-

CWS Market Review – February 15, 2013

Posted by Eddy Elfenbein on February 15th, 2013 at 6:07 am“Individuals who cannot master their emotions are ill-suited to

profit from the investment process.” – Benjamin GrahamRemember when stock prices used to change each day?

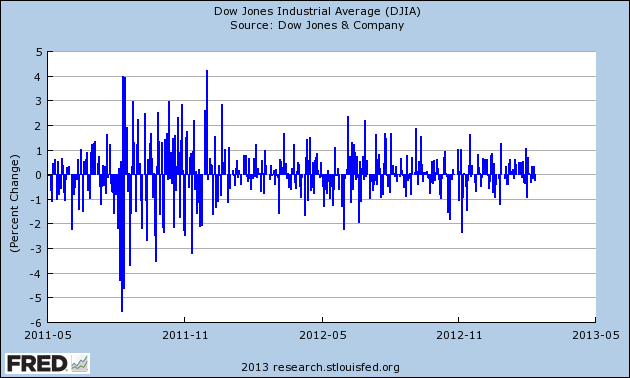

OK, I’m exaggerating…but not by much. Bespoke Investment Group notes that the average daily spread between the high and the low on the Dow Jones is at a 26-year low. Stocks simply ain’t moving around very much these days.

While the stock market got off to a great start this year, since late January it’s nearly slowed down to a complete halt, particularly the intra-day swings. The Volatility Index ($VIX) is near a six-year low. Fortunately, the little volatility there has been has been positive, so the broad market indexes have continued to rise, albeit very slowly. On Thursday, the S&P 500 closed at its highest level since Halloween 2007.

One theme that’s been dominating Wall Street lately is the idea of a Great Rotation, meaning money will massively swarm out of bonds and into stocks. I do think some of that will happen—in fact, it’s currently happening—but I don’t foresee sky-high bond yields anytime soon. The 10-year T-bond is right at 2%, which is pretty darn low. Instead, what we’re seeing is investors gradually becoming bolder and taking on more risk. That’s very good for our style of investing.

In this week’s CWS Market Review, I want to take a closer look at this moribund market. As quiet as it’s been, I don’t think the market’s reticence will last much longer. I also want to highlight an outstanding earnings report from DirecTV ($DTV). The stock crushed Wall Street’s estimate by 42 cents per share! We’ll also focus on Bed, Bath & Beyond ($BBBY), which has finally drifted low enough to be a very compelling buy. But first, let’s look at what’s been happening on the street of dreams.

Investors Need to Focus on High-Quality Stocks

One important development is that economically cyclical stocks are again leading the market. If you recall, the cyclicals began a massive rally last summer right around the time when Mario Draghi promised to do “whatever it takes” to save the euro. The cyclicals were given another boost a few weeks after that when the Fed announced its QE-Infinity program.

Consider this: If the S&P 500 had kept pace with cyclicals, it would be at about 1,750 today instead of 1,521. Cyclical leadership finally petered out in late January but has come back with a vengeance. The Morgan Stanley Cyclical Index (CYC) has outpaced the S&P 500 for five days in a row. The ratio of the Cyclical Index to the S&P 500 is now close to an 18-month high.

I think there are two reasons for this trend. One is simply that many cyclical stocks got very cheap. I think our own Ford Motor ($F) is a perfect example of that. Harris ($HRS) and Moog ($MOG-A) are other good examples. But another reason is that economy is probably better than many analysts realize. The negative GDP report for Q4 understandably upset a lot of folks, but the recent trade numbers will probably cause that negative 0.1% to be revised upward to somewhere around +1.0%.

Earnings for Q4 have been pretty. According to data from Bloomberg, 73% of the 288 companies in the S&P 500 that have reported Q4 earnings have topped estimates; 67% have beaten sales estimates. As I’ve discussed before, the major concern is that corporate profit margins have been stretched about as far as they can go. I’m concerned that Wall Street’s earnings forecasts are too optimistic, and we’re going to see a spate of earnings as the year goes on.

One of the interesting aspects of the recent rally is that the large mega-caps haven’t really joined in. Since the beginning of October, the S&P 100, which is the biggest stocks in the S&P 500, has consistently lagged the S&P 500. That’s not necessarily bad news, but it means that the little guys are getting most of the gains. One possible worry is that the gains are largely going to low-quality names. That’s often a sign of a market peak. Our Buy List, for example, started trailing the overall market in 2007. But when the plunge came, we didn’t fall nearly as much as rest of the market.

Until this sleepy market eventually wakes up, I urge investors to focus on top-quality. Please pay close attention to my Buy Below prices on the Buy List. We don’t want to go chasing after stocks. Let the good stocks come to you. Speaking of which, my favorite satellite TV stock just reported great earnings, and the stock is lower than where it was five months ago.

