-

Industrial Production Falls 0.5% in April

Posted by Eddy Elfenbein on May 15th, 2013 at 10:01 amSince the price of gold started falling, I suspected that deflationary pressures were stronger than most people realized. Today the government reported that wholesale prices dropped by 0.7% in April. That’s the biggest drop in more than three years. March had a drop of 0.6%. A lot of the decrease is due to lower energy prices, but even the “core rate,” which excludes food and energy, rose by just 0.1% in April.

The stock market is down slightly today. The S&P 500 is currently off by 3.20 points or 0.19%. Our Buy List is fairly quiet this morning, though I noticed that Ford Motor ($F) got up to $14.44 which is another new 52-week high. The S&P 500 has gone 177 days without a 5% pullback, which is a new record for this bull market.

The Federal Reserve said that U.S. industrial production fell by 0.5% in April. That’s the biggest drop in eight months. Manufacturing fell by 0.4% which was the third drop in the last four months. Today is the mid-way point of Q2 and the consensus among economists is that real GDP grew by 1.6% for the quarter.

The really exciting market has been the Japanese Nikkei. The index just broke 15,000 yesterday. Six months ago, it was below 8,700. On the downside, the Japanese yen has fallen against the dollar, but the Nikkei is still up impressively in dollar terms. For the first time in more than 20 years, there’s actual excitement about the Japanese economy.

-

Morning News: May 15, 2013

Posted by Eddy Elfenbein on May 15th, 2013 at 7:30 amGermany Can’t Stop Euro Zone From Sinking Into Longest Recession

King Says ‘A Recovery Is in Sight’

Documentary Depicts ‘Lost’ François Hollande As He Faces EU Pressure

EU Raids Oil Majors In Probe Over Possible Price Fixing

Oil Shockwaves From U.S. Shale Boom Seen by IEA Ousting OPEC

Import Prices Down 0.5% on Falling Oil Costs

Uninvited Guest Gives Japan’s Business Culture a Jolt

CBO Sees Brighter Economy With Budget Deficit To Plunge To $642 Billion This Year

HSBC Plans More Job Cuts in Effort to Save Up to $3 Billion

EU Regulators To Investigate Spanish Aid For Ford

In Role Reversal, Goldman Chief Advises Dimon

Baba Is 35-Year-Old Billionaire With Zombie and Bear Apps

Joshua Brown: The Death of Cold Calling

Phil Pearlman: Best of StockTwits Charts: Banks Taking Leadership Edition

Be sure to follow me on Twitter.

-

18 Tuesdays in a Row

Posted by Eddy Elfenbein on May 14th, 2013 at 4:11 pmIt’s official. The Dow has now risen for the last 18 Tuesdays in a row. The S&P 500 has risen for 15 of the 18 last days. The Dow climbed 123.57 points today to close at 15,215.25 while the S&P 500 added 16.57 points to finish at 1,650..34.

Our Buy List is now up 13% year-to-date which still trails the S&P 500 but not by much. Thanks to its dividend increase FactSet ($FDS) had a very good day. The stock rose 1.95% today. Several of our Buy List stocks such as Ford ($F), Wells Fargo ($WFC), Medtronic ($MDT), DirecTV ($DTV), Moog ($MOG-A) and Stryker ($SYK) hit new 52-week highs.

-

The Golden Age for Financial Stocks

Posted by Eddy Elfenbein on May 14th, 2013 at 1:06 pmIn December 2011, I changed my mind on the financial sector and said that it was finally a good buy. At the time, the Financial Sector ETF (XLF) was at $12.82 per share and today it’s been as high as $19.60. That’s a nice 52% run.

Actually, that call wasn’t completely out of the blue. Three months before, I said that the XLF would be a good speculative buy if it fell below $12. I wasn’t ready to say the sector was a flat out buy. The XLF did fall below $12. In fact, it briefly dropped below $11. As usual, market trends can last longer than you thought possible.

