Archive for 2013

-

Morning News: February 11, 2013

Eddy Elfenbein, February 11th, 2013 at 6:59 amEurope Threatened With The Slap Of Harsh Reality

Kuroda Says Additional BOJ Easing Can Be Justified for 2013

Putin Turns Black Gold to Bullion as Russia Outbuys World

G-7 Said to Discuss Statement to Calm Currency War Concern

U.S. Soy Supply at 48-Year Low as Brazil Ships Held

Investor Aims High With Price For Dell

American and US Airways May Announce a Merger This Week

Hakon Agrees to Buy ICA Stake From Ahold for $3.1 Billion

Samsung Emerges as a Potent Rival to Apple’s Cool

Novo Nordisk Hit Hard As U.S. Rebuffs Insulin Drug

Disruptions: Where Apple and Dick Tracy May Converge

Rating Victims Didn’t Know S&P’s Toxic AAA Born of Greed

Complex Investments Prove Risky as Savers Chase Bigger Payoff

Credit Writedowns: Inflationary Pressure In Brazil Is Building

Epicurean Dealmaker: Skin in Which Game?

Be sure to follow me on Twitter.

-

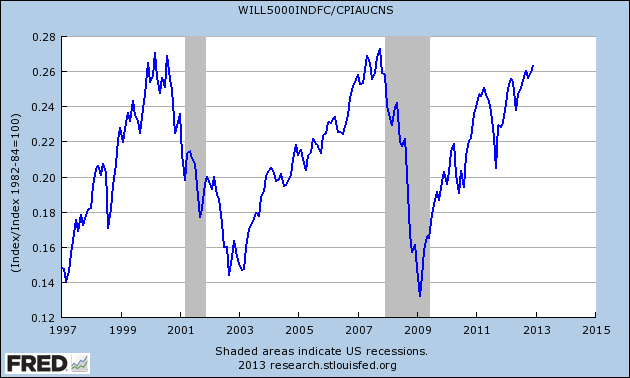

Stock Market At Inflation-Adjusted All-Time High

Eddy Elfenbein, February 8th, 2013 at 4:53 pmI can’t be absolutely certain of this but I’m reasonably confident in reporting that the total real return of the U.S. stock finally reached an all-time high today. By this, I mean adjusting for dividends and inflation, we took out the old peak from 13 years ago.

Note: The above chart goes to the end of 2012.

Here are some numbers: The Wilshire 5000 Total Return Index has increased by 35.41% from March 24, 2000 to today. Meanwhile, the CPI has increased by 34.1% from March 2000 through December 2012. The numbers for January won’t come out until later this month. Despite this, it would be a noticeable break from the recent trend for the January CPI to knock out the small lead that stocks appear to enjoy.So raise a glass to stocks. It only took 13 years to make a real profit. A very, very, very, very small (but real) profit.

-

CWS Market Review – February 8, 2013

Eddy Elfenbein, February 8th, 2013 at 8:12 amThat money talks I’ll not deny,

I heard it once: It said, “Goodbye.”

-Richard ArmourLast Friday, the Dow pierced 14,000 for the first time in five years. But as I suspected, investors got a case of the jitters, and the Dow hasn’t been able to hold 14,000. We even had a small uptick in volatility as the S&P 500 had three straight moves of greater than 1%. One money manager said, “We’ve moved so far so fast that the market’s just looking for any kind of sign to take something off the table.” I think that’s exactly right.

Wall Street is still focused on earnings. While fourth-quarter earnings season has been good (not great), I’m starting to have concerns that Wall Street’s earnings outlook is too optimistic. According to the Street, earnings growth will accelerate, meaning the pace of growth itself will increase, throughout 2013. That’s certainly possible, but I see that as a best-case scenario. More likely, earnings growth will flat-line or grow rather modestly.

That’s not necessarily awful news. Corporate America has been raking it in lately. The companies in the S&P 500 will probably net a cool $1 trillion this year. But we have to face the fact that the easy money in this bull market has already been made. Stocks have more than doubled in less than four years. The next four years won’t be so fortunate.

That’s why I urge all investors to focus on high-quality stocks for the long term like the stocks on our Buy List. We had more good news this week, including a 21% dividend increase from Ross Stores ($ROST), and JPMorgan ($JPM) reached yet another 52-week high. Now let’s look at some of our earnings reports this week.