Buy DirecTV Up to $55 per Share

We had very good news on Thursday when our satellite-TV stock, DirecTV ($DTV), reported blow-out earnings for Q4. The company raked in $1.55 per share for the quarter, which creamed Wall Street’s forecast by 42 cents per share. Wow! For comparison, DTV made $1.02 per share in the fourth quarter of 2011,

So what’s the secret to DirecTV’s success? That’s easy; it’s all about Latin America. DirecTV has done very well in the United States, but that’s a fairly saturated market. Not so in the Latin world, where satellite TV demand is just getting started. DTV now has 10.3 million subscribers in Latin America, up from 7.9 million one year ago. Last quarter, DirecTV added 658,000 customers in Latin America, which was a lot more than expected.

For Q4, DirecTV added 103,000 subscribers in America, which brings their total to 20.1 million. That’s a big business, and I especially like anything involving recurring revenue. The company said it expects to see mid-single-digit revenue growth in the U.S. over the next three years. I was also pleased to see that the cancellation rate in the U.S. dropped from 1.52% to 1.43%. DirecTV has specifically made an effort to increase retention. The cost of adding one new subscriber is far more than that of retaining an existing one. For all of 2012, DTV had a solid year, earning $4.58 per share.

The only negative is that DTV said its earnings will take a one-time hit from the currency devaluation in Venezuela. The company also announced a $4 billion share buyback, which is equivalent to about 13% of DTV’s market value. I think DTV should have little trouble earning $5 per share this year. This is a good stock going for a good value. DirecTV remains an excellent buy up to $55.

Bed, Bath & Beyond Is Finally Looking Cheap

I want to focus on Bed, Bath & Beyond ($BBBY), which had been one of my favorite Buy List stocks, but a string of earnings warnings rocked the shares last year. While 2012 was unpleasant, I think the stock has now fallen back into being a very good buy at this price.

Let’s review what happened last year. In June 2012, Wall Street had been expecting fiscal year earnings (ending February 2013) of $4.63 per share, which represented 14% growth over the year before. But the company surprised investors by telling us to expect earnings growth somewhere between the single digits and the low double digits.

No biggie, right? Guess again. Traders gave BBBY a super-atomic wedgie as the stock got crushed for a 17% loss in one day. Now here’s the odd part: Here we are eight months later, and it looks like BBBY will earn about $4.54 per share for the year, give or take. In other words, that dreaded earnings warning turned out to be about 2% or so.

After the earnings report in September, BBBY got hammered for a 10% one-day loss when it reiterated the exact same full-year forecast. Then, for the December earnings report, BBBY only got nailed for 6.5% after it reiterated, you guessed it, the exact same full-year earnings forecast.

For Q4 (which covers the holidays so it’s the big dog of BBBY’s fiscal year), the company said earnings would range between $1.60 and $1.67 per share. The Street was expecting $1.75 per share. C’mon, this lower guidance isn’t that bad. But traders have lost confidence in BBBY. The shares have plunged from over $75 in June to as low as $55 in December, although it’s come up a bit since then.

Now let’s run some numbers: If Bed, Bath & Beyond can increase earnings by 10% for next fiscal year (which begins in two weeks), that should bring them to roughly $5 per share. That means we’re looking at a stock that’s going for less than 12 times earnings and growing at 10% per year. Furthermore, the recovering housing market should continue to aid them. While BBBY looks cheap, I suspect it will take a while before the stock comes back to life. The earnings warnings really spooked traders. The next earnings call isn’t until April 10. Bed, Bath & Beyond is a good buy up to $60 per share.

That’s all for now. Next week, the stock market will be closed on Monday in honor of George Washington’s birthday. On Tuesday morning, Medtronic ($MDT) will report fiscal Q3 earnings. Last month, MDT bumped up the low end of their fiscal year guidance. We’ll also get the CPI report on Thursday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. I recently posted a list of 11 very overpriced stocks that you should sell ASAP.

-

Morning News: February 15, 2013

Posted by Eddy Elfenbein on February 15th, 2013 at 5:45 amWar Not Worth Winning as G-20 Debates Yen Intentions

Weidmann Says ECB Won’t Cut Interest Rates to Weaken Euro

Confidence on Upswing, Mergers Make Comeback

Berkshire and 3G Capital in a $23 Billion Deal for Heinz

US Airways CEO Parker Is Man Behind The Merger

Icahn Ups Stakes in Ackman Feud With Herbalife Holding

PepsiCo 4th-Quarter Profit Rose 17%; Issues Weak Year View

G.M.’s Profit Rises Despite Weakness in Europe

CBS Profit Misses Estimates as Streaming Revenue Slumps

PPR Predicts 2013 Growth as Bottega Veneta Leads Luxury Boom

Under Armour Finds Feminine Side to Go Beyond $2 Billion

Blackstone Keeps Most of Its Money With SAC

De Beers Sees Glimmer Of Hope For Hard-Pressed Diamond Market

Joshua Brown: Why Investors Need to Understand “Total Yield”

Jeff Carter: European GDP Takes a NoseDive

Be sure to follow me on Twitter.

