Will Be No $24 Billion Economic Loss From the Government Shutdown

Bitcoin Has Gone on an Insane Surge

U.S. Deal With JPMorgan Followed a Crucial Call

U.K.’s Hinkley Nuclear Power Station Gets Go-Ahead As Coalition Signs Off EDF Deal

SAP Reducing ByDesign Investment – A Cautionary Tale

Starbucks Under Media Fire In China For High Prices

Philips’ Profits Improve Across the Group

Sharp Japan Export Slowdown Dents ‘Abenomics’, Flags Asia Weakness

Nokia Record Cash Targets Alcatel Wireless Unit

Changing Philips Top to Bottom: CEO Van Houten

Joshua Brown: The Infographic That Ate Wall Street

Jeff Miller: Weighing the Week Ahead: Will Disappointing Earnings End the Stock Market Rally?

Be sure to follow me on Twitter.

-

Game 7, 1965 World Series

Posted by Eddy Elfenbein on October 18th, 2013 at 4:04 pmOn YouTube, I recently stumbled across the complete Game 7 of the 1965 World Series.

What I found fascinating was the restrained celebration after the final out. Perhaps it shows how much American culture has changed over the past 48 years.

If you skip ahead to 2:20:16, you can see the final out. SPOILER ALERT – Sandy Koufax strikes him out. But notice how subdued the celebration is. Of course, the game is in Minnesota and not Los Angeles, so that certainly is a factor. Everyone is happy but it’s far from the over-the-top New Year’s-like manic celebrations we see nowadays. No man-pile. No confetti. Just hearty handshakes.

This was also a remarkable performance for Koufax. He pitched a three-hit shutout just three days after pitching a four-hit shutout. Koufax didn’t pitch in game #1 as it coincided with the Jewish holiday of Yom Kippur.

I guess people acted with a little more dignity back then. But as much as things change, there’s one constant — Vin Scully.

-

Earnings Season So Far

Posted by Eddy Elfenbein on October 18th, 2013 at 1:24 pmEarnings season is still young but Bloomberg has some numbers so far:

While the rate of profit growth is slowing in the S&P 500, companies in the index have reported record annual earnings for more than two years, holding valuations close to the historical average even as the gauge’s price reached an all-time high in March and kept climbing.

Profits for companies in the S&P 500 probably increased 1.4 percent during the third quarter as sales rose 2 percent, according to analysts’ estimates compiled by Bloomberg. Among the 87 companies in the index that have reported so far, 72 percent exceeded analysts’ estimates, about the same proportion as the previous quarter.

S&P 500 companies are projected to earn a record $107.90 a share this year, up from $45.82 a share in 2009, according to data compiled by Bloomberg. Among the 20 biggest companies that released results, the median one-day stock move afterward has been a gain of 1.2 percent.

Weakening profit growth will limit stock gains, according to Donald Selkin, who helps manage about $3 billion as the New York-based chief market strategist at National Securities Corp. The shutdown has shaved at least 0.6 percent off of fourth-quarter 2013 gross domestic product growth, taking $24 billion out of the economy, S&P Ratings Services said this week.

They also note that over the last 10 years, the S&P 500 has gained 1.1% during the first four weeks of earnings season, which is about double the growth rate of the index over that time.

-

Stryker CEO Kevin Lobo on CNBC

Posted by Eddy Elfenbein on October 18th, 2013 at 12:32 pm -

10^100 = 10^3

Posted by Eddy Elfenbein on October 18th, 2013 at 10:21 amGoogle ($GOOG) hit $1,000 per share this morning. The company went public on August 19, 2004 and the underwriting price was $85 per share. The company is expected to earn $51 per share next year.

-

CWS Market Review – October 18, 2013

Posted by Eddy Elfenbein on October 18th, 2013 at 7:07 am“Democracy is the art and science of running the

circus from the monkey cage.” – H. L. MenckenYou know it, H.L. On Wednesday evening, the absurd 16-day government shutdown finally came to an end. Unfortunately, the deal doesn’t resolve the issue in question; it merely kicks the can down the road for a few more months.

Previously, I had said that some deal would be reached because there was simply too much to lose if the politicos had let this silliness carry on much further. One of the ratings agencies put the U.S. on notice, not due to our finances but due to our politics. How sad is that?

