Archive for 2013

-

ADP Jobs Report: +192K

Eddy Elfenbein, January 30th, 2013 at 2:39 pmThe big jobs report is this Friday. The last few initial claims reports have been quite good. Another positive omen was today’s jobs report from ADP, the private payroll firm. According to ADP, 192,000 private sectors jobs were created last month. Wall Street had been expecting 175,000.

Small businesses led the way, hiring 115,000 workers. Medium-sized businesses added 79,000 jobs, while large firms cut 2,000 positions.

“That’s a good solid number,” said Mark Zandi, chief economist for Moody’s Analytics, which works with ADP on the report. “The job growth is broad-based, across may industries.”

Most jobs were created in the service sector, which added 177,000 positions. The goods producing sector added 15,000. Bright spots included construction, trade, and professional services. The manufacturing sector lost 3,000 jobs.

-

Today’s Fed Statement

Eddy Elfenbein, January 30th, 2013 at 2:20 pmInformation received since the Federal Open Market Committee met in December suggests that growth in economic activity paused in recent months, in large part because of weather-related disruptions and other transitory factors. Employment has continued to expand at a moderate pace but the unemployment rate remains elevated. Household spending and business fixed investment advanced, and the housing sector has shown further improvement. Inflation has been running somewhat below the Committee’s longer-run objective, apart from temporary variations that largely reflect fluctuations in energy prices. Longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic growth will proceed at a moderate pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. Although strains in global financial markets have eased somewhat, the Committee continues to see downside risks to the economic outlook. The Committee also anticipates that inflation over the medium term likely will run at or below its 2 percent objective.

To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee will continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.

The Committee will closely monitor incoming information on economic and financial developments in coming months. If the outlook for the labor market does not improve substantially, the Committee will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until such improvement is achieved in a context of price stability. In determining the size, pace, and composition of its asset purchases, the Committee will, as always, take appropriate account of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Charles L. Evans; Jerome H. Powell; Sarah Bloom Raskin; Eric S. Rosengren; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen. Voting against the action was Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.

-

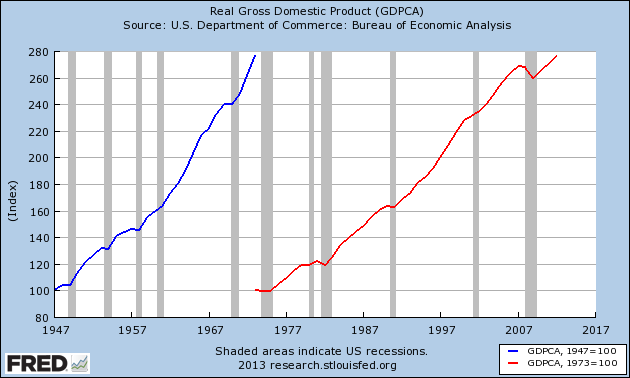

The U.S. Economy Grew Less in the Last 39 Years Than in the 26 Years Before That

Eddy Elfenbein, January 30th, 2013 at 9:21 amEarlier this morning, I tweeted out a fact that got a lot of attention so I wanted to flesh it out a bit more.

The US economy grew more in real terms from 1947 to 1973 than from 1973 to 2012. That’s 26 years compared with 39 years, exactly 50% longer.

The total growth was almost exactly the same, but the earlier, and shorter, period won by a nose. To be specific, the U.S. economy grew by 176.84% from 1947 to 1973, and 176.60% from 1973 to 2012. Here’s the data source at the FRED database.

The U.S. economy also grew less over the last 12 years than in the five years prior to that. Over the last 20 quarters (five years), real GDP has grown by 2.41%. Historically, the economy should grow around 16% to 17% over a five-year stretch.

-

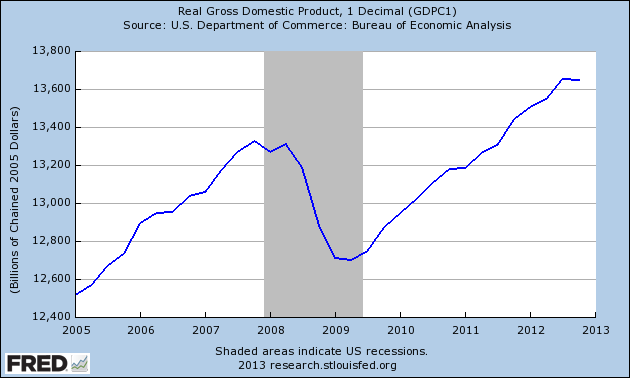

Q4 GDP = -0.1%

Eddy Elfenbein, January 30th, 2013 at 9:06 amA few moments before today’s GDP report, I tweeted that if the number is negative, Twitter would go into complete melt down mode. I was only kidding, but the GDP number was in fact negative. Well, -0.1%. And it was Rick Santelli, CNBC’s in-house scare-monger, that melted down.

