-

Fiserv Earned $1.39 Per Share for Q4

Posted by Eddy Elfenbein on February 5th, 2013 at 4:14 pmFor Q4, Fiserv ($FISV) earned $1.39 per share which matched Wall Street’s forecast.

Fiserv, Inc., a leading global provider of financial services technology solutions, today reported financial results for the fourth quarter and full year 2012.

GAAP revenue was $1.16 billion and adjusted revenue was $1.08 billion in the fourth quarter, both consistent with the fourth quarter of 2011. For the full year, GAAP revenue was $4.48 billion compared with $4.34 billion in 2011. Adjusted revenue was $4.20 billion compared with $4.07 billion in 2011, an increase of 3 percent.

GAAP earnings per share from continuing operations for the fourth quarter was $1.18 compared with $1.07 in 2011. GAAP earnings per share from continuing operations for the full year was $4.34 compared with $3.40, which included a loss from early debt extinguishment of $0.37 per share, in 2011.

Adjusted earnings per share from continuing operations in the fourth quarter increased 9 percent to $1.39 compared with $1.27 in the fourth quarter of 2011. Adjusted earnings per share from continuing operations for the year grew 12 percent to $5.13 compared with $4.58 in 2011.

“Our 2012 results were highlighted by our 27th consecutive year of double-digit adjusted earnings per share growth and meaningful strategic progress,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “We capped off a strong sales year with exceptional performance in the fourth quarter.”

This basically matches what Fiserv told us to expect three weeks ago. Fiserv earned $5.13 per share for the entire year. They expect growth of 15% to 18% for this year, and specified an earnings range of $5.88 to $6.07 per share. If that’s correct, then FISV is going for less than 14 times this year’s earnings.

-

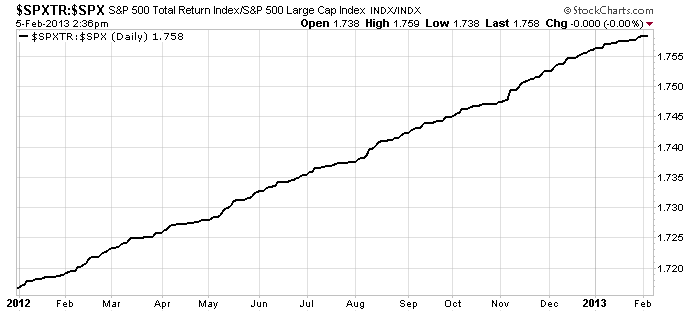

Total Return to Dividends

Posted by Eddy Elfenbein on February 5th, 2013 at 2:43 pmHere’s an interesting chart. This shows the S&P 500 Total Return Index divided by the S&P 500. In other words, this shows an investor’s return solely from dividends.

There seems to be a surge every three months (mid-May, mid-August, mid-November, and less so in February), when the bulk of dividends are paid out. You can also see that the fourth quarter was especially good for dividends as companies rushed to beat the taxman.

I think investors too often ignore dividends. Not only do you get money, but dividends are a good way to gauge a company’s health. It’s not fool-proof, but when a company raises its quarterly dividend, it’s often a sign of confidence that business is going well.

-

Walgreen Breaks $41

Posted by Eddy Elfenbein on February 5th, 2013 at 1:35 pmLast March, I tweeted:

$WAG is looking like a good value. Earnings are next week. Anyone else think it can be a $40 stock? $$

At the time, shares of Walgreen ($WAG) were at $33.56. This morning, the company reported strong sales for January thanks to flu season. The stock has been as high as $41.61 today which is a new 52-week high. The stock has done about three times better than the S&P 500.

-

Canada Fires Its Penny

Posted by Eddy Elfenbein on February 5th, 2013 at 12:33 pmFrom the Chicago Tribune

The Canadian government has begun to phase out the penny, saying it’s too expensive to produce the coin.

Besides its “excessive” production value, Canada has long cited the significant handling costs for the nation’s retailers and environmental considerations that lessen the penny’s worth. The country, which produced its last pennies on Monday, estimates the move will save taxpayers about $11 million a year.

The potential savings have enticed U.S. officials to consider the possibility as well.