Fortunately, Wall Street remained calm and anticipated that a deal was near, as stocks rallied impressively over the past week. As it turned out, the S&P 500 rallied 2.4% over the course of the 16-day shutdown. On Thursday, the S&P 500 closed at 1,733.15, its highest level ever. Our Buy List is also at a new all-time high. We’re now up 27.7% for the year, which is more than 6% ahead of the S&P 500.

In this week’s CWS Market Review, we’ll take a look at our recent Buy List earnings reports. Last Friday, JPMorgan Chase ($JPM) beat expectations by a mile. That is, when you discount their gigantic legal bills. I’ll also preview the three Buy List earnings reports we have coming next week. Later on, I’ll list several updated Buy Below prices for our stocks. But first, let’s look at the strong earnings reports coming from our big banks.

Strong Earnings from JPMorgan and Wells Fargo

Shortly after I sent out last week’s newsletter, Wells Fargo ($WFC) reported third-quarter earnings of 99 cents per share. That was two cents more than analysts had been expecting, and it was a nice increase from the 88 cents per share they earned last year.

As I expected, there was a big slowdown in home refinancings. Wells had been riding that gravy train very well for the last few quarters, so the easy money had been made. Rising mortgage rates have altered the economics of that business. The important point for Wells is that the economy continues to improve, albeit slowly. This means that fewer people are late with their debt payments. Last quarter, Wells was able to release $900 million worth of reserves for credit losses.

I was troubled to hear that Wells announced layoffs in its mortgage division, which I can’t say was unexpected. That move clearly helped Wells’s bottom line last quarter. The bank’s total revenue fell from $21.1 billion last year to $20.5 billion this year. The reserve releases and cost-cutting drove the higher profits.

This is one of the advantages of investing in well-run companies: they’re able to change when the environment changes. The stock initially dropped in early trading last Friday, but traders soon came to their senses. By the end of the day on Thursday, WFC was at a four-week high. Wells Fargo continues to be a good buy up to $45 per share.

Also on Friday, JPMorgan Chase ($JPM) reported a loss of $380 million, or 17 cents per share. But I have to note that that includes a massive $7.2 billion charge for the bank’s legal bills. Excluding that, the bank earned a profit of $1.42 per share, which easily topped Wall Street’s forecast of $1.30 per share. I said JPM could earn as much as $1.50 per share, which seemed very optimistic at the time, but I wasn’t that far off.

If we dig into the numbers at JPM, we see that the business’s outlook is very similar to Wells’s. I honestly don’t see how Jamie Dimon can stay at the helm considering the massive legal bills they have. Still, the core businesses are running well. JPMorgan Chase remains a good buy up to $56 per share.

Stryker Is a Buy up to $75 per Share

After the bell on Thursday, Stryker ($SYK) reported earnings of 98 cents per share which missed expectations by two cents per share. Revenues for the orthopedics company rose 4.8% to $2.15 billion, which hit consensus on the nose.

This earnings miss isn’t such a big deal. The important thing is that they reiterated their full-year guidance range of $4.20 to $4.26 per share. Stryker has unfortunately been getting nicked by currency exchange. The company estimates that the impact on the top line this year from forex will be between 1.5% and 2.0%. When looking at a company, I try to look past these issues. Sometimes foreign exchange helps you, sometimes it hurts. What I want to see is a strong, healthy business.

I think Stryker looks very good here. Many investors felt that it was going to get hammered by the implementation of President Obama’s healthcare reform. Stryker started the year very strongly, and it has gradually drifted higher since then. It’s now a 32% winner on the year for us, and I’m expecting another dividend increase in a few weeks. This is a good company. I’m raising our Buy Below on Stryker to $75 per share.

Earnings Next Week from Bard, Microsoft and CA Technologies

We have three more earnings reports due next week: Microsoft, CR Bard and CA Technologies. Let me add that I track the releases as best as I can, but some companies aren’t very forthcoming with their earnings dates, so there might be some errors.

Microsoft ($MSFT) finds itself in the unusual position of being widely criticized, yet the financial results are still pretty decent. Everyone likes to predict the end of MSFT, but the folks in Redmond still churn out a healthy profit. The software giant is due to report earnings on Wednesday, October 23.

Three months ago, Microsoft missed big and the stock got slammed. MSFT has since recovered, thanks in part to the news that Steve Ballmer will be leaving. For Q3, Wall Street has set the bar quite low. The consensus is for earnings of 54 cents per share, which is only one penny higher than last year. They should be able to top that. I also like that Microsoft recently raised their dividend to 28 cents per share. That was a bold move. The shares now yield 3.2% which is very good for this market. I’m raising our Buy Below on Microsoft to $37 per share.

