Archive for 2013

-

Fiserv’s Guidance for 2013

Eddy Elfenbein, February 6th, 2013 at 10:23 amSeeking Alpha has posted the transcript of yesterday’s earnings call for Fiserv ($FISV). Here’s a key part on the company’s outlook for this year.

We expect 2013 adjusted revenue to increase by more than 10%, and that adjusted internal revenue growth will be in a range of 3% to 4%. These numbers include approximately $50 million in lost revenue, more than 100 basis points of internal growth this year due to the unusual migration of an account processing client that transitioned to its parent’s account processing platform and the impact of the 10-year Bank of America renewal.

We expect 2013 adjusted earnings per share growth of 15% to 18% or a range of $5.88 to $6.07 over 2012. We estimate free cash flow per share will be more than $6.60 per share, an increase of at least 18% over 2012. We expect adjusted operating margin to expand in a range of 10 to 50 basis points. This estimate includes the approximately 60-basis-point negative impact from the revenue headwind and also margin dilution associated with the Open acquisition.

For modeling purposes, we anticipate that our revenue and earnings growth will be sequentially stronger each quarter as we move through the year. A number of our larger recurring revenue client conversions are planned for the second and third quarters of 2013, and the impact of the negative headwinds are also more pronounced in the first half of the year. We also expect the Open Solutions results to increase during the year, consistent with their normal business model, the cumulative effect of integration benefits and the pay-off of the higher cost debt.

We’re in the process of realigning the specific annual targets for our operational effectiveness and integrated sales targets to consider the Open Solutions acquisition. Accordingly, we are now prepared to communicate annual targets for 2013. However, you can be sure we are very focused on these initiatives and we’ll provide you with an update at the end of the quarter — sorry, at the end of the first quarter.

In summary, 2012 was a good year. We made strategic progress, grew recurring revenue, achieved our earnings targets and closed a number of significant sales, all which we believe will accelerate our internal revenue growth, earnings and cash flow. We are starting to see measurable impact from some of our investments and innovation, and are delivering more value to clients. We are also focused on the integration of Open Solutions, which should allow us to deliver new and enhanced value to their more than 3,300 clients. That, combined with the commitment of our more than 20,000 associates, is creating momentum, which should lead to strong results in 2013, and has lifted our confidence for 2014 and beyond.

This was a good quarter for Fiserv. The stock is currently down about 0.6% today.

-

WEX Inc. Drops on Weak Guidance

Eddy Elfenbein, February 6th, 2013 at 10:06 amBefore the opening bell, WEX Inc. ($WXS) reported fourth-quarter earnings of $1.07 per share. That was a penny below consensus. Quarterly revenue rose 20.9% to $169 million.

But the stock is getting smacked around this morning due to the company’s weak guidance. For Q1, WXS expects earnings to range between 89 cents and 96 cents per share. The Street had been expecting $1.08 per share. For all of 2013, WXS sees earnings between $4.30 and $4.50 per share. The Street was expecting $4.88 per share. For all of 2012, WXS made $4.06 per share which was a nice increase from $3.64 per share on 2011.

-

Morning News: February 6, 2013

Eddy Elfenbein, February 6th, 2013 at 6:33 amRBS Said to Face Up to $783 Million Libor Manipulation Fine

Dollar Rises vs. Yen on BOJ Governor’s Early Exit

Fed Confirms Hackers’ Breach of Website, Reuters Reports

Obama Urges Congress to Act to Stave Off Cuts

S&P Misled Investors On Bonds’ Risks, Suit Says

S&P Analyst Joked of Bringing Down the House Before Crash

Lenovo’s Diplomatic Response to Dell Buyout

Virgin Media Chief Attracts $16 Billion Buyout as Final Act

4 Reasons To Be Skeptical Of Zynga

UBS Owes Brazil $1.2 Billion Taxes For 2006-09

Google Said in Talks to Invest $50 Million in Vevo Site

Corporate Forces Endangered the Twinkie, but May Save It

Health Insurance Companies Get in Shape for 2014

Joshua Brown: T.I.N.A. (or the Seller’s Dilemma)

Edward Harrison: China’s Huge Demographic Challenges Have Already Begun

Be sure to follow me on Twitter.

