-

Morning News: January 21, 2013

Posted by Eddy Elfenbein on January 21st, 2013 at 6:35 amEuro Ministers Set to Clash Over Terms of Channeling Aid

In Davos, Atmosphere for Bankers Improves

France Lifts Doubt Over Dutchman As New Eurogroup Head

Best Facebook Analyst Jobless Amid Kazakh Brokerage Cull

The China Miracle: A Rising Wealth Gap

An Overture From China Is Yet to Win Hollywood

JPMorgan Embraces Offshore Yuan as Trading Doubles

Dell Close To $22 Billion Leveraged Buyout Amid Decline In PC Market

$11.2 Billion Thai Bid Poised to Win Singapore Conglomerate

Huawei Pledges Openness To Woo Critics

What Went Wrong at Boeing: My Two Cents

Unusual Roots for Firm in Caterpillar Scandal

Finance Least-Trusted Industry for Third Year in Edelman Survey

Cullen Roche: Black Rock: The 2013 Macro View

Roger Nusbaum: The Big Picture for the Week of January 20, 2013

Be sure to follow me on Twitter.

-

RIP: Stan “The Man” Musial

Posted by Eddy Elfenbein on January 20th, 2013 at 1:27 pmMusial had 3,630 career hits; 1,815 came at home and 1,815 came on the road.

-

Cramer Was Right

Posted by Eddy Elfenbein on January 18th, 2013 at 1:48 pmThe Federal Reserve released the full transcripts of their meetings from 2007 today. While the minutes are released a few weeks after each meeting, the public can’t see the whole transcript for until five years have passed. That’s why we’re getting 2007 today.

In August of 2007, Jim Cramer made news with his famous “they know nothing rant” on CNBC. While he was broadly mocked for his outburst, Zachary Shrier makes a good point — Cramer was right. The Fed was clueless. The one from August 7th is particularly damaging,

I have talked to the heads of almost every one of these firms in the last 72 hours and he has NO IDEA what it’s like out there. NONE! And Bill Poole, he has NO IDEA what it’s like out there. My people have been in this game for 25 years and they’re LOSING THEIR JOBS and these firms are gonna GO OUT OF BUSINESS and it’s nuts. They’re NUTS! They know NOTHING! This is a different kinda market. And the Fed is ASLEEP. Bill Poole is a shame, he’s SHAMEUL! He oughta GO, and READ the Accredited Home document, at least I READ the darn thing.

Here’s Dennis Lockhart speaking during the meeting of August 7, 2007:

In the past few days, I have had substantive conversations with some well-positioned credit market observers, including managers of large investment portfolios, suggesting that the skittishness of financial markets is not likely to abate until later this fall. They have suggested that the choppiness in financial markets will be the rule in the near term and, very important, that the threshold for what constitutes a shock is now much lower than usual. I believe that the correct policy posture is to let the markets work through the changes in risk appetite and pricing that are under way, but the market observations of one of my more strident conversational counterparts—and that is not Jim Cramer [laughter]—are worth sharing. This party sees problems in the subprime structured debt market spreading to the CLO leveraged-loan market and, in a knock-on effect, to repo and commercial paper markets as well as to investment-grade corporate credit. This party points to nonprice rationing, commercial paper rollover risk, and general CDO contagion caused by the damaged credibility of rating agencies and contraction of collateral values. This party argues that treating the widening of credit spreads as normalization ignores substantial subsurface potential dislocations as evidenced by the collapse of American Home Mortgage Corporation. All that said, another counterpart noted a large pool of money now on the sidelines that is ready to provide financing for reasonable deals if prices fall low enough. Importantly, a large portion of this money comes from reliable long-term sources of investment, pension funds and insurance companies. Notwithstanding some descriptive rhetoric, this is not the credit crunch of the late 1980s, when the traditional financial intermediaries were strained for capital. The traditional investors are still out there with substantial liquidity, and they are just temporarily on the sidelines for understandable reasons and, barring further shocks, should return to the markets in force later this fall. The dislocations in the financial markets call for a posture of vigilant monitoring of developments but nothing more for now.

-

CWS Market Review – January 18, 2013

Posted by Eddy Elfenbein on January 18th, 2013 at 8:18 am“Good investing is boring.” – George Soros

Last week, I told you how fear was slowly melting away from this market. That trend continued into this week. Major stock indexes hit five-year highs. The small- and mid-cap indexes made all-time highs. Volatility dropped to a five-year low. So did initial unemployment claims. Poor home construction and industrial production; they only made four-and-a-half year highs.