CA Technologies ($CA) has been a surprisingly strong performer for us this year. This is one of the more conservative stocks on our Buy List, and it’s ideal for folks who get antsy from a lot of volatility. CA’s earnings report is due next Thursday, October 24, and it will be for their fiscal second quarter. The company has already said they see full-year earnings (ending next April) coming in between $2.90 and $3.00 per share. Wall Street’s consensus for the quarterly report is for 73 cents per share. The last few earnings have beaten estimates by a good margin. Look for another strong number. For now, I’m keeping our Buy Below at $31 per share but I may raise it soon.

CR Bard ($BCR) has been a remarkably good stock lately. It’s risen for six of the last seven trading sessions and is at a new 52-week high. I know many investors don’t like high-priced stocks, but it really is an irrational fear. Bard will report its earnings on Tuesday, October 22. The company has told us to expect earnings to range between $1.37 and $1.41 per share. I think they’ll hit that with little difficulty. I’m raising our Buy Below on BCR to $126 per share.

Several Higher Buy Below Prices

My plan was to hold off raising our Buy Below prices until earnings came out, but the market’s dip and recovery during the shutdown altered those plans. The market’s recent surge has pushed several of our stocks out of range, and I don’t want investors left behind. In addition to the higher Buy Below prices I’ve already mentioned for Stryker, Bard and Microsoft, I have a five more this week.

AFLAC ($AFL) has been particularly strong lately (see chart below). The shares broke $66 on Thursday and look as strong as ever. Expect another good earnings report at the end of the month. I’m raising my Buy Below on AFLAC to $70 per share.

Fiserv ($FISV) continues to be a rock star for us. The stock reached a new 52-week high on Thursday. What I love about Fiserv is the steadiness of their earnings growth. The next earnings report comes out on October 29. This week, I’m raising the Buy Below on Fiserv to $108 per share. This is another solid stock.

Nicholas Financial ($NICK) has been very strong lately. Some of these smaller stocks can sit and do nothing for weeks and then suddenly spring to life. We still haven’t heard anything about the buyout offer, but given the stock’s performance, I’m not sorry if the board shot down an inadequate offer. I think we’ll see a nice dividend increase before the end of the year. I’m raising our Buy Below on NICK to $18 per share. Go NICK!

Moog ($MOG-A) is still our #1 performer this year, with a stunning 44% gain. It’s hard to believe that almost a year ago Moog was going for $34 per share, and now it’s closing in on $60. The company hasn’t announced when it will release earnings for Q3, but it should be within the next two weeks. I’m raising our Buy Below on Moog to $61 per share. I still want to keep a tight range on this one.

Cognizant Technology Solutions ($CTSH) continues its upward climb. This stock has been a phenomenal performer over the last four months. Last Friday, CTSH nearly cracked $89 per share. It was close to $60 this summer. Earnings are due out in early November. I’m raising our Buy Below on Cognizant to $90 per share.

That’s all for now. Stay tuned for more earnings next week. Now that the government has reopened, we’re also going to get economic reports again. Plus, we’ll get the backlog of reports. On Tuesday, the Labor Department will finally give us the September jobs report. A tepid report may cause the Fed to hold off on any tapering plans until next year. Plus, we don’t know the full impact of the government shutdown, but it wasn’t good. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: October 18, 2013

Posted by Eddy Elfenbein on October 18th, 2013 at 6:22 amEU Races for Bank-Failure Deal Deadline to Avert Quagmire

China’s Third-quarter GDP Grows 7.8%

Chinese to Invest in British Nuclear Power

India Gears Up To Launch Interest Rate Futures

S&P 500 Sets Record High On Relief Over U.S. Fiscal Deal

Dollar Set for Weekly Drop on Fed QE Extension Bets; Won Climbs

After Pause, Resupplying Economic Data

Google Boosts Ad Volumes to Counter Mobile-Driven Price Drop

Fall in Revenue at Goldman Sachs Raises Concerns

IBM Shares Tumble After Sixth Quarterly Sales Decline

Verizon Profit Beats Estimates as Wireless Revenue Grows

Controlling Chaos: Twitter’s Wild Ride From Doodle to IPO

Plea Agreement Could End SAC’s Advisory Business

Jeff Miller: How to Profit from the Shutdown Aftermath

Epicurean Dealmaker: Our Glassy Essence

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His