AFLAC Is a Buy up to $54 per Share

After the close on Tuesday, AFLAC ($AFL) reported fourth-quarter earnings of $1.48 per share. Make no mistake: this was a solid quarter for the duck stock, and it was squarely in line with what they told us to expect. Three months ago, AFLAC said Q4 EPS should range between $1.46 and $1.51.

But here’s the issue for us: Since most of AFLAC’s business comes from Japan, their bottom line can be adversely impacted (or helped) by fluctuations in the yen/dollar exchange rate. Lately, the government in Japan has aggressively stated its intention of pursuing a pro-inflation policy. That’s caused the yen to tank against the dollar. In response, the Nikkei Index has soared.

As I said, AFLAC as a business is fine and dandy and as strong as it’s ever been. I want to make it clear that I’m not overly worried about the exchange rate, but I have to say that it’s an issue for investors. AFLAC said the falling yen cost dinged their Q4 by four cents per share. Not fun, but not a disaster either. Bear in mind that AFLAC’s full-year earnings for 2012 were actually helped by one penny per share, thanks to the exchange rate. So it works in both directions.

For all of 2012, AFLAC made $6.60 per share in operating earnings. The company said it sees operating earnings growth of 4% to 7% for this year. On a currency-neutral basis, that means operating earnings of $6.86 to $7.06 per share.

Now here’s the tricky part (warning: math ahead). Each move in the exchange rate of one yen from 78.5 will cost AFLAC 4.3 cents per share for the year. So if the exchange rate averages 90 for the entire year, that will cost AFLAC 49.45 cents per share (11.5 times 4.3). That stings, but it’s roughly 50 cents per share out of $7 of earnings. It’s not enough for me to change my opinion that AFLAC is a very solid stock to own. And of course, I have no idea what the exchange rate will do this year. However, I suspect that most of the damage to the yen has already been done.

Shares of AFL pulled back after the earnings report, but the stock is basically where it was three months ago. AFLAC remains an excellent company. Due to the recent pullback, I’m going to lower my Buy Below to $54 per share.

Good News from FISV and CTSH, Bad News from WXS

Also on Tuesday, Fiserv ($FISV) reported Q4 earnings of $1.39 per share, which exactly matched Wall Street’s forecast. The company already told us that this was going to be a good quarter. Remarkably, this is Fiserv’s 27th-straight year of double-digit earnings growth. There aren’t many companies that can boost a record like that.

For 2012, Fiserv earned $5.13 per share, which is a very nice increase over the $4.58 per share they made in 2011. Fiserv said that they expect growth of 15% to 18% for this year, and they specified an earnings range of $5.88 to $6.07 per share. If that’s correct, FISV is going for less than 14 times this year’s earnings. This is a solid stock. Fiserv is a buy up to $88 per share.

We had a great earnings report from Cognizant Technology Solutions ($CTSH) on Thursday. The company reported Q4 earnings of 99 cents per share, which is up from 84 cents for Q4 of 2011. That’s eight cents more than the Street had been expecting. Quarterly revenue rose 17.1% to $1.95 billion. For all of 2012, revenue rose 20% to $7.35 billion, and earnings-per-share increased from $3.07 in 2011 to $3.70 for 2012. This is clearly a rapidly-growing outfit.

Cognizant also offered very impressive guidance for Q1 and all of 2013. The company sees Q1 revenue rising by 20% to “at least” $2 billion and expects earnings-per-share to hit $1.01. Wall Street had been expecting 93 cents per share. For the whole year, CTSH sees revenue climbing to “at least” $8.6 billion. That’s an increase of 17%. Cognizant also sees earnings-per-share of at least $4.31. That’s a big increase over Wall Street’s expectation of $4.00 per share. CTSH is an excellent buy anytime you see it below $81.

Our dud this week came from WEX Inc. ($WXS). The company reported fourth-quarter earnings of $1.07 per share, which was a penny below consensus. Quarterly revenue rose 20.9% to $169 million.