Cash transactions in Canada will now be rounded to the nearest 5-cent mark. The penny’s retirement will have no effect on payments made by checks or credit cards.

For example, if the total price of coffee and a sandwich is $4.92, a customer that was paying in cash would owe $4.90, according to the Royal Canadian Mint. But those using another method of payment would pay $4.92, and the pennies would be tallied electronically.

The cost of the metal that goes into a penny has surged in recent years, making the coin’s production more expensive than its face value.

In the U.S., it now cost 2.41 cents to make every penny, which is made mostly of zinc. The penny has cost more than its face value since 2006.

Although the U.S. has conducted significant research into alternatives for the penny, the U.S. Mint says it still needs more research before it can make a decision to either change its composition or do away with it altogether.

Any new materials for the penny would need to simulate the current look and durability of the nation’s most circulated coin.

-

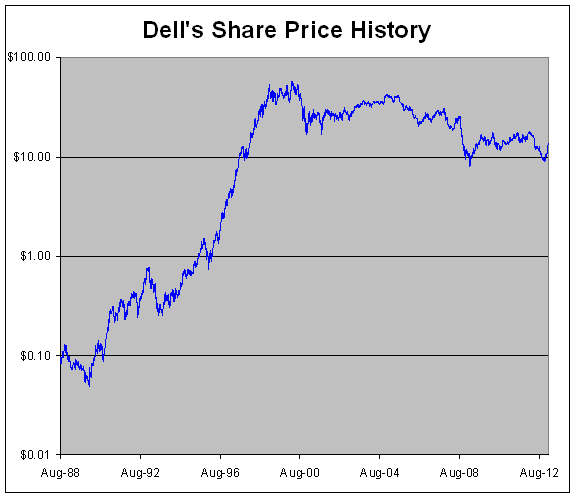

Dell to Go Private at $13.65

Posted by Eddy Elfenbein on February 5th, 2013 at 9:59 amIt’s official. Dell is going to be taken private. A group of investors led by Michael Dell will buy the entire firm for $13.65 per share. Interestingly, Microsoft will lend the buyout syndicate $2 billion for the deal.

Let’s look at some numbers: Dell’s IPO was on June 22, 1988 at $8.50. Since then, the stock has split 96-for-1 so that initial price works out to 8.85 cents per share. The buyout price is 154 times the IPO price. At one point in the late-1990s, shares of Dell split 2-for-1 three separate times in less than one year. At one point, Dell split 2-for-1 six times in just over 40 months.

Dell was actually not a screaming success as an IPO. The shares did indeed rally from the IPO price of $8.50 to a high of $12.50 by October 25, 1988 (or 13 cents adjusted for splits). But after that, Dell plunged to an all-time low of $4-5/8 by early 1990 (or 4.8 cents).

Then Dell put on one of the most remarkable runs in the history of capitalism. The shares skyrocketed to an all-time high close of $58.13 on March 22, 2000 ($59.69 intraday). During the decade of the 1990s, Dell advanced 890-fold which works out to 97% per year. Today’s buyout price is 77% below Dell’s high reached 13 years ago.

-

Legacy of Benjamin Graham

Posted by Eddy Elfenbein on February 5th, 2013 at 9:37 am -

Morning News: February 5, 2013

Posted by Eddy Elfenbein on February 5th, 2013 at 7:15 amEuro Zone Economy Shows Signs Of Recovery

Momentum Suggests Investors Seeking Euro Exit

World Risks ‘Perfect Storm’ on Capital Flows, Carstens Says

Platinum Trades Near 17-Week High on Concern Supplies Will Fall

McGraw-Hill, S&P Sued by U.S. Over Mortgage-Bond Ratings

The Morning Ledger: DOJ vs. Rating Firms

UBS Posts Quarterly Loss on Libor Fine, Reorganization

Barclays Sets Aside Additional $1.6 Billion on Misselling

Malone Eyes Virgin Media in Challenge to Murdoch

Dell Nears a Buyout of More Than $23 Billion

Toyota Raises Fiscal-Year Outlook

Seeking a Company’s Elusive Sales Data

Roger Nusbaum: Charlie Sheen Portfolion (winning)

Howard Lindzon: Momentum Wrap – Expected Pullback

Be sure to follow me on Twitter.

