Archive for 2013

-

CWS Market Review – November 1, 2013

Eddy Elfenbein, November 1st, 2013 at 7:07 am“Time is on your side when you own shares of superior companies.” – Peter Lynch

After rising on 13 out of 15 days, the stock market has taken a small breather the last two days. This has been quite an impressive run for the market, so a little relief is understandable. This year is shaping up to be the best for the S&P 500 in a decade. The index has been positive for the entire year, with an amazing 33 record highs so far.

We’re heading into the back end of earnings season. So far, the results for Q3 have been decent. Companies are topping estimates, but those estimates have been steadily pared back for the last 18 months.

The latest numbers show that 364 of the 500 members of the S&P 500 have reported earnings so far. Of those, 75% have beaten earnings estimates, while 53% have beaten sales estimates. When the final numbers are in, analysts see the index posting 3.7% earnings growth for Q3. Remember that overall earnings fell in Q1 and Q2 of this year, so this is a nice turnaround. In fact, analysts forecast that earnings growth will continue to accelerate. For Q4 (which is now one-third over) analysts see earnings growth rising to 7.5% and climbing another 8.3% for Q1 of 2014.

In this week’s CWS Market Review, I want to cover some of the great Buy List earnings reports from this week. Fiserv beat earnings and raised guidance. Harris jumped nearly 6% on a nice earnings beat. WEX Inc. also beat and raised guidance. The stock spiked nearly 7% in two days.

Not all the earnings news was good. Frankly, the earnings reports from Nicholas Financial and AFLAC were a bit disappointing, but nothing too severe. The best news was that AFLAC raised its dividend for the 31st year in a row. Not many stocks can say that.

I’ll also take a look at our remaining earnings reports. In particular, I’m expecting good news from Cognizant Technology. But first, let’s look at the great earnings report from Harris.

Harris Is a Buy up to $65 per Share

In last week’s CWS Market Review, I said “it’s very likely” Harris ($HRS) would beat earnings. I was right. On Tuesday, the communications-equipment company reported earnings for their fiscal Q1 of $1.18 per share, which was five cents better than Wall Street’s consensus. The shares jumped nearly 6% on Tuesday to reach a new five-year high. The rally in this little stock has been amazing. Harris is now up over 50% in a little over six months.

I was pleased to see Harris reaffirm its full-year guidance of $4.65 to $4.85 per share. This is for the fiscal year that ends in June. The Street had been expecting $4.74 per share. The details of this report were very impressive. I’m raising my Buy Below on Harris to $65 per share.

Fiserv Beat Earnings and Raised Guidance

After the closing bell on Tuesday, Fiserv ($FISV) reported Q3 earnings of $1.56 per share, which was also five cents better than the Street’s view. Earnings were up 24% for the quarter and 18% for the first three quarters. Fiserv’s CEO said, “We remain on track to achieve our 2013 financial objectives and have meaningful momentum as we head into 2014.”

That’s certainly true. Fiserv now sees 2013 earnings ranging between $5.94 and $6.02 per share. That’s an increase of 10 cents per share on the low end. It also implies a growth rate of 17% to 19%, which is very good for this environment. Fiserv remains an excellent buy up to $108 per share.

WEX Is a Buy up to $99 per Share

On Wednesday, WEX Inc. ($WEX) reported earnings of $1.29 per share, which was a full ten cents per share above expectations. Business is obviously going better than the company anticipated. Three months ago, WEX said that earnings for Q3 would be between $1.16 and $1.23 per share.

WEX put up some impressive numbers. Quarterly revenue jumped 19% to $191.5 million. The CEO said, “For the quarter, revenue increased 19% year over year and was towards the high end of our guidance, while adjusted net income, increasing 20%, exceeded our expectations.”

WEX also raised its full-year guidance range to $4.37 – $4.44 per share. The earlier range was $4.27 – $4.37 per share. That’s a nice increase. For Q4, WEX sees earnings coming in between $1.04 and $1.12 per share. Wall Street had been expecting $1.11 per share.

Thanks to the earnings report, the stock rallied 4.3% on Wednesday and another 2.3% on Thursday. The shares crossed $94 and hit a new all-time high. I’m raising my Buy Below on WEX to $99 per share.