In the CWS Market Review from two months ago, I said that we’re in a Golden Age for investing in financial stocks.

Let’s run down some of the reasons why the financial sector is so appealing. The biggest is that the Federal Reserve is keeping short-term interest rates near 0% and has promised to keep them there for some time. The Fed’s position clears up a lot of uncertainty, and Wall Street likes it that way. Another big reason in favor of financials is that the economy is slowly improving. At a firm like Nicholas Financial, the overall quality of their loan portfolio has improved dramatically.

We also have to look at the mortgage market. For obvious reasons, many financial stocks are closely tied to the mortgage market, and the U.S. housing sector continues to improve. Thanks to Bernanke and his friends at the Fed, the bond-buying policy has pushed down mortgage rates and they’ll probably stay low. This time, the improvement in the housing market is far sounder and more sustainable than it was last decade. Let’s not forget that lending standards have thankfully improved.

Another key point is that valuations for many financial stocks are still quite modest. JPM just broke though $50 per share and it’s going for less than nine times Wall Street’s estimate for next year’s earnings. Based on Thursday’s close, JPM yields 2.4% and I’m expecting the bank to raise its dividend soon. I think the current 25-cent quarterly dividend will go up to 30 cents per share. That would still be less than 22% of their full-year earnings.

Given the current environment, I doubt many investors will be able to beat XLF this year or do it with less volatility. We’re going to look back at this era as a great time to buy financial stocks.

I turned out to be right about JPM’s dividend. Less than a week later, the bank raised its dividend to 30 cents per share.

-

FactSet Research Boosts Quarterly Dividend

Posted by Eddy Elfenbein on May 14th, 2013 at 10:49 amFactSet Research Systems ($FDS) announced today that it’s increasing its dividend by 12.9%. The quarterly dividend will rise from 31 cents per share to 35 cents per share.

In the big picture, FactSet’s dividend is pretty small. The new dividend translates to a yield of just 1.45% based on yesterday’s close. But what impresses me is the company’s record of continually increasing its dividend. In 2005, their dividend was just five cents per share. FactSet has increased its earnings every year for the last 16 years, and they’re going to do it again.

-

Citizen Pittman

Posted by Eddy Elfenbein on May 14th, 2013 at 8:55 am

Mark Pittman is a guy whose life should be made into a Hollywood movie.

Actually, it already has, sort of. He’s one of the chief commentators to appear in an indie documentary, American Casino, about the subprime-mortgage debacle. His encyclopedic knowledge of the events of 2008 contributed handsomely to what the film’s directors called its “thriller-like exposition.”

Pittman’s own story, however, is even more thrilling than some of the Wall Street scams he spent 15 years of his life exposing. He’s the guy, you see, who dared to sue the Fed. And he won. Vindicated, with all the justice in the world on his side, in the eyes of no less august an institution than the U.S. Federal Courts.

The tragedy is that he didn’t live to enjoy the spoils of his battle with America’s most powerful bank.

It all started with a series of articles Pittman, a veteran financial reporter, wrote for Bloomberg News back when the witches’ brew of Wall Street malfeasance was still coming to a boil. In them, he was among the first to point out the precariousness of the financial markets, with their endless, incomprehensible repackagings and resellings. Later he was the first to detail how Goldman Sachs, Morgan Stanley, and the rest profited from the government’s bailout of AIG. Still later, not one to rest on his laurels, he demonstrated Hank Paulson’s curious double role in the crisis, as one who had both made the mess and later been hired to clean it up.

Award-winning work, all of it, but Pittman was just getting started. In late 2008, as the financial system was hemorrhaging and the government was scrambling to perform triage, Pittman wrote some numbers on a dry-erase board, scratched his head, and asked a simple question: How much money was the government spending, and where was the money going? Doing some simple math, he arrived at a figure of some $12.8 trillion, not all of it clearly accounted for. Later analysts have contested this sum, but correct or no, it’s indisputable that the Federal Reserve in particular refused to disclose who exactly was receiving the $2 trillion it had earmarked for distribution.