But the earnings weren’t the bad part; it was the guidance. For Q1, WXS expects earnings to range between 89 cents and 96 cents per share. The Street had been expecting $1.08 per share. For all of 2013, WXS sees earnings between $4.30 and $4.50 per share. The Street was expecting $4.88 per share. For all of 2012, WXS made $4.06 per share which was a nice increase from $3.64 per share on 2011.

Frankly, this guidance is very disappointing news. I’m not ready to toss in the towel with WXS; the stock has been a huge winner for us over the last eight months. But for now, I’m going to lower the Buy Below price to $72.

Ross Stores Is a Buy up to $62

Ross Stores ($ROST) gave us great news this week. The retailer reported blowout sales for January, and thanks to the rush of business, Ross sees Q4 earnings coming in at $1.06 to $1.07 per share, and $3.52 to $3.53 per share for the entire year. (Note that like a lot of retailers, Ross ends their fiscal year at the end of January.) The earnings report should be out in mid-March.

But the best news is that Ross raised their quarterly dividend from 14 cents to 17 cents per share. That’s a 21% hike. Ross pays out a very small amount of their profits as dividends to shareholders (about 20%). Based on Thursday’s closing price, Ross yields 1.13%. That’s obviously not a very high yield, but the dividend increase and strong sales news are a good omen for Ross Stores. ROST remains a very good buy up to $62.

Before I go, I want to highlight two Buy List stocks that look especially attractive. Again, Microsoft ($MSFT) looks very good here. The pullback in Harris ($HRS) seems about done. Shares of HRS got hit hard for a modest decrease in guidance.

That’s all for now. Next week, we get important reports on retail sales and industrial production. Our final earnings report of this cycle will be from DirecTV ($DTV) on Wednesday, February 13th. Wall Street expects $1.13 per share. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: February 8, 2013

Eddy Elfenbein, February 8th, 2013 at 7:10 amChina Trade Growth Hints At Strong 2013

European Leaders Struggle to Bridge Budget Gaps

Aso Says Pace of Yen Decline Too Fast With G-20 Set to Meet

Draghi’s Powerful Weapon Is Words as Euro Heeds His Voice

German Exports Rose in December to Cap Trillion-Euro Year

4 Years After Crisis, Ireland Strikes Deal to Ease a Huge Debt Load

Gold Sideways in Asia as Outlook Unclear; Precious Metals Lower

Worker Productivity in U.S. Declines, Pushing Up Labor Costs

Business and Labor Unite to Try to Alter Immigration Laws

Apple With $137 Billion in Cash Considers Preferred Stock

Hewlett Directs Its Suppliers in China to Limit Student Labor

BMW Posts Record Group Sales In January, Up 9.9 Percent

Google Suit Against IRS Planned Over Domestic Tax Dispute

Roger Nusbaum: Position Management

Be sure to follow me on Twitter.

-

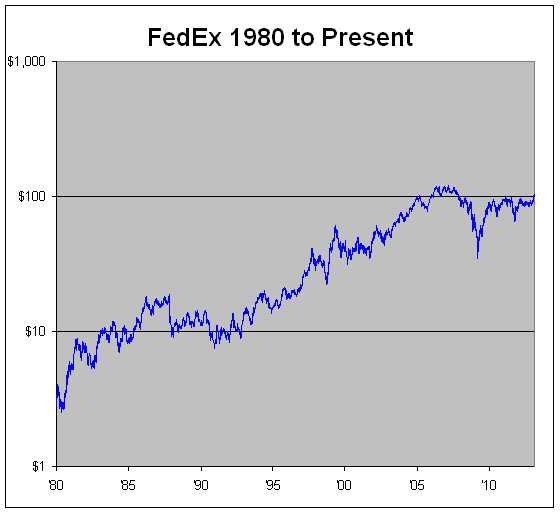

FedEx +4,147%

Eddy Elfenbein, February 7th, 2013 at 1:37 pmThe U.S. Post Office just announced major cutting measures including the ending of Saturday service. Last year, the USPS lost $15.9 billion.

As a comparison, I think it’s interesting that FedEx ($FDX) just hit a new five-year high today. From May 6, 1980 to yesterday’s close, shares of FDX are up 4,147%. That would turn a $25,000 investment into over $1 million.

