-

FactSet Research Systems Earns $1.20 per Share

Posted by Eddy Elfenbein on September 17th, 2013 at 10:49 amThis morning, FactSet Research Systems ($FDS) reported fiscal fourth-quarter earnings of $1.20 per share. The stock is down today because technically, that counts as an “earnings miss.” The Street was at $1.21 per share but that’s just traders being traders. Three months ago, FactSet gave us a range of $1.18 to $1.21 per share so the company is hitting its own targets. FactSet’s revenues rose 6% to $219.3 million, and net income was $51 million.

The big metric for FactSet is ASV or annual subscription value. For the quarter, ASV rose by 6% to $888 million. That’s a good number and it points towards strong revenue over the next year.

For fiscal Q1, which ends in November, FactSet expects revenues between $222 and $225 million. They also see earnings coming in between $1.21 and $1.24 per share. Wall Street had been expecting $1.23 per share. The bottom line is that business continues to go well for FactSet. The company earned $1.11 per share in last year’s Q1.

From the earnings report, here are some financial highlights from Q4:

ASV from U.S. operations was $606 million and $282 million was related to international operations.

U.S. revenues were $149.9 million, up 6% from the year ago quarter.

Non-U.S. revenues rose 5% to $69.4 million as compared to the same period in fiscal 2012. Excluding the impact from foreign currency, the international growth rate was 6%.

GAAP operating margin was 32.2%. Adjusted operating margin was 33.4%, compared to 34.0% a year ago.

The effective tax rate for the fourth quarter was 28.1%, down from 31.7% a year ago. Excluding income tax benefits recorded during the second quarter of fiscal 2013 primarily from the reenactment of the U.S. Federal R&D credit, the annual effective tax rate was 28.9%.

Quarterly free cash flow was $71 million, up 38% over the year ago quarter. For the full fiscal 2013 year, FactSet generated $251 million in free cash flow which is 20% higher than a year ago.

Here are their expectations for Q1:

Revenues are expected to range between $222 million and $225 million.

Operating margin is expected to range between 33.0% and 34.0%, which includes a 30 basis point reduction from Revere.

The annual effective tax rate is expected to range between 28.5% and 29.5% and assumes the U.S. Federal R&D tax credit will be re-enacted by the end of the first quarter of fiscal 2014.

GAAP diluted EPS should range between $1.21 and $1.24, the midpoint of the range represents 10% growth over last year’s first quarter. GAAP diluted EPS assumes the U.S. Federal R&D tax credit will be re-enacted. If the U.S. Federal R&D tax credit is not re-enacted, first quarter’s GAAP diluted EPS will be reduced by $0.03.

Yesterday, the shares hit an all-time high of $113.05. Today they’re down to $108-$109.

-

Microsoft Ups Dividend by 22%

Posted by Eddy Elfenbein on September 17th, 2013 at 10:10 amThe stock market has rallied for nine of the ten days in September thus far, and we’re on track for another up day today. All eyes are on the Fed which begins its important two-day “tapering” meeting in Washington.

The best news this morning is that Microsoft ($MSFT) just announced a big dividend increase. I had projected that MSFT would raise their quarterly dividend by three cents — rising from 23 cents to 26 cents per share. I wasn’t optimistic enough. The software giant just raised their quarterly dividend by five cents per share to 28 cents. That’s a 22% increase. MSFT also announced a $40 billion buyback program.

The new repurchase program, which has no expiration date, replaces another $40 billion buyback plan that was due to lapse at the end of this month, Redmond, Washington-based Microsoft said today in a statement. The company’s quarterly dividend will rise 22 percent to 28 cents a share, payable to shareholders on Dec. 12.

“These actions reflect a continued commitment to returning cash to our shareholders,” Chief Financial Officer Amy Hood said in the statement.

For the year, the company will pay out $1.12 per share. Based on yesterday’s close, that translates to a yield of 3.41%.

-

Morning News: September 17, 2013

Posted by Eddy Elfenbein on September 17th, 2013 at 6:21 amThe Landesbanken: Inside Germany’s Trillion Euro banking Blind Spot

U.K. Inflation Slows to 2.7% on Transport, Clothing Prices

Europe August Car Sales Drop as Demand Lowest on Record

Poland Proves Best in Years Since Lehman: Riskless Return

A Bitter ‘Fertilzer War’ Gripping Belarus and Russia is Helping U.S. Farmers

Manufacturing Rebound Led by Autos Supports Growth

Two-Name Race Drops to One, but Guessing Continues

In Budget Faceoff, Obama Warns of ‘Economic Chaos’

Less Tapering Becomes Tightening Credit No Matter What Fed Says

Wall Street Exploits Ethanol Credits, and Prices Spike

Regulators to Charge JPMorgan Chase $750 Million in London Whale Cases

Anglo American Drops Alaska Investment

Packaging Corp. to Buy Boise for $1.28 Billion

Jeff Carter: Why Going Public Is Good For Twitter

Roger Nusbaum: A Doozy of Quote

Be sure to follow me on Twitter.