-

My Favorite Heinz Movie Reference

Posted by Eddy Elfenbein on February 14th, 2013 at 11:55 amAngela Lansbury and James Gregory in The Manchurian Candidate:

-

$72.50 is Too Much for Heinz

Posted by Eddy Elfenbein on February 14th, 2013 at 11:08 amWarren Buffett’s Berkshire Hathaway ($BRKB) has agreed to buy H.J. Heinz ($HNZ) in a deal worth more than $23 billion. The deal calls for HNZ shareholders to get $72.50 per share in cash. That’s a 20% premium to yesterday’s closing price.

I like Heinz. It’s a great consumer staples business: steadily rising sales, earnings and dividends. My concern, however, is the buyout price. I think Buffett is paying far too much for Heinz. Here are the earnings-per-share figures for the last few years: $2.38, $2.63, $2.90, $2.87, $3.08, $3.35. We’re half-way through this fiscal year (which ends in April) and HNZ is on track to earn $3.54 per share, and the Street expects 3.79 per share for next year.

That’s a good trend. Heinz is growing but it really isn’t growing that fast. Over the last nine years, sales have increased from $8.24 billion to $11.65 billion. That’s less than 4% per year.

I understand that the market places a premium on stability of earnings but I have a hard time valuing Heinz at more than $60 per share. And that’s just at fair value. If I were looking to get Heinz at a bargain, I would be more interested in seeing close to $50 per share.

I should point out that Buffett’s part of the deal is quite good. He’s putting up $4.4 billion in equity and buying $8 billion of 9% preferred stock. At the elevated price, the equity will yield 2.84%.

-

DirecTV Earns $1.55 Per Share

Posted by Eddy Elfenbein on February 14th, 2013 at 9:59 amGreat news this morning from DirecTV ($DTV). The satellite-TV company reported blow-out earnings. For Q4, DTV earned $1.55 per share which was up from $1.02 per share a year ago. Wall Street has been expecting $1.13 per share so this was a big beat.

The key to DirecTV’s success is its business in Latin America. They’re growing very well there. DTV now has 10.3 million subscribers in that region which is up from 7.9 million one year ago. Last quarter, DirecTV added 658,000 customers in Latin America which was more than expected.

DirecTV is still huge in the United States, but growth has slowed down as the market has matured. Last quarter, DTV added 103,000 subscribers in the U.S. to bring their total to 20.1 million. I was also pleased to see that the cancellation rate in the U.S. dropped from to 1.43% from 1.52% last year.

The only negative is that DTV said its earnings will take a hit from the currency devaluation in Venezuela. The company also announced a $4 billion share buyback which is equivalent to about 13% of DTV’s market value. The shares have been up as much as 3.4% today. For all of 2012, DTV earned $4.58 per share.

-

Morning News: February 14, 2013

Posted by Eddy Elfenbein on February 14th, 2013 at 7:20 amEuro Zone 2012: Not a Single Quarter Showing Economic Growth

BOJ Chief Defends Policy Ahead Of G20 As Economy Contracts

Indian Inflation Slows to 38-Month Low; Boosts Rate-Cut Case

BNP Paribas Begins Overhaul After Fourth-Quarter Profit Drop

Obama Bid for Europe Trade Pact Stirs Hope on Both Sides

Calmly, Pick for Treasury Offers Replies to Senators

401(k) Balances Reached Record on 2012 Stock Market Rally

Small Businesses Still Struggle, and That’s Impeding a Recovery

American and US Airways Announce $11 Billion Merger Deal

Citigroup Lost $15 Million With UBS’s ‘Crap’ CDO Blessed by S&P

Cisco Forecasts Sales That Miss Some Analysts’ Estimates

Rio Tinto’s New CEO Vows Cost Cuts And Disposals

India’s Tata Motors Q3 Net Profit Halves, JLR Margin Sags

Groupon Surges on Expected E-Commerce Expansion

Credit Writedowns: Japanese RORO

Roger Nusbaum: Not All Stock Picking is Wildly Complex

Be sure to follow me on Twitter.

-

11 Stocks to Sell Right Now

Posted by Eddy Elfenbein on February 13th, 2013 at 12:01 pmHere’s a list of 11 stocks that investors should sell as soon as possible. I’ve included yesterday’s closing price for future reference.

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His