Disappointing Earnings from AFLAC and NICK

Not all the earnings news was positive this week. On Tuesday, AFLAC ($AFL) reported Q3 earnings of $1.47 per share, which was a penny below expectations. I want to emphasize that this was only slightly disappointing, and my overall view on AFLAC hasn’t changed at all. The company is still matching its own numbers. In July, they gave us a range for Q3 of $1.41 to $1.51 per share.

The enemy of AFLAC’s bottom line is quite obvious. The yen/dollar exchange rate gobbled up 21 cents per share last quarter. I tend to look past currency exchange because it’s a transient issue. Sometimes it helps you; sometimes it doesn’t. Over the last few months, it’s hurt AFLAC. We shouldn’t complain too much since the weaker yen probably helps the Japanese economy, which is where AFLAC does most of its business.

AFLAC’s based its forward guidance on a yen/dollar rate of 95 to 100. For Q4, they see earnings ranging between $1.38 and $1.43 per share. That works out to full-year earnings of $6.16 to $6.21 per share. The previous range was $5.83 to $6.37 per share.

For 2014, AFLAC sees earnings coming in between $6.28 and $6.52 per share. AFLAC has said that its goal for this year is to grow its currency-neutral operating earnings by 4% to 7%. Next year, due to a number of business headwinds, that growth rate will drop to 2% to 5%. The company said that those headwinds should pass by the end of next year.

I have to stress that this is all in earnings per share because AFLAC plans to buy back a whole lot of shares. The company plans to buy $800 million worth of shares this year and another $800 million to $1 billion next year.

AFLAC also raised its dividend by 5.7%. The quarterly payout rises from 35 to 37 cents per share. This is the 31st year in a row that AFLAC has raised its dividend. The stock dropped 3% after the earnings report, but I’m not at all worried. This is a fine company that’s navigating a difficult environment. As Peter Lynch said, “Time is on your side when you own shares of superior companies.” AFLAC remains a very good buy up to $70 per share.

The other disappointing report came from Nicholas Financial ($NICK), which reported quarterly earnings of 35 cents per share. I had been expecting earnings closer to 45 cents per share.

I still need to dig into the numbers, but it appears that NICK had a large increase in operating costs. There was also a 22% increase in their provision for credit losses. I’m not sure what drove these increases, but they account for the entire earnings shortfall. NICK tends to be pretty conservative with its business, so these results were rather unexpected.

Again, I’m still a fan of the company. I’m just a little curious as to what exactly happened last quarter. On Thursday, the stock dropped 5%, which places it back where it was a few weeks ago. I hope to see a dividend increase from the board before the end of the year. NICK continues to be a good buy up to $18 per share.

Earnings Next Week from DirecTV and Cognizant Technology

Next Tuesday we get our final two earnings reports for this season as DirecTV ($DTV) and Cognizant Technology ($CTSH) report. DTV is a hard stock to predict. For Q1, the company had a massive earnings beat. Then for Q2 they missed badly. The difficulty is that a major growth area for DTV is Latin America, but the economy has been rough in that region lately. Wall Street currently expects Q3 earnings of $1.02 per share. DirecTV is a buy up to $64 per share.

In the CWS Market Review from August 30, I said that Cognizant “may be the best bargain right now on our Buy List.” The stock’s up more than 17% since then, and I think it’s still a good value. Three months ago, they beat earnings and guided higher. For Q3, CTSH said to expect earnings of $1.09 per share. I think they can beat that. Cognizant is a very good buy up to $90 per share.

Two items before I go. Ross Stores ($ROST) has been very strong lately. The retailer reports in three weeks, but I want to raise my Buy Below to $81 before it gets away from us. This is a very good stock.

Also, Moog ($MOG-A), our #1 performer this year, is due to report on Friday. The earnings report may be out by the time you’re reading this. Wall Street expects earnings of 96 cents per share. Moog is a solid buy up to $61 per share.