-

Cognizant Guides Higher for 2013

Eddy Elfenbein, February 7th, 2013 at 10:49 amBefore the opening bell, Cognizant Technology Solutions ($CTSH) reported Q4 earnings of 99 cents per share which is up from 84 cents for Q4 of 2011. That’s eight cents more than the Street had been expecting. Quarterly revenue rose 17.1% to $1.95 billion. For all of 2012, revenue rose 20% to $7.35 billion, and earnings-per-share increased from $3.07 in 2011 to $3.70 for 2012. As you can see, this is a rapidly-growing outfit.

Cognizant also offered very strong guidance for Q1 and all of 2013. The company sees Q1 revenue rising by 20% to “at least” $2 billion and earnings-per-share hitting $1.01. Wall Street had been expecting 93 cents per share. For the whole year, CTSH sees revenue climbing to “at least” $8.6 billion. That’s an increase of 17%. Cognizant also sees earnings-per-share of at least $4.31. The Street had been expecting $4.00 per share.

-

Ross Stores Hikes Dividend 21%

Eddy Elfenbein, February 7th, 2013 at 9:57 amGood news this morning from Ross Stores ($ROST). The company reported blowout sales for January. Thanks to the rush of business, the company sees Q4 earnings coming in at $1.06 to $1.07 per share, and that’s $3.52 to $3.53 per share for the entire year. (Note that like a lot of retailers, Ross ends their fiscal year at the end of January.) The earnings report should be out in mid-March.

Best of all, Ross is raising the quarterly dividend from 14 cents to 17 cents per share. That’s a 21% hike. Ross pays out a very small amount of their profits as dividends to shareholders (about 20%). Based on yesterday’s close, Ross yields 1.15%. That’s obviously not a very high yield but the dividend increase and strong sales news is a good omen for Ross Stores.

-

Morning News: February 7, 2013

Eddy Elfenbein, February 7th, 2013 at 7:31 amEuro Gains on Speculation Draghi to Signal Optimism; Pound Rises

Carney Backs Flexible Inflation Targeting in BOE Testimony

Ireland Increasingly Hopeful of ECB Agreement

Royal Bank of Scotland Settles Case on Rigging

Harvard’s Gopinath Helps France Beat Euro Straitjacket

Trying to Stem Losses, Post Office Seeks to End Saturday Letter Delivery

Credit Suisse Posts Quarterly Profit, Raises Cost-Cutting Goal

Liberty’s Bid for Virgin Media Pushes the Envelope on Debt

Platinum Advances to 16-Month High on Supply Woes; Gold Climbs

Google To Buy ICG Group Unit For $125 Million

TransCanada Looks East Amid Keystone Pipeline Delay

Vodafone Misses Estimates As Sales In Europe Drop

Alcatel-Lucent Chief Resigns as Company Posts Loss

Cullen Roche: Some Brief Thoughts on the CBO’s New Budget Projections

Jeff Carter: The Trusted Network

Be sure to follow me on Twitter.

-

AFLAC’s 2013 Outlook

Eddy Elfenbein, February 6th, 2013 at 1:31 pmFrom the earnings call, here’s AFLAC‘s ($AFL) outlook for this year (I think Seeking Alpha’s transcription is rather muffled, but you can follow what they’re saying):

Lastly, let me comment on the earnings outlook for 2013. As you’ve heard Dan say, we’ve affirmed our guidance for 2013 of 4% to 7% increase in operating earnings per diluted share, excluding the impact of the yen. To understand the significant our 2013 EPS objective over 2012 actual results winning to this perspective for you.

In 2012, we received tax benefit from our tax exempt for the years 2008 and 2009, and we’ve made a revision for the full year impact of tax effective tax rate. The unusual benefits received in 2012 totaled approximately $38 or $0.08 per share. We also recovered a previously written-off coupon as part of the sales transaction executed during the year that resulted in a one-time benefit to operating earnings of $23 million, or $0.05 per share. If you exclude the impact of these benefits from the 2012 operating earnings note, operating earnings per diluted share in sale would have been $6.47.

This year we estimate that a one yen move on the average annual exchange rate will equal approximately $4.3 for diluted share. Considering the weakening of the yen in recent months, if we achieve our objective of 4% to 7% increase in operating earnings per diluted share for the year at yen averages 90 for the full year, we would expect operating EPS to be in the range of $6.37 to $6.57 per diluted share.