Pittman’s next move was to file a Freedom of Information Act request. He reasoned that it was the taxpayers’ money, and that those taxpayers therefore had a right to know just what the Fed was doing with it. The bank stonewalled. Pittman filed another request. Again the Fed refused to play ball.

So Pittman sued. Together with Bloomberg News, he brought the case to federal court, where a judge found that the Fed was indeed obliged to hand over the data requested, and gave the bank five days to comply. Still the Fed didn’t want to do the right thing. It filed appeal after appeal, until finally it was given a stay of implementation until the case could be heard by the Supreme Court. The latter, however, declined to get involved, thus effectively upholding the lower courts’ anti-Fed ruling.

At this point, one would think the Fed would be gracious and concede the victory to its opponents, but still the data were not forthcoming. They began to publish printouts of e-mails, communications logs—anything and everything but the data requested. So that when Pittman died on November 25, 2009, his soul may have gained access to paradise, but his case was still in bureaucratic limbo, endlessly waiting.

But his determination wasn’t for nothing. Some two years later, just before Christmas of 2011, the Fed finally released spreadsheets that detailed the amounts borrowed by some 400 banks. Some have argued that the data actually make the Federal Reserve look good, but all agree the information represents a victory for those in favor of greater government transparency. Scholars and financial analysts can better sort through the wreckage now that one of the black boxes has come to light.

One of Pittman’s friends, Congressman Brad Miller, eulogized the intrepid reporter thus in The Huffington Post:

What made it so entertaining to talk with him was his irreverence for the financial industry, which was a refreshing contrast to the industry’s self-reverence. He didn’t have an angry, confrontational ‘Speak Truth To Power!’ attitude towards the industry; he just saw them as grifters. Mark didn’t see much difference between selling AAA-rated bonds backed by subprime mortgages and sending e-mails claiming to be African royalty in need of help transferring a fortune to a U.S. bank, and he was amused by the financial industry’s pretensions that they were making a great contribution to our economy.

Hollywood would barely have to doctor Pittman’s story to sell it to audiences. Its narrative arc is as perfect as its protagonist’s integrity.

-

Morning News: May 14, 2013

Posted by Eddy Elfenbein on May 14th, 2013 at 7:03 amECB Picks Fight With Germany on EU Plans for Failing Banks

Grind of Euro Crisis Wears Down Support for Union, Poll Finds

Janet Yellen, a Top Contender at the Fed, Faces Test Over Easy Money

Retail Sales in U.S. Unexpectedly Increase on Broad-based Gains

Supreme Court Supports Monsanto in Seed-Replication Case

U.S. Hedge Fund Calls For Sony Entertainment Spin-Off

SolarCity Posts Loss as Spending on New Systems Increases

Amazon Introduces Amazon Coins — Virtual Currency for Buying Apps and Games

How A CEO Can Wreck A Brand In One Interview: Lessons From Abercrombie & Fitch Vs. Dove

Lehman Reaches Beyond Grave to Grab Millions From Nonprofits

Verizon Wireless Agrees to Pay Co-Owners $7 Billion Dividend

Bloomberg’s Top Editor Calls Client Data Policy ‘Inexcusable’

Jeff Carter: 500 Startups: Risk vs Reward, Do VCs Execute?

Credit Writedowns: Zero Rates Mean Americans Are Giving Up On Certificates Of Deposits

Be sure to follow me on Twitter.

-

Dylan the Day-Trader

Posted by Eddy Elfenbein on May 13th, 2013 at 12:27 pmIn the Washington Post, Steven Pearlstein profiles a 25-year-old day-trader named Dylan Collins. Frankly, it’s a scary existence. I’m happy to say that I have neither the interest or skills to be a day-trader.

Dylan started at AMR in August 2010. He didn’t have a positive trading month until January. He didn’t “make his bank” and get his first paycheck until May. In June, he lost it all.