That’s all for now. We have still more earnings reports to come next week. Cognizant and DirecTV both report on Tuesday. We’re also going to get some important economic reports. On Thursday, we’ll get our first look at third-quarter GDP growth. Then on Friday, the Labor Department will release the October jobs report. If we see any pickup in hiring, that could lead to the Fed finally getting its tapering act together. I’m beginning to think we won’t see any taper until next year. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: November 1, 2013

Eddy Elfenbein, November 1st, 2013 at 6:23 amDraghi’s Deflation Risk Complicates Recovery

Economists React: China Manufacturing Up in October

R.B.S. to Split Off Troubled Loans of About $61 Billion Into “Bad Bank”

South Korean Exports Hit Record High on Smartphone and Car Demand

The Fed Left One Big Question Unanswered

Fannie Mae Sues Banks for $800 Million Over Libor-Rigging Claims

IRS Eases Rules on Healthcare Flexible Spending Accounts

Walmart Kicks Off Online Holiday Deals Early in Intense Season

Sony Shares Drop 11% on Poor Earnings

Angry Over U.S. Surveillance, Tech Giants Bolster Defenses

Three Reasons Buffett’s Not Buying

Here’s What Happened When Cisco Lost A $1 Billion Deal With Amazon

Oracle Shareholders Oppose Compensation for Ellison

Cullen Roche: Margin Debt: What Does It Really Tell Us?

Roger Nusbaum: Does It Make Sense to Implement the Taleb Portfolio?

Be sure to follow me on Twitter.

-

Chicago PMI Has Biggest Jump in 30 Years

Eddy Elfenbein, October 31st, 2013 at 1:28 pmI usually don’t write about the Chicago PMI, but today’s report had the largest jump in 30 years. The stat measures economic activity in the Chicago region.

Chicago PMI, a gauge of manufacturing in the Midwest, surged to 65.9 in October, from 55.7.

This is the highest level since March 2011, and the biggest monthly increase in over 30 years.

This crushed expectations for 55.

While the stock market is slightly positive, the bond market is selling off. The 10-year bond yield had been at a four-month low, but the yield has creeped up about 10 basis points since yesterday. It’s not a lot, but the PMI report is about the only data point showing strong economic activity.

-

Nicholas Financial Earns 35 Cents Per Share

Eddy Elfenbein, October 31st, 2013 at 9:46 amNicholas Financial ($NICK) reported earnings of 35 cents per share:

CLEARWATER, Fla., Oct. 31, 2013 (GLOBE NEWSWIRE) — Nicholas Financial, Inc. (NICK) announced that for the three months ended September 30, 2013 net earnings decreased 16% to $4,317,000 as compared to $5,150,000 for the three months ended September 30, 2012. Per share diluted net earnings decreased 17% to $0.35 as compared to $0.42 for the three months ended September 30, 2012. Revenue increased 1% to $20,949,000 for the three months ended September 30, 2012 as compared to $20,705,000 for the three months ended September 30, 2012.

For the six months ended September 30, 2013 net earnings decreased 5% to $10,017,000 as compared to $10,558,000 for the six months ended September 30, 2012. Per share diluted net earnings decreased 6% to $0.82 as compared to $0.87 for the six months ended September 30, 2012. Revenue increased 1% to $41,425,000 for the six months ended September 30, 2013 as compared to $41,133,000 for the six months ended September 30, 2012.

“Our results for the three months ended September 30, 2013 were adversely affected by a non-cash charge related to the change in fair value of interest rate swap agreements, an increase in operating expenses as a percentage of finance receivables, net, and an increase in the net charge-off rate,” stated Peter L. Vosotas, Chairman and CEO. “We continue to develop additional markets and expect to open between 1-3 new branch locations during the remainder of our current fiscal year, which ends March 31, 2014.”

This was much less than I expected. I saw them earnings 45 cents per share, give or take.

I’m surprised by the sharp rise in operating costs. One year ago, operating costs were 60.2 cents per share. Last quarter that rose to 65.6 cents per share. This is in the context of revenue-per-share being almost identical to one year ago.

The provision for credit losses rose from 26.8 cents last year to 32.3 cents this year. The difference between credit losses and operating costs knocks about 11 cents per share off NICK’s pre-tax income. The stock is currently down about 4%.