Here’s what investors need to understand: The denouement of the Fed’s Quantitative Easing policy is the market’s embracing of riskier assets. That’s helped our Buy List tremendously, and it’s precisely why I wrote in the CWS Market Review from five weeks ago, “(t)he risk right now is finding yourself getting left behind.” Our Buy List is already up 5.1% on the year, and we’re barely halfway through January.

Of course, as patient investors, we know that the stock market can quickly take back what’s it’s given us, so that’s why we’re focused on the long-term. I urge all investors to pay close attention to our Buy Below prices. Too often, a bull market makes investors lazy. Mr. Soros is right: “good investing is boring.”

In this week’s CWS Market Review, I want to focus on the strong earnings report from JPMorgan Chase ($JPM). Last week, I told you to expect an earnings beat, and that’s exactly what happened. We also had record earnings from Wells Fargo ($WFC) last Friday. Next week, we have three earnings reports on tap: CA Technologies ($CA), Stryker ($SYK) and Microsoft ($MSFT). I’ll get to those in a bit. But first, let’s look at what’s happening at the legendary House of Morgan.

Buy JPMorgan Chase up to $50

I wish I could take massive amounts of credit for predicting JPMorgan’s ($JPM) earnings beat earlier this week, but honestly, it wasn’t hard to see. Anyone paying attention could see how their business was improving.

For the fourth quarter, JPM earned $1.39 per share, which was up from 90 cents per share in the fourth quarter of 2011. It was also well above Wall Street’s consensus of $1.20 per share. This was a strong quarter across the board. CEO Jamie Dimon said, “The firm’s results reflected strong underlying performance across virtually all our businesses for the fourth quarter and the full year, with strong lending and deposit growth,”

Breaking down the numbers, quarterly revenue jumped 10% to $21.5 billion. For the year, JPM made a profit of $21.3 billion from revenue of $97 billion. This bank is absolutely enormous. It’s more than 1,000 times larger than our beloved Nicholas Financial ($NICK). I’m showing you these numbers because much of the true story about JPMorgan gets lost in the headlines.

Let me explain. Earlier this year, the bank took a $6 billion bath thanks to bone-headed trading out of its London office from the infamous “London Whale.” Yes, that was a terrible, terrible episode, and heads should roll. The point I tried to make last year is that even a gigantic loss like that is still manageable for a titan like JPM.

But when the London Whale news broke, investors panicked and rushed for the exits. In just five weeks, the shares plunged from $44 to $31 (see the chart above). Bear in mind that this was only a few weeks after the company quintupled its dividend. Fortunately, we held on and JPM has been a big winner for us. As well as it’s done for us, I still think the stock is a bargain.

Digging deeper in the earnings report, I was particularly impressed by JPM’s strength in the mortgage sector. Fees from their mortgage business climbed from $723 billion in Q4 of 2011 to just over $2 billion in Q4 of 2012. Bernanke and Co. are clearly making a difference. JPM set aside a smaller amount for mortgage loan losses than Wall Street had expected. This line in the income statement always seems to drive some folks batty, but making provisions for loan losses is what banks do. They can either do too much or too little. They’re never going to be exactly right. I’m going to give a bank that didn’t report a single quarterly loss during the financial crisis the benefit of the doubt.

I also noticed that in JPM’s credit-card business, loans delinquent over 30 days fell from 2.81% a year ago to 2.1% now. That’s a very good sign. On the negative side, the bank took a big $700 million charge in Q4 for the mortgage-abuse settlement that was announced recently.

Here’s how I see JPMorgan. It’s a solid bank. The stock is cheap. Business is doing well, and profits are growing. The problem is that the bank has a poor reputation, and not all of that is unfair. Jamie Dimon is a talented leader, but he’s a loudmouth. He was a good leader during a crisis, but now I think Jamie should depart so JPM can work on rebuilding its image. He can still be on the board, but the bank needs a new public face. Preferably one that’s a little boring.

On Thursday, shares of JPM got as high as $46.87, which is the highest level since April 13, 2011. Due to this strong earnings report, I’m raising my Buy Below on JPM to $50. This is an excellent stock. One more thing: Expect to see a dividend increase in a few weeks.

Fiserv Raises Full-Year Earnings Guidance

There was some rather bizarre news surrounding Fiserv ($FISV) this week. The company announced that it was buying Open Solutions for $850 million. That’s not the odd part. The same day, Fiserv was downgraded by an analyst due to the Open Solutions deal, although an analyst at Oppenheimer upped his price target to $89.

In the very same press release announcing the Open Solutions deal, Fiserv guided higher for all of 2013. Specifically, the company sees 12% earnings growth for 2012, and another 15% to 18% growth for 2013. Since Fiserv earned $4.58 per share in 2011, their guidance translates to earnings of $5.13 per share for 2012, and $5.90 to $6.05 per share for 2013. The Street had been expecting $5.78 for 2013.