The yen is currently at 93.345 to the dollar.

-

Morgan Housel’s Startling Facts About the Economy

Eddy Elfenbein, February 6th, 2013 at 12:36 pmMorgan Housel of the Motley Fool comprised a great list of “100 Startling Facts About the Economy.” I’m tempted to list them all, but I’ve culled some of my favorites:

14. Including dividends, the S&P 500 gained 135% from March 2009 through January 2013, during what people remember as the “Great Recession.” It gained the exact same amount from 1996 to 2000, during what people remember as the “greatest bull market in history.”

19. From 2006 to 2011, Hewlett-Packard ($HPQ) spent $51 billion on share repurchases at an average price of $40.80 per share. Shares currently trade at $16.50.

21. Despite the overall population doubling, more babies were born in the U.S. in 1956 than were born in 2009, 2010, or 2011.

27. According to Bloomberg, “The 50 stocks in the S&P 500 with the lowest analyst ratings at the end of 2011 posted an average return of 23 percent [in 2012], outperforming the index by 7 percentage points.”

29. Thanks in large part to cellphone cameras, “Ten percent of all of the photographs made in the entire history of photography were made last year,” according to Time.

32. Fortune magazine published an article titled “10 Stocks To Last the Decade” in August, 2000. By December 2012, the portfolio had lost 74.3% of its value, according to analyst Barry Ritholtz.

44. According to California Common Sense, “Over the last 30 years, the number of people California incarcerates grew more than eight times faster than the general population.”

45. One in seven crimes committed in New York City now involves an Apple product being stolen, according to NYPD records cited by ABC News.

49. According to the Center for Economic and Policy Research, 44% of those working for minimum wage in 2010 had attended at least some college, up from 25% in 1979.

60. The International Energy Agency predicts that the U.S. will become the world’s largest oil-producer by 2020, overtaking Saudi Arabia.

62. According to BetterInvesting, the number of investment clubs has declined by 90% since 1998 from 400,000 to 39,000.

67. During the Federal Reserve’s June 2007 policy meeting, the word “recession” was used three times; the word “strong” was used 61 times. The economy entered recession six months later.

68. Last year, Franklin Templeton asked 1,000 investors whether the S&P 500 went up or down in 2009 and 2010. Sixty-six percent thought it went down in 2009, while 48% said it declined in 2010. In reality, the index gained 26.5% in 2009 and 15.1% in 2010.

71. According to a survey by Paola Sapienza and Luigi Zingales, effectively all economists agreed that stock prices are hard to predict. Only 59% of average Americans felt the same way.

79. Related: 84% of actively managed U.S. stock funds underperformed the S&P 500 in 2011.

80. According to The Wall Street Journal, 49.1% of Americans live in a household “where at least one member received some type of government benefit in the first quarter of 2011.”

85. The U.S. birthrate declined 8% from 2007 to 2010, according to Pew. At 63.2 per 1,000 women of childbearing age, the 2011 U.S. birthrate was the lowest since records began in 1920.

86. According to Wired magazine, “In a 2006 survey, 30 percent of people without a high school degree said that playing the lottery was a wealth-building strategy…On average, households that make less than $12,400 a year spend 5 percent of their income on lotteries.”

88. We are used to hearing how much faster the earnings of the top 1% grow compared with everyone else’s, but we often forget that it used to be the other way around. From 1943 to 1980, the annual incomes of the bottom 90% of Americans doubled in real terms, while the average income of the top 1% grew just 23%, according to Robert Frank.

92. Federal nondefense discretionary spending — all spending minus defense and entitlements — is on track to hit its lowest level as a share of GDP in more than 50 years, according to data from the Congressional Budget Office.

94. According to The Economist, “Over the past ten years, hedge-fund managers have underperformed not just the stock market, but inflation as well.”

95. According to Bloomberg, “Americans have missed out on almost $200 billion of stock gains as they drained money from the market in the past four years, haunted by the financial crisis.

98. “More than 50 million Americans couldn’t afford to buy food at some point in 2011,” writes CNNMoney, citing U.S. Department of Agriculture data. In June 2012, 46.7 million Americans received food stamps.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}