Archive for 2013

-

Worst Day Since November

Eddy Elfenbein, February 25th, 2013 at 7:06 pmUgh! Today was an ugly day for the stock market. The S&P 500 dropped 27.79 points or 1.83%. This was the worst drop since the day following President Obama’s reelection. At one point early today, the index was actually up 0.68%.

But shortly after 10 am, the stock market started heading downhill and really started to plunge after 3 pm. Interestingly, the S&P 500 has fallen on every single Monday this year.

The talking heads are saying that political confusion in Italy is to blame. The early election results showed that Pier Luigi Bersani’s left-of-center ticket was doing well very well in the lower house. However, as time went on, Silvio Berlusconi appeared to do well in the Senate. The fear is that Italy is in a political stalemate and new elections may have to be called soon.

The cyclicals felt the brunt of the damage. The Financial Sector lost 2.69%. Energy was down 2.51%, while the Materials stocks were off 2.24%. The big Wall Street banks dominated the bottom part of the S&P 100 today. Our own JPMorgan Chase ($JPM) only lost 2.51% which was much better than its peers. Wells Fargo ($WFC) lost 2.88%. Ford closed at $12.13 which gives the stock a yield of 3.3%.

Defensive sectors like Telecom, Utilities and Healthcare did the best, meaning they were down the least. The VIX soared 34% today. From last Tuesday’s low to today’s high, it jumped 60%.

Here’s a short equation: for the last six months, the stock of any company that consumers had to borrow money for (cars, homes, travel) did very well, as did the big banks and credit card companies. The bigger the price tag, the better it probably did. The key was the intersection of the average consumer and finance. Today was a complete reversal of that dynamic.

Every stock on the Buy List closed lower today, but we didn’t fall as much as the broader market which represents the conservatism of our portfolio. All told, our Buy List lost 1.61% which was 22 basis points better than the S&P 500.

-

Best Industries Last Six Months

Eddy Elfenbein, February 25th, 2013 at 1:49 pmI thought this was interesting. Here’s a look at the best industries over the last six months. If there’s one theme that connects them all, it’s the promise of lower interest rates.

Industry Name Percent Change Dow Jones U.S. Mortgage Finance Index 44.57% Dow Jones U.S. Business Training & Employment Agencies Index 36.48% Dow Jones U.S. Investment Services Index 35.83% Dow Jones U.S. Airlines Index 34.42% Dow Jones U.S. Real Estate Services Index 34.25% Dow Jones U.S. Furnishings Index 31.25% Dow Jones U.S. Auto Manufacturers Index 27.19% Dow Jones U.S. Durable Household Products Index 27.03% Dow Jones U.S. Marine Transportation Index 25.58% Dow Jones U.S. Asset Managers Index 25.30% Silvio Killed the Rally!

Eddy Elfenbein, February 25th, 2013 at 11:48 amSilvio killed the rally! Allow me to explain. The rally we had this morning was based on news from the elections in Italy. Now it turns out that Silvio Berlusconi’s party may have carried the Italian Senate. The returns are still coming but investors are clearly uncomfortable with that news.

Check out the massive swing in the Italian ETF ($EWI):

The market also seemed to be pleased that Japan’s Prime Minister was going to appoint a central bank head who’s all in favor of gunning the money.

The big concern, however, is the sequester. If nothing happens by March 1st, automatic spending cuts will go into effect.

I also want to highlight an interest stock story today. Shares of Affymax ($AFFY) are down 85% after its antianemia drug was recalled. That’s gotta hurt.

The Low-Volatility Low-Quality Rally

Eddy Elfenbein, February 25th, 2013 at 9:52 amWhat’s starting to concern me, though I don’t think it’s a problem yet, is the low-quality nature of this rally. Simply put: A lot of lousy stocks are doing well. This is what we typically see in the late stages of a bull market when stocks whose business operations consist of little more than a stock puppet surge higher each day.

The unusual aspect of the current market is that it’s been low quality and low volatility which seem to be contradictory. In this case, I think the low volatility is the result of the market’s satisfaction that the current environment of low interest rates will last for some time.

It’s hard to see low quality but here’s a chart showing the performance of the High Beta ETF ($SPHB) alongside the S&P 500. Over the last seven months, the High Betas have been ruling.

Obviously, a high-beta rally shouldn’t be a surprise. This is what high beta is all about — they do well when the market does well. This also represents a slant towards small-cap stocks and cyclical stocks. Let me stress that I don’t think this is the omen of a market top. At least, not yet. The time to worry is when the spread between the two ends of the market become a vast chasm. In 1999 and 2000, value stocks weren’t merely trailing the bull market. Those stocks were falling.