As odd as this may sound, the GDP report truly wasn’t that bad. There was a big drop off in military spending. There was also a decline in inventory build-ups which is hardly a bad thing. The numbers “under the hood” were rather decent:

Real personal consumption expenditures increased 2.2 percent in the fourth quarter, compared with an increase of 1.6 percent in the third. Durable goods increased 13.9 percent, compared with an increase of 8.9 percent. Nondurable goods increased 0.4 percent, compared with an increase of 1.2 percent. Services increased 0.9 percent, compared with an increase of 0.6 percent.

Real nonresidential fixed investment increased 8.4 percent in the fourth quarter, in contrast to a decrease of 1.8 percent in the third. Nonresidential structures decreased 1.1 percent; it was unchanged in the third quarter. Equipment and software increased 12.4 percent in the fourth quarter, in contrast to a decrease of 2.6 percent in the third. Real residential fixed investment increased 15.3 percent, compared with an increase of 13.5 percent.

-

Morning News: January 30, 2013

Eddy Elfenbein, January 30th, 2013 at 6:51 amDeutsche Bank Seen Missing Goldman-Led Gains on Cost Rise

Santander’s Capital in Focus as Spain Property Purge Ends

Japan Has Changed The Game, And Now There Really Could Be A Currency War

Consumer Confidence in U.S. Falls to Lowest Level Since 2011

TARP Watchdog Spars With Treasury on Ally Financial Exit

Breuer Leaves Justice Department With Shift in Tactics

Analysts See the Good in Amazon’s Poor Results

UPS’s Dropped TNT Acquisition Is Formally Blocked by EU

Roche Boosted By Robust US Sales

LG Electronics Posts Loss After EU Fine

Canon Sees Profit Growth on Weaker Yen

Joshua Brown: Business Lessons From The Beatles

Phil Pearlman: Research In Motion: The Phone’s The Thing

Be sure to follow me on Twitter.

-

Rotten Day for our Buy List

Eddy Elfenbein, January 29th, 2013 at 4:53 pmI always try to upfront about the performance of our Buy List. There are a lot of sketchy characters on the Internet, so I want to be as transparant as possible. Fortunately, we’ve done well over the years so there’s been a lot of celebrating. But there are bad days, too, and today was one.

For the day, our Buy List dropped 0.34% while the S&P 500 gained 0.51%. Ouch, that stings. The good news is that we’re still ahead of the index for the year.

The culprits are easy to spot. Ford fell by 4.64% and Harris lost 4.39%. Our Buy List is very well-diversified so we can often shake off one stock having a bad day, but two weaklings is tough. Outside Ford and Harris, we were only modestly behind the S&P 500 today.

What’s more important to me is that I thought both earnings reports were quite good. I like Ford a lot. While Harris’ lower guidance was troubling, the shares are still going for less than 10 times forward earnings. I expect both stocks to rebound soon.

Today’s lesson: Not every day is a winner for us, but we’re still focused on the long-term.

-

The Market Isn’t Rallying, the Fear Premium Is Fading

Eddy Elfenbein, January 29th, 2013 at 10:56 amThe U.S. stock market isn’t rallying so much as the fear premium is slowly fading away. The net effect, of course, is the same: rising share prices. But bear in mind what’s going on under the hood; earnings estimates for 2013 are lower than they were several months ago. The Street currently expects the S&P 500 to earn about $112 this year. In April, it was close to $119.

So why are investors willing to pay more for less? Multiples are driven by sentiment, and the widespread fear that plagued the market is melting away. Let’s look at the performance of stocks versus bonds. From mid-2011 to mid-2012, bonds (especially secure U.S. Treasury bonds) soared. Stocks are only beginning to play catch up.

Remember last year how everyone was watching what was happening in the Spanish or Italian bond market? Not so anymore. The guys at Bespoke note that European spreads are near 52-week lows.

The Spanish and Italian stock markets are also rebounding after severe losses.

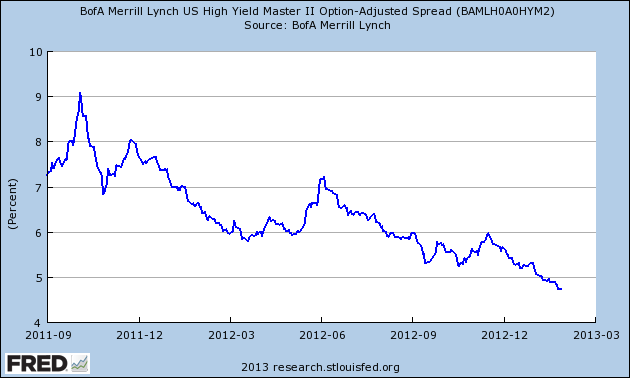

Junk bond spreads are plummeting.