-

AFLAC Earned $1.48 Per Share for Q4

Eddy Elfenbein, February 5th, 2013 at 7:24 pmAfter the closing bell, AFLAC ($AFL) reported Q4 operating earnings of $1.48 per share which matched Wall Street’s estimate. Three months ago, the company told us to expect earnings to range between $1.46 and $1.51 per share, so they were squarely in the ballpark.

A lot of people are concerned about the impact of the weaker yen on AFLAC’s bottom line. It turns out the yen dinged their earnings by four cents per share last quarter. It hurts, but it’s not that bad. On a currency neutral basis, earnings rose by 4.8% from a year ago.

For the full-year, operating earnings came in at $6.60 per share. The full-year earnings were actually boosted by a penny per share thanks to the yen/dollar rate. Earnings for the year rose by 5.1%.

As far as this year is concerned, CEO Daniel P. Amos said:

I want to reiterate that our objective for 2013 has not changed: To increase operating earnings per diluted share 4% to 7%, or approximately $6.86 to $7.06 per share, on a currency neutral basis. Therefore, if the yen/dollar exchange rate averages 90 yen for the full year, it’s likely operating earnings per diluted share will be $6.37 to $6.57 for 2013. I would point out that 2013 earnings comparisons to 2012 will be more difficult because earnings in 2012 were significantly better than we originally anticipated.

In the after-hours market, the stock is off about 1.6%.

Here’s a look at how much the yen has plunged over the last four months.

-

Fiserv Earned $1.39 Per Share for Q4

Eddy Elfenbein, February 5th, 2013 at 4:14 pmFor Q4, Fiserv ($FISV) earned $1.39 per share which matched Wall Street’s forecast.

Fiserv, Inc., a leading global provider of financial services technology solutions, today reported financial results for the fourth quarter and full year 2012.

GAAP revenue was $1.16 billion and adjusted revenue was $1.08 billion in the fourth quarter, both consistent with the fourth quarter of 2011. For the full year, GAAP revenue was $4.48 billion compared with $4.34 billion in 2011. Adjusted revenue was $4.20 billion compared with $4.07 billion in 2011, an increase of 3 percent.

GAAP earnings per share from continuing operations for the fourth quarter was $1.18 compared with $1.07 in 2011. GAAP earnings per share from continuing operations for the full year was $4.34 compared with $3.40, which included a loss from early debt extinguishment of $0.37 per share, in 2011.

Adjusted earnings per share from continuing operations in the fourth quarter increased 9 percent to $1.39 compared with $1.27 in the fourth quarter of 2011. Adjusted earnings per share from continuing operations for the year grew 12 percent to $5.13 compared with $4.58 in 2011.

“Our 2012 results were highlighted by our 27th consecutive year of double-digit adjusted earnings per share growth and meaningful strategic progress,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “We capped off a strong sales year with exceptional performance in the fourth quarter.”

This basically matches what Fiserv told us to expect three weeks ago. Fiserv earned $5.13 per share for the entire year. They expect growth of 15% to 18% for this year, and specified an earnings range of $5.88 to $6.07 per share. If that’s correct, then FISV is going for less than 14 times this year’s earnings.

-

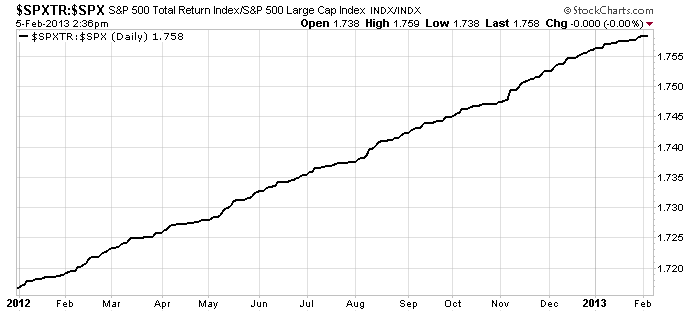

Total Return to Dividends

Eddy Elfenbein, February 5th, 2013 at 2:43 pmHere’s an interesting chart. This shows the S&P 500 Total Return Index divided by the S&P 500. In other words, this shows an investor’s return solely from dividends.

There seems to be a surge every three months (mid-May, mid-August, mid-November, and less so in February), when the bulk of dividends are paid out. You can also see that the fourth quarter was especially good for dividends as companies rushed to beat the taxman.