The 2012 forecast works out to $1.38 per share for Q4 (which is the only missing piece), and this is four cents below the Street. That, combined with the analyst downgrade, was enough to cause a 3% drop in Fiserv’s stock on Tuesday. Yet the company raised guidance! That’s just silly. Fiserv remains an excellent buy any time you see it below $88 per share.

Three Buy List Earnings Reports Next Week

Next week, three of our Buy List stocks are reporting earnings. The most important will be Microsoft ($MSFT), which Wall Street has turned against recently. MSFT’s last earnings report was a complete dud, and the stock took another hit in November, when the head of Windows abruptly left.

For the upcoming earnings report, Wall Street expects 75 cents per share, which would be a decrease of three cents from one year ago. Unlike the situation with JPM, I can’t so easily say that MSFT will beat earnings. The lower share value, however, has taken a lot of the risk out of owning the stock. Microsoft below $28 has the potential to be a big winner for us, but it’s not in the bag just yet. Let’s be conservative here and rate it a good buy up to $30 per share.

The other reports next week are from Stryker ($SYK) and CA Technologies ($CA). Interestingly, Stryker is our #1 performer for 2013, with a 10.6% gain. If you recall, the company recently raised the low end of its 2012 guidance by a penny per share, and reiterated its full-year forecast of $4.25 to $4.40 per share. I like this stock a lot. Stryker remains a good buy up to $62.

CA Technologies is our second-best performer for 2013, +10.2%. After a horrible slide late last year, CA has impressively recovered lost ground. Wall Street currently expects earnings of 57 cents per share. I think CA should be able to beat that. I’m raising my Buy Below on CA Technologies to $27.

In addition to raising JPM to $50 and CA to $27, I’m also bumping up Cognizant Technology (CTSH) to $81 and Medtronic ($MDT) to $48.

That’s all for now. Remember that the stock market will be closed on Monday in honor of Dr. Martin Luther King’s birthday. We’ll also have a few more earnings reports next week. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: January 18, 2013

Posted by Eddy Elfenbein on January 18th, 2013 at 7:07 amCameron Speech Excerpts Raise Specter of EU Exit

China Exits Slowdown as Quarterly Growth Tops Forecasts

China Wealth Gap Data Stoke Skepticism

Bank of Japan Eyes Open-Ended Asset Buying, Agrees New Inflation Goal

Australia Posts Worst Back-to-Back Job Growth Since ’97

Desert Massacre Threatens Africa’s Largest Gas Industry

S&P 500 Advances to Five-Year High on Economic Reports

Mortgage Crisis Lingers On at Citigroup and Bank of America

Intel’s Weak Outlook, Spending Hikes Unnerve Wall Street

Boeing 787 Plane of Future Struggles to Overcome Past

How the Qualified Mortgage Rules Could Hit the Jumbo Market

Sony Sells New York HQ For Highest-Priced US Bldg In Two Years

Winfrey’s Channel Is Set to Break Through

Phil Pearlman: If DeMark Is Right About Apple, Its Insanely Bullish for the Large Cap Indices

Be sure to follow me on Twitter.

-

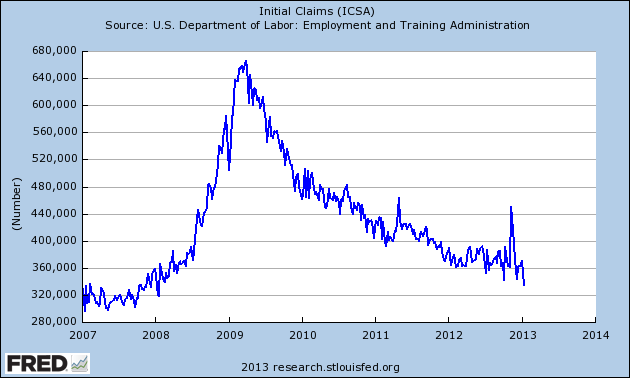

Initial Jobless Claims Drop to 5-Year Low

Posted by Eddy Elfenbein on January 17th, 2013 at 1:52 pmInitial claims for state unemployment benefits fell 37,000 to a seasonally adjusted 335,000, the lowest level since January 2008, the Labor Department said on Thursday. It was the largest weekly drop since February 2010 and ended four straight weeks of increases.

While problems adjusting the data for seasonal fluctuations might have exaggerated the size of the decline, economists said the report still suggested an improvement in sluggish labor market conditions and the broader economy as a whole.

“Having taken a pinch of salt, however, we would suggest that the trend in claims generally show no pickup in layoff activity around the turn of the year,” said John Ryding, chief economist at RDQ Economics in New York.