As sentiment returns to normal, volatility is fading away as well.

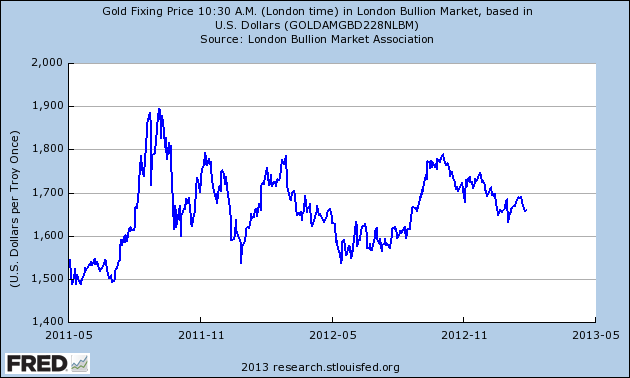

Even gold, which had been a big winner for so long, hasn’t been able to make a new high in nearly 18 months.

-

Harris Beats But Lowers Full-Year Guidance

Eddy Elfenbein, January 29th, 2013 at 10:26 amBesides Ford Motor ($F), we had another Buy List earnings report this morning. Harris Corp. ($HRS), the communications equipment company, reported earnings of $1.25 per share for the December quarter which is the company’s fiscal second quarter. The consensus on Wall Street was for earnings of $1.20 per share. Revenue dropped from $1.31 billion to $1.29 billion.

While these results were good, the news that has me concerned is that Harris lowered its full-year guidance. Before, the company saw earnings ranging between $5.10 and $5.30 per share. Harris lowered that range by 10 cents at both ends. The company now sees earnings ranging between $5 and $5.20 per share. Harris sees revenue dropping by 2% to 4%. The previous range was flat to negative 2%. The company blamed the lower guidance on “slower government spending resulting from growing budget uncertainty.”

Shares of Harris are currently down about 2.2% today.

-

Ford Motor Beats Earnings for Q4

Eddy Elfenbein, January 29th, 2013 at 9:01 amFord Motor ($F) posted strong quarterly results this morning. For Q4, the company earned 31 cents per share, which was six cents per share more than expectations. Ford earned 20 cents per share during Q4 of 2011.

Quarterly revenue rose from $32.6 billion to $34.5 billion. Wall Street had been expecting $32.94 billion. In terms of net earnings, Ford earned $1.59 billion last quarter compared with $1.03 billion the year before. For the entire year, Ford raked in $5.66 billion on revenue of $134.3 billion.

The equation continues to be the same: they’re doing well in North America, but not so well in Europe. During 2012, Ford lost $1.75 billion in Europe. To give you an idea of how rough that is, they only lost $27 million there in 2011. In fact, the company said today that it’s expecting to lose $2 billion in Europe this year. Previously Ford had said they expected the same loss for this year as they had last year. Pre-tax earnings in North America rose 110%.

The New York Times described Ford’s Q4 as a “microcosm of Ford’s recent overall performance.” That’s a nice way of putting it. Alan Mulally, the head honcho, said, “We are well positioned for another strong year in 2013, as we continue our plan to serve customers in all markets around the world with a full family of vehicles.”

As bleak as things look in Europe, I like the steps that Ford is taking there. They’re being very aggressive, and they’re way ahead of GM. Basically, Ford is doing in Europe today what they did in North America a few years ago. Namely, restructure, reorganize and streamline operations. It’s painful in the short-term as we’re seeing in Europe today. But it’s very profitable in the long-term as we can see in Ford’s North American results today.

The stock looks to pull back a little today. Don’t be alarmed. Ford continues to do very well.

-

Morning News: January 29, 2013

Eddy Elfenbein, January 29th, 2013 at 6:37 amIn Japan, Dreamliner Woes Test Cozy Corporate Ties

Economists React: Reserve Bank of India Cuts Key Policy Rate

Royal Bank of Scotland Bonuses Spell Trouble For Osborne

Monti Minister to Defend Paschi Bailout After Hidden Losses

Iceland Wins Case On Deposit Guarantees

Bernanke Seen Buying $1.14 Trillion in Assets in 2014

Durable-Goods Demand Points to U.S. Factory Pickup

The Chief of Yahoo Lifts Sales, and Spirits

Caterpillar Chief Faults China Unit

Philips Exits Consumer Electronics

Little Debbie Maker to Buy Drake’s Brand, Hostess Says

As Music Streaming Grows, Royalties Slow to a Trickle

Jeff Miller: Weighing the Week Ahead: Will the Average Investor Take the Plunge?

Howard Lindzon: What Could go Wrong? …And Is Apple Still Leading The Market

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His