“There was this Canadian company, Sino-Forest, that we were all buying,” Dylan says. “It looked like the perfect contramove. Then, all of a sudden, trading was halted because of a federal investigation, and it turned out the whole thing was a Ponzi scheme. The whole office lost somewhere between 1 and 2 million dollars. For me it was devastating. . . basically I had to start back at square one.”

Within a few weeks, however, markets were roiled by the first big troubles in the euro zone. Markets became, Dylan recalls, “insanely volatile” — exactly the conditions in which the office at West Palm thrives. By the end of July, Dylan had made back his “bank.” In August, a year into the job, his trading profits were $70,000, two-thirds of which went to him.

It was up and down after that, and more up than down, with swings of as much as $30,000 a month. His $25,000 “bank” grew to $100,000 as he put more and more of his earnings back into the pot. Then, one day last August, Knight Capital, a small investment bank, suffered a glitch in its automated trading that caused trading in dozens of stocks to go haywire. This was just the sort of unexplained, irrational price deviations that are manna from heaven for Dylan and his colleagues. They dove in with all they had. On that day alone, Dylan’s trading profits exceeded $140,000.

A lot of people have moral problems with what Dylan and AMR do. Not me. The market has pricings and they fix them. Assuming you can consistently exploits the market’s mistakes for money–it’s a young man’s game.

“The reason why there aren’t older guys in the office is because of the stress,” Dylan says. “I can see even now that you can get burned out after doing it for five, 10 years. There are nights you can’t sleep because you’re so exposed, or you lie there thinking about the big jobs number that is coming out tomorrow and you know you’re either going to earn $50,000 or lose $50,000, but you don’t know which.”

Under stress, a trader is apt to become too cautious or too comfortable with one trading strategy — and before long he’s caught in one of those self-reinforcing downward spirals of declining income, declining confidence and declining risk tolerance.

Perhaps with that in mind, a couple of the more successful West Palm alumni cashed in their chips, moved back to where they came from and made the transition from day trading to longer-term investors. -

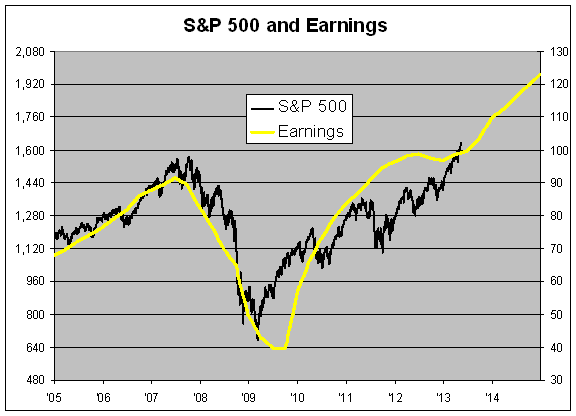

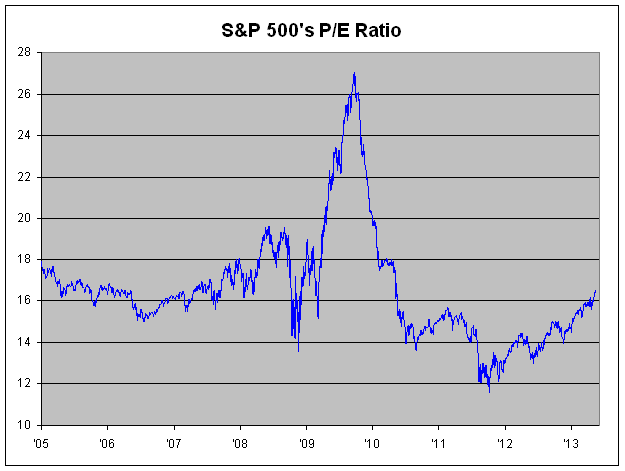

Three-Year High for the S&P 500’s P/E Ratio

Posted by Eddy Elfenbein on May 13th, 2013 at 10:00 amOn Friday, the Price/Earnings Ratio for the S&P 500 closed at a three-year high. By historical comparisons, the P/E Ratio still ain’t that high. It’s currently at 16.49. The ratio has been quite low for the last few years. At its low point in October 2011, the S&P 500’s P/E Ratio touched a 22-year low. All told, the market’s P/E Ratio was expanded by more than 40% which adds a nice breeze to any market rally.