-

Predicting Disaster Is a Great Business

Posted by Eddy Elfenbein on February 4th, 2013 at 12:25 pmOne of my constant complaints about market commentary is that predictions of doom and gloom are rarely held accountable. Bearish news sells and the scarier the better.

I don’t mind people saying bad things will happen, but I do mind the way that certain (not all) perma-bears are allowed to move the goal posts with their predictions. They key, it seems, is to never give a time horizon for the Apocalypse. That way, you’re never wrong, just a little early.

There’s a mini-industry of folks who predict the most outrageous events, and then when something bad comes along, they claim credit for predicting it.

Sixteen months ago, the BBC had Alessio Rastani on as a guest. I’m still not exactly sure who this clown is, but he said that the market was about to collapse, and he got a huge amount of attention.

Since then, the Dow has gained 3,000 points and no one seems to care how badly Rastani was off the mark. Note that the embedded video has more than 2.2 million views, and likes outnumber dislikes by 14-to-1.

-

“We Are Way Overdue for Some Sort of Bullshit Crisis”

Posted by Eddy Elfenbein on February 4th, 2013 at 11:18 amIn the WSJ, Scott Adams makes the case to “buy, buy, buy“:

Should you dive into the stock market? Absolutely. And if you have no money to invest, I recommend getting cash advances against your credit cards. And stop eating, entertaining, and saving for your kids’ educations. Sell your blood if you need to. Put all of that extra money in the stock market. My reasoning is simple: I own stocks and I want you to drive up their prices.

I have a feeling that the smart money is already in the market and those folks are crouching like sprinters, waiting for any sign of bad news. Meanwhile, we are way overdue for some sort of bullshit crisis like the Year 2000 bug, or California going into a death spiral, or an artificial debt limit, or North Korea testing a satellite-based death-ray. When the new fake crisis happens, sometime within the next month, the market will pull back 10%. That’s when I expect to go into a panic and start selling my stocks at a loss.

What the stock market needs – and what I need – is for lots of people who know absolutely nothing about investing to pile into the market and buy broad market ETFs. Then I need those people to poke out their own eyes and caulk their ear holes so they don’t accidentally encounter any news. I don’t think that is too much to ask.

-

Factory Orders Weigh on Market

Posted by Eddy Elfenbein on February 4th, 2013 at 11:06 amThe stock market is backing off the five-year highs it made on Friday. The S&P 500 is currently down 10 points or about 0.7%.

The Commerce Department said that factory orders rose by 1.8% in December which was below the 2.3% Wall Street was expecting. The number for November was revised down to a 0.3% drop.

A fourth-quarter pickup in consumer spending is spurring companies including automakers such as Chrysler Group LLC and Ford Motor Co. (F), reviving a manufacturing industry that cooled in the second half of 2012. The acceleration extended into January, according to a gauge last week that showed factories expanded at the strongest pace in nine months.

“Manufacturing’s fine,” said Brian Jones, senior U.S. economist at Societe Generale in New York, who projected a 1.9 percent gain in orders. “The economy continues to improve.”

The bright spot in today’s report is that demand for durable goods rose by 4.3%. That increase was helped by a 12.2% increase in construction equipment and a 6.4% rise for computers.

On our Buy List, Oracle ($ORCL) is buying Acme Packet for $2.1 billion.

The deal is Oracle’s biggest since it bought Sun Microsystems in 2010 for about $7 billion. The company bought nearly a dozen companies in 2012, including Eloqua Inc for $810 million in December.

Telecom carriers have been dumping wireline and other legacy services as people increasingly use a newer breed of devices to access Internet and businesses shift to IP (internet protocol) networks, an area where Acme Packet specializes.

“Users are increasingly connected and expect to communicate anytime and anywhere using their application, device, and network of choice,” Oracle said in a statement.

Oracle Chief Executive Larry Ellison, who has used acquisitions to boost the company’s revenue dramatically over the past decade, had said in October he would not rule out a big deal “down the road”.

Oracle has rallied almost non-stop since the middle of November. From the November 14th low to last Friday’s high, Oracle has gained 23%.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His