I think investors too often ignore dividends. Not only do you get money, but dividends are a good way to gauge a company’s health. It’s not fool-proof, but when a company raises its quarterly dividend, it’s often a sign of confidence that business is going well.

-

Walgreen Breaks $41

Eddy Elfenbein, February 5th, 2013 at 1:35 pmLast March, I tweeted:

$WAG is looking like a good value. Earnings are next week. Anyone else think it can be a $40 stock? $$

At the time, shares of Walgreen ($WAG) were at $33.56. This morning, the company reported strong sales for January thanks to flu season. The stock has been as high as $41.61 today which is a new 52-week high. The stock has done about three times better than the S&P 500.

-

Canada Fires Its Penny

Eddy Elfenbein, February 5th, 2013 at 12:33 pmFrom the Chicago Tribune

The Canadian government has begun to phase out the penny, saying it’s too expensive to produce the coin.

Besides its “excessive” production value, Canada has long cited the significant handling costs for the nation’s retailers and environmental considerations that lessen the penny’s worth. The country, which produced its last pennies on Monday, estimates the move will save taxpayers about $11 million a year.

The potential savings have enticed U.S. officials to consider the possibility as well.

Cash transactions in Canada will now be rounded to the nearest 5-cent mark. The penny’s retirement will have no effect on payments made by checks or credit cards.

For example, if the total price of coffee and a sandwich is $4.92, a customer that was paying in cash would owe $4.90, according to the Royal Canadian Mint. But those using another method of payment would pay $4.92, and the pennies would be tallied electronically.

The cost of the metal that goes into a penny has surged in recent years, making the coin’s production more expensive than its face value.

In the U.S., it now cost 2.41 cents to make every penny, which is made mostly of zinc. The penny has cost more than its face value since 2006.

Although the U.S. has conducted significant research into alternatives for the penny, the U.S. Mint says it still needs more research before it can make a decision to either change its composition or do away with it altogether.

Any new materials for the penny would need to simulate the current look and durability of the nation’s most circulated coin.

-

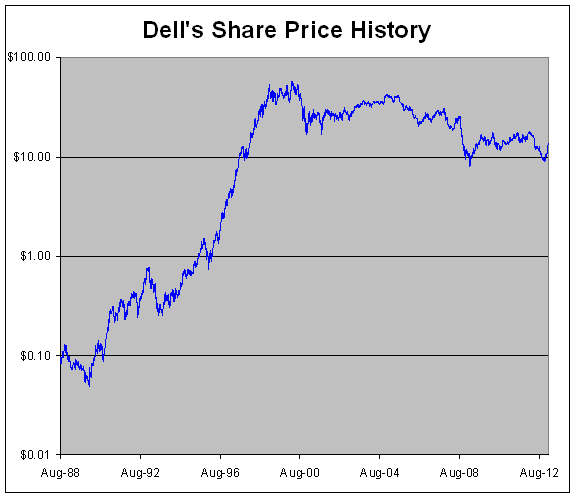

Dell to Go Private at $13.65

Eddy Elfenbein, February 5th, 2013 at 9:59 amIt’s official. Dell is going to be taken private. A group of investors led by Michael Dell will buy the entire firm for $13.65 per share. Interestingly, Microsoft will lend the buyout syndicate $2 billion for the deal.

Let’s look at some numbers: Dell’s IPO was on June 22, 1988 at $8.50. Since then, the stock has split 96-for-1 so that initial price works out to 8.85 cents per share. The buyout price is 154 times the IPO price. At one point in the late-1990s, shares of Dell split 2-for-1 three separate times in less than one year. At one point, Dell split 2-for-1 six times in just over 40 months.

Dell was actually not a screaming success as an IPO. The shares did indeed rally from the IPO price of $8.50 to a high of $12.50 by October 25, 1988 (or 13 cents adjusted for splits). But after that, Dell plunged to an all-time low of $4-5/8 by early 1990 (or 4.8 cents).

Then Dell put on one of the most remarkable runs in the history of capitalism. The shares skyrocketed to an all-time high close of $58.13 on March 22, 2000 ($59.69 intraday). During the decade of the 1990s, Dell advanced 890-fold which works out to 97% per year. Today’s buyout price is 77% below Dell’s high reached 13 years ago.

-

Legacy of Benjamin Graham

Eddy Elfenbein, February 5th, 2013 at 9:37 am

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His