Here’s a look at the S&P 500 (black line, left scale) along with its earnings (yellow line, right scale). I scaled the two lines at a ratio of 16-to-1 so whenever the lines cross, the P/E Ratio is exactly 16. As you can see, we just dipped our heads above the line. For technical note, I’m using the operating earnings as provided by S&P.

Let me point out a few deficiencies of the P/E Ratio. (By the way, just because there are some problems with a metric doesn’t make it useless. You simply need to be aware of its limitations.) The P/E Ratio is made up of two numbers, the price and the earnings. Price is a fixed-point number. You know exactly what it is at any point in time. Earnings, however, are a ratio. It’s the amount of money earnings between two points. The P/E Ratio mixes these two numbers. That usually isn’t an issue, but sometimes it can be.

The biggest problem is that stock prices look ahead while earnings tell you what just happened. Notice how in 2009 the stock market, the black line correctly anticipated the upturn in earnings, the yellow line. Because of the mismatch, the P/E Ratio soared. I remember this caused a lot of consternation among market bears. The P/E Ratio was telling us the market was expensive when it was really its cheapest.

Here’s a look at the market’s P/E Ratio. It’s the exact same graph as above except it’s the black line divided by the yellow line.

But we can also see something interesting about the market crackup in 2007 and 2008. What makes that period noteworthy is that it was largely unexpected as the stock prices quickly reacted to crumbling earnings. On the other hand, you can see how market downdrafts in 2011 and 2012 were incorrect expectations of trouble ahead. Perhaps the market was so burnt in 2008 that it’s become overly cautious today.

The issue for us right now is the stalling out of earnings growth over the last few quarters. The future part of the yellow line is Wall Street’s forecast. If analysts are correct that this is just a small notch in an upward earnings trend, the market is probably underpriced. At ratio of 16 and expected earnings of $123.13, it could be at 1,970 by the end of next year. That’s a 20.6% gain in about 20 months.

Of course, that involves a lot of assumptions that are probably too thin to rely on. Last year, I recall Barry Ritholtz pointing out a chart showing the success rate of analysts’ forecasts. It’s not an enviable record. To oversimplify things, corporate earnings tend to go in two modes — slow, steady rises or sharp dropoffs. Analysts try to split the difference by almost always predicting modest increases. As a result, they’re usually slightly too pessimistic or wildly overly optimistic. The hard part is catching the economy’s turning points. Once you’ve mastered that (LOLz), everything else is easy.

-

Morning News: May 13, 2013

Posted by Eddy Elfenbein on May 13th, 2013 at 6:42 amConfusion Reigns: Europe Bickers Over Banking Union

Malta Unlikely To Follow Cyprus Into Crisis

Japan Shares Rise, Bonds Fall on G-7 Tolerance as Gold Declines

China—Slower and More Unbalanced

China’s Investment Slows as Production Trails Estimates

Chinese Creating New Auto Niche Within Detroit

In Taiwan, Lamenting a Lost Lead

What Saudi Arabia Thinks About the U.S. Oil Boom

Gold Bears Pull $20.8 Billion as BlackRock Says Buy

Goldman: The S&P Has Already Hit Our Year-End Price Target, But We Think It Will Go A Lot Higher

Privacy Breach on Bloomberg’s Data Terminals

CEO Sees Profit, IPO for Virgin America

Google+ Struggles To Attract Brands, Some Neglect To Update

Jeff Miller: Weighing The Week Ahead: Are Consumers Ready To Buy? What About Housing?

Epicurean Dealmaker: Go Ahead, Live a Little

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His