Another report from the Commerce Department showed that new home construction rose by 12.1% in December to reach the highest level since 2008.

-

Morning News: January 17, 2013

Posted by Eddy Elfenbein on January 17th, 2013 at 6:42 amGermany Goes for Gold—To Bring Home

Euro Area Seen Stalling as Draghi’s Pessimism Shared

Merkel’s Offshore Wind-Power Dream for Germany Stalls

Next Made-in-China Boom: College Graduates

Boeing 787 Incidents Prompt First U.S. Grounding in 34 Years

JPMorgan’s Board Uses a Pay Cut as a Message

H.P. Said to Have Suitors for Two Units

Rio Tinto to Book $14 Billion Charge; C.E.O. Steps Down

Taiwan Semiconductor Q4 Net Profit Jumps 32% Amid Mobile Device Boom

Finland Steps In to Help Nokia Resolve India Tax Dispute

EBay Sales Beat Estimates as Donahoe Pushes Mobile Sales

Unitedhealth Says Fourth Quarter Earnings Rose

Of All The Brand New Mortgage Rules, This One Is Our Favorite

Jeff Carter: Manti Te’o Teaches a Lesson About Due Diligence

Credit Writedowns: Where to Look For Signs of Recession

Be sure to follow me on Twitter.

-

“Founding Father of the Quants Was Revolutionary Marxist”

Posted by Eddy Elfenbein on January 16th, 2013 at 5:51 pmCrazy! Here’s a snippet:

Jacob Marschak may not be a household name today, but he inspired a number of financial practitioners and thinkers, from Milton Friedman to Harry Markowitz, and his insights are now the backbone of trading strategies and computer algorithms worldwide.

Marschak was born to a Jewish family in Kiev, Ukraine, in 1898. He played a part in the Russian Revolution as a teenager, working as a Menshevik activist. The liberation of Ukraine from the czar’s Russian Empire vaunted Marschak into the position of labor minister of the short-lived independent state of Terek.

Within months, the state was absorbed by another region and then subsumed into the Soviet Union. A disillusioned Marschak fled to Germany, where he received training in the Austrian School of free-market economics. He hoped to make a permanent home in Germany, but when the Nazis came to power, the Jewish- radical-turned-Marxist-turned-Austrian-School-economist wisely left the country, moving first to England and then to the U.S., where he joined the New School in New York as part of an anti- fascist University in Exile.

-

Remember Volatility?

Posted by Eddy Elfenbein on January 16th, 2013 at 4:11 pmCheck out the last five closes for the S&P 500:

January 10: 1,472.12

January 11: 1,472.05

January 14: 1,470.68

January 15: 1,472.34

January 16: 1,472.63That’s an average daily swing over the last four days of just 0.085%. That’s the lowest in more than seven years.

-

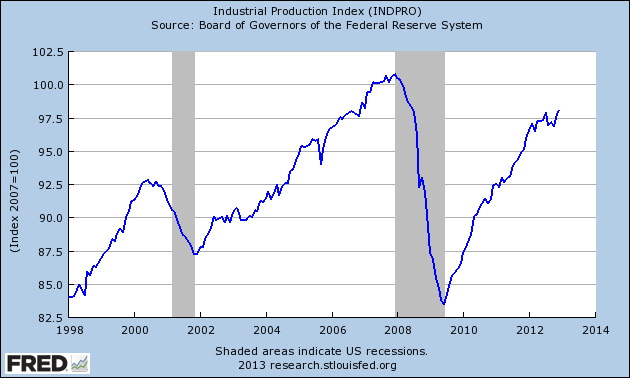

Industrial Production Reaches 4-1/2 Year High

Posted by Eddy Elfenbein on January 16th, 2013 at 1:57 pmWe had some important economic reports today. Let’s run down a few highlights:

The government said that consumer inflation was unchanged in December. The “core rate,” which excludes volatile food and energy prices, rose by 0.1%. This exactly matched consensus. For all of 2012, inflation rose by 1.7% while the core rate was up by 1.9%.

The Federal Reserve said that industrial production rose by 0.3% in December. That follows a 1% rise in November which was largely a post-Sandy rebound. Industrial production is now at its highest level since June 2008, and we’re not too far from the all-time high reached in December 2007. Capacity utilization is up to 78.8%.

Yesterday, the Census Bureau reported that retail sales rose 0.5% in December on a seasonally-adjusted basis. Sales were up 4.7% from a year ago. Bill McBride of Calculated Risk notes that retail sales are up 25.4% from the bottom of the recession, and are up 9.7% since the pre-recession peak.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His