-

Morning News: October 31, 2013

Eddy Elfenbein, October 31st, 2013 at 7:06 amCentral Banks Give Each Other Access to Currency

Fracking Rules Set in Spain to Boost Shale Gas, Oil Work

BoJ Content to Ignore Fed Tapering and Go Its Own Way

Fed Extends Stimulus as Growth Stumbles

Citigroup, JPMorgan Said to Put Currency Dealers on Leave

Bitcoin Pursues the Mainstream

Mobile Ads Fuel a Jump in Profit at Facebook

Shell Profit Misses Analyst Estimates as Global Production Drops

Sony’s Hirai Cuts Forecasts as Tsuga Leads Panasonic Revamp

Alcatel-Lucent Reports Narrower Third-quarter Loss

Lufthansa, Air France – KLM Post Lower Profit in Q3

Robert Shiller: Young People With A Moral Purpose Should Work For Goldman Sachs, Not Google

Billionaire Eike Batista’s Dreams Crumble

Pragmatic Capitalism: Why the Fed Can’t Taper

Credit Writedowns: Has US Retail Sales Growth Peaked?

Be sure to follow me on Twitter.

-

Today’s Fed Statement

Eddy Elfenbein, October 30th, 2013 at 2:01 pmInformation received since the Federal Open Market Committee met in September generally suggests that economic activity has continued to expand at a moderate pace. Indicators of labor market conditions have shown some further improvement, but the unemployment rate remains elevated. Available data suggest that household spending and business fixed investment advanced, while the recovery in the housing sector slowed somewhat in recent months. Fiscal policy is restraining economic growth. Apart from fluctuations due to changes in energy prices, inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic growth will pick up from its recent pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. The Committee sees the downside risks to the outlook for the economy and the labor market as having diminished, on net, since last fall. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, but it anticipates that inflation will move back toward its objective over the medium term.

Taking into account the extent of federal fiscal retrenchment over the past year, the Committee sees the improvement in economic activity and labor market conditions since it began its asset purchase program as consistent with growing underlying strength in the broader economy. However, the Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases. Accordingly, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. In judging when to moderate the pace of asset purchases, the Committee will, at its coming meetings, assess whether incoming information continues to support the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective. Asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s economic outlook as well as its assessment of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Charles L. Evans; Jerome H. Powell; Eric S. Rosengren; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen. Voting against the action was Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.

-

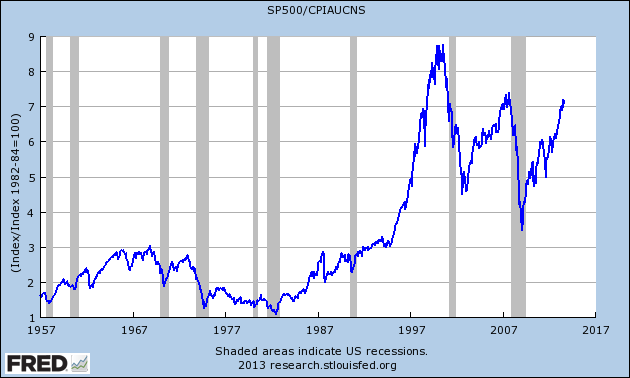

The S&P 500 Matches Inflation-Adjusted High

Eddy Elfenbein, October 30th, 2013 at 11:56 amGreat news! Adjusted for inflation, the S&P 500 has done nothing in the past six years! And it’s taken a lot for us to get there.

This morning, the government released the inflation report for September. I had to do a little massaging of the numbers, but if we assume the inflation trend that we had in September continues in October, then the S&P 500 just surpassed its inflation-adjusted peak from October 2007.

Note that this is just the S&P 500 and it doesn’t include dividends. All things being equal, you can expect the market’s dividend rate to follow the inflation rate fairly closely. While we’re above the 2007 peak, the S&P 500 is still about 18.5% below the inflation-adjusted peak from 2000.

We can never say for certain where the inflation-adjusted index is because there’s some lag time before the inflation report comes out. Here’s the latest FRED chart which goes from 1957 through September 2013. The next data point should reflect the six-year high.

It’s interesting to see that the 2009 low nearly matched the 1966 high.