Markets Rise In Early Trading

Eddy Elfenbein, February 25th, 2013 at 9:35 amThe stock market looks to open higher today. This will be an interesting week for Wall Street. Ben Bernanke will give us semi-annual Congressional testimony this week. It’s a two-day affair: tomorrow in front of a Senate committee, and again on Wednesday in front of a House committee. The members of Congress do themselves no favor by asking inane questions.

I’m also curious to see the revision to Q4 GDP. The initial number came in at -0.1%. Thanks to positive trade data, the revision will most likely be positive. GDP could be as high as +1.0%.

In Italy, the markets seem relieved that Pier Luigi Bersani, a former Communist, seems poised to win the parliamentary elections.

Morning News: February 25, 2013

Eddy Elfenbein, February 25th, 2013 at 7:00 amNew Bank of Japan Head Branded ‘Out of Mainstream’

China Flash PMI Retreat Shows Not To Get Too Bullish, Too Quickly

Markets Shrug Off UK Downgrade Ahead of Italian Election Results

Bernanke’s Stimulus Spurring U.S. Employment in Housing-Autos

MasterCard Takes Aim at Plastic With Mobile Platform

Yum’s KFC to Tighten Supplier Reviews After China Sales D

Why Marissa Mayer Told Remote Employees To Work In An Office … Or Quit

Major Banks Aid in Payday Loans Banned by States

GM Bringing 4G Broadband to New Vehicles Next Year With AT&T

Royalty Pharma Offers to Acquire Elan for $6.5 Billion

Sinopec to Buy Stake in Chesapeake Assets for $1.02 Billion

Lowe’s Quarterly Results Top Analysts’ Estimates

Twitter Hackings Put Focus on Security for Brands

Howard Lindzon: I Don’t Know…and Long-Term I Still Don’t Know

CWS Market Review – February 22, 2013

Eddy Elfenbein, February 22nd, 2013 at 6:47 am“Lost in a gloom of uninspired research.” – William Wordsworth

As soon as I started joking about the stock market’s slumber party, we should have known something was up. In last week’s CWS Market Review, I said that trading had become dead boring; intra-day volatility had fallen to a 26-year low. Sure enough, the bears woke up from their hibernation this week and feasted on freshly grilled bull.

On Wednesday, the S&P 500 dropped 19 points—its biggest drop this year. The selling continued on Thursday, when the index lost another 9.53 points and briefly dropped below the crucial 1,500 barrier. In just two days, the S&P 500 shed more than $250 billion.

No, the Fed’s Bond Buying Isn’t about to End

So what went wrong? As is often the case, we can turn our eyes towards the Federal Reserve. On Wednesday, the central bank released the minutes from their late-January meeting. You think the jargon-packed minutes of a meeting of economists can’t evoke excitement? Well, welcome to Planet Wall Street, my friend.

What happened is that several members of the policy committee said the Fed should alter the size of its bond purchases in response to the economy. In other words, some of Bernanke’s posse are talking about pulling back on all the bond buying they’ve been doing.

It’s not exactly a state secret that Wall Street loves Quantitative Easing. In the Street’s eyes, the more the better, and that’s certainly been a major factor in causing the S&P 500 to double in less than four years. So once there was any hint that it might come to an end, the bears rushed in to take charge.

Here’s what we know. Fact one: The Fed is buying tons of bonds to prop the economy. Fact two: To borrow from LTC Kilgore, someday this policy is going to end. What we don’t know is when. All the Fed has said is that there should be “substantial” improvement in the labor market. While there’s been some improvement in the labor market, in my opinion, we’re still a long, long, loooong way from calling it substantial. As far as 0% interest rates go, the Fed has said that it’s pledged to that as long as unemployment is above 6.5% and inflation is below 2.5%. That’s at least a year away. Probably more.

What the minutes told us is that there are some voices within the Fed talking about a QE Exit Strategy. This really shouldn’t be a surprise. Instead of a sudden halt, they’re considering scaling back some of the purchases. Let me make something clear, something which has been overlooked: There was nothing in the Fed minutes about ending QE.

Here’s my take. The Fed minutes weren’t a reason to sell. Instead, they were a reason for people who had already been looking for a reason to sell to sell. Given that the S&P 500 has climbed for seven weeks in a row, I certainly understand that there are folks looking to clear out some positions.