-

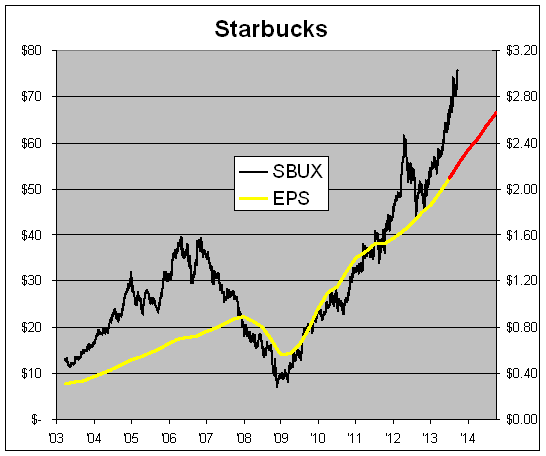

Looking at Starbucks

Posted by Eddy Elfenbein on September 16th, 2013 at 2:57 pmI don’t have much that is profound to say with this graph, but I spent some time making it and didn’t want it to go to waste. This is the share price of Starbucks ($SBUX) along with its earnings-per-share.

The share price is in black and it follows the left scale. The earnings are in yellow and follow the right scale. The red line is Wall Street’s consensus. The two lines are scaled at a ratio of 25 to 1 so whenever the lines cross, SBUX’s P/E Ratio is exactly 25.

The point I wanted to get across is how rapidly SBUX’s valuation has grown over the last year. It’s also interesting to see, despite some wild stock moves, how stable SBUX’s earnings growth appears to be.

I can’t say if 25 is the right P/E Ratio for Starbucks. I used 25 simply because I think it makes the chart look best. In 2006, SBUX traded at more than 56 times earnings.

I want to make it clear that looking at a stock’s P/E Ratio is just one way to analyze a stock. To get a full picture, there are many other metrics you must look at. I was struck by how dramatic the recent run-up is. The company is also benefiting from a steep drop in coffee prices. Personally, I don’t think Starbucks would be a bargain unless it dropped to $60 per share.

-

Traders Now See Later Rate Hike

Posted by Eddy Elfenbein on September 16th, 2013 at 12:12 pmThe reason for the Larry Rally is that traders see a rate hike coming later under Yellen:

Traders now give a 55 percent probability of the first rate hike in December 2014, and 68 percent chance in January 2015, according to CME Group’s Fed Watch, which generates probabilities based on the price of federal funds futures traded at the Chicago Board of Trade. On Friday, traders saw a better-than-even chance of the first increase in October 2014.

The Fed has said they don’t see raising rates until the middle of 2015 at the earliest.

-

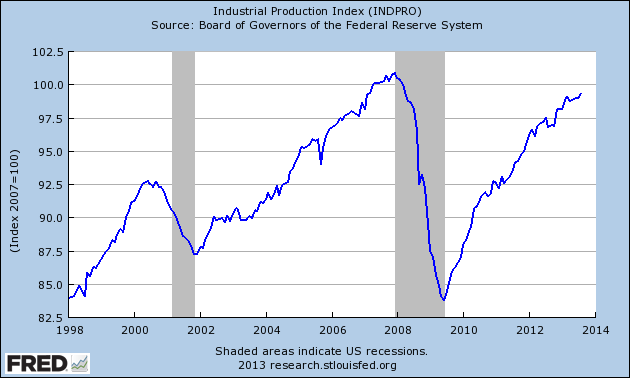

Industrial Production Rises 0.4% in August

Posted by Eddy Elfenbein on September 16th, 2013 at 11:27 amThe Federal Reserve reported that industrial production rose by 0.4% last month. That’s the biggest increase in six months. This data series has been quietly weak the last few months. Wall Street had been expecting a rise of 0.5%. Fortunately, this small miss isn’t enough to quell the Larry Rally.

Output at factories, mines and utilities climbed 0.4 percent after no change the prior month, a report from the Federal Reserve showed today in Washington. The median forecast in a Bloomberg survey of 85 economists called for a 0.5 percent advance in August. Manufacturing, which makes up 75 percent of total production, advanced by the most this year.

The strongest vehicle sales in almost six years are propelling factory activity, encouraging companies such as Ford Motor Co. (F) to boost plant capacity. A pickup in global markets and stronger consumer demand would help spark further progress in the sector that struggled earlier this year.

“Companies have to increase production in order to keep up with demand,” said Brett Ryan, a U.S. economist at Deutsche Bank Securities Inc. in New York, whose firm is the second-best forecaster of production for the past two years, according to data compiled by Bloomberg. “You have an elevated level of unfilled orders, so that bodes well for production.”