-

WEX Inc. Earns $1.29 Per Share

Eddy Elfenbein, October 30th, 2013 at 10:57 amMore good earnings news today. This morning, WEX Inc. ($WEX) reported Q3 earnings of $1.29 per share. That’s 10 cents more than estimates. Three months ago, WEX said that earnings for Q3 would be between $1.16 and $1.23 per share.

Quarterly revenue jumped 19% to $191.5 million. These are very good numbers. The shares are currently up 5% this morning. WEX’s CEO had good things to say in today’s report.

“We continue to experience momentum throughout our business, driven by the solid execution of our long-term strategy. For the quarter, revenue increased 19% year-over-year and was towards the high-end of our guidance, while adjusted net income, increasing 20%, exceeded our expectations. Our results were driven by robust volume growth, Other Payments growth, foreign exchange rate contributions and expense management,” commented Michael E. Dubyak, WEX’s chairman and chief executive officer.

“We continue to see ongoing expansion in our domestic fleet business as we realize synergies from Fleet One and further bolster our competitive position. Furthermore, investments in our virtual card product are continuing to generate positive returns as we penetrate attractive geographies including Europe, Asia Pacific and South America. Looking towards the future, we expect to continue to leverage the foundations we are building and our dynamic pipeline to drive growth as we close out the year,” concluded Mr. Dubyak.

For Q4, WEX sees earnings coming in between $1.04 and $1.12 per share. Wall Street had been expecting $1.11 per share. WEX also raised their full-year guidance range to $4.37 to $4.44 per share. The earlier range was $4.27 to $4.37 per share.

-

Morning News: October 30, 2013

Eddy Elfenbein, October 30th, 2013 at 6:47 amChina Official PMI Seen Hitting 18-Month High in October

Spain Exits Two-year Recession as Rajoy Seeks Recovery

German Unemployment Rises a Third Month as Growth Slows

RBS Said to Review Currency-Trading Practices Amid Probe

World’s First Bitcoin ATM Launched in Canada

Chocolate Factory, Trade War Victim

Consumer Confidence in U.S. Slumps by Most Since August 2011

The President Wants You to Get Rich on Obamacare

Housing Prices in U.S. Cities Rise by Most Since Early 2006

Barclays Profit Rises to $1.2 Billion But Fixed Income Trading Slumps

Linkedin’s Conservative Forecast Gives Pause To Sizzling Stock Surge

Sears Weighs Spinoff of Lands’ End

Honda Q2 Net Up 42% on U.S. Sales Rise, Slightly Below Forecast

Joshua Brown: The Starbucks Global Takeover

Howard Lindzon: Being Wrong Works at Scale…Hedge Funds and Bank of America

Be sure to follow me on Twitter.

-

AFLAC Earns $1.47 Per Share, Raises Dividend 5.7%

Eddy Elfenbein, October 30th, 2013 at 12:04 amAfter the closing bell, AFLAC ($AFL) reported Q3 earnings of $1.47 per share which was one penny below Wall Street’s forecast. In July, the company gave us a range for Q3 of $1.41 to $1.51 per share, so at least AFLAC is hitting its own guidance. The problem continues to be the yen/dollar exchange rate which knocked 21 cents per share off AFLAC’s earnings last quarter.

If you ignore the exchange rate issue, AFLAC’s operations are doing just fine. The company also gave forward guidance which assumes a yen/dollar rate between 95 and 100. Here are the details: AFLAC narrowed its full-year 2013 guidance to $6.16 to $6.21 per share. The previous range was $5.83 to $6.37 per share. For Q4, AFLAC expects earnings between $1.38 and $1.43 per share. Wall Street had been expecting $1.42 per share. Excluding the exchange rate, AFLAC aims to grow operating earnings by 4% to 7% this year.

AFLAC also gave its first guidance for 2014, again assuming a 95 to 100 exchange rate. For next year, they see earnings coming in between $6.28 and $6.52 per share. They’re aiming to grow operating earnings by 2% to 5% next year.

I have to stress that this is all in earnings-per-share because AFLAC plans to buy back a whole lot of shares. The company plans to buy $800 million of shares this year, and another $800 million to $1 billion next year.

AFLAC also raised their dividend by 5.7%. The quarterly payout rises from 35 to 37 cents per share. This is the 31st year in a row that AFLAC has raised their dividend.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His