Here’s the odd part: The Fed minutes were basically a dumb reason to make some smart moves. There’s no reason to fear that the Fed is going to pull the rug out from under the economy. But there is a good reason for investors to expect a modest pullback, which I’ve talked about for a few weeks. Earnings expectations are probably too high. I’ve also been disturbed by the fact that the low-quality stocks are leading the rally. This isn’t so troubling for us, since we concentrate on high-quality names, but our Buy List has lagged the broader market this month. That tends to happen when the market gets ahead of itself.

There’s really nothing in the Fed’s minutes that anyone should find surprising, at least anyone who’s been paying attention. As far as inflation goes, that’s not a worry at all. This week’s CPI report was very tame. In fact, there’s some emerging evidence that spiraling healthcare costs might finally be coming under control. Of course, the irony of the Fed minutes is that they’re talking about reining in QE because the economy is doing well (or at least better).

The key to watch is employment. That’s part of the Fed’s dual mandate, and the part that Congress is most interested in. The unemployment rate is currently at 7.9%, and that’s not counting the folks who have stopped looking for work. I’d say that the jobless rate would have to fall to 7% before they entertained the idea of cutting back on Quantitative Easing. Not ending it, mind you, but just trimming its sails. For now, the Fed is on the side of higher stock prices.

What Would Reduced QE Mean for Investors?

Let’s look ahead and talk about what will happen when the Fed finally takes away the punchbowl. The biggest impact would be in the gold market, and we got a preview of that this week. A drop in gold makes sense because we’re talking about higher real interest rates. The higher interest rates go above inflation, the worse it is for gold.

Interest rates have been close to or below inflation for years, and that’s been great for gold. However, the yellow metal hasn’t made a new high in nearly 18 months. Gold is down more than $200 an ounce since October, and it recently fell for five days in a row, including a $40 plunge on Wednesday. Like I said, it’s going to be a while before the Fed starts raising interest rates, but once it does, it won’t be pretty for gold.

Reduced QE would also be a big negative for cyclical stocks. The Morgan Stanley Cyclical Index (CYC) did much worse than the rest of the market on Wednesday. The CYC has now trailed the market for four days in a row. The Homebuilder ETF (XHB), a classic cyclical sector, dropped more than 4.4% on Wednesday. On our Buy List, cyclicals like Ford (F) got smacked around. Shares of Ford are now down to $12.39, which, I should add, is an excellent deal. Ford currently yields 3.2%, which is roughly 3.2% more than Bernanke.

Another victim of the Fed’s minutes was obviously low volatility. On Tuesday, the Volatility Index (VIX) reached a six-year intra-day low. From Tuesday’s close to Thursday’s close, the VIX jumped more than 23%. Not bad for two days’ work. Of course, this is an increase from very, very low to very low. Interestingly, the folks in the futures pits aren’t convinced that volatility is on its way back. I think they’re right. QE will be around for a while, and so will low volatility.

Medtronic Is a Buy up to $48 per Share

We only had one Buy List earnings report this week, and that came from Medtronic (MDT). I’ve been impressed by how well the medical-device maker has been doing for us lately. At one point, MDT was up more than 15% on the year. In January, we got good news from Medtronic when the company raised the low end of their full-year guidance by four cents per share. They now see earnings coming in between $3.66 and $3.70 per share. (Note that MDT’s fiscal year ends in April.)

On Tuesday, Medtronic reported that they earned 93 cents per share for their third quarter, which was two cents more than Wall Street’s consensus. That’s a nice increase from the 84 cents per share they earned one year ago. Sales rose by 2.8% to $4.03 billion, which was a teeny bit below consensus.

Despite the good earnings news, the shares lost ground on Tuesday and Wednesday. The two-day loss came to 5%, which I found rather surprising. Apparently, the market didn’t like Medtronic’s weak sales in Europe. The company generates about one-fourth of their total sales from the Old World. Medtronic also experienced a sales decline in their spinal-products business (ick!) and their defibrillators and pacemakers unit.

There was also good news as Medtronic said that the 2.3% excise tax that’s part of President Obama’s healthcare reform will cost the company $25 million this year, which is half the original projection. I’ll be curious to hear what guidance Medtronic gives for next year. The Street expects $3.86 per share, which I suspect is too conservative. Medtronic remains a very good buy below $48. The company has increased its dividend every year since 1977.

Nicholas Financial’s Quarterly Dividend

I want to add a quick note on Nicholas Financial (NICK)´s dividend. Perhaps I misunderstood, but I thought NICK’s big $2 dividend late last year was in lieu of all cash dividends for this year. Apparently, that’s not the case. The company just announced another 12-cent quarter dividend. The dividend will be paid on March 29th to shareholders of record as of March 22nd. Going by Thursday’s close, NICK yields 3.62%.