-

The Summers Rally

Posted by Eddy Elfenbein on September 16th, 2013 at 11:05 amToday is the start of Fed week, but the big Fed news today isn’t about this week’s meeting. Instead, it’s that Larry Summers has withdrawn his name from consideration for being the next Fed chair. This almost certainly means that President Obama will appoint Janet Yellen to succeed Ben Bernanke.

The market is rallying strongly on the news. The S&P 500 is back over 1,700 this morning and is currently up to 1,702. We’re not far from an all-time high for the index. The Russell 2000, in fact, is already at a new high.

I think Wall Street saw the Summers vs. Yellen battle as a proxy of easy money versus tighter money. I understand the feeling and I’m in support of continued stimulus but those characterizations are very much over-simplified. Anyone who has studied the Fed from the mid-1990s knows that Janet Yellen is far from an automatic vote for the doves. She was once described by a colleague as a “small lady with a large I.Q.”

While I think Larry Summers is brilliant, as he’s often described, I’ll charitably add that being Fed chair doesn’t match well with his skill set. As a rule of thumb, if the S&P 500 gains $125 billion in market value on the news that you won’t be in charge of the Fed, then that’s probably a sign that it wasn’t meant to be.

One interesting group to watch lately has been the homebuilders. The Homebuilders ETF ($XHB) had been a giant winner until this spring. XHB vaulted from $12 in October 2011 to $32 by this May. Then it started lagging the market as interest rates rose. From May 14th to August 14th, the XHB lost 10.6% while the S&P 500 gained 2.1%. That’s not a huge loss but it was a surprise after being such an easy winner for so long. But lately, the XHB has snapped back to life.

Our Buy List stocks are doing quite well this morning. AFLAC ($AFL) is back over $62 per share. FactSet ($FDS) and Ross Stores ($ROST) both hit new 52-week highs, and Cognizant ($CTSH) is close as well. Oracle ($ORCL) is doing well, but we’ll learn a lot more later this week when they report.

-

Morning News: September 16, 2013

Posted by Eddy Elfenbein on September 16th, 2013 at 6:17 amThree Losses to U.K. in a Week Limit EU Financial Reform Plans

Taiwan Chip Industry Powers the Tech World, But Struggles for Status

Indian Inflation Unexpectedly Accelerates As Food Prices Explode

Sahara Tomatoes Lure Graduates as Algeria Shifts From Oil

Eurozone Govts Must do More to Stimulate Investment: ECB Chief, Mario Draghi

How Bernanke Gets What He Wants Without Doing Anything

Former Obama Aide Summers Withdraws From Fed Chair Consideration

Five years After Lehman, Americans Still Angry at Wall Street

S&P Lifts JetBlue Rating on Improved Liquidity

American Airlines’ Plan Wins Bankruptcy Judge’s Approval

United Will Honor Free Tickets Sold By Mistake

Retailers Fight Exile From Gmail In-Boxes

Fiat CEO Says Chrysler To File For Listing This Week: FT

Epicurean Dealmaker: Go Ask Alice

Jeff Miller: Larry Summers Withdrawal: What Are The Implications?

Be sure to follow me on Twitter.

-

Blast from the Past

Posted by Eddy Elfenbein on September 15th, 2013 at 1:17 amThe New York Times:

Lehman Files for Bankruptcy; Merrill Is Sold

By ANDREW ROSS SORKIN

Published: September 14, 2008This article was reported by Jenny Anderson, Eric Dash and Andrew Ross Sorkin and was written by Mr. Sorkin.

In one of the most dramatic days in Wall Street’s history, Merrill Lynch agreed to sell itself on Sunday to Bank of America for roughly $50 billion to avert a deepening financial crisis, while another prominent securities firm, Lehman Brothers, filed for bankruptcy protection and hurtled toward liquidation after it failed to find a buyer.

The humbling moves, which reshape the landscape of American finance, mark the latest chapter in a tumultuous year in which once-proud financial institutions have been brought to their knees as a result of hundreds of billions of dollars in losses because of bad mortgage finance and real estate investments.

But even as the fates of Lehman and Merrill hung in the balance, another crisis loomed as the insurance giant American International Group appeared to teeter. Staggered by losses stemming from the credit crisis, A.I.G. sought a $40 billion lifeline from the Federal Reserve, without which the company may have only days to survive.

The stunning series of events culminated a weekend of frantic around-the-clock negotiations, as Wall Street bankers huddled in meetings at the behest of Bush administration officials to try to avoid a downward spiral in the markets stemming from a crisis of confidence.

“My goodness. I’ve been in the business 35 years, and these are the most extraordinary events I’ve ever seen,” said Peter G. Peterson, co-founder of the private equity firm the Blackstone Group, who was head of Lehman in the 1970s and a secretary of commerce in the Nixon administration.

-

The Scarecrow

Posted by Eddy Elfenbein on September 13th, 2013 at 4:45 pm

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His