Before I go, I want to highlight a few stocks on our Buy List that are currently exceptionally good values. Microsoft (MSFT) had a good Q4 report, and the yield is up to 3.35%. As I mentioned before, shares of Ford (F) have slid back to $12.39. That’s a good price. Remember, Ford doubled their dividend a few weeks ago. Plus, the company just announced that it’s expanding its engine output in the United States. I discussed Bed Bath & Beyond (BBBY) in last week’s issue. BBBY has fallen into the bargain bin; below $58 is a very good price. Last month, I told you not to worry about Moog’s (MOG-A) lower guidance. The stock came within a penny of making a new 52-week high this week. Moog looks very good here.

That’s all for now. Next week, the government will revise its Q4 GDP report. It’s very likely that the trade data will cause them to revise the original -0.1% to a positive number. It could be as high as 1%. Then on Friday, we’ll get the ISM report for February. The report for January was surprisingly good. Let’s hope the trend continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Morning News: February 22, 2013

Eddy Elfenbein, February 22nd, 2013 at 6:03 amEuropean Countries Will Miss Deficit-Reduction Targets in 2013

EU Says Euro Zone to Shrink in 2013 as Unemployment Rises

BOE Plans to Sign Yuan Currency Swap Deal With China

Fattened Margins Seen Shrinking 40% at Banks

SEC Boosts Tally of Enforcement Successes With Routine Actions

U.S. Food-Inflation to Ease on Bigger Grain Crops, USDA Says

Federal Spending Cuts Threaten Delays in Air Travel

Wal-Mart, Despite Profit Gain, Says Rise in Payroll Tax Hindered Shoppers

AgBank to Add Traders as Dim Sum Sales Seen Rising

Air France-KLM Net Loss Widens

Apple Preferred Stock Plan Would Help Value, Einhorn Says

Sign of a Comeback: U.S. Carmakers Are Hiring

Nielsen Adjusts Its Ratings to Add Web-Linked TVs

Credit Writedowns: A Brief History of the Chinese Growth Model

Cullen Roche: Did Keynes Understand Endogenous Money?

Be sure to follow me on Twitter.

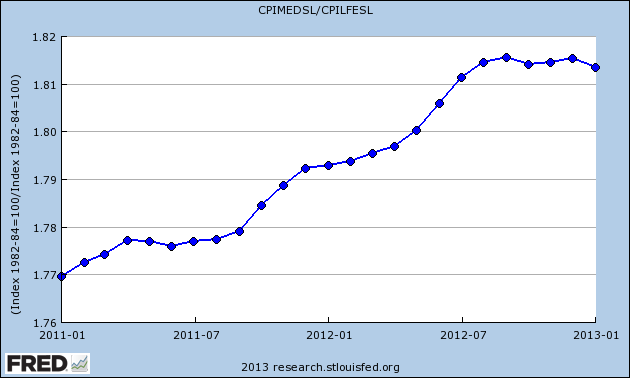

More Good News on Healthcare Costs

Eddy Elfenbein, February 21st, 2013 at 11:15 amToday’s CPI report showed that prices were unchanged last month. Economists were expecting an increase of 0.1%. The core rate, which excludes food and energy prices, was up 0.3%.

We also got the latest data point on the trend I discussed earlier this week. Medical prices are largely matching core inflation. Actually, this is far too short to call a trend, but it is a hopeful sign.

The Fed’s Minutes Scare the Market

Eddy Elfenbein, February 21st, 2013 at 11:05 amThe broadly expected sell-off may finally be happening. The S&P 500 fell 19 points yesterday and it’s down another 7.5 points today. The index may even drop below 1,500 very soon.

What had investors in a bad mood is possibly signals from the recent Fed minutes that the central bank is considering pulling back on its Quantitative Easing policy. Personally, I think folks are using this rather tame bit of news as an excuse to exit some positions. The markets have risen quite rapidly so I understand the temptation.

The odd part is that what the Fed really said is that the economy is improving and because of that, it may downshift on the amount of their bond purchases. So the market is down on somewhat optimistic economic news.

Perhaps the Gold market had suspected this news was going to happen because the price of the precious metal had been pulling back. If the Fed takes its foot off the pedal, that means real interest rates would rise and gold would take a tumble. Gold fell for five days in a row and it plunged $40 per ounce on Wednesday.

At its high in September 2011, gold got to $1,923 per ounce. Today, it’s down to $1,579 per ounce. Gold is also close to a death cross which is when the 50-day moving average falls below the 200-day moving average.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His